Introduction

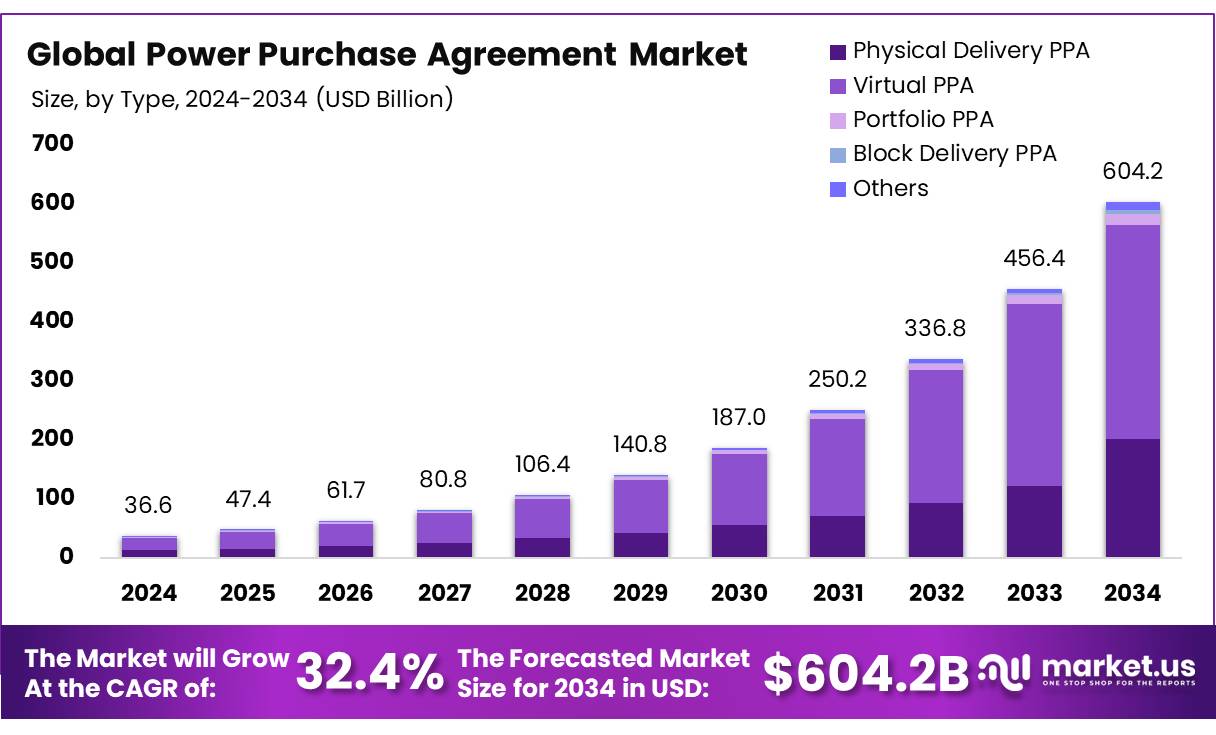

The global Power Purchase Agreement (PPA) Market is projected to grow significantly, increasing from USD 36.6 billion in 2024 to approximately USD 604.2 billion by 2034. This reflects a strong CAGR of 32.4% between 2025 and 2034, highlighting the rising demand for long-term renewable energy procurement solutions across industries.

A Power Purchase Agreement (PPA) is a long-term contract in which a third-party developer installs, owns, and manages an energy system—commonly solar or wind—at a customer’s site. Instead of paying upfront installation costs, the customer agrees to buy the electricity generated by the system for a fixed period, usually 10 to 25 years, often at rates lower than standard utility prices.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

PPAs are widely used in renewable energy projects because they provide immediate cost savings, price stability, and predictable energy expenses. The contract price may include a yearly escalation clause to account for maintenance costs, equipment efficiency changes, and rising electricity tariffs. This structure creates a win-win model: customers secure affordable clean energy, while developers benefit from tax incentives and long-term revenue.

Beyond solar and wind, PPAs are also applied to technologies such as combined heat and power (CHP), making them a flexible framework for broader energy solutions. Their ability to reduce financial risk and support sustainability goals has made them increasingly attractive to commercial and industrial users worldwide.

The global PPA market is being driven by supportive government regulations, renewable energy targets, and strong corporate sustainability commitments. North America—especially United States—continues to lead market expansion through policy support and technological progress, while Europe is also experiencing robust growth, with Germany, Spain, and United Kingdom emerging as key markets for PPA adoption.

Top Market Takeaways

- In 2024, the global power purchase agreement market was valued at US$ 36.6 Billion.

- The global power purchase agreement market is projected to grow at a CAGR of 32.4% between 2024 and 2034.

- By type, the virtual PPAs held a major market share of 59.9% in 2024.

- By location, the off-site segment dominated the global market with 83.9% market share in 2024.

- By category, the corporate segment accounted for 87.1% of the global market.

- Based on the deal type, the wholesale segment led the market with a 61.9% market share in 2024.

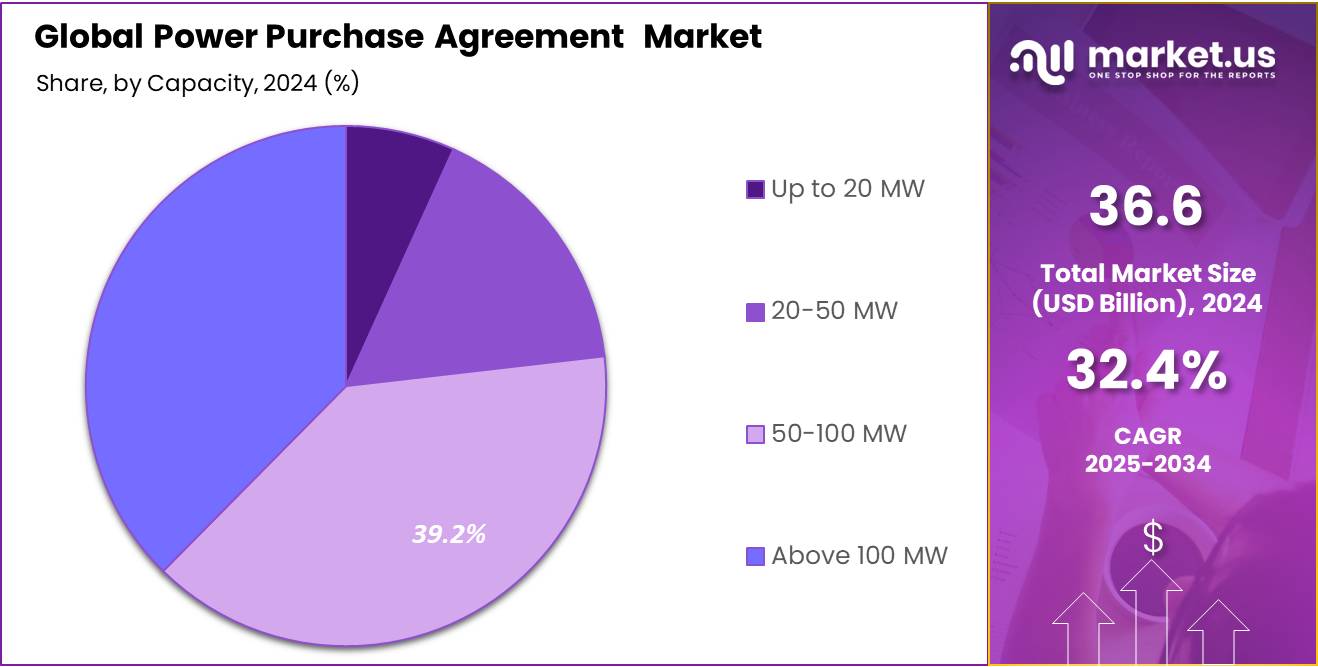

- By capacity, the 50-100 MW segment dominated the market in 2024, accounting for over 39.2% market share.

- By application, the wind segment accounted for the fastest growth, accounting for 37.3% CAGR during the forecasted period.

- Based on the end-use, the commercial segment dominated the market with 49.1% market share in 2024.

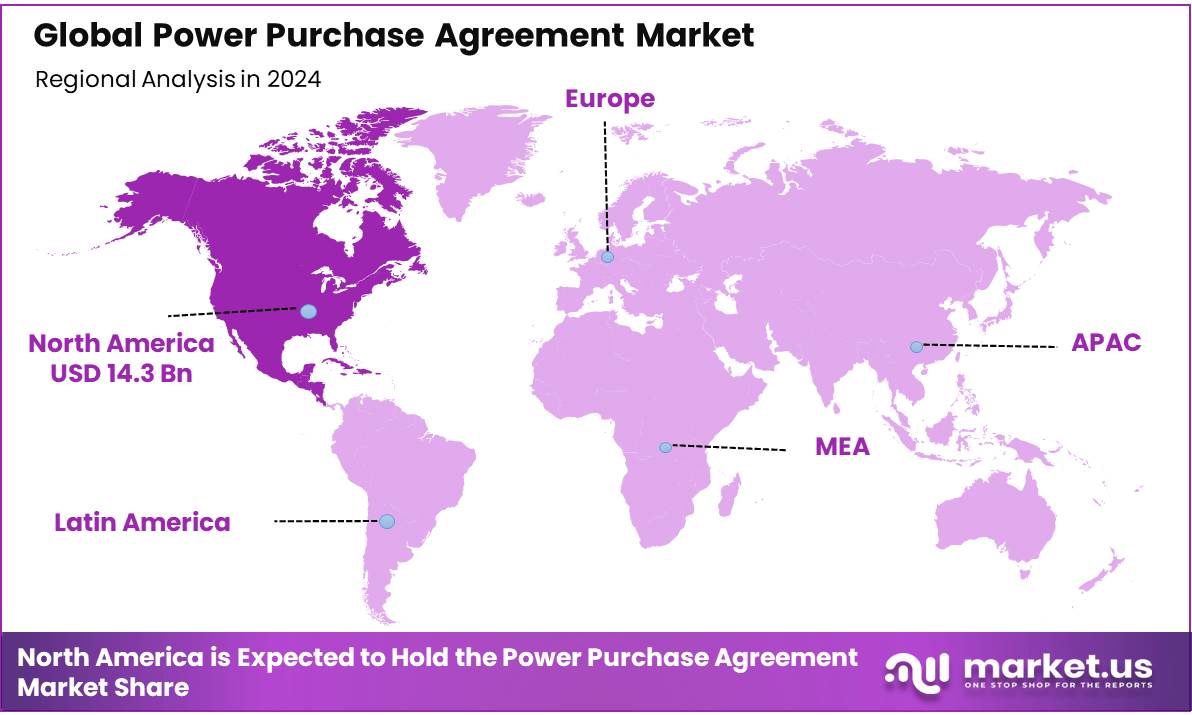

- In 2024, North America dominated the market with the highest revenue share of 39.2%.

- In 2022, According to the American Public Power Association, 36.7 gigawatts (GW) of offsite projects were supported by power purchase agreements signed by more than 167 companies.

- Australia’s Renewable Energy Target (RET) influences PPAs by setting targets for electricity generation from renewable sources. For instance, the country has set a national renewable electricity target of 82% by 2030.

Scope and Research Methodology

The study on Power Purchase Agreements (PPAs) will focus on analysing the design, risk allocation, pricing structure, and performance of long‑term contracts used for grid‑connected power projects, with emphasis on utility and corporate renewable PPAs. The scope will cover different PPA types and key contractual clauses such as term, contracted capacity, pricing and indexation mechanisms, take‑or‑pay provisions, performance guarantees, curtailment rules, termination events, and force majeure.

It will examine how major risks—price, volume, regulatory, grid, counterparty, construction, and operational—are shared between buyer and seller, within a defined geography and time period. Short‑term power trading contracts, spot market transactions, and detailed plant engineering aspects will remain outside the scope, and financial modelling will rely on simplified price and demand assumptions consistent with available data.

The research will follow a mixed‑methods, applied analytical design that combines doctrinal contract review with quantitative financial and risk assessment of PPA cash flows. Secondary data will be collected from standard and model PPAs issued by governments and international agencies, regulatory and tariff orders, competitive bidding guidelines, and academic and industry literature on PPA structures and valuation. Where possible, this will be complemented by semi‑structured interviews with project developers, utilities, lenders, and regulators to understand negotiation practices and perceptions of risk allocation.

By Type Analysis

The Power Purchase Agreement market is segmented into physical delivery PPAs, virtual PPAs, portfolio PPAs, block delivery PPAs, and others. In 2024, the virtual PPA segment was the most lucrative, accounting for 59.9% of the global market, driven by its flexibility, scalability, and competitive pricing. Virtual PPAs enable companies to procure renewable energy from off-site projects without physical proximity to the generation site, making them particularly suitable for businesses with limited on‑site space while providing long‑term price stability in volatile energy markets. The scalability of these agreements allows large renewable projects to be integrated into corporate portfolios, supporting decarbonization targets and energy cost optimization.

By Location Analysis

By location, the PPA market is divided into on‑site and off‑site agreements, with the off‑site segment dominating at 83.9% share in 2024. Off‑site PPAs allow buyers to source renewable electricity from geographically distant, resource‑rich regions where generation costs are lower, helping them overcome on‑site constraints such as limited space, grid integration challenges, and upfront infrastructure requirements. This model supports large‑scale procurement and often yields more competitive pricing, enhancing both sustainability performance and operating cost reduction.

By Category Analysis

The market is further segmented by category into corporate, government, and others, with corporate buyers clearly dominating. In 2024, the corporate segment captured 87.1% of total PPA revenues and is projected to grow at a CAGR of about 32.8% over the forecast period, reflecting strong adoption of renewable energy by businesses seeking to cut emissions and lock in long‑term energy prices. Corporations increasingly use PPAs as strategic hedging instruments against energy price volatility while signalling commitment to sustainability and ESG goals, a trend reinforced by supportive policies and improving renewable technology economics.

By Deal Type Analysis

By deal type, the PPA market is segmented into wholesale, retail, and others, with the wholesale segment holding a 61.9% share in 2024. Wholesale PPAs appeal to large energy purchasers and utilities because they enable the procurement of substantial volumes of electricity at predictable rates, typically from utility‑scale renewable projects that deliver economies of scale. These agreements are crucial for project developers, as they secure long‑term revenue streams, enhance bankability, and attract investment into new capacity. Regulatory support for large‑scale renewables and increasing corporate sustainability commitments further reinforce wholesale PPA growth.

By Capacity Analysis

Capacity‑wise, the market is divided into up to 20 MW, 20–50 MW, 50–100 MW, and above 100 MW, with the 50–100 MW band emerging as the leading segment at a 39.2% market share in 2024. This range offers an attractive balance between scale and manageability: projects are large enough to capture economies of scale and reduce per‑MW costs, yet small enough to integrate more smoothly into existing grid infrastructure and permitting frameworks than very large plants. The segment’s appeal is illustrated by deals such as the 2024 PPA between Evonik and EnBW for 50 MW of offshore wind from the “He Dreiht” project over 15 years, supplementing an earlier 100 MW contract.

By Application Analysis

By application, the market is segmented into solar, wind, geothermal, hydropower, carbon capture and storage, and others, with solar PPAs clearly in the lead. In 2024, solar PPAs accounted for about 50.9% of total PPA revenues, reflecting their predictable pricing, scalability, and rapidly declining installation costs. Solar contracts are particularly attractive to commercial and industrial buyers seeking to hedge against volatile power prices while meeting decarbonization commitments. Technological improvements in photovoltaic modules have raised efficiency and further enhanced project economics, while competitive PPA pricing continues to encourage adoption; for instance, average solar PPA prices in North America dipped slightly to about USD 49.09 per MWh in Q2 2024.

By End-Use Analysis

By end‑use, the PPA market is segmented into residential, commercial, and industrial customers, with the commercial sector holding the largest share at 49.1% in 2024. Commercial entities typically exhibit higher and more consistent electricity demand than residential users, creating a strong need for long‑term, stable procurement arrangements that PPAs are well suited to provide. These agreements enable businesses to lock in predictable energy costs, reduce exposure to market price volatility, and demonstrate progress on sustainability and net‑zero commitments.

Regional Analysis: North America

In 2024, North America dominated the Power Purchase Agreement (PPA) market, accounting for 39.2% of the total market share. The region’s leadership is largely supported by strong renewable energy policies and favorable regulatory frameworks.

Governments across United States and Canada have introduced incentives, tax benefits, and clean energy mandates that encourage both energy producers and consumers to adopt renewable power solutions. These supportive measures have made PPAs an increasingly attractive option for securing long-term, cost-effective clean electricity.

According to American Clean Power Association, commercial and industrial (C&I) companies in the US signed nearly 20 GW of clean energy PPAs in 2022, marking a record level of corporate power purchasing activity in the country. This milestone highlights the growing role of businesses in driving renewable energy demand through long-term power agreements.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Key Players Analysis

The global Power Purchase Agreement (PPA) market is highly competitive, with major players such as General Electric, Siemens AG, Shell Plc, and Statkraft playing a central role. These companies significantly influence market growth through their wide range of renewable energy services, project development capabilities, and global operational networks.

These leading firms are helping shape the renewable energy ecosystem by supporting the development, financing, and operation of clean energy projects worldwide. Their market strength is driven by factors such as global presence, advanced technology expertise, and the ability to build strategic partnerships and long-term power agreements.

Companies like Iberdrola, S.A., Ørsted A/S, and Enel Global Trading have been especially influential in expanding the PPA market. Their strong renewable portfolios and international reach have accelerated adoption across multiple regions and industries.

The competitive landscape is further strengthened by specialized providers such as Ameresco and Ecohz, which deliver customized sustainability and energy procurement solutions. As the market continues to grow, these players are expected to drive innovation, increase renewable capacity, and support the global shift toward a more sustainable energy future.

Top Key Players in the Market

- General Electric

- Siemens AG

- Shell Plc

- Statkraft

- Fairdeal Greentech India Pvt. Ltd.

- Ameresco

- RWE AG

- Enel Global Trading

- Ecohz

- Greensphere Cleantech Services Private Limited

- Iberdrola, S.A.

- Ørsted A/S

- Renew Energy Global PLC

- Drax Energy Solutions Limited

- Other Key Players

Recent Developments

In October 2024, Statkraft and Chiesi Group entered into a 10-year renewable power purchase agreement to provide over 30 GWh of clean electricity annually. This partnership is expected to help Chiesi secure long-term electricity price stability while significantly lowering CO₂ emissions—an impact comparable to powering more than 12,500 households each year.

Also in October 2024, RWE signed its first US power purchase agreement with the state of New York. The agreement covers electricity generated from 1,300 MW of offshore wind capacity, marking a major milestone in RWE’s expansion in the US renewable energy market. The project was awarded to the company’s joint venture with National Grid Ventures.

In September 2024, Shell Energy Europe finalized a 15-year PPA with HANSAINVEST Real Assets to secure 600 MW of capacity at Witznitz Energy Park, the largest solar project in Germany. Developed by MOVE ON Energy, the agreement also includes Shell supplying electricity from 323 MW of the solar capacity to Microsoft, reinforcing the growing role of long-term PPAs in corporate clean energy strategies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 36.6 Bn |

| Forecast Revenue (2034) | US$ 604.2 Bn |

| CAGR (2024-2034) | 32.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Physical Delivery PPA, Virtual PPA, Portfolio PPA, Block Delivery PPA, and Others), By Location (On-site and Off-site), By Category (Corporate, Government, and Others), By Deal Type (Wholesale, Retail, and Others), By Capacity (Up to 20 MW, 20-50 MW, 50-100 MW, and Above 100 MW), By Application (Solar, Wind, Geothermal, Hydropower, Carbon Capture and Storage, and Others), By End-Use (Residential, Commercial, and Industrial) |

| Regional Analysis | North America: The US and Canada; Europe: Germany, France, The UK, Italy, Spain, Russia & CIS, and the Rest of Europe; APAC: China, India, Japan, South Korea, ASEAN, and the Rest of APAC; Latin America: Brazil, Mexico, and Rest of Latin America; Middle East & Africa: GCC, South Africa, and Rest of Middle East & Africa. |

| Competitive Landscape | General Electric, Siemens AG, Shell Plc, Statkraft, Fairdeal Greentech India Pvt. Ltd., Ameresco, RWE AG, Enel Global Trading, Ecohz, Greensphere Cleantech Services Private Limited, Iberdrola S.A., Ørsted A/S, Renew Energy Global PLC, Drax Energy Solutions Limited and Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |