Introduction

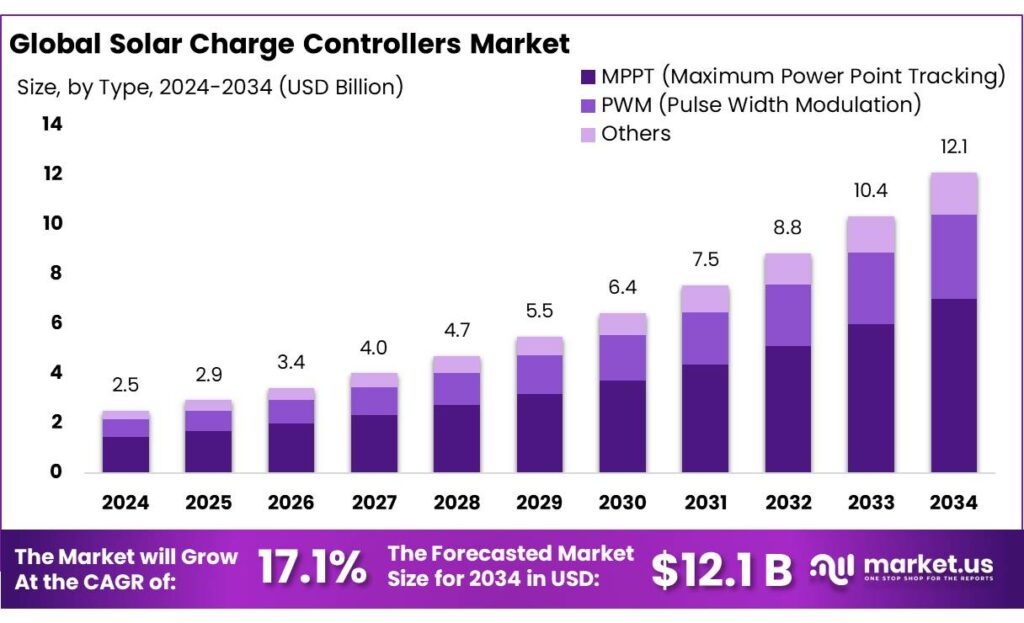

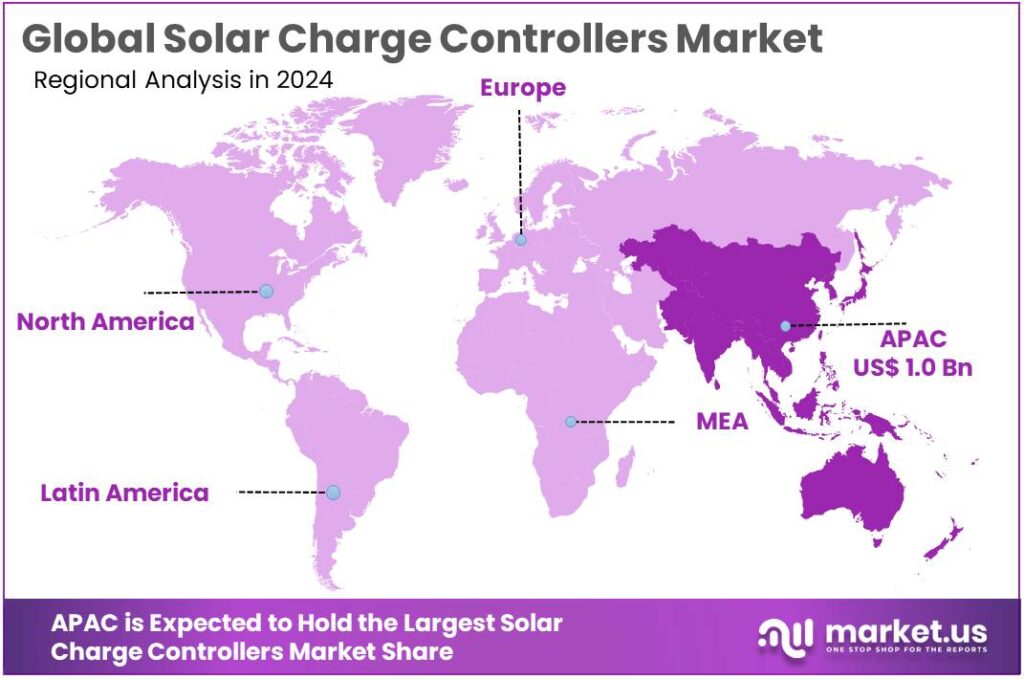

The global solar charge controllers market is projected to grow strongly, reaching USD 12.1 billion by 2034 from USD 2.5 billion in 2024, expanding at a 17.1% CAGR from 2025 to 2034. In 2024, Asia Pacific led the market with a 41.90% share, accounting for nearly USD 1.0 billion in revenue, supported by strong rooftop solar adoption, rural electrification, and large-scale renewable investments.

Solar charge controllers play an essential role in solar power systems by regulating voltage and current flow from PV panels to batteries and connected loads. They help prevent battery overcharging, deep discharge, and system instability, making them highly important in off-grid, hybrid, and small grid-connected installations. Their demand is rising alongside solar PV expansion, as global installed solar capacity reached 1,865 GW by the end of 2024, compared with 710 GW in 2020, with 451 GW added in 2024 alone.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

The market is being shaped by the rapid scale-up of solar installations worldwide. Cumulative solar PV capacity reached nearly 1.6 TW in 2023, rising from 1.2 TW in 2022, while annual renewable additions increased by almost 50% to 510 GW, the fastest pace seen in two decades. As solar module prices continue to decline, demand is shifting toward advanced power electronics, monitoring features, and intelligent charge management systems.

A major growth driver is the rising need for distributed and off-grid energy access. In 2023, around 750 million people still lacked electricity access, with sub-Saharan Africa representing nearly 80% of this population. Off-grid solar remains the most cost-effective solution for 41% of first-time electricity connections expected by 2030, and the sector has already served about 560 million people globally.

India is also emerging as a strong growth center. The country’s solar capacity reached 132.85 GW, including 23.16 GW rooftop and 5.55 GW off-grid systems. Government-backed schemes such as PM Surya Ghar and PM-KUSUM are further creating strong demand for controller-integrated solar systems across households and agricultural pumps.

Top Market Takeaways

- Solar Charge Controllers Market size is expected to be worth around USD 12.1 Billion by 2034, from USD 2.5 Billion in 2024, growing at a CAGR of 17.1%.

- MPPT (Maximum Power Point Tracking) held a dominant market position, capturing more than a 57.8% share.

- Natural held a dominant market position, capturing more than a 45.2% share.

- Asia Pacific held a dominant regional position in the solar charge controller market, capturing 41.90% of regional share with an estimated market value of USD 1.0 billion.

Scope and Research Methodology

The scope of the solar charge controllers market study covers a detailed assessment of the industry across product type, technology, voltage rating, application, end-use, and region. The analysis includes key controller technologies such as PWM and MPPT, along with their use across residential rooftop systems, commercial solar installations, industrial backup systems, agricultural pumps, telecom towers, street lighting, and off-grid rural electrification projects.

The research methodology follows a balanced combination of primary and secondary research approaches to ensure reliable market insights. Secondary research includes the study of government renewable energy reports, ministry publications, utility data, company annual reports, trade journals, industry white papers, and trusted energy agency databases to understand market size, technology trends, and policy developments. Primary research includes interviews with manufacturers, distributors, EPC companies, solar installers, battery system integrators, and industry experts to validate market assumptions and demand trends.

By Type Analysis

MPPT dominates with 57.8% share, supported by higher efficiency and better solar energy optimization.

In 2024, MPPT (Maximum Power Point Tracking) held a dominant market position, capturing more than a 57.8% share. Its strong market presence was mainly supported by its ability to extract the highest possible power from solar panels even when sunlight intensity and temperature keep changing throughout the day. This makes MPPT controllers highly preferred in residential, commercial, and larger solar installations, where better energy output directly improves system performance.

By Application Analysis

Commercial applications lead with 45.2% share, driven by rising solar adoption across business facilities.

In 2024, the commercial application segment held a dominant market position, capturing more than a 45.2% share. This leadership was driven by the rising installation of solar systems across office buildings, retail complexes, warehouses, educational institutions, and small industrial units, where businesses are increasingly focused on lowering electricity expenses and improving energy security. Commercial buyers generally prefer high-performance charge controllers that offer stable output, remote monitoring, and battery storage compatibility, helping them manage energy usage more efficiently.

Regional Analysis: Asia Pacific

Asia Pacific leads with 41.90% share USD 1.0 Bn, supported by rapid solar growth and rising battery storage adoption.

In 2024, Asia Pacific held the leading position in the solar charge controller market, accounting for 41.90% of the global share, with an estimated value of nearly USD 1.0 billion. The region’s dominance was mainly supported by large-scale solar PV installations, rapid rooftop solar expansion, and increasing use of battery-backed energy systems across homes, businesses, and industrial facilities.

A major growth factor behind this leadership was the strong pace of policy-driven renewable energy development across countries such as China, India, Japan, and Southeast Asian nations. Government incentives, solar subsidy programs, and corporate clean-energy procurement pushed new solar projects at a faster pace, directly increasing demand for efficient charge controllers with MPPT capability, battery support, and remote monitoring features.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Top Key Players

- SUNGROW

- Morningstar Corporation

- Schneider Electric

- BEIJING EPSOLAR TECHNOLOGY CO. LTD

- Wenzhou Xihe Electric Co.,LTD.

- Sunforge LLC

- Luminous India

- KATEK Memmingen GmbH

- AIRKOM

- Victron Energy B.V.

Recent Developments

In 2024, Sunforge LLC strengthened its position in the solar charge controller space through its Genasun-branded MPPT controller portfolio, which is widely recognized for compact design and high efficiency performance. Products such as the GV-4 with 50 W capacity and the GV-10 with 140 W capacity remained popular in specialized solar and battery charging applications. A key strength of these controllers is their electrical efficiency of up to 99.85%, combined with extremely low self-consumption, making them well suited for rugged, remote, and battery-sensitive installations where every watt matters.

In 2024, Morningstar Corporation continued to maintain its reputation as a highly specialized solar charge controller provider with a strong global footprint. Since its establishment, the company has sold more than 4 million controllers and related solar power products across 100+ countries, reflecting long-term customer trust and strong adoption in off-grid, telecom, industrial, and remote power systems. This wide installed base highlights Morningstar’s continued strength in reliable and durable controller solutions.

In 2024, Sungrow Power Supply Co., Ltd. delivered strong financial and operational performance, supported by rapid global renewable energy deployment. The company reported approximately USD 10.2 billion in operating revenue, along with net profit of nearly USD 1.3 billion, demonstrating solid demand across its solar and power electronics portfolio. Its continued expansion in smart solar solutions, energy storage integration, and global renewable projects further strengthened its role in the solar charge controller and broader power conversion market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.5 Bn |

| Forecast Revenue (2034) | USD 12.1 Bn |

| CAGR (2025-2034) | 17.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (PWM (Pulse Width Modulation), MPPT (Maximum Power Point Tracking), Others), By Application (Industrial, Commercial, Residential) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | SUNGROW, Morningstar Corporation, Schneider Electric, BEIJING EPSOLAR TECHNOLOGY CO. LTD, Wenzhou Xihe Electric Co.,LTD., Sunforge LLC, Luminous India, KATEK Memmingen GmbH, AIRKOM, Victron Energy B.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |