Introduction

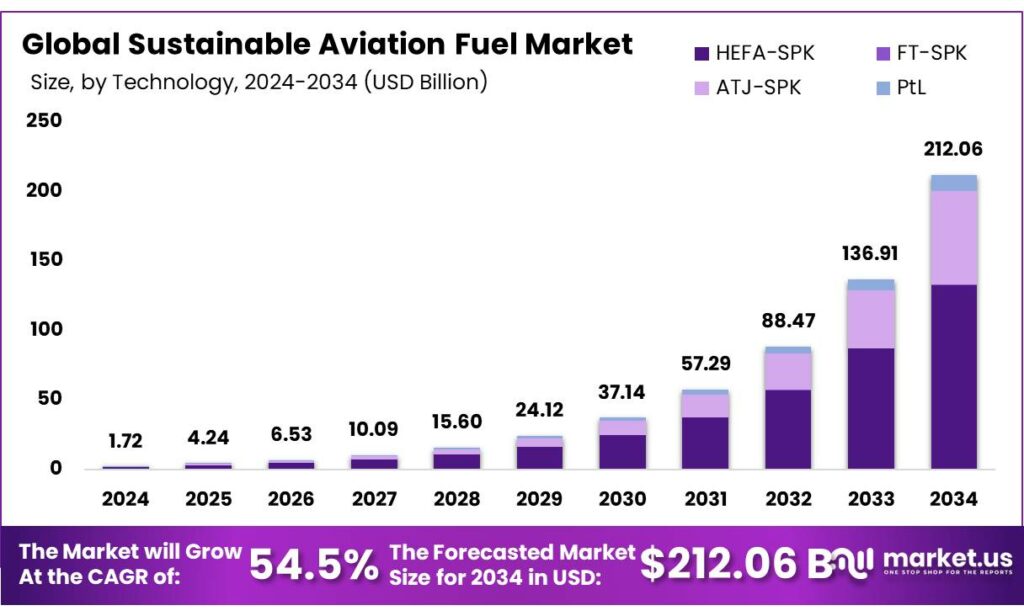

The global Sustainable Aviation Fuel (SAF) market is set for exceptional growth, with its value projected to rise from USD 1.72 billion in 2024 to nearly USD 212.06 billion by 2034. This remarkable expansion represents CAGR of 54.5% from 2025 to 2034, driven by the aviation industry’s urgent transition toward low-carbon fuel alternatives.

In 2024, Europe led the market with a dominant 72.25% share, generating approximately USD 1.24 billion in revenue. The region’s leadership is supported by strong climate policies, advanced SAF infrastructure development, and strict regulatory mandates promoting cleaner aviation fuels.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

The SAF market is evolving rapidly due to global net-zero aviation goals for 2050, backed by strong policy frameworks and rising private-sector investments. International Air Transport Association aims to reduce 1.8 gigatons of CO₂ annually, while International Civil Aviation Organization supports this transition through its Long-Term Global Aspirational Goal (LTAG). SAF is expected to contribute nearly 65% of the aviation sector’s required emission reductions, supported by regulations such as the EU ReFuelEU Aviation Regulation, the U.S. Inflation Reduction Act (IRA), and national blending mandates in Japan, India, and United Arab Emirates.

Despite this momentum, the market still faces major infrastructure and supply chain challenges, with less than 1% of the required global SAF production infrastructure currently operational. To bridge this gap, the industry is expected to require around USD 2.4 trillion in capital investment for biorefineries, feedstock supply chains, and distribution networks.

At the same time, emerging technologies such as Power-to-Liquid (PtL) and carbon capture-based synthetic fuels are creating strong growth opportunities. These innovations can reduce dependence on conventional feedstocks and move the sector closer to near-zero carbon aviation, especially as green hydrogen production scales globally. In parallel, airline offtake agreements and vertical integration models are improving project bankability, securing long-term demand, and accelerating the commercialization of new SAF capacity.

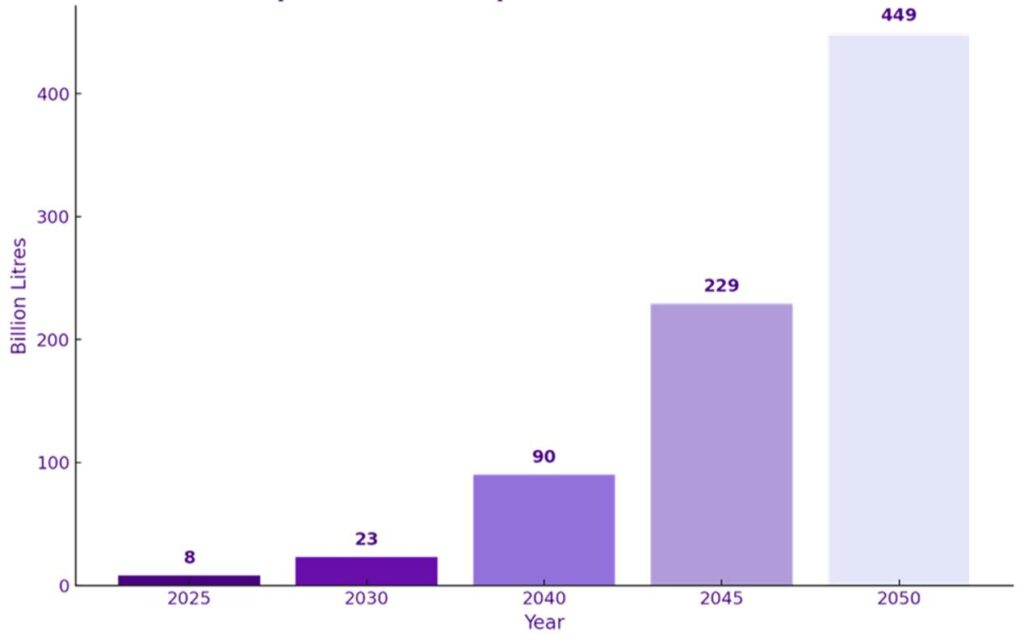

Expected SAF Required For Net Zero 2050

Source: International Air Transport Association

Top Market Takeaways

- The global sustainable aviation fuel market was valued at USD 1.72 billion in 2024.

- The global sustainable aviation fuel market is projected to grow at a CAGR of 54.5% and is estimated to reach USD 212.06 billion by 2034.

- Between technologies, HEFA-SPK accounted for the largest market share of 99.64%.

- Among blending capacities, Up to 20% accounted for the majority of the market share at 96.22%.

- Fixed-wing Aircrafts domianated the market with a market share of 98.55%.

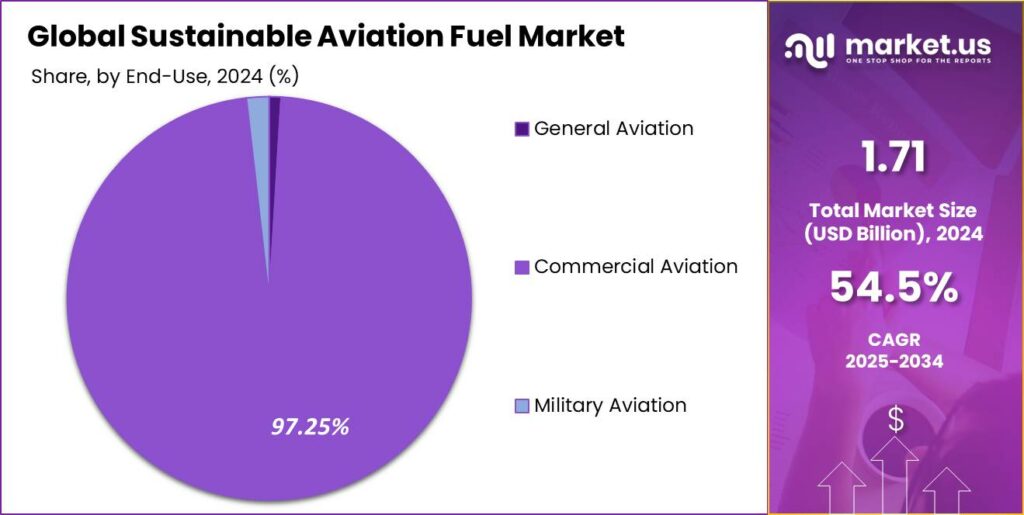

- Based on end-uses, commercial aviation dominated the global sustainable aviation fuel market with a 97.25% market share

- Europe is estimated as the largest market for sustainable aviation fuel with a share of 72.25% of the market share.

- North America was estimated second largest market with a CAGR of 58.2%.

Scope and Research Methodology

The Sustainable Aviation Fuel (SAF) market scope covers a detailed evaluation of the industry across fuel pathways, production technologies, blending ratios, aircraft types, end-use sectors, and regional demand patterns. It includes key SAF technologies such as HEFA-SPK, FT-SPK, ATJ-SPK, and Power-to-Liquid (PtL), along with their commercial maturity, feedstock availability, and infrastructure readiness. Regulatory frameworks like ReFuelEU Aviation, CORSIA, and the U.S. Inflation Reduction Act are key parts of the market scope because they directly shape demand and investment flows.

The research methodology for the SAF market combines both primary and secondary research approaches to ensure accurate market sizing and forecasting. Secondary research includes the study of industry reports, company annual reports, government aviation policies, IATA and ICAO publications, refinery expansion announcements, and sustainability mandates. This is supported by primary research through interviews with fuel producers, airlines, airport fuel operators, regulators, and technology providers to validate assumptions around pricing, capacity, offtake agreements, and future investments.

Technology Analysis

The Sustainable Aviation Fuel (SAF) market is strongly led by HEFA-SPK, which accounted for 99.64% of total SAF production in 2024. Its dominance is mainly due to its technological maturity, commercial scalability, and full regulatory certification. Produced from widely available feedstocks such as used cooking oil, animal fats, and vegetable oils, HEFA-SPK uses established hydroprocessing technology that integrates smoothly with existing refinery systems. Its drop-in compatibility, allowing use without aircraft or engine modifications, further strengthens adoption. Compared with emerging pathways like FT-SPK, ATJ-SPK, and PtL, HEFA-SPK remains the most commercially viable near-term SAF solution, supported by policy incentives and tax credits across major global markets.

Blending Capacity Analysis

SAF blends of up to 20% held the leading position in 2024, capturing 96.22% of the market share. This segment dominates because lower blending ratios align well with current aviation safety standards, certified fuel specifications, and existing airport infrastructure. Although aircraft can technically operate with higher certified blends, airlines commonly prefer 10–20% blending levels to ensure smooth integration, reduce operational risks, and avoid logistical complexity. Limited SAF availability and higher costs compared to conventional jet fuel also make lower blends the most practical choice for large-scale deployment.

Aircraft Type Analysis

By aircraft type, fixed-wing aircraft dominated the global SAF market with an impressive 98.55% share. This leadership is driven by the heavy fuel consumption of commercial airliners, cargo planes, business jets, and military aircraft, all of which rely on long-haul and high-frequency operations. Since these aircraft account for the majority of global aviation fuel demand, they are the primary focus for decarbonization initiatives and SAF adoption. In contrast, rotary-wing aircraft such as helicopters represent a much smaller share of aviation activity and fuel use, limiting their contribution to SAF demand.

End-Use Analysis

The commercial aviation segment led the SAF market in 2024, holding a 97.25% market share. Its dominance stems from the sector’s large operational scale, strong sustainability commitments, and regulatory compliance requirements. Passenger airlines and air cargo operators consume the largest share of jet fuel globally, making them the main adopters of SAF to meet carbon reduction targets. Major carriers such as Delta Air Lines, Lufthansa, Emirates, and Air France-KLM are actively securing long-term SAF supply through strategic agreements. With lifecycle emissions reductions of up to 80%, SAF enables airlines to significantly lower their carbon footprint while using existing engines and airport fueling infrastructure.

Regional Analysis: Europe

In 2024, Europe held the leading position in the global Sustainable Aviation Fuel (SAF) market, accounting for a 72.25% market share. The region’s dominance is largely driven by its strong regulatory environment, advanced technological capabilities, and rapidly growing SAF production capacity.

Europe’s market strength is supported by a well-established policy framework, including the ReFuelEU Aviation Regulation, the revised EU Emissions Trading System (EU ETS), and the Renewable Energy Directive III (RED III). These policies create clear SAF blending mandates and financial incentives, providing a stable demand outlook and encouraging long-term investments across the aviation fuel value chain.

The region has also emerged as a major global hub for SAF production due to the early commercialization of HEFA-based fuels and a growing network of certified biorefineries. Countries such as Netherlands, Finland, France, and Spain are at the forefront of production expansion. In addition, the integration of SAF blends into the Central Europe Pipeline System (CEPS) has significantly improved logistics, distribution efficiency, and supply reliability across both NATO and EU airports.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Key Players Analysis

Product innovation and strong research & development (R&D) are the primary growth strategies adopted by leading players in the Sustainable Aviation Fuel (SAF) market. Major companies are focusing on capacity expansion, technology diversification, and strategic collaborations to strengthen their competitive position and secure long-term market leadership.

A key strategy involves expanding SAF production through new biorefineries and upgrades to existing refining facilities. Companies are increasing output across multiple fuel pathways, including HEFA, Fischer–Tropsch, and Power-to-Liquid (PtL) technologies, to meet the rapidly growing demand for low-carbon aviation fuels.

Another major focus is the signing of long-term offtake agreements with airlines, which helps ensure stable demand, supports financing for new projects, and improves long-term revenue visibility. These agreements are becoming critical for scaling SAF adoption globally.

In addition, companies are building stronger partnerships across the value chain, connecting feedstock suppliers, refiners, logistics providers, and airports to improve supply chain efficiency and fuel availability. At the same time, continued investments in advanced feedstocks, higher conversion efficiency, and cost reduction technologies are helping the industry move closer to price competitiveness with conventional jet fuel while maintaining compliance with global sustainability standards.

Top Key Players in the Market

- Neste Corporation

- GEVO, INC.

- World Energy, LLC

- TotalEnergies SE

- Montana Renewables, LLC

- Eni SpA

- Valero Energy Corporation

- LanzaTech

- SkyNRG BV

- OMV Aktiengesellschaft

- BP p.l.c.

- Synhelion AG

- Exxon Mobil Corporation

- Repsol S.A.

- Moeve

- Other Key Players

Recent Developments

In June 2025, Neste signed an agreement to supply 7,500 metric tons (2.5 million gallons) of Neste MY Sustainable Aviation Fuel (SAF) to Amazon Air for operations at San Francisco International Airport and Ontario International Airport. This made Amazon the first SAF user at Ontario International Airport. Produced from renewable waste and residue feedstocks, the fuel can reduce greenhouse gas emissions by up to 80%, while Neste’s expanding pipeline and renewable diesel truck network highlights the continued growth of SAF infrastructure across the U.S. West Coast.

In October 2025, Gevo Inc. received an extension from the U.S. Department of Energy on its conditional commitment for a USD 1.46 billion loan guarantee supporting its SAF project in Lake Preston, South Dakota. The extension, now valid until April 16, 2026, provides additional time to assess possible project scope enhancements, including a proposed 30-million-gallon-per-year Alcohol-to-Jet (ATJ-30) facility in North Dakota. This development strengthens Gevo’s long-term expansion strategy in sustainable aviation fuels.

In May 2024, World Energy entered into a five-year agreement with Boston Consulting Group to supply Sustainable Aviation Fuel certificates (SAFc), representing BCG’s largest SAF-related purchase to date. The agreement is expected to reduce 100,000 metric tons of CO₂ emissions through 2028, covering more than half of BCG’s 2023 air travel footprint. Produced using HEFA technology from waste fats and oils, the fuel meets strict sustainability standards and supports BCG’s net-zero by 2030 target, while also reinforcing World Energy’s leadership in scaling low-carbon aviation solutions through corporate partnerships.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.72 Bn |

| Forecast Revenue (2034) | USD 212.06 Bn |

| CAGR (2025-2034) | 54.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (HEFA-SPK, FT-SPK, ATJ-SPK, & PtL), By Blending Capacity (Up to 20%, 20 to 40%, & Above 40%), By Aircraft Type (Fixed-wing & Rotary-wing) By End-use (General Aviation, Commercial Aviation & Military Aviation) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Neste Corporation, GEVO, INC., World Energy, LLC, TotalEnergies SE, Montana Renewables, LLC, Eni SpA, Valero Energy Corporation, LanzaTech, SkyNRG BV, OMV Aktiengesellschaft, BP plc, Synhelion AG, Exxon Mobil Corporation, Repsol S.A., Moeve, & Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |