Disclaimer: This press release/article is provided by a third party, which is solely responsible for its content. It is published on Sci-tech Today exactly as received from the issuing organization, without any edits, verification, or endorsement by Sci-tech Today.

Sci-tech Today does not guarantee the accuracy, completeness, or reliability of the information. Readers are advised to independently verify all information and do their research before acting on it or investing any money. Sci-tech Today is not responsible for any financial loss that may result from reliance on this content.

Screenless Laptop Market Size

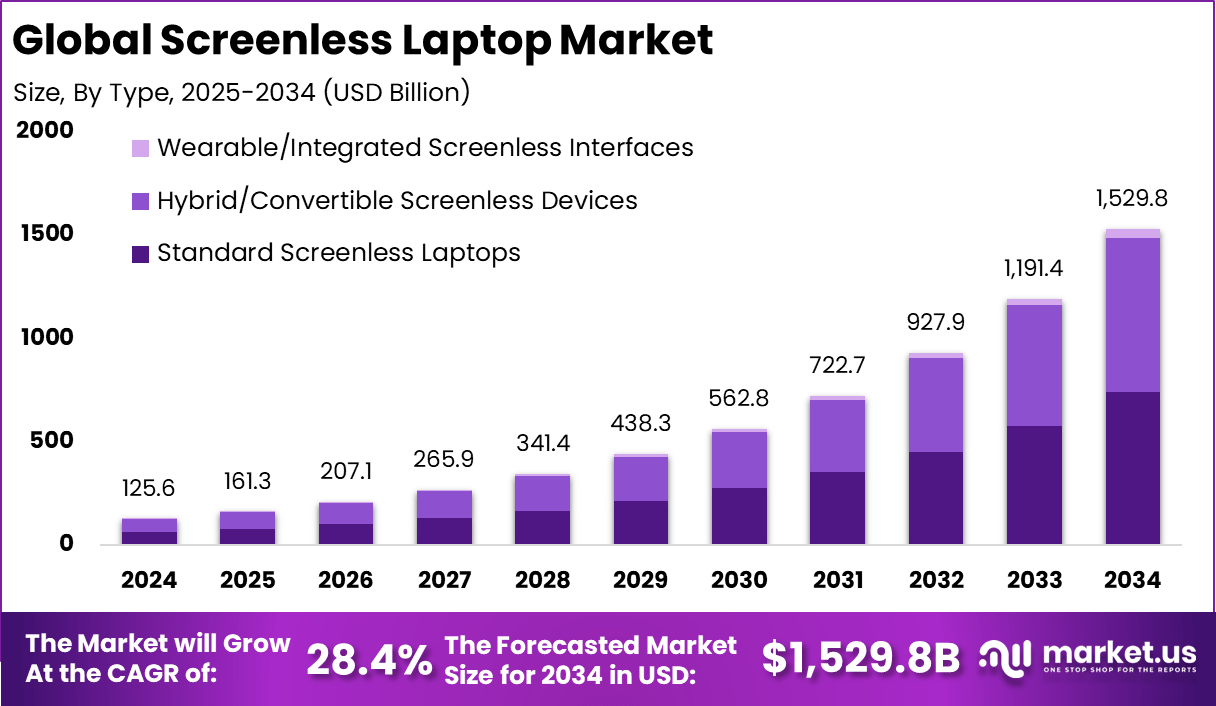

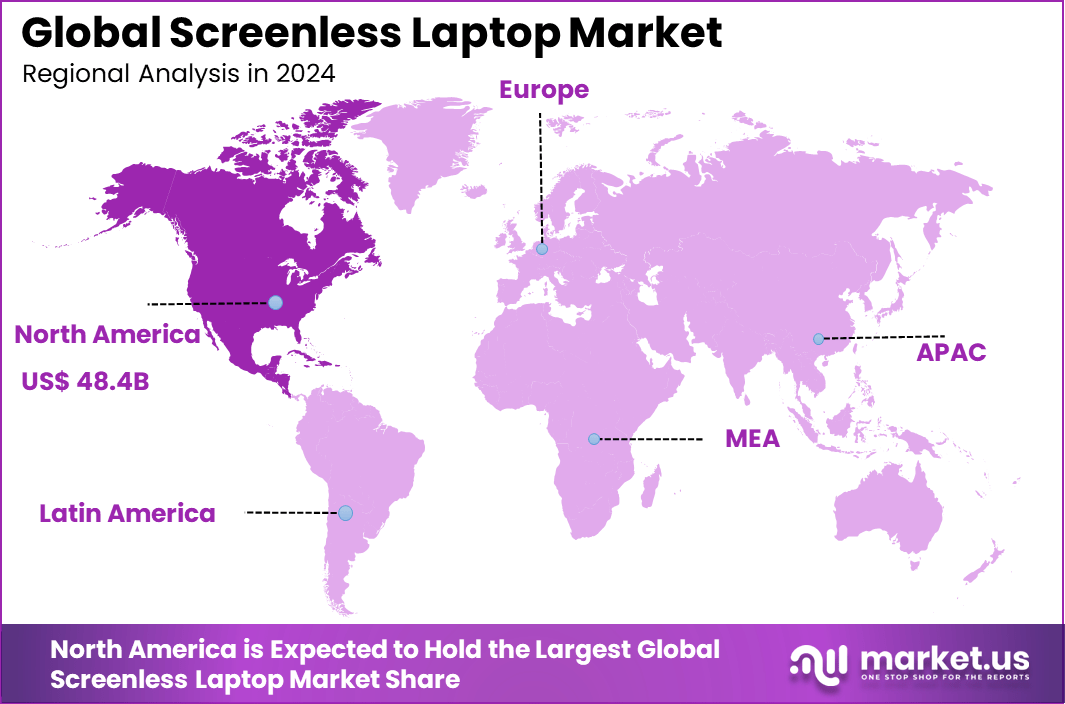

According to Market.us, The global screenless laptop market is anticipated to reach a value of USD 1,529.8 billion by 2034, up from USD 161.3 billion in 2025, reflecting a compound annual growth rate (CAGR) of 28.4% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing over38.6% of the market share, with revenue totaling USD 48.4 billion.

The Screenless Laptop market refers to a subset of computing devices that eliminate the traditional integrated display and instead use alternative visual output technologies such as augmented reality glasses, holographic projection, or external screens to present information to the user. These systems maintain the full computing power of a conventional laptop while reducing bulk and enhancing portability by decoupling the display from the device’s main body. The concept is rooted in advances in screenless display technologies that project or present data without conventional flat panels, offering new interaction models for mobile computing.

Driving factors for the Screenless Laptop market are closely linked to innovation in display technology and the growing demand for lightweight, flexible computing solutions. As users and enterprises seek devices that support dynamic work environments, the ability to offload display functionality into wearable or projective technologies has become attractive. Portability, enhanced privacy when working in public settings, and the potential for expansive virtual workspaces contribute to this trend. These motivations are reinforced by improvements in augmented reality and spatial computing that enable immersive visual interfaces without built‑in screens.

Gain Access to 2026 Market Intelligence for More Informed Business Strategies – Request a Sample

Top Market Takeaways

- Standard screenless laptops led with a 48.5% share, reflecting early adoption of familiar form factors without integrated displays.

- Projection-based interfaces accounted for 40.6%, driven by demand for flexible and portable display solutions in personal and professional settings.

- Personal and home use represented 36.5%, as consumers embraced screenless devices for minimal setups, space efficiency, and privacy-focused computing.

- Online sales dominated distribution with 58.4%, supported by direct-to-consumer channels, wider product availability, and competitive pricing.

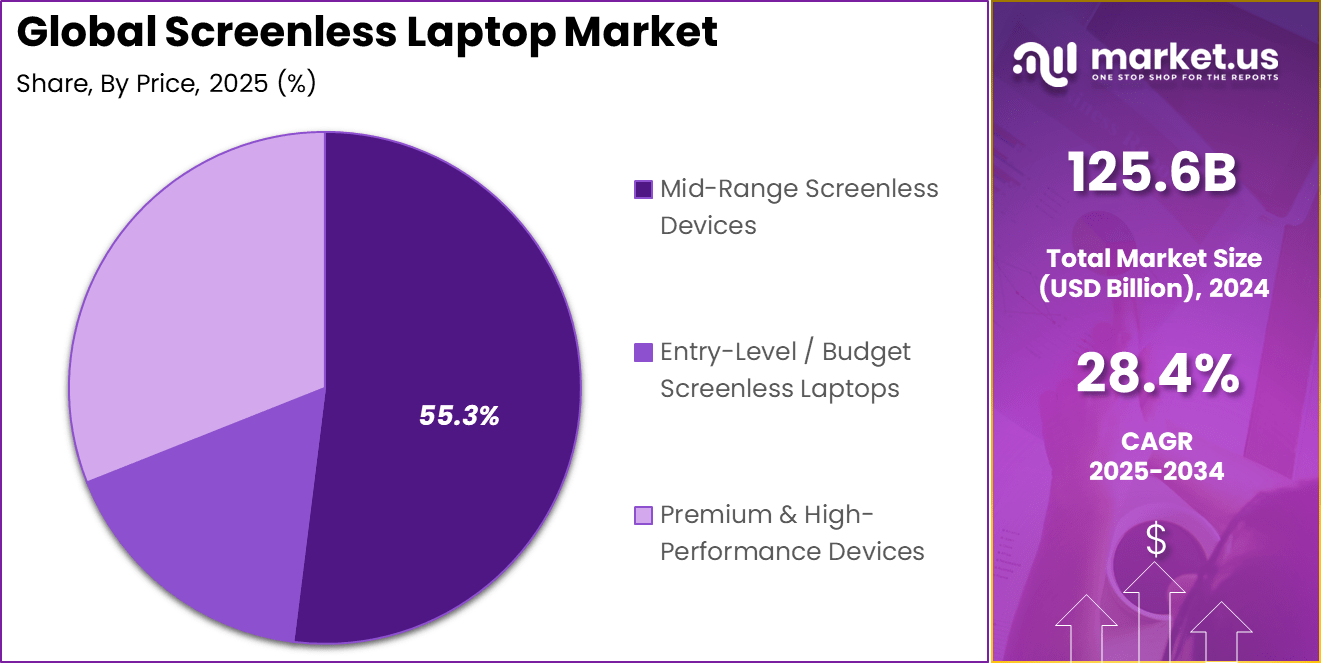

- Mid-range screenless devices captured 55.3%, indicating strong demand for balanced performance at accessible price points.

- North America held 38.6% share, fueled by high consumer tech adoption and strong e-commerce penetration.

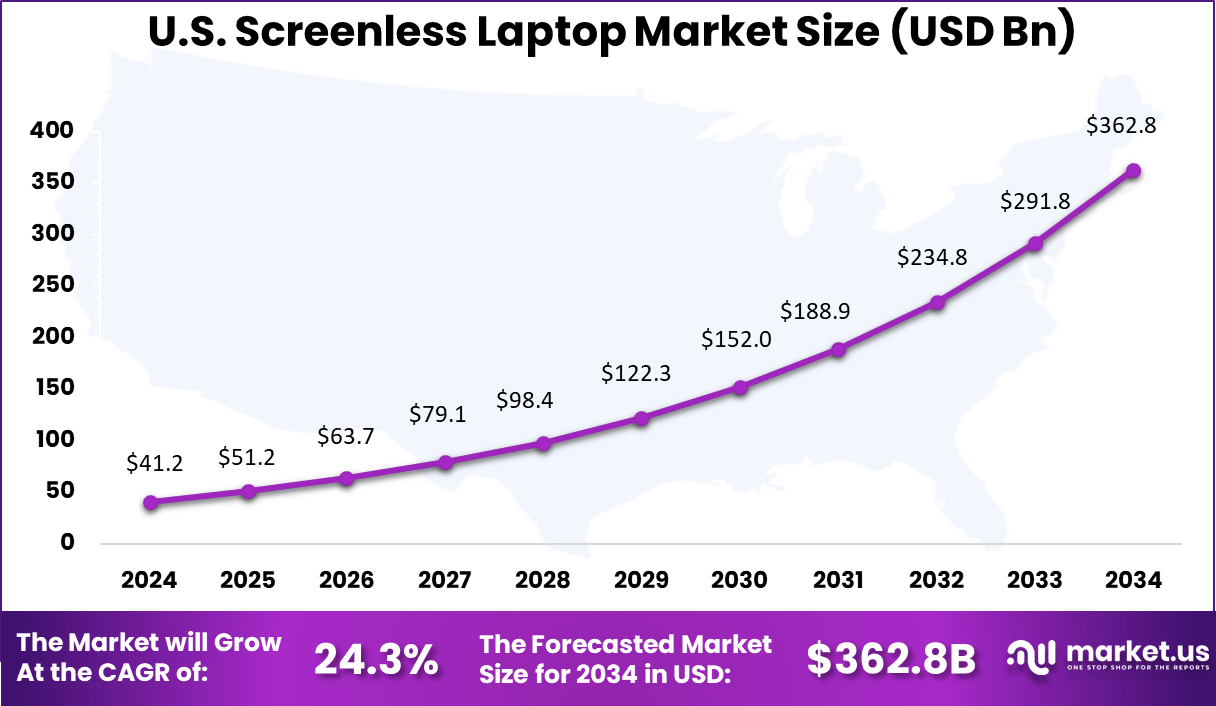

- The U.S. market reached USD 41.23 billion, growing at a 24.37% CAGR, driven by rapid innovation, early adopter interest, and increasing demand for next-generation computing form factors.

Report Scope

| Report Features | Description |

| Market Value (2024) | USD 125.6 Bn |

| Forecast Revenue (2034) | USD 1,529.8 Bn |

| CAGR(2025-2034) | 28.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Standard Screenless Laptops, Hybrid/Convertible Screenless Devices, Wearable/Integrated Screenless Interfaces), By Technology / Interface (Projection-Based Interfaces, Holographic Display Systems, Retinal / Direct-Eye Output, Voice & Gesture Interaction Systems), By Application (Personal & Home Use, Professional / Enterprise Use, Gaming & Entertainment, Development & Programming, Industrial & Field Operations, Healthcare, Government, Others), By Distribution Channel (Online Sales, Offline Retail), By Price (Entry-Level / Budget Screenless Laptops, Mid-Range Screenless Devices, Premium & High-Performance Devices) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Sightful, Lenovo, XREAL, Inc., Qualcomm Technologies, Inc., Microsoft Corporation, ASUSTeK Computer Inc., HP Development Company, L.P., Wistron Corporation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

By Type

In 2025, standard screenless laptops led the market with a 48.5% share, reflecting the growing adoption of familiar form factors without integrated displays. These devices cater to consumers who prioritize portability, flexibility, and minimalism, offering a sleek alternative to traditional laptops with built-in screens. The trend is driven by the increasing demand for devices that can be connected to external displays, allowing users to customize their setup according to personal preferences.

The screenless laptop segment continues to appeal to both professionals and consumers looking for compact, adaptable technology solutions. As remote work and flexible work environments gain momentum, the demand for screenless laptops that can seamlessly integrate into various settings has risen. This form factor’s ability to cater to a diverse range of computing needs – without sacrificing portability or functionality – has solidified its position as the leading choice in the market.

By Technology and Interface

Projection-based interfaces held 40.6% of the market, driven by the demand for flexible and portable display solutions. These interfaces allow users to project images or videos onto surfaces, offering a highly versatile and space-efficient way to interact with digital content. As consumers and professionals seek innovative, portable solutions that do not rely on traditional screens, projection-based devices have gained popularity in both personal and professional settings.

The ability to project content onto any surface has made these devices particularly attractive for presentations, meetings, and on-the-go usage. The growing interest in mobile computing and flexible work environments has fueled the adoption of projection-based interfaces, as users can enjoy a larger display without needing a dedicated screen. This technology is becoming increasingly integrated into a variety of devices, expanding its applications and enhancing the overall user experience.

By Application

Personal and home use accounted for 36.5% of the market, as consumers increasingly explore screenless devices for minimal setups, space efficiency, and privacy-focused computing. These devices offer a streamlined, clutter-free alternative to traditional technology setups, appealing to consumers who prioritize simplicity and functionality in their home environments. The desire for devices that do not compromise on performance while minimizing the need for physical screens is fueling the growth of this segment.

Consumers are becoming more conscious of their digital privacy, and screenless devices provide an added layer of security by reducing exposure to surveillance or unauthorized viewing. Additionally, the compact nature of these devices makes them ideal for small living spaces where space efficiency is key. As home-based work and learning continue to be prominent, the demand for these devices that can integrate seamlessly into everyday life is expected to rise.

By Distribution Channel

Online sales dominated the distribution channel with 58.4% of the market, supported by direct-to-consumer channels, wider product availability, and competitive pricing. The rise of e-commerce has made it easier for consumers to access a wide variety of screenless devices, often at more competitive prices compared to traditional brick-and-mortar stores. Direct-to-consumer sales channels have allowed companies to reach a larger audience, providing customers with the convenience of purchasing from the comfort of their homes.

E-commerce platforms also offer more extensive product reviews, comparison tools, and customer feedback, helping consumers make informed purchasing decisions. With online sales representing the bulk of distribution, the growth of digital platforms continues to drive market expansion, making these devices more accessible and appealing to a global audience. The ease of purchase and the convenience of home delivery are key factors contributing to the dominance of online sales in this market.

By Price

Mid-range screenless devices captured 55.3% of the market, indicating strong demand for products that balance performance with affordability. These devices appeal to a wide range of consumers who seek high-quality features without the premium price tag associated with high-end models. By offering solid performance, reliable battery life, and versatile functionality, mid-range screenless devices meet the needs of both budget-conscious individuals and those seeking accessible alternatives to more expensive options.

The mid-range segment has become increasingly important as consumers look for devices that provide the best value for their money. As the screenless device market continues to evolve, mid-range offerings are expected to be a primary driver of growth, catering to a broader consumer base while maintaining strong performance and usability. These devices represent a sweet spot in the market, offering the right balance of price and capability.

Regional Insight

North America held a 38.6% share of the market, backed by high consumer tech adoption and strong e-commerce penetration. The region’s well-established digital ecosystem, coupled with widespread access to innovative technology, has positioned it as a key player in the screenless device market. North America’s early adoption of emerging technologies, along with its robust e-commerce infrastructure, has contributed significantly to the growth of the market.

The U.S. market alone reached USD 41.23 billion and is expanding at a 24.37% CAGR, driven by rapid innovation, early adopter interest, and rising demand for next-generation computing form factors. As the market continues to evolve, North America’s leadership in technological development and digital adoption will remain a significant factor in shaping the future of screenless devices. The combination of strong market demand, technological advancements, and e-commerce growth ensures that North America will continue to lead the charge in the global screenless device market.

Key Players Analysis

In the screenless laptop market, Sightful is a pioneering player, offering innovative solutions that utilize augmented reality (AR) and projection technology to replace traditional screens. Lenovo and XREAL, Inc. also contribute significantly with their cutting-edge screenless laptop concepts, focusing on integrating immersive visual experiences through wearable technology and AR devices. Qualcomm Technologies, Inc. and Microsoft Corporation continue to innovate, leveraging their strengths in hardware and software integration to enhance screenless computing experiences.

ASUSTeK Computer Inc. and HP Development Company, L.P. are key players in the market, exploring alternative display methods such as holographic projections and AR headsets. Their offerings promise to reshape the way users interact with laptops, making devices more portable and versatile. Wistron Corporation plays a vital role by providing manufacturing expertise and technology solutions, enabling the mass production of screenless laptops.

The market continues to grow with contributions from other emerging players, who are working on improving hardware capabilities and software integration for seamless screenless computing experiences. These innovations are expected to drive the adoption of screenless laptops in various sectors, including business, education, and entertainment.

Top Key Players in the Market

- Sightful

- Lenovo

- XREAL, Inc.

- Qualcomm Technologies, Inc.

- Microsoft Corporation

- ASUSTeK Computer Inc.

- HP Development Company, L.P.

- Wistron Corporation

- Others

Emerging Trend Analysis

Augmented Reality‑Based Screenless Computing

A notable emerging trend in the screenless laptop market is the rise of augmented reality (AR)‑based computing interfaces that replace traditional physical displays with virtual screens projected through wearable devices. Screenless laptops now combine compact compute hardware with AR glasses to deliver large, immersive virtual workspaces directly in the wearer’s field of view, allowing users to interact with multiple virtual screens without physical panels. These systems aim to provide flexibility in workspace layouts while reducing the bulk and weight of conventional laptops.

This trend reflects an evolving user preference for more adaptable computing environments that can accommodate professional, creative, or mobility‑focused use cases. AR‑based screenless computing is especially appealing for users who require large visual real estate without sacrificing portability. As spatial‑computing hardware and software mature, the functionality of these devices is improving, and early adopters are defining new workflows centered around virtual displays.

Driver Analysis

Demand for Portability and Enhanced Privacy

The screenless laptop concept is being driven by user demand for greater portability and enhanced privacy in mobile computing. Removing the physical display reduces device weight and bulk, enabling more compact form factors that still offer full computing performance when paired with AR headsets or projection systems. This shift appeals to professionals and mobile users who value lightweight solutions without compromising productivity or multitasking capabilities.

Enhanced privacy is another motivating factor as virtual displays can be inherently more secure in public or open environments, with visual output visible only to the intended user. Screenless laptops thus align with evolving user expectations for both convenience and confidentiality, particularly in enterprise use cases. As hardware ecosystems and spatial computing interfaces develop, this driver continues to encourage innovation around screenless designs.

Restraint Analysis

Limited Awareness and Experimental Perception

One significant restraint on the market adoption of screenless laptops is user awareness and the perception of these devices as experimental rather than mainstream tools. Many potential buyers lack a clear understanding of how screenless laptops fit into traditional computing workflows, as early models rely on emerging AR or projection technologies that are unfamiliar to broad audiences. This perception slows adoption, as users typically prefer established laptop formats with proven performance and usability.

The lack of widespread use cases beyond niche or early adopter segments can further constrain adoption, leading some buyers to delay investment until experience with screenless interfaces becomes more common. Without clearer value propositions and education on practical benefits, the transition from conventional laptops to screenless alternatives may remain gradual rather than rapid.

Opportunity Analysis

Integration with Evolving Spatial Computing Ecosystems

The evolution of spatial computing ecosystems presents a substantial opportunity for screenless laptops to expand their relevance and appeal. As AR hardware, software platforms, and developer tools improve, screenless laptops can integrate seamlessly with broader spatial productivity workflows, including virtual collaboration, immersive visualization and context‑aware applications. These integrations could unlock new productivity paradigms not possible with traditional screen‑based laptops.

Additionally, markets where compact form factors and flexible display interfaces are highly valued such as field operations, remote work environments, or creative media production – may see accelerated adoption. Screenless laptops that deliver large virtual workspaces without physical screens can cater to these segments by offering both performance and adaptability.

Challenge Analysis

Technical and User‑Experience Complexities

A core challenge for the screenless laptop market is the technical complexity of delivering a consistent and comfortable user experience across diverse real‑world usage scenarios. AR‑based screenless interfaces must account for factors such as head‑tracking stability, user comfort over extended periods, and precise interaction models that match or exceed traditional screen performance. These technical hurdles require sophisticated hardware and software coordination that is still in early refinement stages.

User experience challenges also include ensuring clarity, responsiveness, and ergonomic comfort, which are essential for productivity tasks. If AR visuals drift or require frequent adjustment, user fatigue can increase, impacting long‑term usability. Overcoming these technical and experience complexities will be critical for screenless laptops to transition from novel prototypes to widely accepted computing solutions.

Conclusion

In conclusion, the screenless laptop market is positioned at the intersection of advanced computing and emerging display technologies. As industries and consumers increasingly seek devices that offer flexibility, portability, and immersive user experiences, screenless laptops are poised to offer significant value. The continued evolution of technologies such as augmented reality, holographic projection, and retina‑direct displays holds the potential to reshape how we interact with computing devices, offering new opportunities for personal and professional use.

While still in its developmental phase, the market is gaining traction due to the growing demand for next‑generation computing platforms and the increasing focus on mobility and usability. With further innovation and investment, screenless laptops could redefine the future of personal computing, providing more efficient, ergonomic, and engaging solutions across various industries.