Stellantis reported Q1 2026 adjusted diluted EPS of €0.21 (vs ~€0.56 expected) and net revenues of €38.1 billion (roughly $44.4 billion), up 6% year-over-year. Adjusted operating income surged to €960 million, nearly triple the year-ago figure and well above analyst estimates of €568 million. Despite the operational beat, shares dropped up to 10% on April 30, settling at roughly 6% lower by end of session, as investors focused on negative free cash flow and earnings quality concerns.

About Stellantis

Stellantis N.V. (NYSE: STLA / Euronext Milan: STLAM / Euronext Paris: STLAP) is one of the world’s largest automotive manufacturers, formed on January 17, 2021, through the merger of Fiat Chrysler Automobiles and France’s PSA Group. The company is legally headquartered in Hoofddorp, Netherlands, with CEO operations based out of Auburn Hills, Michigan.

Stellantis operates a portfolio of 14 iconic vehicle brands including Jeep, Ram, Fiat, Peugeot, Citroën, Alfa Romeo, Maserati, Dodge, Chrysler, Opel, Vauxhall, DS Automobiles, Lancia, and Abarth, plus two mobility brands: Free2move and Leasys. With a commercial presence in more than 130 markets worldwide, the company employs approximately 260,000 people across six global regions. As of May 3, 2026, Stellantis carries a market capitalization of approximately $20.7 billion. The current trailing twelve-month P/E ratio is approximately -6.14, reflecting the full-year loss recorded in 2025.

Top Financial Highlights

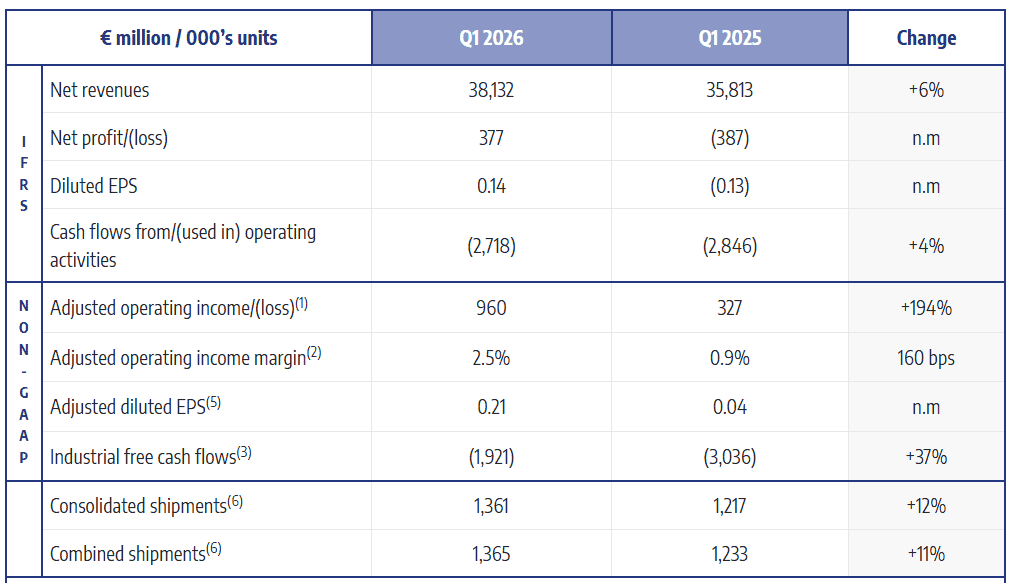

- Net revenues reached €38.1 billion (~$44.4 billion), up 6% year-over-year from €35.8 billion in Q1 2025

- Net profit recovered to €377 million, reversing a net loss of €387 million in Q1 2025

- Diluted EPS: €0.14 vs -€0.13 in Q1 2025

- Adjusted diluted EPS: €0.21, up from €0.04 a year ago

- Adjusted operating income (AOI) surged to €960 million, up +194% from €327 million in Q1 2025

- AOI margin improved to 2.5%, up 160 basis points from 0.9% a year earlier, with most regions positive

- Industrial free cash flows improved 37% to -€1.9 billion, versus -€3.0 billion in Q1 2025, despite ~€0.7 billion in cash outflows from H2 2025 charges

- Cash flows from operating activities: -€2.72 billion, vs -€2.85 billion in Q1 2025

- Consolidated shipments rose 12% to 1,361 thousand units

- North America AOI swung positive to €263 million from a prior-year loss; U.S. market share reached 7.9%, up 80 bps YoY

- Ram U.S. sales up approximately 20% year-over-year, the highest Q1 since 2023

- EU30 market share reached 17.5% (+20 bps YoY); including Leapmotor, 18.1% (+70 bps)

- Industrial available liquidity ended at €44.1 billion, representing 28% of trailing 12-month net revenues

- €5 billion in hybrid perpetual notes issued in March 2026 across three tranches to reinforce balance sheet flexibility

- FY 2026 Guidance confirmed: Mid-single-digit net revenue growth, low-single-digit AOI margin, improved industrial free cash flows YoY; positive industrial free cash flows expected in 2027

Beat or Miss?

| Metric | Reported | Estimate | Difference / Analysis |

| Adjusted Operating Income (AOI) | €960 million | €568 million (avg. consensus) | Beat by ~€392M (+69%) |

| Adjusted Diluted EPS | € 0.21 | ~€0.56 (consensus) | Missed by ~€0.35; raised earnings quality concerns |

| Net Revenue | €38.1 billion | N/A | No qualifying analyst consensus available |

| Net Profit | €377 million | N/A | Swing from -€387M loss in Q1 2025 |

| Industrial Free Cash Flow | -€1.9 billion | N/A | 37% improvement YoY, but still negative |

| Full-Year Guidance | Confirmed unchanged | Investors hoped for a raise | Guidance not raised; viewed as mild disappointment |

What Leadership Is Saying?

CEO Antonio Filosa on vision and customer focus:

“As we initiate quarterly reporting, the first three months of 2026 reflect the early results of our actions to return Stellantis to sustainable, profitable growth. The products we launched in 2025 have been well received and we are confident that the 10 new vehicles planned for 2026 will build on this momentum. Our priority is clear: to put our customers back at the center of everything we do.”

CEO Antonio Filosa on execution discipline (post-results media call):

“We are on a path of continued improvement, just as we demonstrated this quarter. We will advance quarter by quarter and year by year. Improvement is evident, we have commercial momentum, and we are disciplined in our pricing and cost management. This gives me confidence that we are on a lengthy journey, but one of steady, incremental progress.”

CFO Joao Laranjo on financials, costs, and guidance:

“Industrial costs are expected to be a tailwind for the full year despite raw material headwinds, citing manufacturing improvements from higher volumes, product-cost opportunities, and expected warranty improvements following actions taken last year. On capital spending, 2026 CapEx is expected to be slightly below 7% of net revenues. We confirmed our 2026 financial guidance as outlined on February sixth, calling for improvement in net revenues, margins, and industrial free cash flow.”

Historical Performance

Stellantis: Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Net Revenue | €38.1 billion | €35.8 billion | +6% |

| Net Profit / (Loss) | €377 million | -€387 million | N/M (swing to profit) |

| Adjusted Operating Income | €960 million | €327 million | +194% |

| AOI Margin | 2.50% | 0.90% | +160 bps |

| Diluted EPS | € 0.14 | -€ 0.13 | N/M |

| Adjusted Diluted EPS | € 0.21 | € 0.04 | N/M |

| Consolidated Shipments | 1,361K units | 1,217K units | +12% |

| Industrial Free Cash Flow | -€1.9 billion | -€3.0 billion | +37% improvement |

Competitor Performance

Ford Motor Company: Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | $43.3 billion | ~$40.8 billion | +6% |

| Net Income | $2.5 billion | $471 million | +431% |

| Adjusted EBIT | $3.5 billion | ~$1.1 billion | +218% |

| Full-Year Adj. EBIT Guidance | $8.5B to $10.5B | $8B to $10B (prior) | Raised |

General Motors: Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | $43.6 billion | $44.0 billion | -0.9% |

| Net Income (stockholders) | $2.63 billion | $2.78 billion | -5.7% |

| EBIT-Adjusted | $4.25 billion | $3.49 billion | +21.9% |

| EPS (Diluted, Adjusted) | $3.70 | N/A | Beat consensus of $2.62 |

How the Market Reacted?

Shares of Stellantis (NYSE: STLA) dropped as much as 10% intraday on April 30, 2026, before paring losses to close approximately 6% lower. The stock opened at $7.18 against a prior close of $7.70, as investors reacted to a material adjusted EPS miss of approximately €0.35 versus consensus and ongoing negative industrial free cash flow.

Analysts flagged that the headline AOI beat did not translate into a proportionate improvement in per-share earnings, raising concerns about tariff-adjusted items and one-time factors inflating the operational figure. As of May 4, 2026, Wall Street maintained a consensus Hold rating with an average price target of approximately $11.12, while shares hovered near $7.26, a dramatic pullback from highs near $23 seen in April 2024.