Veralto reported Q1 2026 diluted EPS of $1.02 (adjusted EPS $1.07) on sales of $1.422 billion, reflecting 6.7% YoY growth and stronger margins, while raising full year EPS guidance; stock reaction will depend on the upcoming earnings call and after-hours movement.

About Veralto

Veralto Corporation(NYSE: VLTO) is a global provider of essential technology solutions focused on water quality and product quality, helping customers deliver clean water, safe food, and trusted consumer goods. Headquartered in Waltham, Massachusetts, the company generates approximately $5.5 billion in annual sales and operates a portfolio of industry leading brands serving critical infrastructure and industrial end markets.

Veralto was formed via separation from Danaher in 2023 and now runs as a standalone public company dedicated to Safeguarding the World’s Most Vital Resources. The company employs roughly 17,000 associates worldwide and leverages the Veralto Enterprise System to drive continuous improvement, productivity, and innovation across its businesses.

While the latest release does not specify Veralto’s current market cap, Q1 2026 results show net earnings of $254 million and an operating margin of 23.8%, underscoring a solid profitability profile relative to industrial peers. Management also emphasizes strong free cash flow generation, with trailing twelve month free cash flow margin at 18.6%, supporting ongoing acquisitions and share repurchases.

Top Financial Highlights

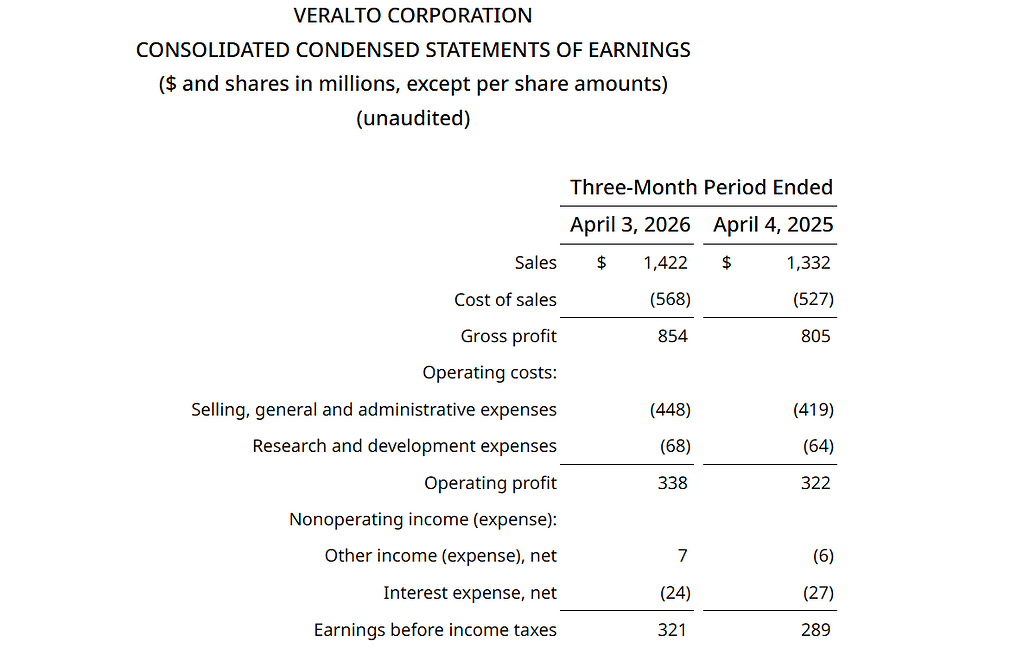

- Q1 2026 sales were $1,422 million, up 6.7% year over year, with non GAAP core sales growth of 1.9%.

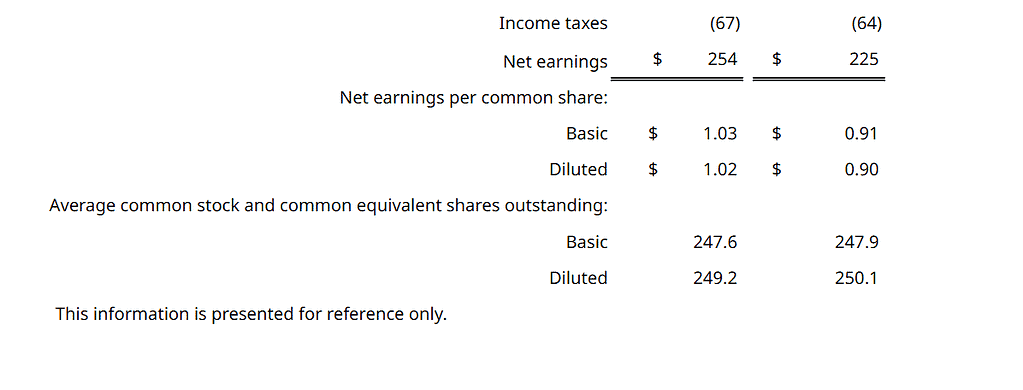

- Net earnings were $254 million, compared with $225 million in Q1 2025.

- Diluted EPS was $1.02, versus $0.90 in the prior year period.

- Adjusted net earnings were $266 million, or adjusted diluted EPS of $1.07, up from $237 million and $0.95 a year ago, roughly 13% EPS growth.

- Operating profit was $338 million, yielding an operating margin of 23.8%, while adjusted operating profit was $357 million with a 25.1% adjusted margin.

- Gross profit was $854 million on cost of sales of $568 million, compared to gross profit of $805 million a year earlier.

- Operating cash flow was $182 million, up from $157 million in Q1 2025.

- Free cash flow was $170 million, an increase from $142 million, implying ~19.5% YoY growth.

- Year to date capital deployment was roughly $1 billion, including about $620 million for the In Situ and GlobalVision acquisitions and $300 million of share repurchases, equal to 1.3% of shares outstanding.

- Veralto’s Water Quality segment delivered total sales growth of 10.1% and core sales growth of 3.8%.

- The Product Quality and Innovation segment posted total sales growth of 1.7%, with core sales down 1.0%.

- Management initiated a cost optimization program expected to incur $85–$105 million in charges and deliver annual savings of $65–$75 million by 2028.

- Q2 2026 guidance calls for core sales growth of 3.0%–4.0%, adjusted operating margin of about 23.5%, and adjusted diluted EPS between $0.96 and $1.00.

- Full year 2026 guidance now assumes core sales growth of 3.0%–4.5%, adjusted operating margin expansion of ~25 bps, and adjusted diluted EPS of $4.20–$4.28, up from prior $4.10–$4.20.

- The company targets free cash flow conversion of approximately 100% of GAAP net earnings for 2026.

Beat or Miss?

Analyst commentary indicates that Q1 2026 revenue modestly exceeded consensus expectations, while EPS also came in ahead of prior guidance ranges.

| Metric | Reported | Difference / Analysis |

| Revenue | $1.422 billion | Above market expectations of about $1.40 billion, implying a small top line beat. |

| Diluted EPS (GAAP) | $1.02 | Above prior full year EPS run rate implied by earlier 2026 guidance; YoY growth from $0.90. |

| Adjusted EPS (non GAAP) | $1.07 | Roughly 13% YoY growth versus $0.95; reflects strong margin performance. |

| Core Sales Growth | 1.90% | Positive but modest; indicates mixed demand with stronger Water Quality offsetting softer Product Quality. |

| Adjusted Operating Margin | 25.10% | Slightly above prior year 25.0%, showing stable to improving profitability. |

What Leadership Is Saying?

“We are off to a strong start in 2026, reflecting the effectiveness of the Veralto Enterprise System, the essential role of our products and services in customers’ operations, and the resilience of our end markets.” – Jennifer L. Honeycutt, President and Chief Executive Officer, Veralto

“In the first quarter, we delivered approximately 7% sales growth and 13% adjusted earnings per share growth while continuing to invest in commercial execution, productivity and innovation.” – Jennifer L. Honeycutt, President and Chief Executive Officer, commenting on margins and EPS performance

Historical Performance

Veralto’s Q1 2026 results show healthy year over year growth in revenue, earnings, and cash generation compared with Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $1,422 million | $1,332 million | ~6.7% increase, driven by Water Quality strength. |

| Net Earnings | $254 million | $225 million | ~12.9% increase, reflecting margin expansion and lower interest expense. |

| Operating Expenses (SG&A + R&D) | $516 million (448 + 68) | $483 million (419 + 64) | ~6.8% increase, roughly in line with sales growth, preserving margins. |

| Operating Profit | $338 million | $322 million | ~5.0% increase, with operating margin at 23.8% vs 24.2%. |

| Free Cash Flow | $170 million | $142 million | ~19.5% increase, aided by higher earnings and lower capex. |

How the Market Reacted?

The Q1 2026 press release and related materials focus on fundamentals and guidance but do not specify how Veralto’s share price traded immediately after the announcement. External previews had highlighted skepticism following a prior quarter sell off, suggesting that positive revenue and EPS surprises plus raised full year guidance could support a more constructive sentiment if sustained.

Taken together, the report reads as fundamentally bullish, with solid top line growth, improving adjusted EPS, and enhanced 2026 guidance, even as core sales growth remains modest. Actual stock performance will be shaped by the tone on the earnings call, updated analyst models, and how investors weigh the cost optimization program and acquisition spending against near term growth.