Harley-Davidson (NYSE: HOG) reported Q1 2026 diluted EPS of $0.22, in line with one consensus estimate of $0.22 but missing other forecasts of $0.25 to $0.34 per share. Revenue came in at $1.17 billion, beating analyst estimates of $1.01 billion. Shares rose approximately 8% on earnings day, reflecting investor relief at the revenue beat and reaffirmed full-year guidance, even as tariff costs and the HDFS restructuring weighed heavily on net income.

About Harley-Davidson

Harley-Davidson, Inc. (NYSE: HOG) is one of the world’s most iconic motorcycle manufacturers, founded in 1903 and headquartered in Milwaukee, Wisconsin. The company designs, manufactures, and sells motorcycles, parts and accessories (P&A), apparel, and related financial services products to riders worldwide. Its principal business segments include Harley-Davidson Motor Company (HDMC), Harley-Davidson Financial Services (HDFS), and the electric vehicle brand LiveWire.

As of May 2026, Harley-Davidson carries a market capitalization of approximately $2.74 to $2.80 billion, reflecting a steep decline from its 2022 peak of over $6 billion. The stock trades at a trailing P/E ratio of approximately 8.33 to 9.61 and offers a dividend yield of approximately 3.1%. The company employs thousands globally and has been a symbol of American motorcycle culture for more than 120 years. Harley-Davidson holds a 38% share of the US 601cc-plus motorcycle segment as of Q1 2026, up two percentage points year over year.

Top Financial Highlights

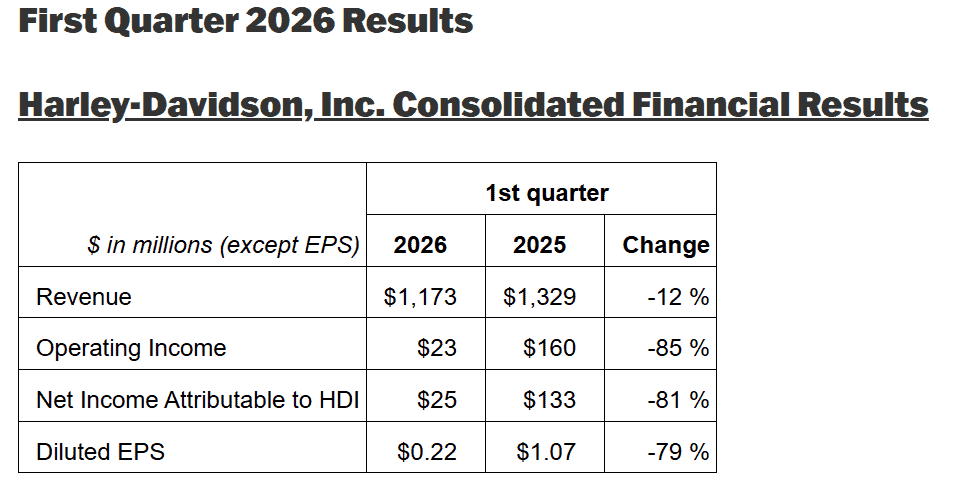

- Total revenue reached $1.17 billion in Q1 2026, declining 12% year over year, primarily due to a sharp reduction in financial services revenue following asset sales.

- Net income attributable to the company was $25 million, down 81% from $133 million in Q1 2025.

- Diluted EPS stood at $0.22, decreasing 79% from $1.07 in the prior-year period.

- Motorcycle segment revenue totaled $1.055 billion, down 2% year over year, reflecting lower wholesale shipments and pricing pressure.

- Motorcycle segment gross margin declined to 25.3%, down 3.9 percentage points from 29.1%, impacted by approximately $45 million in tariff-related costs.

- Motorcycle segment operating income was $19 million, representing an 84% decline from $116 million in Q1 2025.

- Financial services revenue reached $112 million, falling 54% year over year following the transition to a capital-light operating model.

- Financial services operating income margin was 19.9% during the quarter.

- Electric motorcycle segment revenue totaled $5 million, increasing 87% year over year due to stronger product sales.

- Electric motorcycle operating loss improved to $18 million, narrowing by 11% compared to Q1 2025.

- Cash and cash equivalents stood at $1.8 billion at the end of the quarter.

- Operating cash flow reflected a net use of $228 million, compared to an inflow of $142 million in Q1 2025.

- Share repurchases totaled $128 million, representing approximately 6.6 million shares bought back during the quarter.

- Full-year 2026 guidance for the motorcycle segment has been reaffirmed, with expected operating results ranging from a $40 million loss to a $10 million profit.

Beat or Miss?

| Metric | Reported | Estimated | Difference / Analysis |

| Diluted EPS | $0.22 | $0.22 to $0.34 | Met one consensus; missed Zacks by 36.1% and Public.com estimate by 12% |

| Total Revenue | $1.17 billion | $1.01 billion | Beat by approximately $162 million or 16% |

| HDMC Gross Margin | 25.30% | N/A | Down 3.9 pts YoY; $45M tariff headwind was the primary driver |

| HDMC Operating Income | $19 million | N/A | Down 84% YoY; consensus estimates not publicly available for segment |

| HDFS Operating Income | $22 million | N/A | Capital-light transition materially reduced comparative base |

| North America Retail Units | 23,803 | N/A | Up 14% YoY; US up 16%; management cited as ahead of expectations |

What Leadership Is Saying?

CEO Arthur Starrs

“We’re pleased with our first quarter results, which reflect actions we’ve taken to drive demand and improve dealer health. We saw a 14% increase in retail performance in North America, which drove global retail sales growth of 8%, and achieved a 22% year-over-year reduction in global dealer inventories, as we continue to prioritize aligning wholesale with retail demand. We are energized by the positive early reception to our new RIDE marketing platform, and excited to activate against our new growth strategy, Back to the Bricks.”

CFO Jonathan Root

“Within the first quarter, we had $45 million in tariffs, and we expect the impact to decline sequentially through the remaining quarters consistent with our full-year outlook. At this point in time, we expect the cost of increased tariffs to be in a range of $75 million to $90 million for the full year 2026, which is favorable to what we guided to in our prior quarter.”

Historical Performance

HOG Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | $1,173M | $1,329M | -12% |

| HDMC Revenue | $1,055M | $1,082M | -2% |

| HDFS Revenue | $112M | $245M | -54% |

| LiveWire Revenue | $5M | $3M | 87% |

| Net Income (HDI) | $25M | $133M | -81% |

| Diluted EPS | $0.22 | $1.07 | -79% |

| HDMC Gross Margin | 25.30% | 29.10% | -3.9 pts |

| HDMC Operating Income | $19M | $116M | -84% |

| HDFS Operating Income | $22M | $64M | -65% |

| Global Retail Units | 33,507 | 31,010 | 8% |

| North America Retail Units | 23,803 | 20,892 | 14% |

| HDMC Wholesale Shipments | 37,295 | 38,601 | -3% |

| Global Dealer Inventory | Down 22% YoY | Baseline | -22% |

| Operating Cash Flow | ($228M) | $142M | N/M |

| Cash and Equivalents | $1,805M | $1,931M | -7% |

Competitor Comparison

Q1 2026 vs Q1 2025: HOG vs Key Competitor (Polaris Inc.)

Polaris Inc. (NYSE: PII) is Harley-Davidson’s closest listed US powersports peer; it separated its Indian Motorcycle division in early 2026. Indian Motorcycle was previously the most direct head-to-head competitor to Harley-Davidson in the heavyweight motorcycle market.

| Category | Harley-Davidson (HOG) Q1 2026 | Harley-Davidson (HOG) Q1 2025 | Polaris (PII) Q1 2026 | Polaris (PII) Q1 2025 |

| Revenue | $1,173M | $1,329M (-12% YoY) | $1,659M | $1,536M (+8% YoY) |

| Net Income / (Loss) | $25M | $133M (-81% YoY) | ($47M) | ($67M) (improved 29%) |

| Gross Margin | 25.3% (HDMC) | 29.1% (HDMC) | 20.20% | 16.0% (+4.2 pts) |

| Adjusted EPS | $0.22 diluted | $1.07 | $0.13 adjusted | N/A |

| Key Headwind | $45M tariff costs | Comparison base | ~$240M tariff costs (FY) | Comparison base |

Both companies faced significant tariff headwinds in Q1 2026. Polaris beat its own internal expectations and guidance through margin expansion, while Harley-Davidson beat revenue estimates but saw a sharp operating income decline driven by the HDFS restructuring and tariff costs.

How the Market Reacted?

Harley-Davidson shares (NYSE: HOG) rose approximately 8% on May 5, 2026, the day Q1 results were released, with the stock trading up to $25.08 to $25.12 during the session after closing the prior day around $23.21. The positive market reaction appeared driven primarily by the significant revenue beat versus analyst estimates, the 14% North American retail sales growth, the 22% reduction in dealer inventories, and management’s reaffirmed full-year guidance alongside an upbeat tone about the new “Back to the Bricks” strategic plan.

Despite the stock’s intraday gain, analysts remain mixed on the outlook, with 11 analysts covering the stock split across 3 sell, 5 hold, 2 buy, and 1 strong buy ratings, and a consensus 12-month price target of $21.67, representing downside from current levels. The broader sentiment acknowledged that while retail trends improved, underlying fundamentals including an 81% drop in net income and collapsing operating margins represent challenges the company will need to work through as it executes its new strategic plan.