Introduction

Content Creator Economy Statistics: The content creator economy is fundamentally rewriting the rules of traditional media, entrepreneurship, and digital commerce. It has become a global industry where the most powerful assets are a loyal audience, money, and engaging content.

The continuous, rapid growth of the content creator economy is driven by both democratized creation tools and a worldwide change in consumer behavior toward niche, personalized, and subscription-based digital content.

Staying on top of these statistics is a vital thing for creators who want to build a scalable business model in this hyper-competitive, algorithm-driven platform, so stay with us to get an in-depth analysis of content creator economy statistics and learn how to make use of it. Let’s get started.

Editor’s Choice

- According to Market.us, the Global Creator Economy Market is projected to reach USD 1,072.8 billion by 2034, increasing from USD 149.4 billion in 2024.

- The market is estimated to grow at a compound annual growth rate (CAGR) of 21.8% from 2025 to 2034.

- In 2024, North America held the leading position, accounting for more than 37.4% of the global market share.

- Within this region, the United States recorded a strong valuation of USD 50.9 billion, highlighting its major contribution to the overall market growth.

- The segment of Influencers & Social Media Personalities holds the largest financial share, capturing over 8% of the entire market in 2024.

- Entertainment Content is the undisputed leading content segment, securing over 7% of the total revenue in 2024.

- Video-Based Platforms are central to the ecosystem, capturing over 5% of the market share in 2024, emphasizing the crucial role of video formats.

- There are an estimated 208 million content creators across the world.

- The vast majority, approximately 67% of creators, fall into the smaller follower tiers (1,000 to 10,000 followers), establishing the “micro-creator” as the most common figure.

- A significant 58% of creators maintain a separate full-time job, indicating that for most, content creation is a substantial side hustle rather than a sole profession.

- Millennials (aged 29 to 44) currently represent the largest generation in the economy, making up an estimated 41% of the total creator population.

- A substantial 48% of all surveyed creators reported making less than $15,000 annually from their content, underscoring the high barrier to a full-time income.

- The top 10% of earners on a major video platform collectively generated over $171 million in a single year, with their average annual income reaching an impressive $582,000 per creator.

- Subscription-based models generate the highest average annual revenue for top-performing creators at $94,731, proving the value of direct fan support.

- Brand partnerships and sponsored content remain the most common single source of income, with over 82% of US creators using this method.

- Fitness creators report the highest average monthly earnings on video platforms at approximately $11,939.

- YouTube hosts an astronomical base of over 69 million content creators worldwide.

- The average daily time spent by a user on TikTok is approximately 32 minutes, a highly competitive engagement rate.

- Patreon has paid out a cumulative total of over $3.5 billion to its creators to date via the direct fan-support model.

- 5% of content creators report already utilizing AI tools for at least one task in their creation process.

- Decentralised creator platforms are offering creators an increased share of their revenue, allowing them to retain anywhere from 90% to 100% of their profits.

- Long-form videos exceeding 30 minutes have experienced an explosive growth of over 11,000% in the past decade, making them the fastest-growing video segment.

- 59% of Gen Z viewers use short-form video applications to first discover content, which they then transition to watching the longer, more in-depth versions of on other platforms.

- Audience engagement with interactive content is significantly higher, commanding 53% more engagement compared to passive, static content.

- 60% of creators’ total revenue comes from international subscribers, highlighting the global scale and borderless nature of the business.

General Content Creator Economy Statistics

- The content creator community has grown rapidly since 2020, with millions turning personal interests into online brands and communities.

- There are over 64 million YouTube creators around the world.

- More than 165 million people have become social media content creators since 2020.

- Around 6 in 10 creators work full-time jobs while creating content.

- About 2 in 10 creators run their own content-based businesses.

- There are over 1 million TikTok creators globally.

- Nearly 35% of creators have been active for 3 to 5 years.

- Millennials make up the largest group of creators, while Gen Z participation continues to grow.

- Content creation has shifted from a small hobby to a real career option for young people.

- Around 63% of part-time creators plan to go full-time within 2 to 3 years.

- About 42% of creators already treat content creation as their full-time job.

- Nearly 61% of video creators believe their profession is more accepted today.

- Around 95% of creators say their offline friends and family know about their online work.

- More than 60% of video creators earn their living through content creation.

- About 63% of creators have no backup plan if their career fails.

- Around 45% of full-time creators depend on content creation as their main household income.

- The number of people identifying as “content creators” continues to rise.

- Around 97% of brands describe creators as influencers.

- About 86% of creators see themselves as entrepreneurs.

- Consumers trust relatable creators more, which influences how they find and buy products.

- Social shoppers are 54% more likely to buy from relatable creators than from aspirational ones at 39%.

- Around 56% of creators value creative freedom to stay authentic.

- Nearly 56% of consumers want brands to appear more relatable on social platforms.

- About 58% of consumers think ads in creator content blend naturally with other posts.

- Around 87% of consumers say content on topics that matter personally is important.

- Nearly 79% of consumers explore a brand after seeing it in creator content, and 70% talk about or share it.

- Around 76% of consumers say creator content helps them see how a product fits into daily life.

- About 75% say ads in creator videos increase product satisfaction.

- Around 62% of consumers are less likely to trust AI-generated content.

- About 74% of creators worry about deepfakes in AI.

- Nearly 56% have received brand requests to use generative AI, while 40% expect the same pay despite AI use.

- Around 71% of AI-using creators get positive audience feedback, mainly using AI for visual effects.

- Around 44% of advertisers plan to raise investment in creator content by 25% in 2024.

- About 90% of advertisers say it is easy to budget for creator content.

- Nearly 58% find creator content engaging for ads.

- Around 90% of media agencies can measure creator content performance effectively.

- Nearly 89% of advertisers feel positive about placing ads next to creator content.

- Creator posts drive 50% higher brand awareness than standard brand posts.

- About 87% of consumers find new brands through creator content.

- Around 34% dislike overly self-promotional social ads.

- Creator websites are seen as 67% more trustworthy, 57% more useful, and 56% more credible than social media pages.

- Brands shown on creator websites align 66% with readers’ lifestyles.

- Creator content increases purchase intent by 40%.

- Ads on creator videos perform 123% better in research, 130% better in advocacy, and 1.43× better in loyalty.

- Around 77% of creator fans feel connected to brands featured by their favorite creators.

- 70% of consumers make faster purchase decisions after creator ads, and 72% are likely to repurchase.

- Creators rely on multiple income streams like affiliate links, brand deals, and fan support.

- Around 98% earn from affiliate commissions, and 77% depend on brand deals.

- About 50% earn up to $5,000 per year, 17% make $30,000–$100,000, and 7% earn over $100,000.

- Around 70% of top video creators spend at least 4 hours daily creating.

- 49% of expert creators earn most from consulting, and 37% from book sales.

- The creator economy may reach $480 billion by 2027.

- Only 32% of creators are satisfied with their income, while 74% feel fairly paid.

- MrBeast reportedly earns $82 million, making him the highest-paid YouTuber.

- Full-time creators manage about 4 platforms, but only 1.9 generate revenue.

- Many full-time creators operate with just 4,000 total followers.

- Most creators enjoy their careers, and few regret the choice.

- About 75.5% of video creators experience stress or anxiety, but reduce it by outsourcing tasks.

- Only 25% of content shows a strong emotional impact, and 33% reaches high emotional scores.

- Around 1 in 2 influencers prefer social media activity over rest or exercise.

- Only 46% of work time is spent on creating; the rest goes to marketing and admin work.

- Audience growth has become difficult in the crowded market.

- 64% say building an audience is their biggest challenge.

- 45% of aspiring creators cite lack of time or knowledge as barriers.

- 95% believe brands should ask before using their content.

- 47% have had content used without permission, and 73% received no compensation.

- 65% were not credited, and 40% know others affected by the same issue.

- New tools and content formats are transforming creator work.

- 65% of video creators already use AI tools.

- Among AI users, 53% report better quality, 52% more creativity, and many save time.

- 45% of non-users avoid AI due to a lack of familiarity.

- Short-form video stays popular, especially on TikTok, Instagram Reels, and YouTube Shorts.

- Around 66% of creators on TikTok and Instagram prefer image posts, and 59% focus on videos.

- 67% use YouTube, 46% use Instagram, and 18% use TikTok as their main video platforms.

- Live streaming builds stronger communities through real-time interaction.

- Twitch and YouTube Live continue growing as popular live platforms.

- Twitch still has more than 7 million active streamers since 2020.

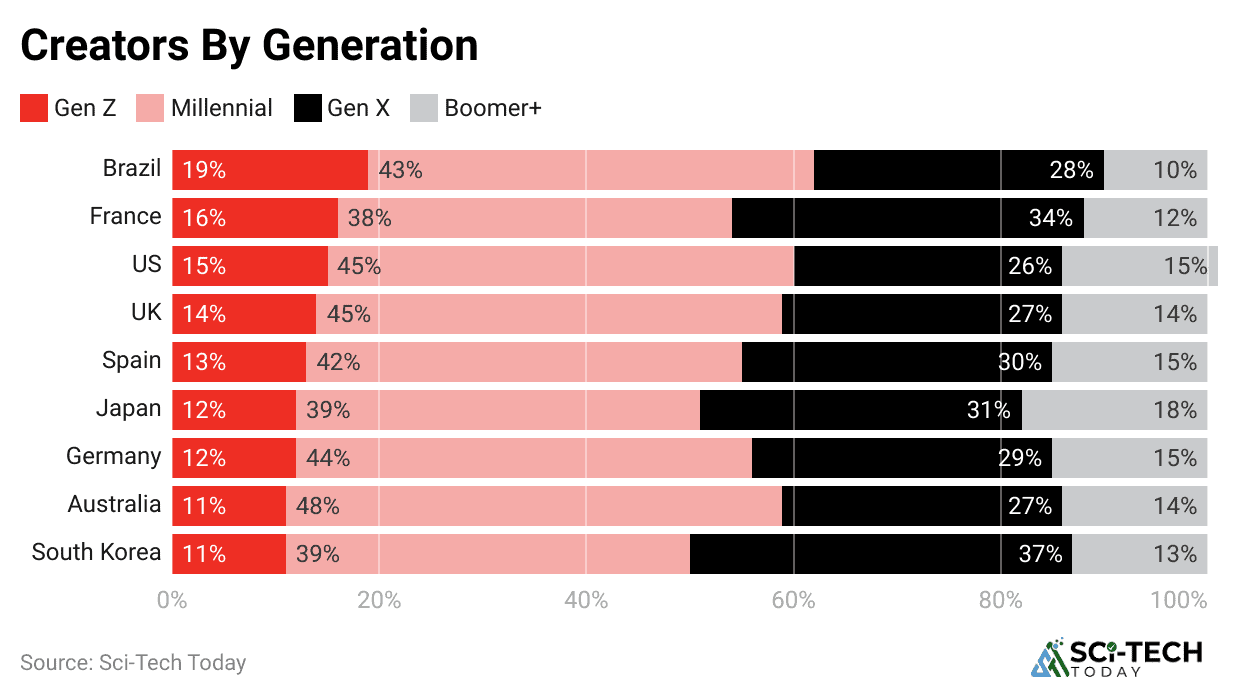

Population and Demographics

(Reference: whop.com)

(Reference: whop.com)

- There are an estimated 208 million content creators across the world, with only a small fraction of this immense group succeeding in making it their primary source of income.

- Brazil currently boasts the largest national count of digital content creators at over 105 million, closely followed by the United States with approximately 86.5 million.

- The large majority of this population falls into the smaller follower tiers, with approximately 67% of creators having an audience of between 1,000 and 10,000 followers.

- Only a tiny fraction, about 2% of all content creators, manage to build audiences exceeding 100,000 followers.

- Millennials, those aged between approximately 29 and 44, are currently the largest generation in the Content Creator Economy, making up an estimated 41% of the entire creator population.

- The composition is surprisingly mature, with Gen X creators accounting for a substantial 30% of the total.

- The split between genders is near parity, with approximately 52% of content creators identifying as men and 47% identifying as women.

- A significant 58% of content creators maintain a separate full-time job in addition to their creative pursuits, highlighting that for most.

- Despite the hustle, a strong majority of part-time creators, roughly 63%, express a clear expectation of transitioning to full-time content creation within the next 2 to 3 years.

| Creator Level | Follower Count |

| Semi-Pro |

1K to 10K Followers |

|

Pro |

10K to 100K Followers |

| Expert |

100K to 1M Followers |

|

Expert+ |

1M+ Followers |

| Total Global Creators |

N/A |

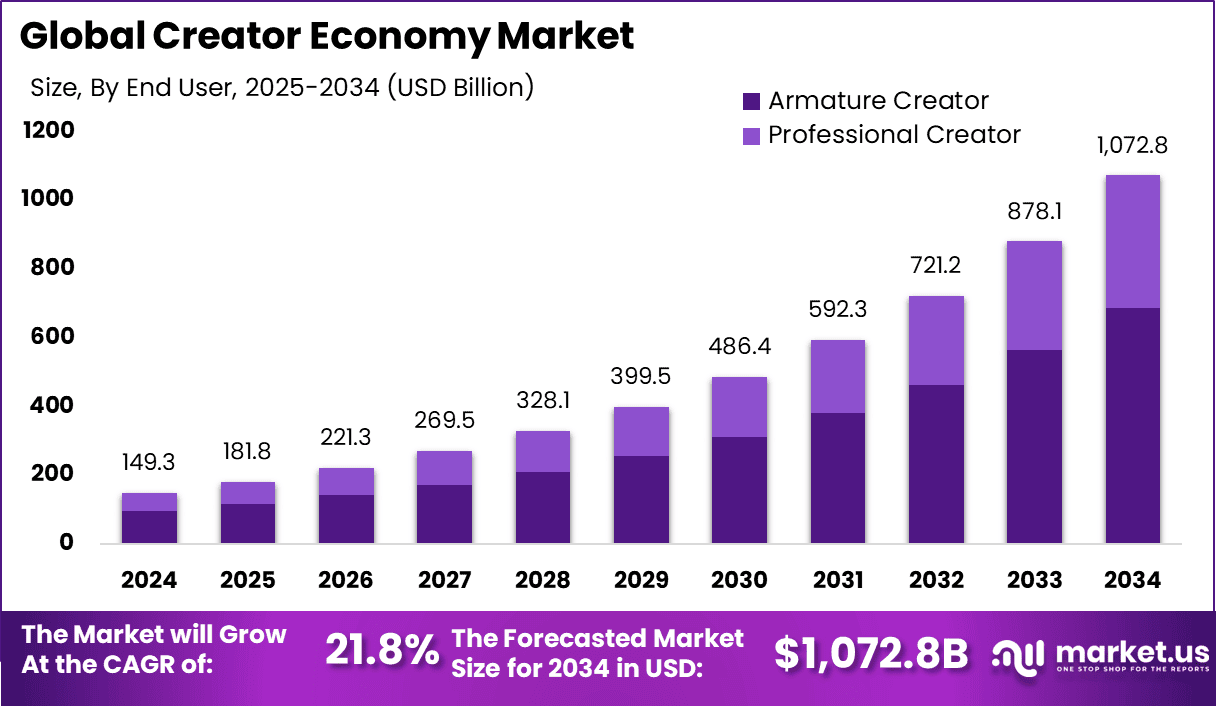

Creator Economy Market Size

(Source: market.us)

(Source: market.us)

According to Market.us, the underlying financial data tells a clear story of aggressive expansion, demonstrating how decentralized digital creativity is building a foundational pillar of the global economy. The market’s potential for high-yield returns is attracting enormous capital investment and entrepreneurial talent worldwide.

- The Global Creator Economy Market is projected to reach USD 1,072.8 billion by 2034 from USD 149.4 billion in 2024, growing at a 21.8% CAGR from 2025 to 2034.

- North America held a 37.4% share in 2024, and the U.S. market was valued at USD 50.9 billion.

- Demand is rising because audiences prefer authentic, relatable, and niche content.

- There were over 400 million creators globally by 2024, indicating a large and diverse ecosystem.

- U.S. full-time digital creator jobs increased from 200,000 in 2020 to 1.5 million in 2024, showing strong employment growth.

- The global creator economy is estimated at USD 191.55 billion according to Exploding Topics, which signals growing economic weight.

- Merchandise companies generate over USD 500 million in annual revenue, adding a direct retail layer to creator income.

- Shopify reported USD 5.2 billion in revenue, reflecting the importance of commerce platforms that support creators.

- About 68.8% of creators rely mainly on brand deals, which remain the primary income source for most creators.

- Only 7.3% of creators report advertising as their top earner, which indicates a shift toward direct partnerships.

- Affiliate marketing income increased by 9%, advertising income increased by 15%, and merchandise income increased by 4%, showing broader monetization.

- Generative AI tools are used by about 59% of creators to speed up ideas and production, which improves publishing efficiency.

- AR, VR, and immersive formats are being adopted steadily, which expands how creators tell stories and engage audiences.

- Analytics, performance dashboards, and real-time insights are helping creators optimize content and improve monetization outcomes.

- Social media platforms account for 27.8% of platform share, which makes them the most common base for building audiences.

- Video streaming platforms hold 24.5% of platform share, which is driven by growth in long-form and high-quality video.

- Video content holds 23.8% of format share, which confirms strong consumer preference for visual storytelling.

- Music content holds 18.3% of format share, which is supported by short-form audio trends and independent artists on streaming services.

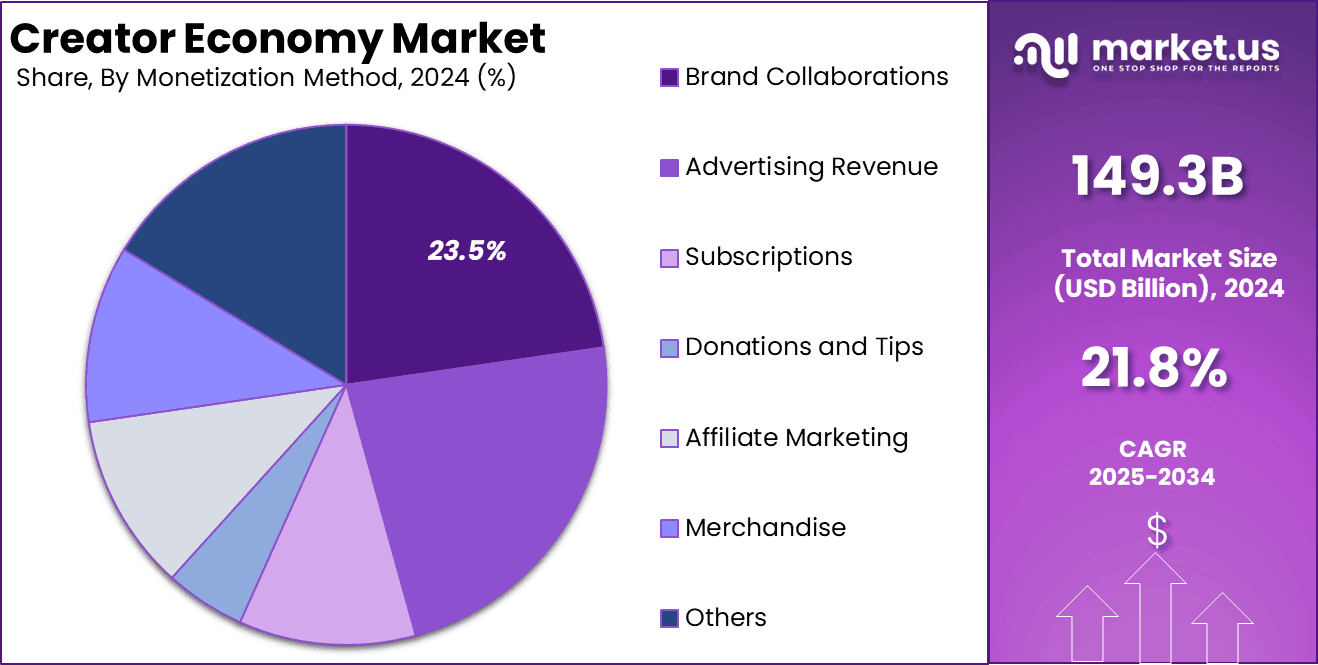

- Brand collaborations account for 23.5% of monetization, which reflects the value of creators providing authentic reach for brands.

- Advertising revenue accounts for 20.9% of monetization, which remains important but trails direct brand partnerships.

- Armature creators represent 64.1% of the base, which shows that low barriers to entry support widespread participation.

- Professional creators make up 35.9% of the base, which indicates a significant full-time segment with structured operations.

- The U.S. creator economy is expanding with a 19.3% CAGR, which signals strong momentum in a mature digital market.

- North America leads with 37.4% share, which is supported by established platforms, robust monetization tools, and advanced digital infrastructure.

(Source: market.us)

(Source: market.us)

- The US Creator Economy Market is valued at USD 50.9 billion in 2024.

- The market is expected to grow from USD 123 billion in 2029 to USD 297.3 billion by 2034.

- The compound annual growth rate for 2025 to 2034 is projected at 19.3%.

- The US share of the North American creator economy declines slightly from 92.2% in 2019 to 91.2% in 2024, indicating gradual diversification.

- Canada’s share increases from 7.8% in 2019 to 8.8% in 2024, suggesting steady expansion within the region.

- Social media platforms remain the largest channel, though the share eases from 31.7% in 2019 to 29.0% in 2024, reflecting maturing usage and broader platform mix.

- Video streaming platforms gain momentum, rising from 22.2% in 2019 to 23.9% in 2024, supported by higher watch time and better monetization tools.

- Content-sharing platforms remain stable, shifting marginally from 15.3% in 2019 to 15.0% in 2024, indicating consistent creator reliance on utility-style hubs.

- Audio platforms grow gradually from 12.0% in 2019 to 12.6% in 2024, helped by podcast adoption and improved ad formats.

- Gaming platforms expand from 10.9% in 2019 to 12.5% in 2024, driven by live streaming, esports tie-ins, and in-stream tipping.

- Other platforms such as e-commerce, decline from 7.9% in 2019 to 7.0% in 2024, as direct creator monetization consolidates on core content platforms.

- Rising mobile use and the popularity of visual and interactive formats such as stories, reels, and live streams increase spontaneous engagement and strengthen social media’s structural dominance through broad reach and multiple revenue streams.

Creator Economy Market Share by Platform Analysis (%), 2019-2024

| Platform | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Social Media Platforms | 31.7% | 31.2% | 30.6% | 30.1% | 29.2% | 29.0% |

| Content-Sharing Platforms | 15.3% | 15.2% | 15.2% | 15.1% | 15.1% | 15.0% |

| Video Streaming Platforms | 22.2% | 22.6% | 22.9% | 23.2% | 23.8% | 23.9% |

| Audio Platforms | 12.0% | 12.1% | 12.2% | 12.4% | 12.5% | 12.6% |

| Gaming Platforms | 10.9% | 11.2% | 11.5% | 11.9% | 12.3% | 12.5% |

| Others (E-commerce Platforms, etc.) | 7.9% | 7.7% | 7.5% | 7.3% | 7.1% | 7.0% |

Content Type Analysis

- In 2024, video held the top spot in the creator economy by content type and captured 23.8% share, supported by strong demand for both short and long videos on YouTube, TikTok, and Instagram Reels.

- Video works best for audience engagement because visuals and stories are easy to watch and share, which improves reach and retention.

- Video supports monetization more efficiently than other formats through ads, brand deals, and fan contributions, which strengthens creator earnings.

- Growth in smartphones, faster mobile internet, and simple editing tools made it easier for creators to produce high-quality videos regularly.

- Viewer preferences have shifted toward visual-first formats, so video continues to guide attention and revenue across global creator ecosystems.

- Video share moved from 21.9% in 2019 to 24.4% in 2024, showing steady year-over-year gains.

- Written content declined from 9.9% in 2019 to 8.7% in 2024, reflecting lower audience time on text-only formats.

- Gaming remained stable at about 17.2% across 2019 to 2024, indicating consistent demand.

- Music eased slightly from 19.6% in 2019 to 19.0% in 2024, showing modest pressure from video-led formats.

- Photography, art, and memes decreased from 11.2% in 2019 to 10.4% in 2024, suggesting slower growth versus video.

- Audio increased from 13.3% in 2019 to 14.0% in 2024, helped by steady podcast and spoken-audio adoption.

- Other formats such as educational content moved from 6.9% in 2019 to 6.2% in 2024, indicating limited share expansion.

| Content Type | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Video | 21.9% | 22.5% | 23.0% | 23.5% | 24.3% | 24.4% |

| Written | 9.9% | 9.7% | 9.4% | 9.2% | 8.9% | 8.7% |

| Gaming | 17.2% | 17.2% | 17.2% | 17.2% | 17.1% | 17.2% |

| Music | 19.6% | 19.4% | 19.3% | 19.2% | 18.9% | 19.0% |

| Photography, Art, and Memes | 11.2% | 11.0% | 10.9% | 10.7% | 10.6% | 10.4% |

| Audio | 13.3% | 13.4% | 13.6% | 13.7% | 13.9% | 14.0% |

| Others (Educational, etc.) | 6.9% | 6.8% | 6.6% | 6.5% | 6.3% | 6.2% |

Platform Specific Statistics

(Source: whop.com)

(Source: whop.com)

#1. YouTube – The Long-Form Video Titan

- YouTube hosts an astronomical base of over 69 million content creators worldwide, solidifying its position as the largest ecosystem for digital video talent.

- The platform’s advertising revenue alone is monumental, totaling $10.47 billion globally in the fourth quarter of 2024.

- In a move toward direct fan support, YouTube Premium and YouTube Music subscriptions have collectively surpassed 100 million global subscribers in 2024.

- Mobile devices are the preferred consumption method, accounting for 63% of all YouTube watch time globally.

- To join the YouTube Partner Program for ad revenue, a creator needs at least 1,000 subscribers and either 4,000 watch hours in the past year or 10 million Shorts views in the last 90 days.

#2. TikTok – The Short-Form Velocity Engine

- The average daily time spent by a user on TikTok is approximately 32 minutes, which is a highly competitive engagement rate that creators leverage for rapid audience growth.

- For every 1,000 video views, TikTok’s Creator Fund is estimated to pay creators between 2 and 4 cents, meaning a video needs 10 million views to generate between $200 and $400 directly from the fund.

- TikTok’s advertising platform demonstrates significant influence on purchasing behavior, with 75% of weekly TikTok users looking for more information on an advertised product after seeing a Lead Generation Ad.

- A substantial 69% of Gen X internet users on the platform express a clear preference for short-form videos over long-form content.

#3. Twitch – The Live-Streaming Leader

- The number of official Twitch Partners has grown by a considerable 44% since 2019, increasing from 35,000 to over 51,000.

- Twitch users are extremely engaged, watching a collective 58 million hours of content daily.

- Top Twitch streamers like Ibai can generate an estimated $185,000 to $233,000 per month just from their over 93,000 paid subscribers alone.

#4. Patreon – The Direct Fan Support Vanguard

- Patreon has successfully paid out a cumulative total of over $3.5 billion to its creators to date.

- The platform has been growing its community functions, with the number of creators starting public chats on the site increasing by a factor of 5X in a single year.

- One-time purchases, in addition to recurring subscriptions, have seen a massive growth rate, with monthly revenue from these single-payment transactions growing by a factor of 4X over the past year.

| Platform | Key Metric | Key Statistic (2024/2025) |

| YouTube | Total Creators | $69 million worldwide |

| YouTube | Q4 2024 Ad Revenue | $10.47 billion globally |

| TikTok | Daily User Time Spent | 32 minutes average |

| Twitch | Daily Watch Hours | 58 hours watched daily |

| Patreon | Total Payout to Creators | Over 3.5 billion to date |

The Web3 and AI Impact

(Source: esparkinfo.com)

(Source: esparkinfo.com)

- 5% of content creators report already utilizing AI tools for at least one task in their creation process, which signals the rapid.

- Despite the time-saving benefits of AI, about 40% of creators who are asked by brands to incorporate generative AI into their content do not expect their brand fees to increase.

- On the consumer side, the reaction to AI integration is surprisingly positive, with 71% of creators who use AI tools reporting a favorable response from their follower base.

- The AI-blockchain market itself, which focuses on tokenizing AI-generated and traditional content, is fiercely competitive and is projected to be valued at over $703 million by 2025.

- Decentralized creator platforms are offering creators a massively increased share of their revenue, allowing them to retain anywhere from 90% to 100% of their profits.

- Non-Fungible Tokens (NFTs) are a primary mechanism for new revenue, with creators using them to sell digital art, tokenized content, and exclusive access.

| Technology | Key Statistic (2024/2025) |

| Artificial Intelligence (AI) | 94.5% |

| Web3 / Blockchain | 90 to 100% |

| NFTs/Smart Contracts | 71% |

| AI-Blockchain Market | $703 million by 2025 |

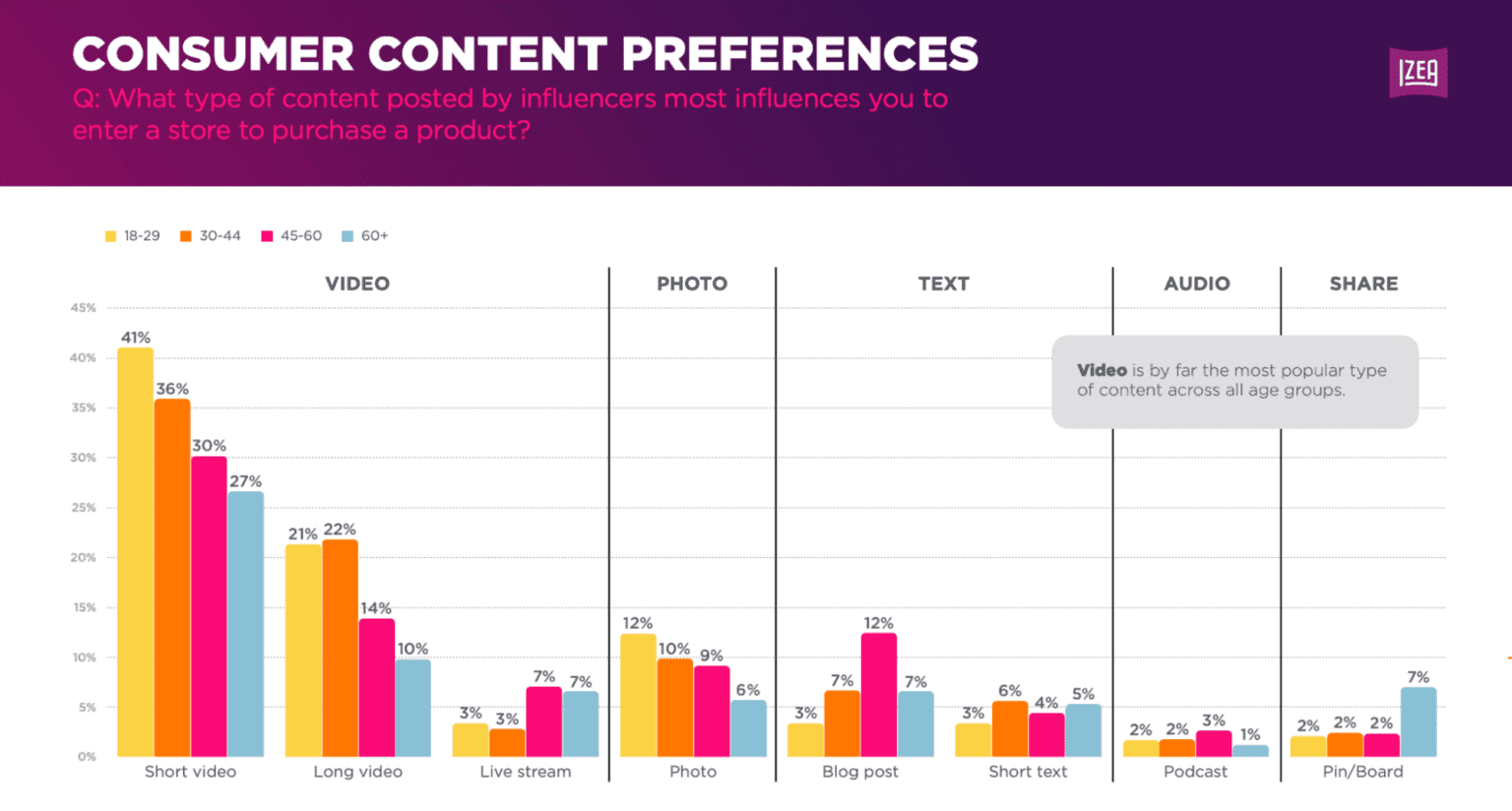

Viewer Behaviour and Content Consumption Trends

(Source: izea.com)

(Source: izea.com)

- American consumers now spend an average of 21 hours per week streaming digital media.

- Audience engagement with interactive content is significantly higher, with interactive formats commanding 53% more engagement compared to passive, static content.

- Long-form videos exceeding 30 minutes, such as webinars and detailed tutorials, have experienced explosive growth of over 11,000% in the past decade.

- A key behavioral link has been established with 59% of Gen Z viewers using short-form video applications to first discover content.

- The viewing landscape is diversifying rapidly: Mobile and TV viewing is increasingly surpassing traditional web viewership for content.

- In the subscription Video-on-Demand (OTT) market, the total revenue is expected to reach $316.40 billion by 2024.

- For creators with membership communities, audience retention is strongly linked to engagement: users who actively participate in the community are 63% more likely to remain active subscribers for a longer duration.

- The international subscriber base is a growing source of revenue, with 60% of creators’ total revenue coming from international subscribers over the last 12 months.

| Content Format | Engagement/Consumption Statistic |

| Streaming Time | Americans stream 21 per week |

| Interactive Content | 53% |

| Long-Form Video (30 min) | 11,000% |

| Gen Z Discovery | 59% |

Conclusion

Overall, these data clearly point out that the content creator economy is both massive and intensely professionalizing. The divide between hobbyists and full-time entrepreneurs will only widen as market valuation skyrockets and platforms introduce new levels of automation and ownership.

Success in this future requires a complete understanding of these statistics, driving creators to, I hope you find this article useful. If you have any questions, kindly let us know. Thanks for staying up till the end.