Introduction

Space Tourism Statistics: Space tourism has kind of shifted, from what used to feel like straight-up science fiction into a quickly emerging commercial scene that’s pulling in billionaires, adventure folks, private astronauts, and even institutional capital. In 2026, the whole thing is at this pivotal point where reusable rocket tech, private space stations, and commercial crewed spaceflight programs are changing the underlying math of getting to orbit.

The market still feels like a niche luxury corner, but a lot of analysts are saying we should expect steep, almost exponential, growth through the next ten years. Companies like Virgin Galactic, Blue Origin, SpaceX, and Axiom Space keep pushing innovation, both with suborbital jaunts and orbital tourism offerings.

The demand side, especially among ultra-high-net-worth buyers, plus ongoing improvements in reusable spacecraft, is expected to nudge space tourism into something like a multi- billion-dollar industry in the coming decade.

Editor’s Pick

- The global space tourism market is expanding at a remarkable 36.6% CAGR, which makes it one of the fastest-growing aerospace sectors.

- Industry revenue is expected to climb from today’s baseline to USD 4.16 billion by 2027 and then to USD 17.74 billion by 2032.

- Commercial operators already hold 57% of the space tourism market, which points to strong private-sector control.

- Only six nations, or political unions, have completed lunar missions between 1959 and 2026.

- The United States leads the Moon push with 45 successful, or semi-successful, Moon missions, basically close to half of all major lunar expeditions.

- Consumer sentiment is still kinda split, with 55% of Americans thinking space tourism will feel common within 50 years.

- Even with that growing optimism, only 35% of Americans say they’d actually want to travel to space themselves.

- Commercial human spaceflight has moved about 100 private individuals into space since 2001.

- SpaceX’s orbital tourism seats command a premium pricing of USD 55–70 million per passenger, the highest in the industry.

- Global customer backlogs now exceed 3,000 confirmed reservations.

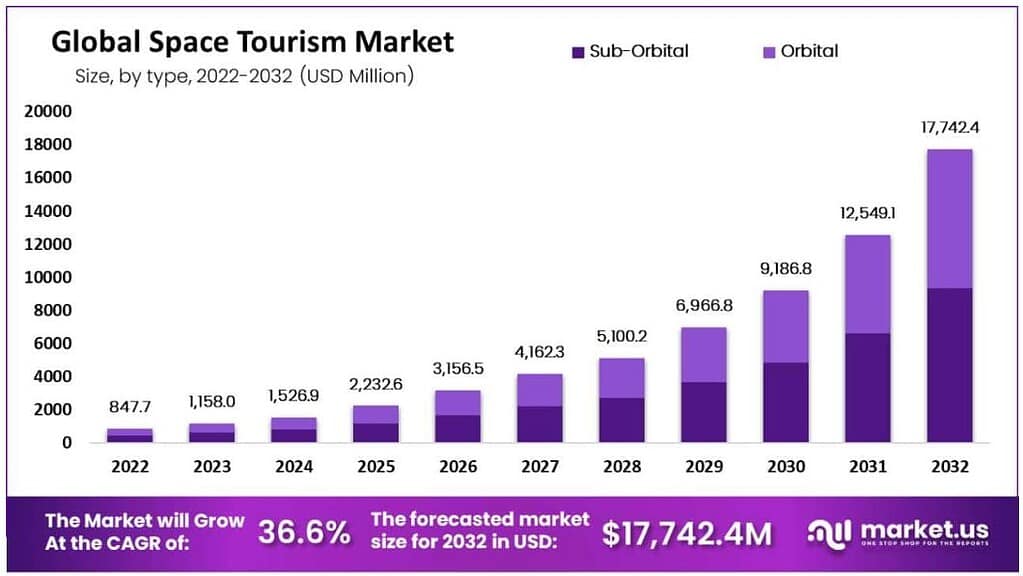

Global Space Tourism Market

(Source: market.us)

- Space tourism has been growing pretty remarkably lately, with a CAGR of 36.6% and revenue basically climbing up, higher and higher, like it never stops.

- By 2027, the market is projected to jump beyond USD 4,162.3 million, and the same upward momentum should keep moving through the next years, finally landing at an eye‑catching USD 17.74 billion by 2032.

- Within this fast-paced, quite competitive field, commercial players take the lead, holding about 57% of the market share.

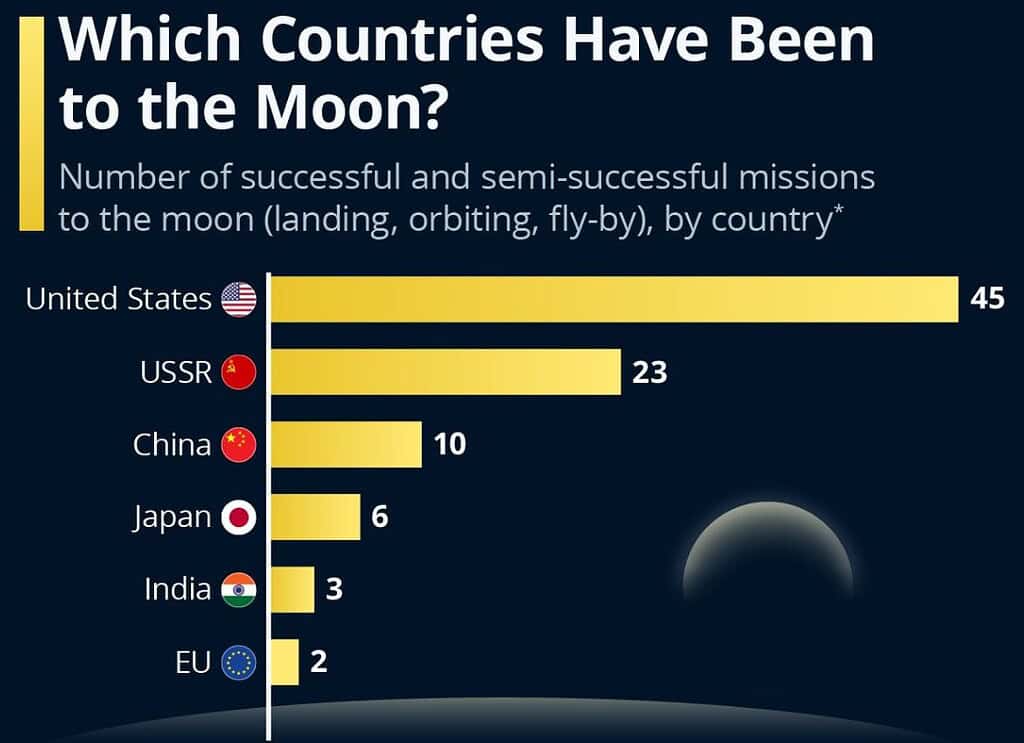

Moon Race By The Numbers

(Source: statista.com)

- Lunar exploration remains one of the most exclusive achievements in human history; at least to me, it still feels that way.

- From 1959 to 2026, only six nations or political unions truly managed to carry out lunar missions that included flybys, orbiters, landings or other operations near the Moon.

- The United States keeps leading the lunar scene, with 45 successful or semi-successful missions, and that’s close to nearly half of all the major lunar expeditions ever recorded.

- The most recent update arrived with Artemis II in April 2026, which basically reinforces America’s leadership in deep-space exploration.

- The former USSR sits second, with 23 missions wrapped up between 1959 and 1976, and it helped put a lot of those early milestones in place during the original Space Race era.

- China looks like the fastest-growing lunar power, piling up 10 missions since its first lunar mission in 2007. Its steady mission performance shows how quickly its space abilities have expanded over the last couple of decades.

- Japan follows with 6 missions, including its first successful lunar soft landing, which underscores its growing role in advanced robotic exploration.

- India has done 3 lunar missions, moving from the 2008 Chandrayaan-1 orbital mission to becoming the fourth nation in history to manage a successful Moon landing in 2023 via Chandrayaan-3.

- The European Union (EU) has logged 2 lunar missions, and through orbital plus flyby efforts, it has helped with important technological demonstrations and scientific research, even if the scale is smaller than the others.

- A lot of countries take part in space research; only a few have managed real, sustained lunar mission success.

- The data also seems to suggest a shift away from the Cold War-style dominance of the United States and USSR, toward a more tangled and diverse lunar ecosystem driven by newer space powers like China, India, and Japan.

- With Artemis and other lunar programs ramping up, the next decade could really scramble these rankings a bit, not just nudge them.

Space Tourism Outlook

According to the NASA Public Opinion Survey, U.S. Space Attitudes Survey, the future of space tourism carries this odd blend of hope and hesitation across Americans. Survey data based on 10,329 U.S. adults shows 55% think space tourism might become routine within the next 50 years, which reads like growing faith in the commercialization of space travel. Still, consumer interest is not exactly unified. About 35% of respondents said they’d like to travel to space and orbit Earth, but a larger 65% reported no interest in becoming space tourists themselves. In other words, it looks like public comfort with the idea may grow faster than the number of people who actually sign up.

Long-term expectations are similarly split. Nearly 44% expect space tourism to remain unusual or not truly regular by 2073, pointing to worries about affordability, access, and whether the tech will be dependable enough. Around 70% of Americans say it matters for the United States to keep leading in space exploration, and about 65% think NASA should stay actively involved even as private companies such as SpaceX and Blue Origin keep expanding. Roughly 69% are concerned about space debris over the next 50 years, while 60% see asteroid monitoring as a top NASA priority, and 50% prioritize Earth climate observation too. So overall, these numbers show a crowd that is genuinely excited about space tourism’s possibilities, but at the same time, they’re still anchored on safety, sustainability, and also the bigger scientific value that comes with space exploration.

Commercial Space Travel In 2026

- 2026 stands out as a bit of a defining year for commercial space tourism because private firms are now giving experiences that range from near-space balloon rides to full-on orbital missions.

- Right now, the industry runs across three major tourism areas: suborbital flights, orbital missions, and what’s described as future lunar journeys.

- Since the first private space traveler flew back in 2001, the overall count has grown to around 100 private individuals who have reached space through commercial missions.

- At the “entry” level, Space Perspective provides a stratospheric-style experience that rises to about 30 kilometers above Earth, priced at USD 125,000 per seat.

- Passengers spend about 2 hours at peak altitude within a 6-hour journey. While it does not cross the Kármán Line, it still counts as the most affordable premium space-like option out there.

- The suborbital space tourism market is kinda led by Blue Origin and Virgin Galactic.

- Blue Origin’s New Shepard gets to about 107 kilometers up, it takes up to 6 passengers on an 11-minute kind of mission, with tickets in the USD 200,000–USD 300,000 range per seat.

- Virgin Galactic, meanwhile, goes to around 88 kilometers, you get roughly 5 minutes of weightlessness, and the price is closer to USD 450,000 per passenger.

- Private flights aboard Crew Dragon are estimated at around USD 55–70 million per seat, and that gives travelers a chance to stay several days in orbit.

- Earlier missions have gone as high as 575 kilometers, and then also 700 kilometers, which is basically setting new milestones for crewed commercial spaceflight.

- Planned Starship circumlunar trips are expected to host about 8 passengers, with overall mission costs pegged at more than USD 100 million.

- Commercial lunar travel is aiming to start its first passenger missions in 2027 to 2028.

- All things considered, the figures show a quickly maturing industry where the customer experience spans from roughly USD 125,000 near-space rides to USD 70 million orbital stays.

- Even if it’s still a niche for now, 2026 indicates commercial space travel is moving away from a purely experimental stunt, and toward something more organized and global in vibe, as a tourism category.

Space Tourism Customer Backlog and Ticket Demand

- Honestly, the biggest space tourism story in 2026 isn’t that people aren’t interested; it’s that there simply aren’t enough seats.

- Across the whole sector, thousands of customers have already put down deposits for later journeys, and that’s creating one of the biggest supply constrictions ever seen in commercial space travel.

- Virgin Galactic still looks like one of the clearest signals of this kind of imbalance, honestly.

- The company said it has a backlog tied to around 675 Founding Astronaut customers, plus as many as 125 more ticket holders, so the waiting line is basically sitting near 800 passengers.

- In 2026, it started selling tickets again at USD 750,000 per seat, but it only released about 50 fresh tickets at first.

- Now, if they really manage that long-term idea of 10 flights a month with 6 people per flight, that’s roughly 60 passengers per month, so the older backlog could get handled in maybe 11 to 12 months.

- But with a more conservative plan, like 52 flights across the year, total capacity lands closer to 312 passengers annually, and then the wait could stretch into 2028 or even 2029.

- Space Perspective has a parallel kind of headache. It has already pre-sold more than 1,800 tickets at USD 125,000 each, which works out to roughly USD 225 million in forward bookings.

- Their luxury capsule takes 8 passengers per flight, and even running three flights each week would only deliver around 1,200 seats per year.

- On that schedule, the reservations that already exist would take at least 18 months to clear, just to be clear.

- Put Virgin Galactic’s 800 customers together with Space Perspective’s 1,800+ reservations, then add demand coming from private astronaut programs and other operators, and the global backlog is now over 3,000 confirmed customers queued up for commercial space experiences.

- Since 2021, Blue Origin has carried 92 paying tourists, but the program is now suspended for at least two years, so future customers are getting pushed toward an already crowded market that doesn’t really have much spare room.

- All in all, the stats point to the fact that commercial space tourism demand is still unusually strong.

- The main hassle for the industry is no longer just getting customers; it’s more like building enough flight capacity so it can handle the thousands of travelers already waiting for their chance to leave Earth.

Conclusion

Space tourism in 2026 sits right at that mix of technological innovation, luxury travel, and commercial spaceflight. The market forecasts show solid long-run growth, backed by rising consumer awareness, more investment from the private sector, and improvements in reusable spacecraft tech. Even if ticket prices stay extremely high and access is narrow, demand keeps running ahead of the available flight capacity.

So, you get real customer queues and backlogs across the industry. Businesses like Virgin Galactic, Blue Origin, SpaceX, and Space Perspective are slowly turning human spaceflight into a more organized commercial market. As costs fall and operating capacity rises, space tourism should shift from a rare, VIP sort of thing into a wider global industry.

FAQ

It’s projected to hit around USD 17.74 billion by 2032.

The industry is expected to grow at about a 36.6% compound annual growth rate (CAGR).

A seat on a SpaceX orbital mission is roughly USD 55–70 million per passenger.

About 100 private individuals have gotten to space through commercial missions since 2001.

The global backlog exceeds 3,000 confirmed customers, reflecting strong demand and limited flight availability.