Introduction

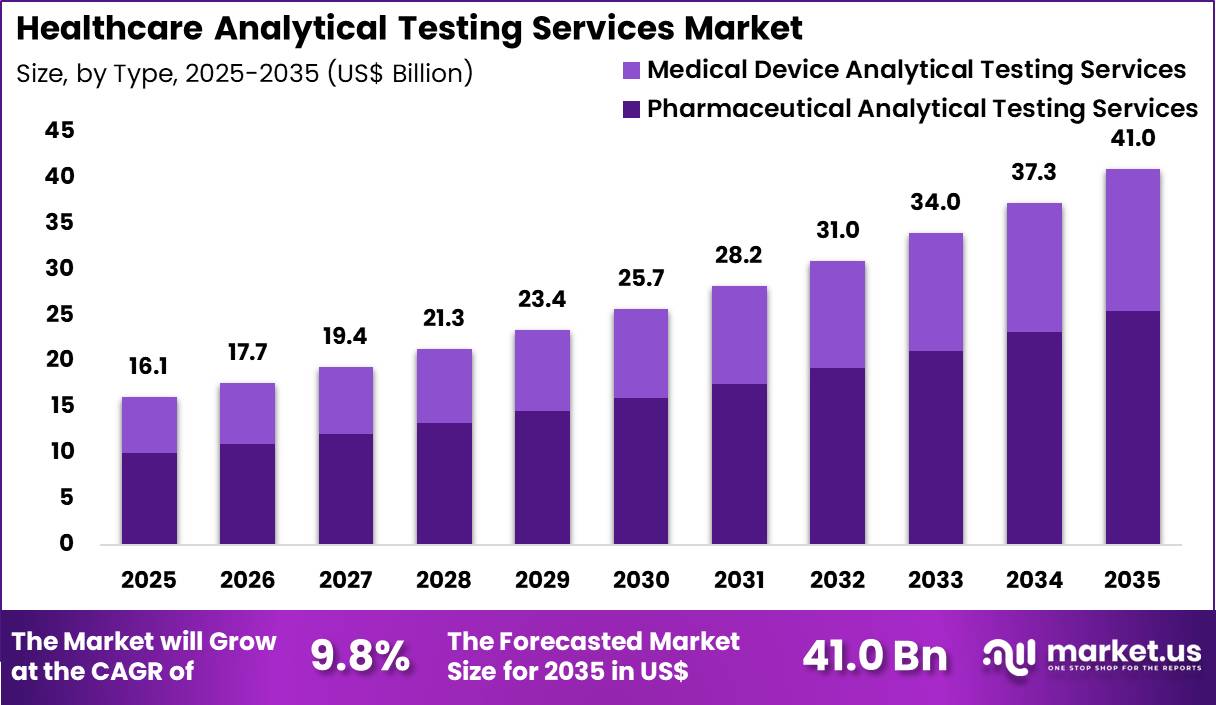

The Global Healthcare Analytical Testing Services Market is projected to grow from US$ 16.1 Billion in 2025 to US$ 41.0 Billion by 2035, registering a robust CAGR of 9.8%. This expansion reflects rising outsourcing of bioanalytical, stability, and microbiological testing as regulatory requirements become more stringent worldwide.

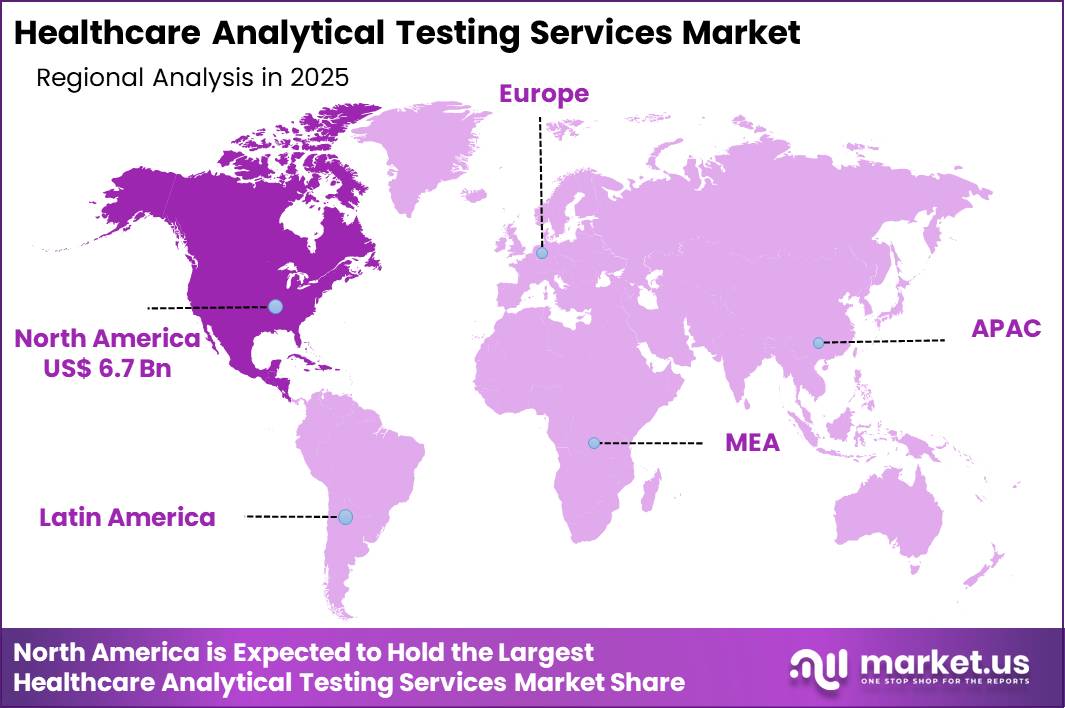

Pharmaceutical analytical testing services account for 62.3% of the market, underscoring the importance of impurity profiling, method validation, and raw material testing across complex biologics and small molecules. With North America holding 41.5% share and Asia Pacific expected to post the fastest CAGR, healthcare analytical testing services are becoming a critical backbone for global life sciences innovation, quality assurance, and timely drug approvals.

Request For Sample Report Here @ https://market.us/report/global-healthcare-analytical-testing-services-market/free-sample/

Key Takeaways

- In 2025, the market generated revenue of US$ 16.1 billion and is projected to reach US$ 41.0 billion by 2035, registering a CAGR of 9.8% during the forecast period.

- By type, the market is segmented into pharmaceutical analytical testing services and medical device analytical testing services, with pharmaceutical analytical testing services leading at 62.3% share.

- North America dominated the market, accounting for a 41.5% revenue share.

Report Scope

| Report Features | Description |

| Market Value (2025) | US$ 16.1 Billion |

| Forecast Revenue (2035) | US$ 41.0 Billion |

| CAGR (2026-2035) | 9.80% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Pharmaceutical Analytical Testing Services (Bioanalytical Testing (PK/PD, Bioavailability, Biomarkers), Method Development and Validation, Stability Testing, Raw Material & Excipient Testing, Batch Release Testing and Others) and Medical Device Analytical Testing Services (Extractable and Leachable (E&L), Material Characterization, Physical Testing, Bioburden & Sterility Testing and Others)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific, SGS SA, Charles River Laboratories, LabCorp, Eurofins Scientific, ICON plc, Toxikon, Syneos Health, Pace Analytical, Intertek, WuXi AppTec, Almac Group, BioAgilytix, QPS Holdings. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

How Growth Is Impacting the Economy ?

Expansion of healthcare analytical testing services is reinforcing the broader life sciences economy by enabling faster, more compliant drug development and accelerating commercialization timelines for innovative therapies. As pharmaceutical and biotech companies outsource complex assays, they reduce capital expenditure on in-house labs while redirecting investment toward high-value R&D and clinical programs. This model stimulates job creation in specialized contract laboratories, spanning analytical chemists, bioinformaticians, and quality professionals, which supports high-skill employment clusters in key regions.

Macroeconomic factors such as inflation and higher interest rates raise operating costs for analytical labs, but mandatory regulatory testing helps sustain demand and underpins resilient long-term growth. Geopolitical tensions and tariffs on analytical equipment can temporarily pressure margins, yet they also encourage regional capacity building and supply diversification.

As governments tighten Good Manufacturing Practice enforcement, third-party testing becomes a structural requirement, embedding these services deeper into national healthcare and industrial policy. Overall, the sector’s steady 9.8% CAGR contributes to stable revenue streams, technology investment, and innovation spillovers across diagnostics, medical devices, and biopharma manufacturing ecosystems.

Key Segmentation

Pharmaceutical analytical testing services accounted for 62.3% of the healthcare analytical testing services market, driven by increasing drug development activity and stringent regulatory requirements. Pharmaceutical companies rely on specialized laboratories for impurity profiling, stability testing, bioanalytical assessments, and bioequivalence studies to ensure product safety and compliance.

The growing pipeline of biologics, biosimilars, and complex formulations has increased analytical complexity, strengthening the demand for outsourced testing services. Regulatory authorities mandate validated methodologies, detailed documentation, and consistent quality monitoring across development and manufacturing stages, further supporting segment growth.

Expansion in therapeutic areas such as oncology, rare diseases, and advanced therapies has also increased testing volumes. Cost optimization strategies encourage pharmaceutical sponsors to outsource analytical functions instead of building in-house capabilities.

Additionally, the rise in global and cross-border clinical trials is promoting centralized laboratory services. As pharmaceutical innovation accelerates and regulatory scrutiny intensifies, pharmaceutical analytical testing services are expected to maintain their leading market position.

Analyst Viewpoint

The healthcare analytical testing services market is currently in a strong, demand-driven cycle, underpinned by robust pipelines in oncology, rare diseases, and advanced biologics that require sophisticated testing at every development stage. Despite cost and geopolitical headwinds, outsourcing remains structurally attractive as sponsors seek flexible capacity and specialized expertise rather than capital-intensive internal labs.

Over the next decade, analysts anticipate that AI-integrated workflows, real-time release testing, and multi-attribute monitoring will significantly enhance lab productivity and data quality. Growth opportunities in cell and gene therapy analytics, companion diagnostics, and high-throughput bioanalytical platforms are expected to expand addressable revenue pools and support sustained double-digit gains in select subsegments.

Overall, the market is positioned for resilient, innovation-led expansion as regulatory expectations tighten and precision medicine scales globally.

Use Cases and Growth Factors

| Use Case / Growth Lever | Description | Growth Factor Contribution |

| Biologics impurity profiling | High‑resolution mass spectrometry to detect host cell proteins, residual DNA, and process contaminants in biologics. | Rising biologics pipelines and strict purity specifications drive recurring testing demand. |

| Stability & degradation studies | Forced degradation and long‑term stability testing for small molecules and complex formulations. | Essential for shelf‑life determination and regulatory submissions, boosting outsourced workloads. |

| Cell & gene therapy analytics | Identity, purity, and potency testing for viral vectors and cell‑based products. | Rapid growth in regenerative medicine creates high‑value, specialized testing needs. |

| Medical device E&L and sterility | Extractables/leachables, bioburden, and sterility assessments for devices and packaging. | Stricter device regulations and complex materials increase testing intensity. |

| Companion diagnostics validation | Analytical validation of biomarker‑based assays for patient stratification. | Expansion of precision oncology and targeted therapies fuels diagnostic testing volumes. |

Strategies for Businesses

- Build long-term strategic partnerships with accredited analytical labs to secure priority access, predictable pricing, and harmonized global quality standards.

- Diversify the supplier base across North America, Europe, and Asia Pacific to mitigate geopolitical, tariff, and logistics risks in critical testing workflows.

- Integrate AI-enabled data analytics, lab automation, and digital LIMS connectivity to improve throughput, reduce errors, and enhance regulatory data integrity.

- Focus internal resources on core research, clinical design, and commercialization while outsourcing high-complexity assays, stability studies, and method validation.

- Co-develop specialized methods for cell and gene therapies, biosimilars, and complex devices with contract labs to shorten time-to-market.

- Invest in risk-based testing strategies and sustainability-oriented methods (e.g., solvent reduction) to control costs while meeting environmental and compliance expectations.

Regional Analysis

North America currently dominates the healthcare analytical testing services market with around 41.5% share, supported by a dense concentration of pharmaceutical, biotechnology, and medical device manufacturers. Strong FDA oversight and high clinical trial activity sustain demand for bioanalytical, stability, microbiological, and sterility testing across development and commercial stages. Europe remains a mature, regulation-driven market where GMP enforcement and extensive generics and biosimilars pipelines underpin consistent outsourcing.

Asia Pacific is projected to register the highest CAGR as regional pharmaceutical production, biosimilar development, and clinical research expand, particularly in China and India. Governments are tightening quality frameworks and GMP alignment with global standards, driving use of contract laboratories for advanced molecular and microbiology analysis. Latin America and the Middle East & Africa offer emerging opportunities as healthcare investment rises and more manufacturers seek compliance with international quality benchmarks.

Business Opportunities

- Specialized testing for cell and gene therapies presents a high-margin opportunity as regenerative medicine pipelines accelerate and regulatory agencies refine guidance on potency and safety assays.

- Expansion of services for biosimilars, complex injectables, and highly potent APIs can differentiate providers with advanced characterization and containment capabilities.

- AI-driven data analytics, anomaly detection, and predictive maintenance for instruments enable new value-added service layers beyond traditional testing.

- Establishing regional centers of excellence in Asia Pacific, Latin America, and the Middle East allows capture of local manufacturing growth while reducing turnaround times.

- Collaboration with diagnostic and companion diagnostic developers can open recurring revenue streams linked to targeted therapy launches.

- Offering end-to-end solutions from method development and validation to batch release and real-time release testing positions providers as strategic long-term partners.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Key Player Analysis

Leading providers in this market are scaling geographically distributed lab networks, enhancing throughput and service breadth to support global pharmaceutical, biotech, and device sponsors. They invest heavily in cutting-edge technologies such as high-resolution mass spectrometry, next-generation sequencing, and process analytical technology to deliver faster, more precise results. Robust quality management systems, international accreditations, and digital reporting platforms enable seamless integration with sponsor systems and regulatory submissions.

Strategic partnerships with biopharma innovators, CROs, and diagnostic developers are common, aligning testing roadmaps with evolving pipelines and securing long-term contracts. Many players pursue targeted acquisitions to expand niche capabilities in bioanalytical, cell and gene therapy, or device testing while consolidating regional presence. Continued technology upgrades, automation, and a customer-centric approach help translate scientific excellence into reliable, scalable operational delivery.

Top Key Players

- Thermo Fisher Scientific, Inc.

- SGS SA

- Charles River Laboratories International, Inc.

- LabCorp

- Eurofins Scientific

- ICON plc

- Toxikon, Inc. (Acquired by Nelson Labs/Sotera)

- Syneos Health

- Pace Analytical Services, LLC

- Intertek Group

- WuXi AppTec

- Almac Group

- BioAgilytix Labs

- QPS Holdings

Recent Developments

- Charles River Laboratories(January 2026): In January 2026, Charles River Laboratories exercised its option to acquire the remaining 79% stake in PathoQuest SAS, a specialist in next-generation sequencing-based GMP quality-control testing, to strengthen its biologics and rapid analytical testing portfolio and embed more in vitro methods into manufacturing release strategies.

- Labcorp (January 2026): In January 2026, Labcorp announced a multi-year plan to build a new, purpose-built central laboratory campus in Brownsburg, Indiana, a 500,000 sq ft facility on a 50 -acre site that will expand its Indianapolis-area lab footprint by about 40% and house central lab, bioanalytical and diagnostics operations to support global clinical trial testing.

- Eurofins Scientific(May 2025): In May 2025, Eurofins Scientific expanded its US bioanalytical laboratory capacity to meet rising biologics and advanced therapy demand, scaling up its biomarker and immunogenicity testing platforms so that biopharma sponsors can consolidate more method development, validation and routine sample analysis within a single Eurofins network hub.

- SGS SA (March 2026): In March 2026, SGS highlighted analytical similarity and functional characterization as the backbone of biosimilar development, signalling continued investment in advanced physicochemical and biofunctional assays that help sponsors de‑risk comparability exercises and satisfy increasingly stringent regulatory expectations around biosimilar analytics.

Conclusion

The healthcare analytical testing services market is positioned for sustained expansion, supported by rising drug complexity, stringent regulatory requirements, and increasing outsourcing by pharmaceutical and biotechnology companies. Strong demand for bioanalytical, stability, and microbiological testing is reinforcing the role of specialized contract laboratories in accelerating compliant product development.

North America maintains leadership, while Asia Pacific is emerging as a high-growth hub driven by expanding manufacturing and clinical activity. Technological advancements, including AI-enabled analytics and high-throughput platforms, are expected to enhance efficiency and data integrity. Overall, the market is projected to deliver resilient, innovation-driven growth, supporting global life sciences development and quality assurance.