Introduction

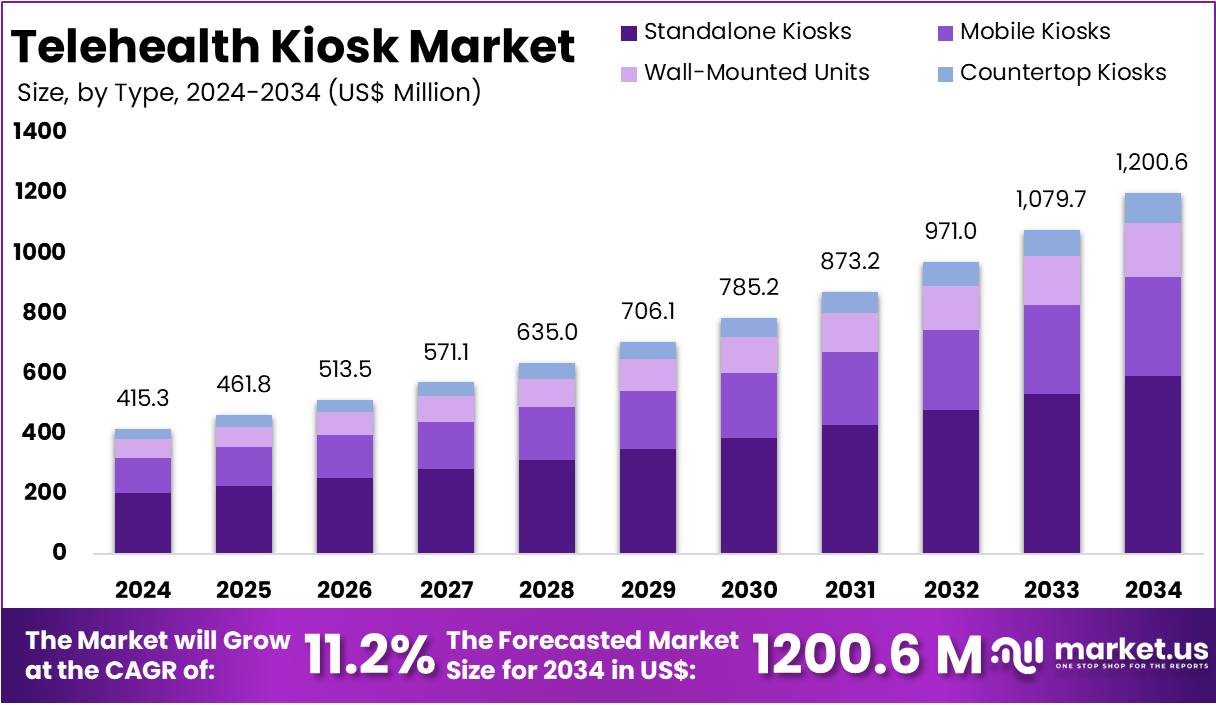

The Global Telehealth Kiosk Market is valued at about US$ 415.3 Million in 2024 and is projected to reach approximately US$ 1,200.6 Million by 2034, registering a robust CAGR of 11.2%. This growth is driven by rising demand for remote clinical access, physician shortages, and expanding digital readiness among patients worldwide.

Standalone kiosks currently account for over 49% of deployments, with hardware and teleconsultation dominating component and application shares, respectively. North America leads with more than 48.5% market share, supported by advanced infrastructure, supportive reimbursement, and strong telehealth adoption.

Get lastest insights and updates at @ https://market.us/report/telehealth-kiosk-market/free-sample/

Key Takeaways

- The global telehealth kiosk market is expected to reach approximately US$ 1,200.6 million by 2034, increasing from US$ 415.3 million in 2024, expanding at a CAGR of 11.2% during the forecast period.

- Standalone kiosks dominated the type segment in 2024, accounting for more than 49.3% of the total market share, supported by ease of deployment and growing demand for self-service healthcare access.

- Hardware solutions led the component segment in 2024, capturing over 44.0% of overall market revenue, driven by increasing adoption of integrated diagnostic devices and touchscreen-enabled kiosk infrastructure.

- Teleconsultation applications represented the leading use case in 2024, contributing more than 47% of total market utilization, due to rising demand for remote consultations and improved patient accessibility.

- Hospitals and specialty clinics emerged as the largest end-user segment in 2024, holding over 43.5% of global demand, supported by increasing implementation of digital patient engagement solutions.

- North America accounted for the highest regional share in 2024, exceeding 48.5% and generating approximately US$ 201.4 million in revenue, driven by advanced healthcare infrastructure and strong telehealth adoption.

How Growth Is Impacting the Economy?

Rapid expansion of telehealth kiosks is reshaping healthcare economics by reducing travel costs, optimizing facility utilization, and improving workforce productivity. Kiosks placed in rural clinics, workplaces, and community hubs cut travel distances by up to several tens of kilometers per visit, directly lowering patient out-of-pocket and system-level logistics costs.

As primary care shortages persist affecting around 75 million people across more than 7,500 U.S. Health Professional Shortage Areas kiosks provide cost-effective coverage without constructing full-scale facilities.

On the payer side, growing acceptance of remote monitoring and teleconsultation, evidenced by more than US$ 500 million in Medicare RPM payments in 2024, helps shift spending from expensive acute episodes to preventive and chronic-care management.

Employers and governments benefit from reduced productivity loss through on-site or near-site kiosks that support occupational health and preventive screening. The resulting macro effect is a gradual reallocation of healthcare expenditure toward digitally enabled, lower-cost access points, while stimulating capital investment in diagnostic hardware, connectivity, and specialized services.

Strategies for Businesses

- Prioritize high-need locations (rural health centers, high-traffic retail, large worksites) where physician shortages and access gaps are greatest to maximize utilization and ROI.

- Adopt modular kiosk architectures that allow easy integration of new diagnostic peripherals and AI tools, future-proofing investments against rapid technology change.

- Build strong partnerships with connectivity providers to secure cost-effective, compliant broadband with service-level agreements suited to clinical traffic.

- Integrate kiosks tightly with EHR and telehealth platforms to enable seamless documentation, analytics, and care coordination across virtual and physical encounters.

- Develop patient and employee engagement programs that normalize kiosk use, with clear workflows for teleconsultation, vital-sign monitoring, and follow-up.

- Explore outcome-based or subscription models with vendors to manage high upfront costs and align payments with realized utilization and clinical value.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Key Segmentation

- Type Analysis: In 2024, standalone kiosks dominated with over 49.3% share, driven by hospital deployments, strong diagnostics, and stable designs. Mobile units gained traction for flexible outreach, while wall-mounted models grew through space efficiency. Countertop kiosks saw adoption supported by lower costs.

- Component Analysis: In 2024, hardware led with more than 44.0% share, supported by demand for durable structures, integrated sensors, and diagnostics. Software expanded through cloud platforms, AI analytics, and subscriptions. Services gained momentum via installation, maintenance, training, and remote support improving reliability.

- Application Analysis: In 2024, teleconsultation dominated with over 47.7% share, driven by remote access and reduced waiting times. Vital signs monitoring expanded through automated assessments. Pharmaceutical dispensing advanced via medication management. Behavioral health and occupational screening gained traction, supported by care initiatives.

- End-User Analysis: In 2024, hospitals and specialty clinics led with over 43.5% share, driven by triage, diagnostics, and specialist consultations. Community centers expanded affordable access. Pharmacies and retail clinics adopted walk-in models, while workplaces, schools, and government sites deployed kiosks for monitoring.

Analyst Viewpoint

At present, the telehealth kiosk market sits at the intersection of structural healthcare shortages, maturing telemedicine workflows, and growing patient comfort with digital health. Hardware reliability and clinically validated sensors have addressed early concerns around diagnostic accuracy, while integration with telehealth platforms and EHRs enables scalable enterprise deployments. Over the next decade, analysts expect kiosks to evolve into intelligent, AI-augmented diagnostic endpoints embedded across pharmacies, workplaces, campuses, and rural hubs.

Future growth will be supported by an expanding portfolio of FDA-cleared AI/ML medical devices, increasing telemedicine penetration in outpatient and mental-health care, and policy environments that maintain favorable reimbursement for virtual services.

As advanced peripherals, automated triage, and remote monitoring tools converge within kiosks, their role will shift from basic teleconsultation booths to comprehensive, self-service health stations. This positions the market for sustained double‑digit growth with rising strategic relevance to health systems, employers, and payers globally.

Use Cases and Growth Factors

| Aspect | Details |

|---|---|

| Primary care access | Teleconsultation kiosks in hospitals, clinics, and rural centers shorten waiting times and extend specialist reach into underserved regions. |

| Retail & pharmacy clinics | Kiosks in pharmacies and supermarkets support minor-illness management, vitals checks, and medication counseling, enabling low-cost walk-in care. |

| Workplace health | Corporate and industrial sites use kiosks for occupational health, preventive screening, and chronic-disease monitoring, improving productivity. |

| Education & public sector | Schools and government facilities deploy kiosks for student health, public screening, and mental-health assessments. |

| Growth driver – access gaps | Persistent primary-care and rural broadband shortages create structural demand for fixed, connected clinical endpoints. |

| Growth driver – digital readiness | Rising online health-information use and sustained telemedicine uptake expand the addressable user base. |

| Growth driver – technology | Validated diagnostic peripherals and over 1,000 authorized AI/ML medical devices enhance clinical value and trust. |

| Growth driver – policy & reimbursement | Continued telehealth coverage, RPM payments, and rural broadband programs support kiosk economics and deployment scale. |

Regional Analysis

North America remains the anchor market, holding more than 48.5% share and about US$ 201.4 million in value in 2024, driven by high telehealth adoption, strong reimbursement, and robust broadband infrastructure. Federal programs such as the FCC’s Rural Health Care initiatives and Medicare’s expanded telehealth coverage lower connectivity and operational barriers for kiosk deployments. The U.S. Veterans Affairs ATLAS network and Canadian virtual-care initiatives demonstrate scalable kiosk models across community sites and remote regions.

Europe is advancing via national digital-health strategies and widespread EHR use, while Asia Pacific shows strong long-term potential, supported by large rural populations and government-backed telemedicine platforms such as India’s eSanjeevani. Latin America and the Middle East & Africa are earlier in adoption but benefit from pilots targeting remote communities and public health screening. Across regions, telehealth kiosks increasingly complement broader hybrid-care ecosystems rather than functioning as standalone point solutions.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Business Opportunities

Telehealth kiosks create multiple revenue and partnership opportunities across hardware, software, services, and connectivity. Hardware vendors can capitalize on demand for modular, healthcare-grade enclosures and integrated sensors, while software providers monetize telehealth platforms, analytics, and AI-based triage embedded in kiosk workflows. Service providers have recurring opportunities in installation, maintenance, staff training, and remote support, especially as deployments scale across distributed networks.

Telecom and cloud providers benefit from the need for secure, high-availability connectivity and data hosting tailored to clinical workloads. Retail chains, pharmacy networks, universities, and employers can develop new health-access offerings by hosting kiosks and partnering with health systems or virtual-care platforms. In emerging markets, public–private partnerships around rural health access and national screening programs represent a significant medium-term opportunity for kiosk vendors and integrators.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 415.3 Million |

| Forecast Revenue (2034) | US$ 1200.6 Billion |

| CAGR (2025-2034) | 11.20% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Standalone Kiosks, Mobile Kiosks, Wall-Mounted Units, Countertop Kiosks), By Component (Hardware, Software, Services), By Application (Teleconsultation, Vital Signs Monitoring, Pharmaceutical Dispensing & Counseling, Behavioral & Mental Health Assessment, Occupational Health & Preventive Screening), By End-User (Hospitals & Specialty Clinics, Community Health Centers, Pharmacies & Retail Clinics, Corporate Offices & Industrial Worksites, Educational Institutions & Government Facilities, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | KIOSK Information Systems, Olea Kiosks, REDYREF, Sonka Medical, American Well, CSI Health, AMD Global Telemedicine, Clinics On Cloud, Elo Touch, Versicles Technologies, OnMed, Howard Medical, MedAvail Technologies, PharmaSmart, UniDoc Health, Higi |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Key Player Analysis

Market participants span hardware-focused kiosk manufacturers, diagnostic-device specialists, and software-centric virtual-care platform providers. Hardware-oriented vendors focus on robust enclosure design, integrated peripherals, and scalable manufacturing to support large deployments across clinics and retail chains. Diagnostic-focused firms emphasize clinically validated sensors, regulatory compliance, and interoperability, enabling accurate vital-signs capture and seamless data flow into provider systems.

Software-led players offer comprehensive telehealth platforms, scheduling tools, and networked provider services that power kiosk-based consultations and care coordination. Integrated solution providers combine hardware, software, and services into turnkey telehealth stations, often targeting specific use cases like pharmacy-based care or corporate wellness. Community- and retail-focused innovators concentrate on user-friendly interfaces, population health screening, and analytics, strengthening kiosk adoption in high-traffic public locations.

Market Key Players

- KIOSK Information Systems

- Olea Kiosks

- REDYREF

- Sonka Medical

- American Well

- CSI Health

- AMD Global Telemedicine

- Clinics On Cloud

- Elo Touch

- Versicles Technologies

- OnMed

- Howard Medical

- MedAvail Technologies

- PharmaSmart

- UniDoc Health

- Higi

Recent Developments

- August, 2025 – Zebra Technologies to acquire Elo Touch Solutions

Zebra announced an agreement to acquire Elo Touch Solutions for about 1.3 billion USD, explicitly aiming to deepen its self-service and kiosk hardware footprint, which includes Elo’s healthcare and telemedicine kiosk touch displays used in patient check-in and telehealth workflows. - March, 2026 – OnMed CareStation market positioning

Coverage of OnMed’s CareStation in 2026 emphasized the kiosk’s role in closing care gaps amid physician shortages, with analysts noting that telehealth kiosks like OnMed’s are riding nearly 20% annual market growth through 2030 as they combine remote consults, diagnostics and AI-assisted triage in a single enclosure. - March, 2025 – Clinics On Cloud manufacturing and footprint expansion

Clinics On Cloud reported that it had surpassed 2,000 installed health kiosks across more than 200 Indian cities and five countries, supported by expanded manufacturing capacity and government plus PSU partnerships for “Health ATM” projects, reinforcing its positioning as a scaled health-kiosk OEM in emerging markets. - August, 2025 – Amwell (American Well) digital-first DHA contract extension

Amwell secured an extension of its next-generation “Digital First” contract as part of a Leidos-led consortium for the U.S. Military Health System, reinforcing federal-sector demand for its virtual-care platform; this platform architecture supports delivery via web, mobile and onsite telehealth kiosks across 9.6 million covered beneficiaries. - November, 2025 – Telehealth kiosk market growth signal (sector level)

Sector research in late 2025 indicated that the telehealth-kiosk space (including vendors such as OnMed, CSI Health, Clinics On Cloud and others) was tracking toward market value of about 10,452.13 million USD in 2025 and projected almost 29,353.36 million USD over the next few years, underlining why vendors continue to push new launches, partnerships and structured deployment programs.

Conclusion

The global telehealth kiosk market is experiencing steady growth, driven by rising demand for remote healthcare access, workforce shortages, and the expansion of digital health adoption. Standalone kiosks, hardware components, and teleconsultation applications continue to dominate the market due to their ease of deployment and integrated diagnostic capabilities.

Hospitals and specialty clinics remain key end users, while retail, workplace, and community deployments are gaining traction. North America leads the market with over 48.5% share, driven by strong infrastructure and reimbursement support.

Advancements in AI-enabled diagnostics, connectivity, and EHR integration are enhancing scalability. Overall, telehealth kiosks are evolving into comprehensive digital care stations that support efficient, accessible, and cost-effective healthcare delivery globally.