Introduction

AI Industry Statistics: In the rapidly growing landscape of technology, Artificial Intelligence Industry has cemented its position as the engine of modern development, fundamentally changing global markets, job roles, and everyday life. The scale of its economic contribution, associated with an accelerating pace of technical advancements, makes the AI Industry a topic of data volume.

In this comprehensive analysis, I would like to discuss more of the core stats and trends changing the AI Industry, providing a benchmark for understanding its profound impact from its academic origins to its current, trillion-dollar trajectory. Without further ado, let’s get into the article.

Editor’s Choice

- According to Market.us, the AI market is set to see explosive growth, jumping from $542.5 billion in 2025 to a massive $10,173.1 billion by 2034.

- Total corporate investment in the AI Industry surged to a record $252.3 billion in 2024, with private investment alone climbing by a massive 5% YoY, confirming the unprecedented level of confidence and capital allocation to this core technology.

- The United States maintains a decisive financial lead in the AI Industry, with $109.1 billion in private investment recorded in 2024, which is nearly 12 times the capital invested in China, underscoring the dominance of the North American development ecosystem. North America commands the largest regional market share at roughly 93%.

- The Generative AI sub-segment is a powerhouse, attracting $33.9 billion in private funding in 2024 and is individually projected to reach a stunning $1.3 trillion market valuation within the next decade.

- This is nearly a 9-fold increase in funding compared to its level just two years ago, illustrating the feverish race in foundation model development.

- The manufacturing sector is projected to realize the largest financial benefit, with the addition of $3.78 trillion in economic value from AI integration by 2035, primarily through automation and efficiency gains. This represents a nearly 45% uplift in the sector’s Gross Value Added GVA.

- The adoption rate of AI in businesses has dramatically accelerated, with 78% of organisations reporting AI use in 2024, up from 55% just one year prior, signalling that AI is rapidly moving from a pilot-project stage to a fundamental part of core business operations. Customer Service 56% and Cybersecurity 51% remain the top applications.

- The global job market faces a significant structural overhaul: while an estimated 300 million jobs are at risk of automation by 2030, the AI Industry is simultaneously expected to create a net gain of 78 million new roles.

- A concerning talent gap persists, with women representing only 22% of the professional AI Industry talent pool globally, resulting in a 72% gender disparity.

- Public demand for safety is overwhelming, with 85% of respondents supporting a national effort to ensure the AI Industry is developed securely and ethically.

- Conversely, only 39% of the public currently believes that existing AI technology is safe, highlighting a major trust deficit that businesses must overcome.

- The essential hardware backbone of the AI Industry, the global AI chip market, is expanding rapidly, projected to reach $83.25 billion by 2027, growing at an aggressive 35%

The Genesis of the AI Industry by Key Dates and Foundational Metrics

(Source: wikipedia.org)

(Source: wikipedia.org)

- The term “artificial intelligence” itself was formally coined in 1955 by John McCarthy for the Dartmouth Summer Research Project on Artificial Intelligence workshop, marking the field’s official birth as an academic pursuit.

- The first operational program to exhibit machine learning was developed in 1952 by Arthur Samuel, a checkers-playing program that could actually learn from experience, representing an early, yet crucial, proof-of-concept for the AI Industry’s core principles.

- The late 1980s saw the first commercial success with Expert Systems, propelling the nascent AI Industry into a billion-dollar enterprise, demonstrating the first tangible, large-scale commercial value of AI technology.

- The current wave of development, largely fueled by the Deep Learning breakthrough, was significantly accelerated by the introduction of the Transformer architecture in 2017, which became the foundation for today’s large language models LLMs that are dominating the AI Industry’s development cycle.

- Early government backing for the AI Industry was substantial, such as the Japanese government’s allocation of $850 million over $2 billion in today’s money in 1981 to the Fifth Generation Computer project, illustrating a significant national commitment to advanced computing and AI research.

| Field’s Founding | Term coined in 1955 |

| First Commercial Scale |

Billion-dollar enterprise by the late 1980s |

|

Generative AI Foundation |

Transformer architecture was introduced in 2017 |

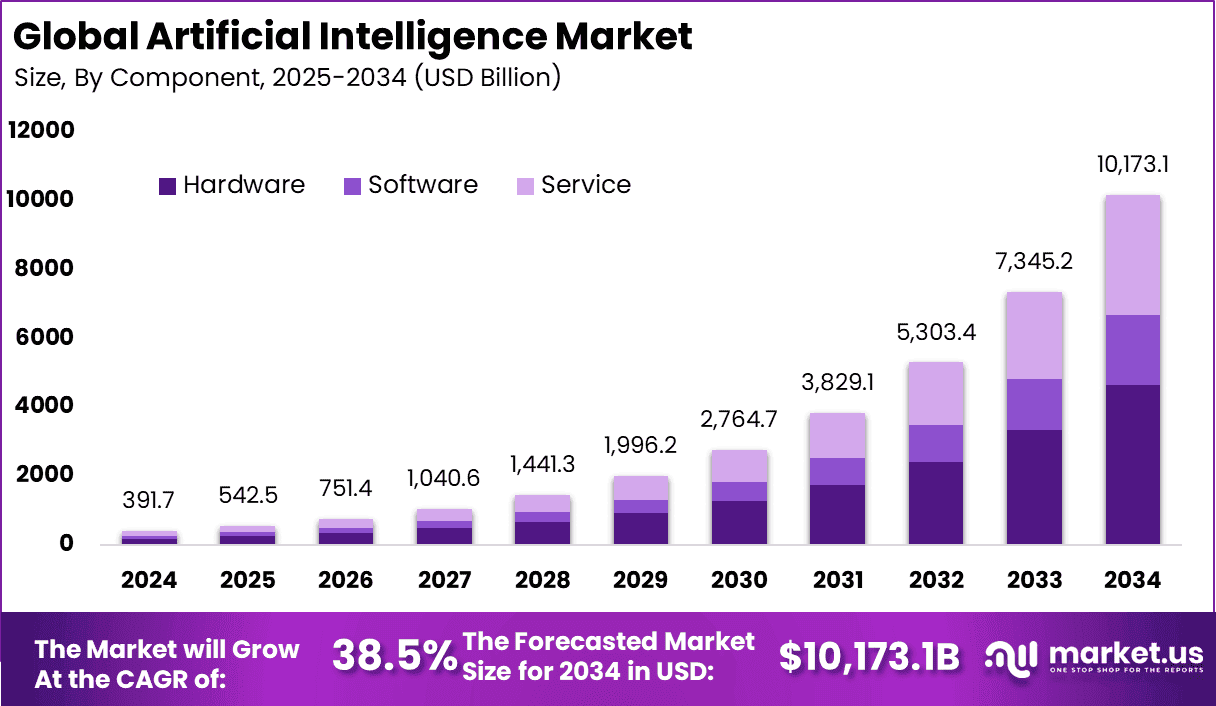

AI Market Size

(Source: market.us)

(Source: market.us)

According to market.us, here are the key numeric insights regarding the overall AI Industry:

- The global AI market was valued at USD 391.70 billion in 2024. It is expected to grow from USD 542.50 billion in 2025 to nearly USD 10,173.05 billion by 2034, with a CAGR of 38.50% between 2025 and 2034.

- North America held the leading share in 2024, generating about USD 143.75 billion in revenue.

- Hardware made up 45.6% of the total AI market share.

- Cloud-based deployment accounted for 67.8% of the market.

- Machine Learning was the most used AI technology with a 43.5% share.

- Healthcare was the top industry using AI, holding 25.7% of the market share.

- The AI market in the United States was worth USD 4.67 billion in 2024 and is growing at a 13.7% CAGR.

- North America as a region held 34.6% of the global AI market.

- In China, 58% of companies currently use AI and 30% are in the process of testing or evaluating it.

- In the United States, only 25% of companies have adopted AI, while 43% are exploring its possible uses.

- The World Economic Forum expects AI to create 97 million new jobs, which will balance out jobs lost to automation.

- Accenture estimates that AI could add USD 3.8 trillion to the manufacturing industry by 2035.

- A Forbes Advisor survey shows that 24% of business owners are concerned that AI could reduce their website traffic.

- More than 25% of startup funding in the United States in 2023 went to AI-focused companies, compared to 12% between 2018 and 2022.

- OpenAI was seeking a valuation of around USD 90 billion in late 2023, showing strong investor trust in generative AI.

- About 20% of generative AI users are between the ages of 25 and 34, indicating high usage among younger professionals.

- The self-driving car market is expected to exceed USD 600 billion within five years due to increasing use of autonomous vehicles.

- In December 2023, Google launched a large language model called Gemini in three versions: Gemini Ultra, Gemini Pro, and Gemini Nano. It can process and generate text, images, audio, and video in one system.

- Forbes Advisor reports that AI could increase the GDP of the United States by 21% by 2030. An internal survey also expects a 21% GDP boost, showing strong confidence in AI’s economic impact.

- ChatGPT reached one million users within five days of launch, showing how fast AI tools are being adopted.

- A Forbes Advisor survey found that 64% of businesses believe AI will greatly improve their productivity.

- Exploding Topics research predicts that the AI industry will grow more than 13 times in the next six years.

- By 2025, up to 97 million people may be employed in the AI sector.

- The AI market is expected to grow by at least 120% each year.

- Around 83% of companies view AI as an important part of their business plans.

- Netflix uses AI for personalized recommendations and earns about USD 1 billion in annual revenue from this feature.

- About 48% of businesses use AI to make better use of big data.

- In healthcare, 38% of medical providers use computer-assisted diagnostics powered by AI.

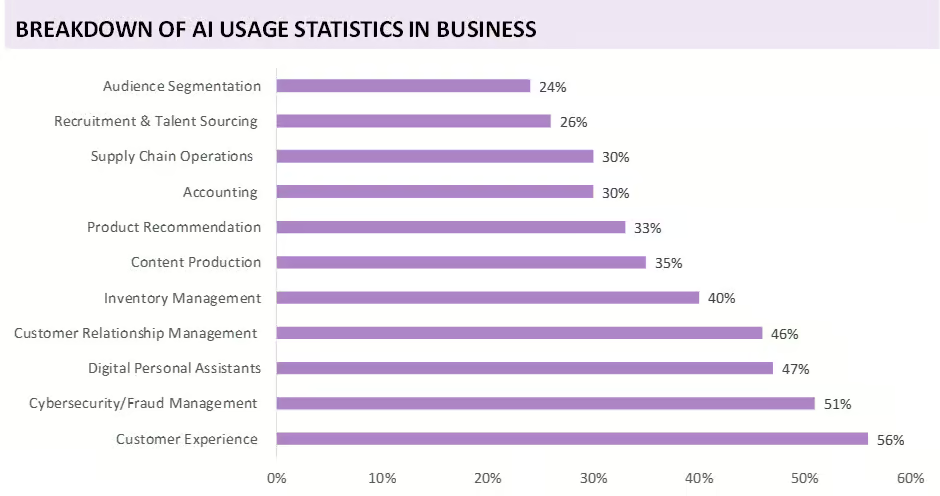

AI Usage in Business Statistics

(Source: Market.us)

- 56% of companies rely on AI to lift overall customer experience, from quicker support to more personalized interactions.

- In 51% of firms, AI plays a core role in cybersecurity and fraud control, spotting risks faster than manual checks.

- 47% of organizations use AI-powered assistants to handle routine tasks and provide instant information to staff.

- Customer relationship efforts benefit in 46% of businesses, where AI helps track leads, predict churn, and guide follow-ups.

- Inventory is managed with AI in 40% of companies, improving stock accuracy and reducing out-of-stock events.

- Content teams in 35% of organizations turn to AI for drafting, editing, and scaling production.

- Product suggestions are AI-driven in 33% of businesses, matching items to user preferences and behavior.

- Supply chain activities use AI in 30% of cases, aiding demand forecasts and logistics planning.

- Accounting functions adopt AI in 30% of companies to automate reconciliations and flag anomalies.

- Recruitment and talent sourcing use AI in 26% of firms to screen resumes and shortlist candidates.

- Audience segmentation is AI-enabled in 24% of businesses, grouping customers for more relevant campaigns.

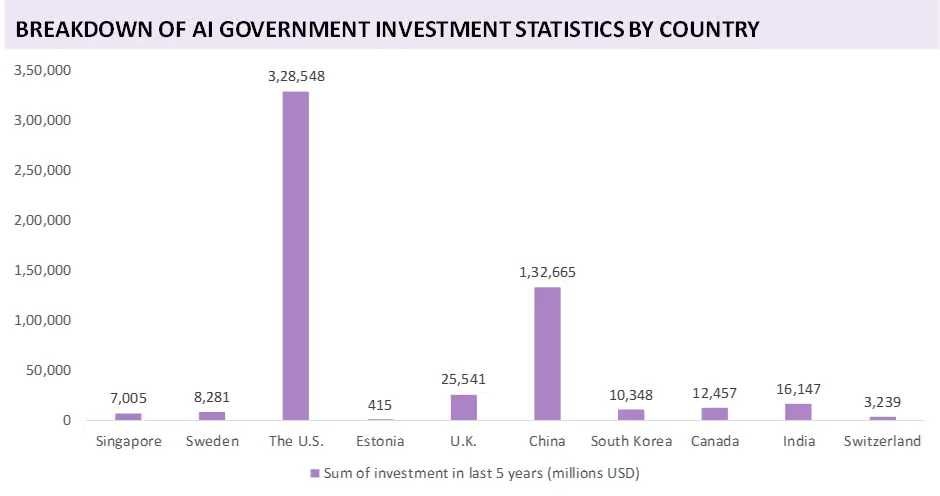

Government Investment Statistics in AI by Country

- The U.S. recorded the largest public spend on AI, totaling 328,548 million USD over the last five years.

- China followed with cumulative government funding of 132,665 million USD during the same period.

- The U.K. has directed 25,541 million USD to AI initiatives across five years.

- India’s government support for AI reached 16,147 million USD in five years.

- Canada’s five-year AI outlay stood at 12,457 million USD.

- South Korea committed 10,348 million USD to AI programs over five years.

- Sweden’s total investment in AI amounted to 8,281 million USD across the period.

- Singapore allocated 7,005 million USD to AI development in five years.

- Switzerland reported 3,239 million USD in government AI funding over five years.

- Estonia showed a smaller but notable contribution, with 415 million USD invested in AI during the period.

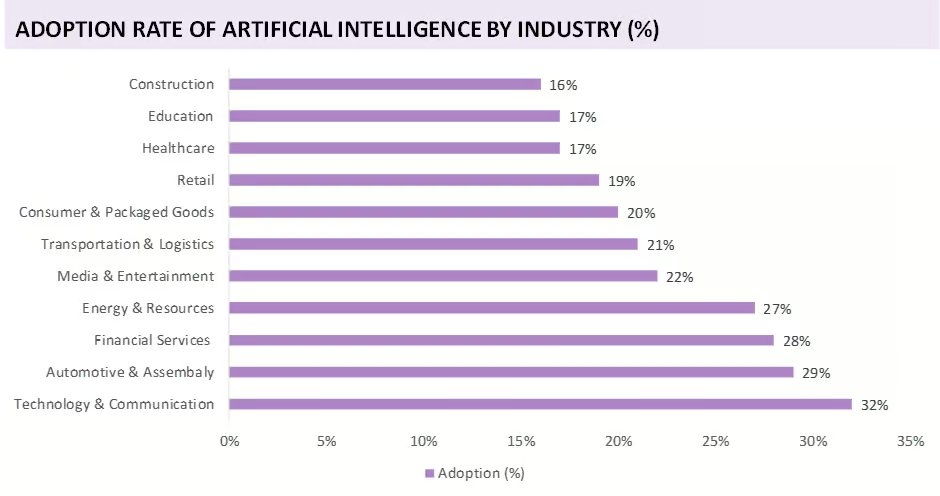

AI Adoption Rate by Industry

(Source: hai.stanford.edu)

(Source: hai.stanford.edu)

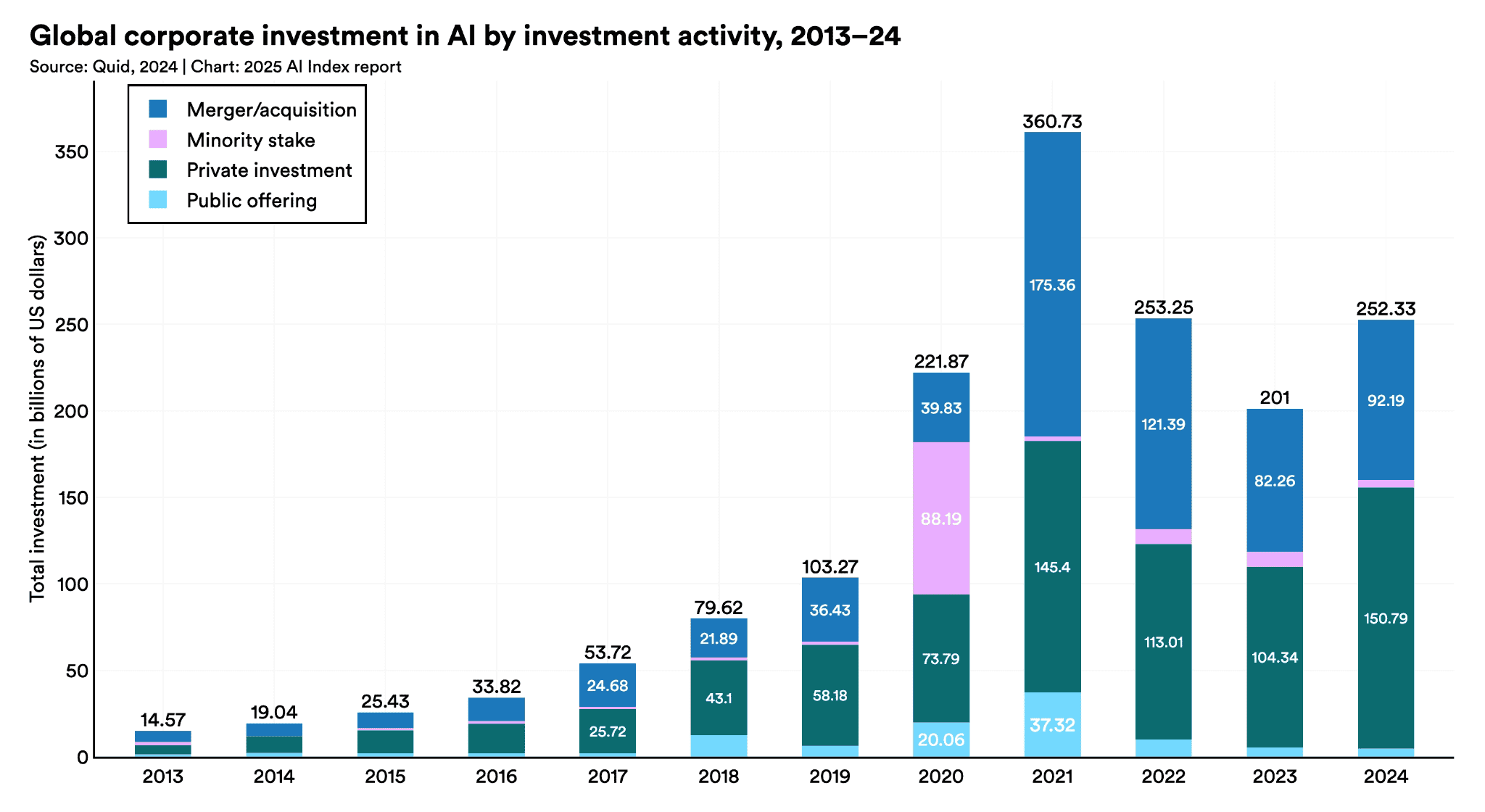

- Global corporate investment in AI reached a remarkable total of $252.3 billion in 2024, representing a substantial 26% growth from the previous year, demonstrating a sustained and rapidly accelerating financial commitment to the AI Industry.

- Private investment, a key part of this, climbed by an even sharper 44.5% over the same period, signaling investor confidence.

- The United States overwhelmingly dominates global private investment, recording a massive $109.1 billion in 2024, which is nearly 12 times the investment seen in China and 24 times the investment in the United Kingdom.

- Private investment specifically directed into the Generative AI sector hit a staggering $33.9 billion in 2024, which is an 18.7% increase from 2023 and represents over 8.5 times the investment seen just two years prior in 2022.

- To further national strategic goals, the Chinese government established a National AI Industry Investment Fund with an initial investment of around $8.2 billion, as part of a larger, long-term national strategy to become the leading AI nation globally by 2030. This large-scale government funding demonstrates the geopolitical nature of the AI Industry race.

- Beyond the US and China, the United Kingdom has also shown significant commitment, allocating a substantial £100 million financial increase to the Alan Turing Institute to enhance its data science and AI development capabilities.

- Other countries like Canada have committed up to $2 billion to improve sovereign AI computer infrastructure, ensuring national access to critical resources for the AI Industry.

| United States | Over $470.9 billion |

| China | Approximately $119.3 billion |

| United Kingdom | Approximately $28.2 billion |

| Global Private Investment 2024 | $252.3 billion |

AI Industry Adoption and Sectoral Impact

(Reference: scalacode.com)

(Reference: scalacode.com)

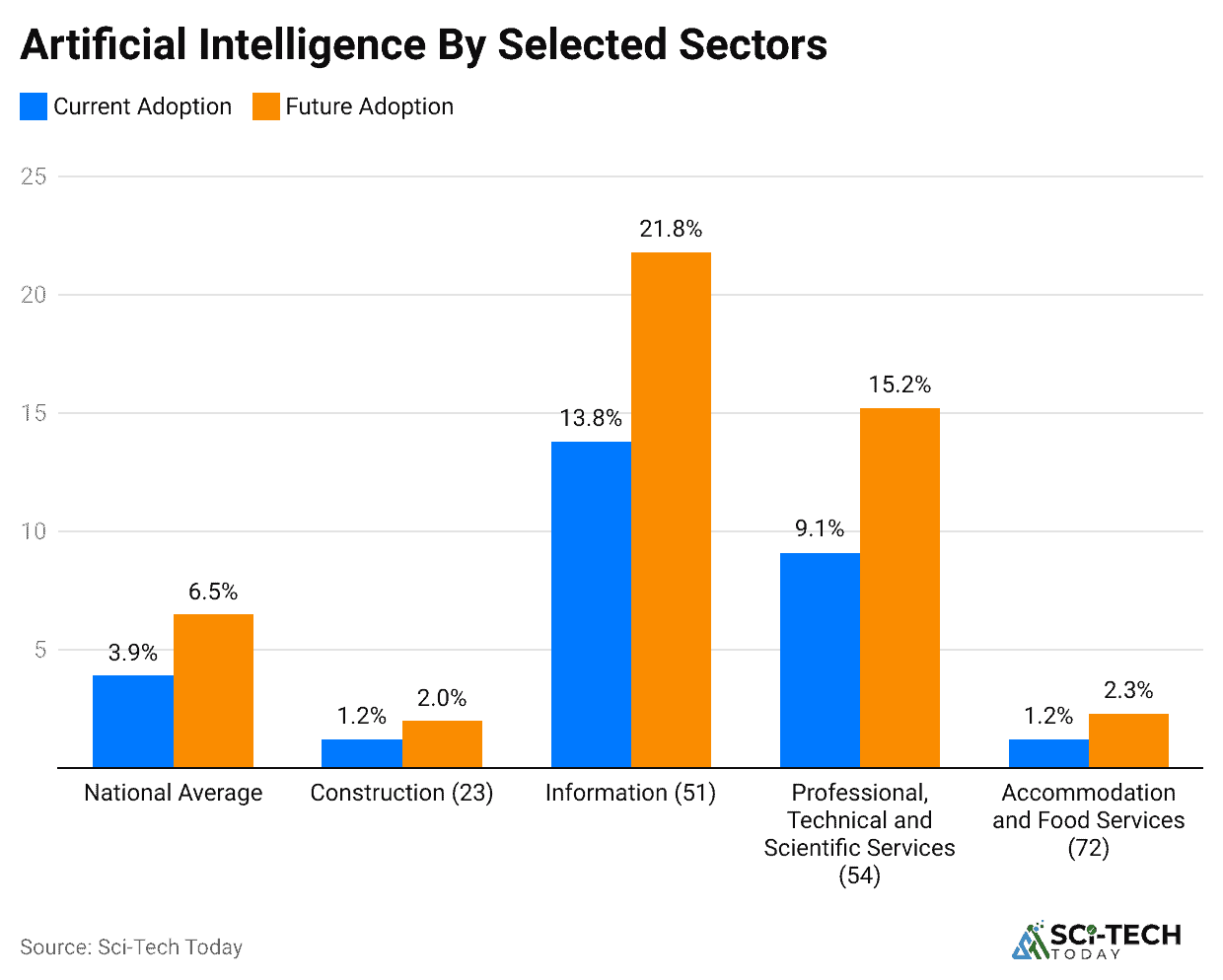

- A significant 78% of organizations reported using AI in some capacity in 2024, a massive jump from only 55% in the previous year, illustrating the rapid mainstreaming and operationalization of AI technologies across the corporate world.

- The financial sector, specifically Financial Services, stands to gain a colossal economic contribution of $1.15 trillion from the integration of AI by 2035, positioning it as one of the top beneficiaries of the current technological wave.

- The Manufacturing sector is forecasted to see the single largest economic gain, with AI expected to contribute an additional $3.78 trillion to the sector by 2035, a nearly 45% increase over business-as-usual projections.

- The Healthcare sector was the leading market segment for AI revenue in 2024, with its adoption fueled by the critical need to enhance diagnostics, improve patient care outcomes, and optimize hospital workflow management.

- Over 38% of medical providers already use computer systems to aid in diagnosis, indicating deep integration.

- In one major real-world application study, worker productivity for customer support agents was demonstrably boosted by 14% through the implementation of generative AI tools like ChatGPT, providing tangible, quantifiable evidence of AI’s direct positive impact on labor efficiency.

- The top three most commonly reported uses for AI in business are Customer Service 56%, Cybersecurity and Fraud Management 51%, and Digital Personal Assistants 47%, showing that the focus of AI Industry deployment is primarily on streamlining customer interaction and safeguarding operations.

| Manufacturing | $3.78 trillion |

| Financial Services | $1.15 trillion |

| Wholesale and Retail | $2.23 trillion |

| Healthcare | $461 billion |

The AI Industry and the Transformation of the Global Workforce

- By 2030, a significant 9.1% of all jobs worldwide, translating to roughly 300 million roles globally, could be replaced by AI-driven automation, with the highest concentration of risk in cognitive, white-collar professions.

- However, the World Economic Forum projects that while 92 million roles could be displaced by 2030, the AI Industry is simultaneously expected to create a net gain of 78 million new jobs in related fields.

- In the United States, an estimated 30% of current jobs could be fully automated by 2030, but a much larger 60% of all jobs will see significant task-level changes due to AI integration.

- The most at-risk jobs for automation are typically clerical and administrative roles, with forecasts predicting the loss of over 7.5 million data entry and administrative secretary jobs by 2027.

- Conversely, the demand for AI and data science specialists is among the fastest-growing job categories in 2025, with the employment of Software Developers projected to see a 17.9% increase from 2023 to 2033.

- A concerning statistic shows that 41% of employers globally intend to reduce their workforce because of AI over the next five years.

| Global Job Displacement Projected | 300 million, 9.1% of all jobs | Expected loss by 2030 due to AI-driven automation. |

| Global Net Job Effect | Net gain of 78 million new roles | Projected outcome of AI Industry creation vs. displacement by 2030. |

| US Jobs with Significant Task Change | 60% of all jobs | Roles where tasks will be significantly modified by AI integration by 2030. |

| Highest Growth Job Category | 17.9% increase in Software Developers | Projected employment growth from 2023 to 2033. |

Demographics and the AI Industry Talent Gap

(Source: edwardconard.com)

(Source: edwardconard.com)

- Globally, women represent only 22% of the professional talent pool in Artificial Intelligence, compared to 78% who are men, which points to a stark, persistent gender gap of 72% yet to be closed in the core AI Industry workforce.

- The gender disparity is particularly pronounced in advanced technical specializations: only 23.5% of those listing AI engineering skills on professional networking platforms were women in 2018, though this figure had encouragingly risen to 29.4% by 2025.

- Women are statistically more likely to be employed in occupations that are at a high risk of automation, with 79% of employed women in the U.S. in such roles, compared to 58% of men.

- A significant gap in training access exists across generations: only 22% of Baby Boomers and 28% of Gen X workers have been offered AI skilling opportunities by their employers, starkly contrasting with 45% of Gen Z and 43% of Millennial workers.

- In the most highly technical roles, such as Deep Learning, the gender divide is even more extreme, with men comprising 76% of the talent pool.

| Women Global | 22% | 72% gender gap in the overall AI Industry talent pool. |

| Men Global | 78% | Dominate all technical specializations, including 76% of Deep Learning talent. |

| Baby Boomers/Gen X | N/A | Only 22 to 28% offered AI skilling opportunities by employers. |

| Gen Z/Millennials | N/A | 43 to 45% offered AI skills, showing greater access to new AI Industry skills. |

Trust, Ethics and Regulation in the AI Industry

(Source: cocreations.ai)

(Source: cocreations.ai)

- A large majority of the public, specifically 85% of respondents in a major survey, support a national and global effort to ensure the AI Industry is developed and deployed safely and securely.

- Public skepticism remains a significant factor, with only 39% of respondents believing that current AI technology is inherently safe and secure, revealing a large trust deficit that the AI Industry must actively address through greater transparency and verifiable assurances.

- Demand for transparency is high, as 85% of people polled want industries to be explicitly transparent about their AI assurance practices before bringing any AI-enhanced products to the consumer market.

- In the healthcare context, a highly sensitive area, a promising 51% of adults surveyed thought that using AI could potentially reduce instances of racial and ethnic bias in care delivery.

- Globally, the United States, the United Kingdom, and the European Union have all seen new regulatory actions in the past year, with the EU’s AI Act setting a global precedent for comprehensive, risk-based regulation

| Support for AI Safety Effort | 85% |

| Belief in Current AI Security | 39% |

| Demand for Transparency | 85% |

| AI’s Potential to Reduce Bias | 51% |

Future Projections and Emerging Trends in the AI Industry

(Source: procurri.com)

(Source: procurri.com)

- Future trends show that 20% of IT leaders’ tech budgets are projected to be dedicated to AI in 2025, with the largest allocation going towards Generative AI applications.

- The evolution towards multimodal AI is a key trend, where models will process not just text, but also audio, video, and image data simultaneously, enabling significantly more intuitive and human-like interactions.

- This capability is expected to advance dramatically in 2025, driving new applications in search and content creation.

- The concept of Hallucination Insurance is emerging as a necessity for the AI Industry, with businesses expected to offer coverage against incorrect or misleading outputs from generative AI models.

- The widespread adoption of Edge AI is a strong future trend, pushing AI processing away from centralized clouds and onto local devices like smartphones and industrial sensors.

- This will be facilitated by new hardware, such as the HP OmniBook 5 series, which includes a Neural Processing Unit NPU capable of 45 TOPS Trillions of Operations Per Second of computational performance.

- The democratisation of AI is accelerating through no-code and low-code platforms and API-driven microservices, which will allow non-experts, entrepreneurs, educators, and small businesses to develop custom AI solutions.

| GenAI Budget Share | 20% of IT tech budgets in 2025 |

| Edge AI Capability | 45 TOPS on new devices, e.g., HP OmniBook |

| Democratization | Rapid growth of no-code/low-code platforms |

| Hallucination Insurance | Financial instrument to mitigate risk |

Conclusion

Overall, the AI Industry is not merely a collection of technologies; it is a global economic force quantified by these compelling data. From a market projected to swell to $1.77 trillion by 2032, to the massive $3.78 trillion in potential gains for the manufacturing sector, the numbers speak to an unmatchable, ongoing transformation.

The concentration of capital, with the U.S. commanding a $109.1 billion lead in private investment in 2024, underscores the fierce global competition at play. While the AI Industry promises immense productivity gains, evidenced by a 14% boost in one study, it also necessitates a critical focus on workforce equity and public trust, given the 72% gender gap and the 85% public demand for verifiable AI safety measures.

So, the future of the AI Industry will be defined not only by its technological leaps but also by how successfully we navigate the ethical and societal challenges that these powerful statistics illuminate. I hope you like this piece of content. If you have any questions, thanks for staying up till the end.