Market Overview

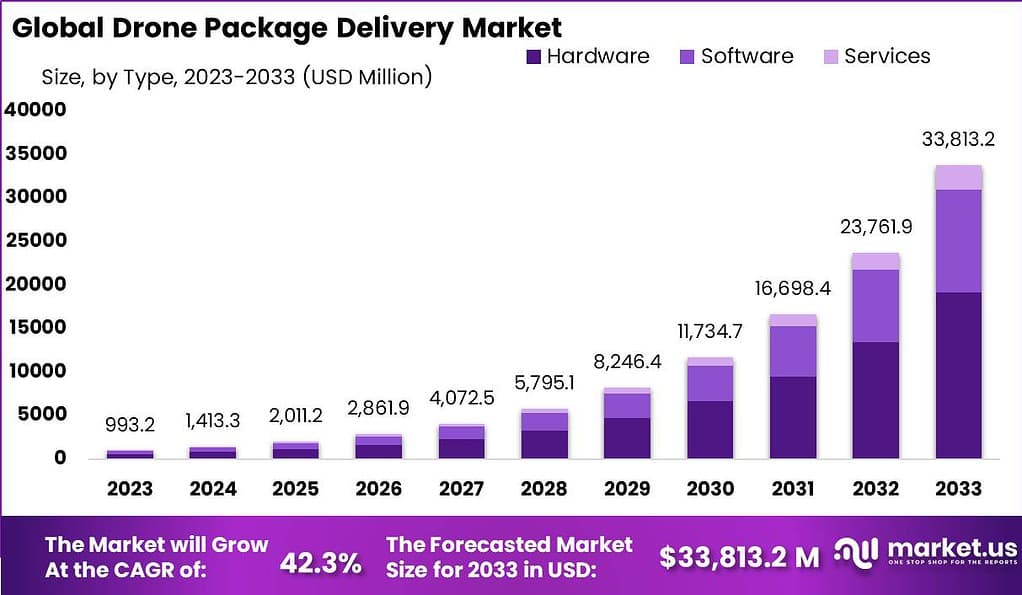

The global Drone package delivery market is set for extraordinary expansion. Valued at USD 993.2 million in 2023, the market is projected to reach USD 33,813.2 million by 2033. This growth reflects a remarkable CAGR of 42.3% across the forecast period from 2024 to 2033, making it one of the fastest-growing segments in modern logistics.

Drone package delivery uses unmanned aerial vehicles (UAVs) to transport goods directly to customers. These systems bypass road traffic and traditional infrastructure, enabling faster last-mile delivery. Logistics firms, retailers, healthcare providers, and food services are the primary adopters of this technology worldwide.

Get further insight into the global trends shaping the future of the drone package delivery industry. Request Sample

E-commerce platforms rely on drone delivery to meet growing consumer expectations for same-day and on-demand fulfilment. Healthcare organizations use drones to deliver medicines and medical supplies to remote communities. Food delivery platforms deploy drones to reduce wait times and improve meal freshness in dense urban areas.

Advances in AI, machine learning, and sensor technology are transforming drone delivery systems. Modern UAVs can navigate autonomously, avoid obstacles in real time, and optimize flight paths. These improvements increase delivery reliability, reduce operational costs, and expand the viable range of drone delivery networks.

Regulatory environments are gradually becoming more supportive of commercial drone operations. Governments in North America, Europe, and Asia Pacific are creating frameworks that allow companies to test and scale drone delivery services. Clearer airspace rules reduce compliance burdens and give businesses the confidence to invest in UAV infrastructure.

According to DHL, over 60% of major logistics companies are expected to integrate drone delivery by 2024. The Consumer Technology Association reports that approximately 50% of consumers will be comfortable with drone deliveries by year-end 2024. These figures signal that mainstream adoption is accelerating, creating strong demand across the global supply chain ecosystem.

Key Takeaways

- The global drone package delivery market was valued at USD 993.2 million in 2023.

- The market is forecast to reach USD 33,813.2 million by 2033, registering a CAGR of 42.3%.

- By component, hardware leads the market with a revenue share of 56.8%.

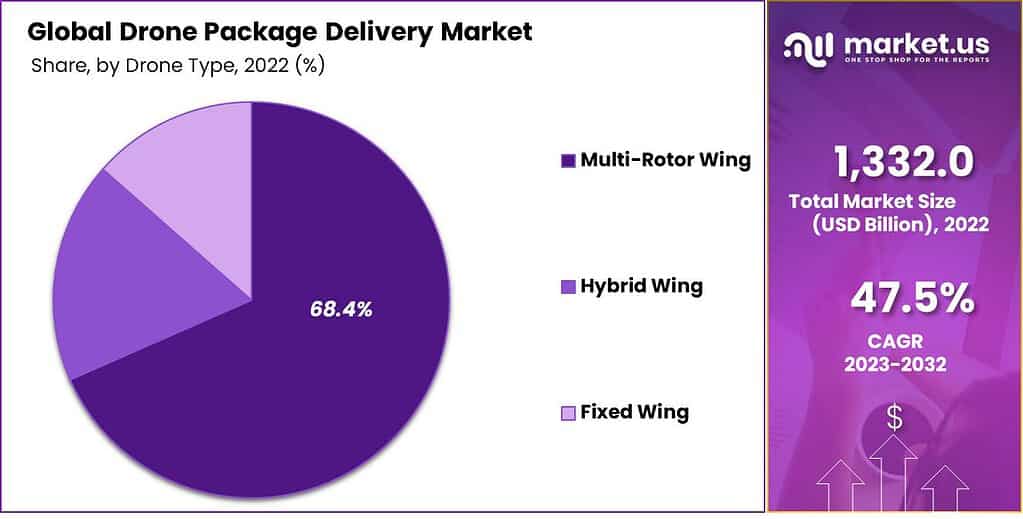

- By drone type, multi-rotor wing drones dominate with a revenue share of 68.4%.

- By package size, less than 2 kg leads the market with a share of 44.6%.

- By duration, less than 30 minutes leads with a revenue share of 60.4%.

- By operation mode, remotely piloted drones hold a revenue share of 52.6%.

- By end-use, food delivery dominates with a revenue share of 38.6%.

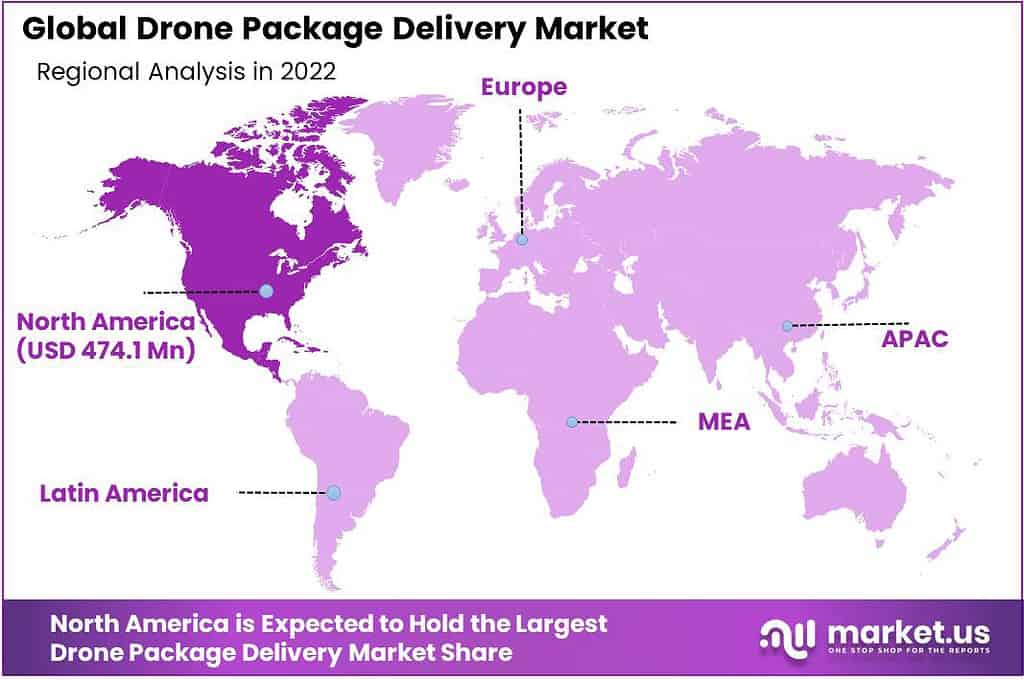

- North America leads all regions with a market share of 35.6%.

Market Segmentation Overview

Hardware leads the drone package delivery market by component, capturing a revenue share of 56.8%. Physical drone systems — including propulsion units, sensors, and communication devices — form the backbone of every delivery operation. As flight performance demands increase, manufacturers continue to invest heavily in hardware innovation, reinforcing this segment’s dominant position.

Multi-rotor wing drones hold a commanding revenue share of 68.4% by drone type. Their vertical takeoff and landing capability makes them ideal for urban environments where runway space is unavailable. Moreover, their precise maneuverability supports deliveries to rooftops and narrow locations, making them the preferred choice for last-mile logistics providers.

Packages under 2 kg account for 44.6% of the market by weight category. Lightweight packages dominate e-commerce, pharmaceutical, and food delivery applications where speed and frequency are critical. Additionally, drones optimized for sub-2 kg payloads face fewer regulatory restrictions, accelerating operational approval timelines for businesses.

Deliveries completed in under 30 minutes lead the duration segment with a share of 60.4%. Ultra-fast delivery aligns with consumer expectations in food, retail, and healthcare sectors. Regulatory approvals also tend to be more accessible for short-range flights, giving operators a practical advantage in scaling same-day delivery networks.

Remotely piloted operation mode commands a revenue share of 52.6%. Human oversight remains a priority for businesses and regulators who require real-time intervention capability. Consequently, this mode benefits from mature technology and streamlined compliance processes, making it the most commercially viable option for current deployment at scale.

Food delivery dominates end-use applications with a revenue share of 38.6%. Urban consumers increasingly demand fast, contactless meal delivery — a trend that accelerated sharply during the COVID-19 pandemic. Drones reduce delivery times and preserve food quality, giving food service operators a meaningful competitive edge in high-density markets.

Drivers

Surging demand for last-mile and remote delivery services is the primary engine of market growth. E-commerce expansion and rising consumer expectations for rapid fulfilment push companies to explore faster alternatives to road-based delivery. Drones bypass congested infrastructure, enabling cost-effective delivery to urban and underserved rural areas alike.

Growing environmental consciousness is also accelerating adoption across logistics and retail sectors. Drones produce significantly lower carbon emissions than conventional delivery vehicles, aligning with corporate sustainability goals and government climate targets. This environmental advantage strengthens the commercial case for drone delivery investment, particularly as ESG reporting becomes standard practice.

Use Cases

Food delivery platforms use drones to transport restaurant meals directly to residential doorsteps in dense urban neighborhoods. This approach cuts delivery times, maintains food temperature, and eliminates road traffic delays. Customers benefit from faster service, while restaurants gain a reliable fulfilment channel that supports high order volumes without additional vehicle fleets.

Healthcare organizations deploy drones to deliver medicines, test samples, and emergency supplies to remote or underserved communities. In August 2023, Wing and Apian partnered to launch medical drone deliveries in Ireland, demonstrating real-world clinical viability. This application improves patient outcomes in areas where ground-based medical logistics are slow or unreliable.

Major Challenges

Fragmented regulatory frameworks across countries create significant compliance burdens for drone delivery operators. Businesses must navigate varying airspace rules, safety standards, and permitting processes in each market they enter. This complexity slows expansion timelines and increases operational costs, particularly for companies targeting cross-border or multi-regional logistics networks.

Geopolitical tensions introduce supply chain vulnerabilities that affect drone component manufacturing and distribution. Trade disputes and export restrictions can disrupt access to critical hardware such as sensors, batteries, and navigation modules. Additionally, economic downturns may reduce corporate investment in emerging delivery technologies, temporarily slowing the pace of fleet deployment and infrastructure buildout.

Business Opportunities

Advances in drone hardware — including higher payload capacity and extended flight range — are unlocking new delivery applications beyond lightweight parcels. Companies that invest in next-generation UAV platforms can expand into pharmaceutical cold-chain logistics, industrial parts distribution, and time-sensitive retail fulfilment. These segments represent significant untapped revenue potential across both developed and emerging markets.

Urban Air Mobility infrastructure development offers a structural opportunity for long-term market growth. Vertiports, drone charging networks, and dedicated air corridors are emerging in major cities globally. Businesses that participate in this infrastructure buildout — whether as operators, technology providers, or real estate partners — can secure competitive positioning before mainstream urban drone traffic scales significantly.

Regional Analysis

North America leads the global drone package delivery market with a revenue share of 35.6%. The region hosts a mature ecosystem of drone manufacturers, technology firms, and major logistics operators including Amazon and UPS. Relatively favorable regulatory conditions, high e-commerce penetration, and strong infrastructure investment collectively sustain North America’s leadership in UAV delivery deployment.

Asia Pacific is forecast to grow at the fastest CAGR during the forecast period. Rapid urbanization, explosive e-commerce growth, and densely populated megacities create ideal conditions for drone delivery adoption. Countries such as China, Japan, and India are investing heavily in UAV technology and smart city infrastructure, positioning the region as the next major growth frontier for autonomous delivery systems.

Recent Developments

- August 2023 — Wing and Apian, a UK-based healthcare drone services firm, partnered to launch medical drone deliveries in Ireland and jointly explore expansion opportunities across the United Kingdom.

- August 2023 — Wing and Walmart launched a collaborative drone delivery service in the Dallas-Fort Worth area, covering a wide product range including meals, groceries, and prescription medicines.

Conclusion

The global drone package delivery market is on a trajectory of exceptional growth, expanding from USD 993.2 million in 2023 at a CAGR of 42.3%. Rising e-commerce demand, supportive regulatory evolution, and accelerating AI integration are collectively driving this expansion. Environmental sustainability benefits further strengthen the long-term commercial case for widespread UAV delivery adoption.

Hardware components and multi-rotor wing drones dominate their respective segments, reflecting the market’s current technological priorities. Food delivery leads end-use applications, while remotely piloted operation modes remain the compliance-preferred choice for most operators. North America maintains market leadership, though Asia Pacific is rapidly closing the gap with superior growth momentum.

Companies seeking to capture market share must invest in next-generation hardware, build regulatory expertise across key geographies, and align delivery offerings with consumer demand for speed and sustainability. Businesses that act early on UAM infrastructure and autonomous navigation capabilities will be best positioned to lead as the market approaches its projected value of USD 33,813.2 million by 2033.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at [email protected]