Introduction

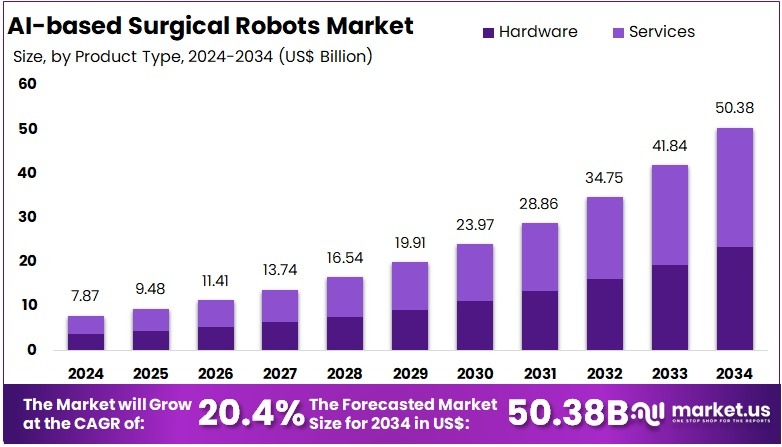

The AI-Based Surgical Robots Market is projected to surge from US$ 7.87 Billion in 2024 to about US$ 50.38 billion by 2034, registering a robust 20.4% CAGR. This expansion reflects rising surgical volumes, growing chronic disease burden, and accelerating adoption of minimally invasive procedures supported by AI-driven precision and real-time analytics.

Services represent over 53.7% of market value due to ongoing maintenance, software upgrades, and training, while hospitals account for 73.9% of demand. With North America holding over 42.2% share in 2024, policymakers, providers, and technology vendors are jointly fueling long-term structural growth.

Click the sample report link for complete industry insights @ https://market.us/report/ai-based-surgical-robots-market/free-sample/

Key Takeaways

- The global AI-based surgical robots market is expected to expand from US$ 7.87 Billion in 2024 to approximately US$ 50.38 Billion by 2034, reflecting a CAGR of 20.4% over the forecast period.

- Within product type segmentation, the services segment held a dominant share exceeding 53.7% in 2024, supported by increasing demand for maintenance, software upgrades, and technical training.

- Semi-autonomous systems accounted for more than 44.1% of the market in 2024, driven by rising adoption of platforms combining automated functionality with surgeon supervision to improve procedural accuracy.

- By application, general surgery represented over 29.7% share in 2024, highlighting broad utilization of AI-enabled robotic systems across diverse surgical procedures.

- Hospitals dominated the end-user segment with above 73.9% share in 2024, supported by higher installation rates in large healthcare institutions and advanced surgical facilities.

- North America captured more than 42.2% market share in 2024, equivalent to around US$ 3.32 billion, driven by strong healthcare investments and early technology adoption.

How Growth Is Impacting the Economy

Rapid growth in AI-based surgical robots is catalyzing a high-value medical technology ecosystem spanning hardware manufacturing, software development, and specialized clinical services. Capital investments in robotic platforms, imaging modules, and sensors drive upstream demand for advanced components and engineering talent, creating skilled jobs and boosting R&D intensity.

As hospitals integrate AI-enabled robots across general, orthopedic, neurological, and urological surgeries, productivity gains shorter procedures, fewer complications, and reduced length of stay translate into more efficient use of hospital infrastructure and public health budgets.

Over time, wider adoption supports the shift from open to minimally invasive surgery, lowering indirect economic costs from lost workdays and long recovery. At a system level, regulatory clarity, digital health strategies, and national scaling initiatives (such as NHS England’s target of 500,000 robotic procedures annually by 2035) signal stable policy support, encouraging long-horizon private investment and industrial innovation.

Impact on Global Businesses

Global businesses across medtech, software, telecom, and healthcare services are feeling the impact of rising AI-based surgical robot deployment. Manufacturers face higher development and compliance costs due to stringent cybersecurity mandates, detailed documentation, and lifecycle risk management requirements.

Connectivity dependence for advanced and remote functions is pushing demand for high-reliability networks, edge computing, and 5G infrastructure, raising capex but also unlocking premium service opportunities.

Key Segmentation Analysis

The AI-based surgical robots market is segmented by product type, level of automation, application, and end-user, enabling targeted growth strategies and positioning. By product type, hardware and services jointly underpin value creation, with services contributing over 53.7% share as hospitals prioritize uptime, performance, and continuous AI upgrades.

By level of automation, semi-autonomous systems hold more than 44.1% share, while autonomous and telerobotic systems are poised for faster growth as regulatory and network barriers ease. Application segments include general, orthopedic, neurological, urological, gynecological, and other surgeries, with general surgery accounting for over 29.7%.

End-users are primarily hospitals, which represent more than 73.9% of demand, followed by ambulatory surgical centers that are gaining traction as minimally invasive outpatient procedures scale globally.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Sector-Specific Impacts

- Healthcare providers: Large hospitals are prioritizing robotic-capable operating rooms, reallocating budgets toward surgical automation and related workforce training.

- Telecom and cloud: 5G and edge providers gain new clinical workloads from telesurgery, tele-mentoring, and real-time video analytics.

- Insurance and HTA bodies: Evidence frameworks such as NICE’s programs are reshaping reimbursement, favoring technologies with proven outcome and cost benefits.

Strategies for Businesses

- Invest in integrated ecosystems: Combine hardware, AI software, training, and services to capture the >53.7% services-heavy value pool and lock in hospital relationships.

- Prioritize cybersecurity and regulatory intelligence: Align product roadmaps with FDA cybersecurity guidance and global device regulations to reduce approval friction.

- Build data and interoperability capabilities: Design systems around interoperable standards and perioperative data pipelines to power AI model training and differentiated decision support.

- Target high-growth use cases: Focus on general surgery, orthopedics, and gynecology, which collectively capture a significant share of applications and show strong robotic adoption.

- Develop ASC-ready solutions: Offer compact, cost-optimized platforms tailored to ambulatory surgical centers as minimally invasive day-care procedures expand.

Analyst Viewpoint

Currently, the AI-based surgical robots market is transitioning from early specialist deployment to scaled, system-level integration across major surgical service lines. Evidence of improved precision, reduced complications, and shorter hospital stays is strengthening clinician and payer confidence. Semi-autonomous systems dominate today due to the need for strong surgeon oversight and regulatory caution, but autonomous and telerobotic platforms are advancing rapidly.

Over the next decade, expansion of national digital-health strategies, structured training, and favorable HTA frameworks should gradually normalize robotic surgery as a standard of care in high-income markets. Longer term, global diffusion into emerging economies, combined with 5G-enabled remote surgery and AI-enhanced video understanding, positions this industry for sustained double-digit growth and broader impact on surgical accessibility worldwide.

Use Case and Growth Factors

| Aspect | Details |

| Use Case 1 | AI-guided general surgery (hernia, bariatric, colorectal) improving precision, reducing recovery times and complications for high-volume procedures. |

| Use Case 2 | Orthopedic joint replacement using robotic navigation for accurate implant alignment, lowering revision rates and speeding rehabilitation. |

| Use Case 3 | Neurological and urological procedures requiring fine motor control, leveraging real-time imaging and AI decision support for safer interventions. |

| Use Case 4 | Telerobotic and tele-mentored surgeries extending specialist expertise to remote or underserved regions via low-latency networks. |

| Growth Factor 1 | National scaling initiatives (e.g., NHS plan for ~500,000 robotic procedures annually by 2035) and structured procurement frameworks. |

| Growth Factor 2 | Global surgical workforce shortages and unmet need exceeding 160 million essential operations annually. |

| Growth Factor 3 | Regulatory programs and HTA frameworks that validate safety, expand indications, and streamline evidence generation. |

| Growth Factor 4 | Expansion of 5G, edge computing, and interoperability initiatives enhancing real-time data, video analytics, and remote capabilities. |

Regional Analysis

North America leads the AI-based surgical robots market with more than 42.2% share and approximately US$ 3.32 billion in value in 2024, driven by early adoption, strong hospital infrastructure, and a mature regulatory environment. The U.S. benefits from FDA-approved pathways (510(k), De Novo, PMA) for AI/ML-enabled devices, well-defined cybersecurity rules, and established reimbursement in selected orthopedic indications.

Canada supports growth via standardized coding and benchmarking of robotic procedures, creating a unified data environment. Europe is strengthened by NICE evidence-generation frameworks and national robotics programs, while Asia Pacific markets such as China, Japan, India, and South Korea are scaling through digital-health strategies and hospital modernization.

Latin America and Middle East & Africa represent emerging opportunities, as tertiary centers adopt robotic platforms and telecom infrastructure improves, but broader penetration remains at an earlier stage.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Business Opportunities

Significant opportunities exist in developing semi-autonomous and telerobotic platforms that can be deployed across multi-site hospital networks and ambulatory surgical centers. Vendors can capture recurring revenue through service contracts, software subscriptions, AI upgrades, and video analytics platforms integrated into surgical workflow.

5G-enabled tele-mentoring, remote proctoring, and cross-site collaboration open new models for training, clinical support, and cross-border care. There is also headroom for mid-cost, compact systems targeting emerging markets and secondary hospitals that currently lack access to premium robotics.

Partnerships between medtech firms, telecom operators, cloud providers, and academic health systems will be essential to commercialize telesurgery, scale digital platforms, and accelerate evidence generation.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 7.87 Billion |

| Forecast Revenue (2034) | US$ 50.38 Billion |

| CAGR (2025-2034) | 20.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Hardware, Services), By Level of Automation (Semi-Autonomous Systems, Autonomous Systems, Telerobotic Systems), By Application (General Surgery, Orthopedic Surgery, Neurological Surgery, Urological Surgery, Gynecological Surgery, Others), By End-User (Hospitals, Ambulatory Surgical Centers) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Intuitive Surgical Inc., Medtronic plc, Johnson & Johnson (Auris Health), Stryker Corporation, Zimmer Biomet Holdings Inc., Accuray Incorporated, CMR Surgical Ltd., Asensus Surgical Inc., Activ Surgical Inc., Titan Medical Inc., Medrobotics Corporation, Smith & Nephew plc, Renishaw plc, Vicarious Surgical Inc., Othe key players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Key Player Analysis

Market leadership is concentrated among a group of large, diversified medical technology companies that combine extensive installed bases with strong surgeon training ecosystems and AI-enhanced visualization and workflow tools. These incumbents leverage integrated imaging, robotic hardware, and instrument portfolios to generate both capital and recurring revenues, reinforced by long-term enterprise procurement agreements.

Orthopedic-focused platforms specializing in AI-enabled planning and navigation for joint replacement and spine surgery are critical growth engines, building closed-loop implant–robot ecosystems that deepen customer loyalty. Alongside, emerging innovators are introducing more compact, cost-efficient robotic systems with advanced computer vision, digital laparoscopy, and navigation features targeting secondary hospitals and ambulatory centers.

Competitive differentiation increasingly depends on software capabilities, cybersecurity strength, clinical evidence, and the scalability of platform architectures across multiple procedures and regions.

Market Key Players

- Intuitive Surgical Inc.

- Medtronic plc

- Johnson & Johnson (Auris Health)

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Accuray Incorporated

- CMR Surgical Ltd.

- Asensus Surgical Inc.

- Activ Surgical Inc.

- Titan Medical Inc.

- Medrobotics Corporation

- Smith & Nephew plc

- Renishaw plc

- Vicarious Surgical Inc.

- Othe key players

Recent Developments

- Intuitive Surgical Inc.: The company reported that more than 3.2 million procedures were performed on its systems in 2025 and that the installed base surpassed 12,000 systems after placing about 1,900 new robots, underscoring continued scale-up despite macro headwinds.

- Medtronic plc: Medtronic announced the first US surgery using its Hugo robotic-assisted surgery (RAS) system at Cleveland Clinic, marking a key inflection point as Hugo shifts from an ex-US growth story into the US soft-tissue robotics market.

- Stryker Corporation: Stryker introduced the fourth-generation Mako system, Mako 4, offering a single platform across total hip, total knee, partial knee and spine, integrated with its latest Q Guidance System to streamline workflows and extend indications.

- CMR Surgical Ltd.: CMR Surgical closed a funding round of more than 200 million USD (equity plus debt), supported by existing backers and new investor Trinity Capital, to accelerate global commercialization of its Versius surgical robotic system.

- Vicarious Surgical Inc.: The company issued 2026 cash-burn guidance of about 35 million USD, an improvement of 10 million versus updated 2025 guidance, and estimated that it would need approximately 25 million USD beyond existing cash to reach design freeze.

- Activ Surgical Inc.: While Activ Surgical’s most visible milestones, such as its first AI-enabled surgical case with ActivSight and introduction of the ActivEdge platform, pre-date 2025, they remain strategically relevant because ActivSight is 510(k)-cleared and designed as an add-on module to existing OR infrastructure.

Conclusion

The AI-based surgical robots market is entering a sustained high-growth phase, supported by rising hospital adoption, expanding service-led revenue models, and increasing deployment of semi-autonomous systems. Strong regional leadership in North America, combined with policy support, digital health strategies, and regulatory clarity, is accelerating commercialization.

Productivity gains from minimally invasive procedures, shorter recovery times, and improved surgical precision are strengthening economic and clinical value propositions. Growing investments in AI software, connectivity, and training ecosystems are further enhancing scalability.

Over the forecast period, integration across specialties, expansion into ambulatory centers, and emerging-market adoption are expected to drive long-term structural growth and recurring revenue opportunities.

Disclaimer: This press release/article is provided by a third party, which is solely responsible for its content. It is published on Sci-tech Today exactly as received from the issuing organization, without any edits, verification, or endorsement by Sci-tech Today.

Sci-tech Today does not guarantee the accuracy, completeness, or reliability of the information. Readers are advised to independently verify all information and do their research before acting on it or investing any money. Sci-tech Today is not responsible for any financial loss that may result from reliance on this content.