Introduction

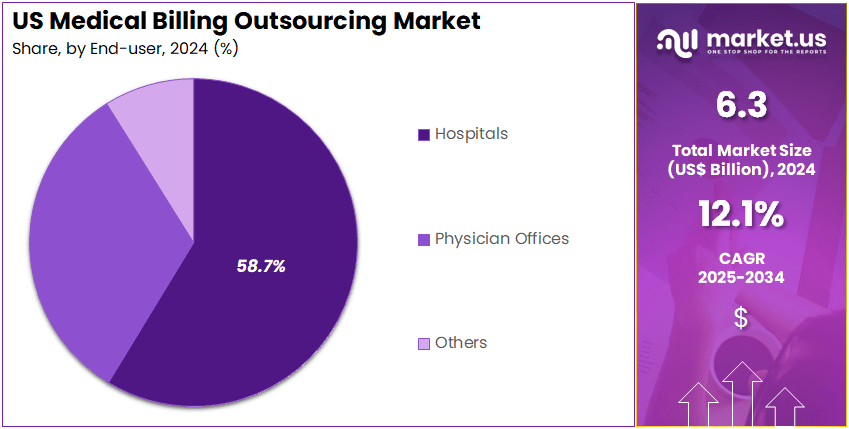

The US Medical Billing Outsourcing Market is projected to grow from USD 6.3 Billion in 2024 to USD 19.7 Billion by 2034, reflecting a robust CAGR of 12.1%. This expansion is driven by increasingly complex healthcare regulations, rising denial rates, and pressure on providers to optimize revenue cycle performance.

Front-end services account for 47.2% of revenues, while outsourced models represent 63.8% of the market, underscoring strong demand for specialized third-party expertise. Hospitals dominate with 58.7% share, as they aggressively outsource billing to control costs, improve cash flow, and ensure regulatory compliance.

Get lastest insights and updates at @ https://market.us/report/us-medical-billing-outsourcing-market/free-sample/

Key Takeaways

- In 2024, the US medical billing outsourcing market generated revenue of US$ 6.3 Billion and is projected to reach US$ 19.7 Billion by 2034, expanding at a CAGR of 12.1% during the forecast period.

- Based on product type, the market is segmented into front-end services, middle-end services, and back-end services. The front-end services segment dominated in 2024, accounting for a 47.2% market share.

- By component, the market is categorized into in-house and outsourced models. Among these, the outsourced segment held a significant share of 63.8%, reflecting increasing preference for third-party billing solutions.

- In terms of end users, the market is divided into hospitals, physician offices, and others. The hospitals segment emerged as the leading end user, capturing the largest revenue share of 58.7% in 2024.

How Growth Is Impacting the Economy

Rapid growth in medical billing outsourcing is reshaping the wider US healthcare economy by reallocating spending from in-house administrative teams to specialized service providers. As hospitals and clinics outsource billing, they reduce fixed labor costs, shift to variable service contracts, and unlock capital for clinical investments and digital health transformation.

This supports job creation in health IT, AI, and revenue cycle management, while traditional back-office roles decline or reskill toward higher-value analytical work. Rising inflation and higher operating costs make outsourcing an efficiency lever, helping providers maintain margins despite reimbursement pressure and rising denial rates.

At the macro level, better revenue capture and fewer claim denials strengthen provider solvency, sustaining access to care and supporting regional healthcare infrastructure, especially as value-based care expands.

Strategies for Businesses

- Build specialized capabilities in front-end services such as patient eligibility checks, coding, and insurance verification to align with the largest product-type segment (47.2% share).

- Invest in AI and automation for claims scrubbing, coding assistance, and denial analytics to reduce errors and speed reimbursement.

- Design flexible pricing models (per-claim, outcome-based, or hybrid) that help providers manage inflationary cost pressure and budget uncertainty.

- Strengthen data security frameworks to meet HIPAA and related privacy standards, addressing key market restraints around breaches.

- Target hospitals and large integrated systems first, given their 58.7% revenue share and high outsourcing propensity.

- Develop consulting-plus-execution offerings to optimize end-to-end revenue cycle, from front-end intake to back-end collections.

Key Segmentation

- Product Type Analysis: The front-end services segment dominated with a 47.2% share in 2024, driven by rising demand for patient registration, insurance verification, and coding accuracy. Increasing claim denials and adoption of automation tools are encouraging healthcare providers to outsource front-end billing operations.

- Component Analysis: The outsourced component accounted for 63.8% share due to growing preference for third-party billing providers. Outsourcing helps reduce operational costs, improve reimbursement timelines, and maintain regulatory compliance. Increasing billing complexity and focus on patient care continue supporting adoption.

- End-user Analysis: Hospitals dominated with a 58.7% revenue share, supported by rising outsourcing of billing functions. Increasing coding complexity, regulatory compliance requirements, and pressure to improve revenue cycle management are encouraging hospitals to adopt outsourced medical billing services.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Analyst Viewpoint

Currently, US medical billing outsourcing sits at the intersection of regulatory complexity, financial pressure, and rapid digitization, creating a structurally attractive growth runway. Market participants that integrate AI, analytics, and seamless EHR connectivity are capturing share as providers seek partners who can both execute and advise.

Over the next decade, rising denial rates, consolidation among health systems, and the shift to value-based reimbursement should deepen outsourcing penetration beyond today’s 63.8% outsourced component mix. Analysts see a positive outlook with recurring, contract-driven revenue, expanding use cases across front, middle, and back-end services, and growing demand from both large hospitals and mid-sized physician groups. Vendors that lead on security, transparency, and measurable ROI are expected to outperform the overall 12.1% CAGR.

Use Cases and Growth Factors

| Use Case / Segment | Description & Value Proposition | Key Growth Factors |

| Hospital front-end services | Outsourced patient registration, eligibility, and pre‑authorization to reduce denials. | Rising complexity of insurance plans, need to cut admin costs, 58.7% hospital share of market revenue. |

| Physician office coding & billing | End‑to‑end coding and claim submission for small and mid‑sized practices. | Limited in‑house expertise, denial pressure, shift to outsourced model (63.8% share). |

| Middle-end denial management | Specialist teams managing payer edits, appeals, and resubmissions. | Higher denial rates from 2022–2023, need for faster cash flow and revenue recovery. |

| Back-end collections and A/R optimization | Management of receivables, patient statements, and collections workflows. | Margin pressure in inflationary environment, demand for working‑capital optimization. |

| AI-driven billing platforms | Automated coding, claims scrubbing, and predictive denial analytics. | Technological advances, venture funding (e.g., AI startups and platforms expanding capabilities). |

Business Opportunities

Vendors can capture significant opportunity by vertically specializing in hospital-grade revenue cycle management tailored to US reimbursement rules. Offering bundled front, middle, and back-end services with embedded analytics creates stickier, higher-value contracts. There is room for niche players focused on specific specialties such as radiology, oncology, or surgery, where coding complexity and claim values are high.

Technology-first providers can differentiate through AI-based coding, denial prediction, and real-time dashboards for CFOs and revenue cycle leaders. Security-centric offerings, including HIPAA-compliant cloud platforms and advanced encryption, address a key adoption barrier and can justify premium pricing.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Key Player Analysis

Leading providers in this market are expanding through mergers and acquisitions, technology integration, and penetration of underserved regions. Many have evolved from pure billing vendors into full revenue cycle partners, integrating patient access, coding, billing, and collections on unified platforms.

Investment in AI and automation is a competitive differentiator, enabling higher accuracy, faster turnaround, and improved denial management. Strong compliance frameworks around HIPAA, ICD-10, and payer-specific rules are central to maintaining client trust and securing long-term contracts. Overall, the competitive landscape favors scaled, tech-enabled players that can deliver measurable financial uplift for healthcare providers.

Top Key Players

- SmarterDx

- Quest Diagnostics

- Promantra Inc

- Oracle

- McKesson Corporation

- Kyron Medical

- Kareo Inc

- eClinicalWorks

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 6.3 billion |

| Forecast Revenue (2034) | US$ 19.7 billion |

| CAGR (2025-2034) | 12.10% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Front-end Services, Middle-end Services, and Back-end Services), By Component (In-House and Outsourced), By End-user (Hospitals, Physician Offices, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SmarterDx, Quest Diagnostics, Promantra Inc, Oracle, McKesson Corporation, Kyron Medical, Kareo, Inc, and eClinicalWorks. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Recent Developments

- March, 2025 – SmarterDx announced a $50 million Series B funding round led by Transformation Capital to scale its clinical AI platform that reviews every chart before billing and lifts hospital revenue integrity.

- March, 2025 – SmarterDx was highlighted in an independent KLAS report, where hospital customers praised its AI-driven pre-bill review for improving case-mix index, reducing missed charges, and safeguarding millions in revenue leakage.

- February, 2026 – Quest Diagnostics reported fourth-quarter 2025 revenues of $2.81 billion, up 7.1% year on year, and raised its 2026 guidance while increasing its quarterly dividend by 7.5%, signaling confidence in long-term diagnostic and revenue-cycle demand.

- May, 2025 – McKesson announced its intent to separate its Medical-Surgical Solutions segment into an independent company, positioning the new entity to focus tightly on growth in healthcare services, supply, and downstream billing support while unlocking shareholder value.

Conclusion

The US medical billing outsourcing market is positioned for strong growth, driven by rising administrative complexity, cost pressures, and increasing adoption of third-party revenue cycle solutions. Front-end services, outsourced delivery models, and hospital end users continue to dominate market demand.

Expanding use of AI, automation, and analytics is improving claims accuracy, accelerating reimbursements, and reducing denial rates. Healthcare providers are shifting toward flexible outsourcing strategies to enhance operational efficiency and maintain margins.

Additionally, consolidation among health systems and the transition toward value-based care are reinforcing outsourcing adoption. Overall, technology integration, regulatory demands, and financial optimization needs are expected to sustain long-term market expansion.