Introduction

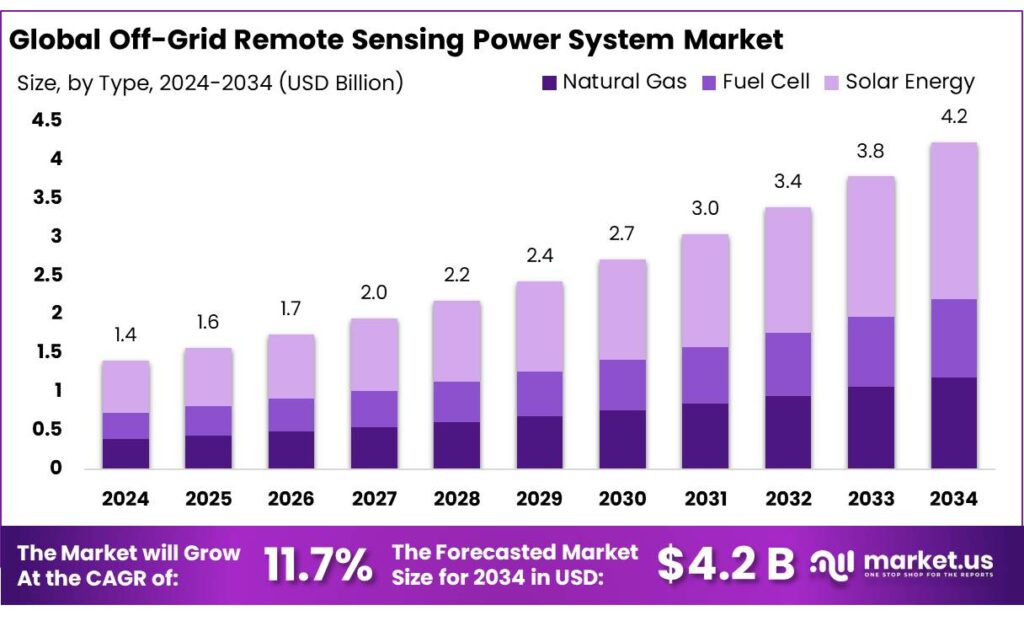

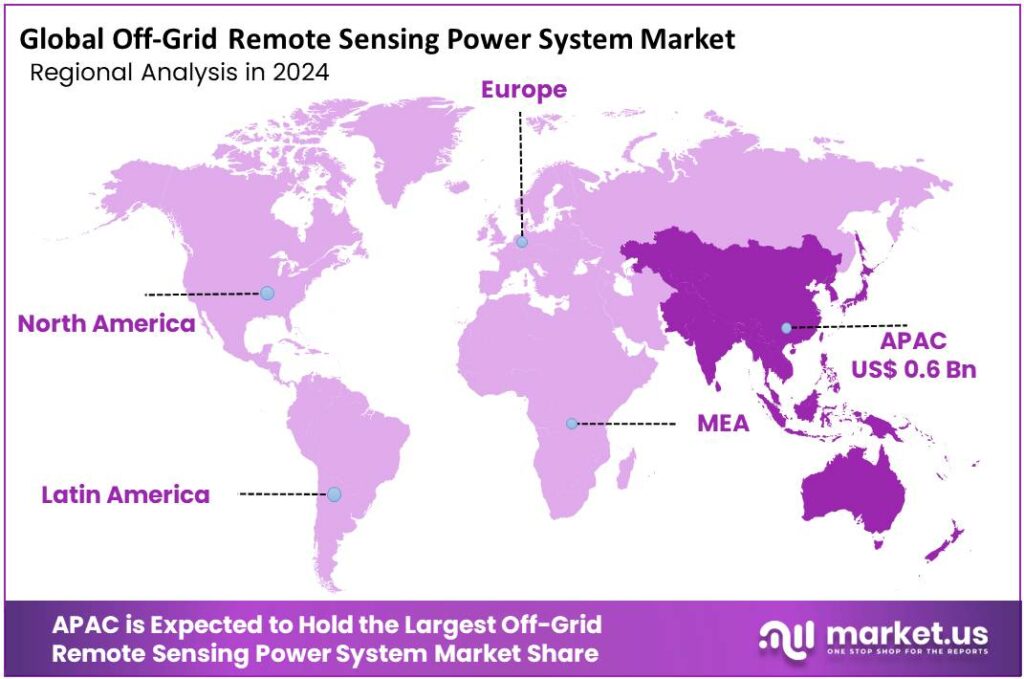

The global off-grid remote sensing power system market is projected to reach USD 4.2 billion by 2034, rising from USD 1.4 billion in 2024, and is expected to expand at aCAGR of 11.7% from 2025 to 2034. In 2024, Asia-Pacific remained the leading regional market, generating approximately USD 0.6 billion in revenue, supported by rising deployment of autonomous sensor infrastructure across agriculture, energy, mining, and climate-monitoring applications.

Off-grid remote sensing power systems are specialized energy solutions designed to keep sensors, data loggers, communication gateways, and telemetry devices operating in locations where grid electricity is unavailable or unstable. In agriculture and food supply chains, these systems are increasingly used for weather stations, irrigation controls, livestock tracking, cold-storage monitoring, and post-harvest logistics visibility. Their role is becoming more critical as the FAO estimates that13.3% of global food is still lost between harvest and retail, making better field-level measurement and storage monitoring a growing operational priority.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

The industrial landscape is evolving from simple single-sensor solar kits toward integrated edge power platforms that combine solar PV, battery storage, smart charge controllers, low-power processors, and resilient connectivity modules. This shift is reinforced by broader infrastructure gaps, as the IEA estimates that around 750 million people still lacked access to electricity in 2023, creating strong demand for quickly deployable autonomous power systems. At the same time, 1.2 billion people still lack adequate cooling access, according to SEforALL, increasing the need for off-grid telemetry in cold-chain and temperature-sensitive logistics.

Growth is further supported by the rapid expansion of solar and IoT ecosystems. The IEA reports that solar PV generation increased by 320 TWh in 2023, strengthening component availability and installer networks that support off-grid system deployment. In parallel, GSMA Intelligence forecasts 38.7 billion IoT connections by 2030, signaling a major increase in distributed sensors and remote assets that will require reliable edge-side power systems.

Policy and multilateral support are also strengthening long-term market prospects. The EU’s Copernicus Earth observation program, backed by the broader €14.88 billion EU Space Programme budget for 2021–2027, provides a major public data infrastructure for climate, agriculture, and environmental monitoring.

Global food security challenges remain significant, with 733 million people facing hunger in 2023, while the World Food Programme reached more than 124 million people in 2024 and identified a USD 13 billion funding need to support vulnerable populations. These conditions are increasing the strategic importance of remote sensing power systems for food security, humanitarian logistics, climate resilience, and last-mile infrastructure visibility.

Top Market Takeaways

- Off-Grid Remote Sensing Power System Market size is expected to be worth around USD 4.2 Billion by 2034, from USD 1.4 Billion in 2024, growing at a CAGR of 11.7%.

- Solar Energy held a dominant market position, capturing more than a 48.2% share.

- Oil and Gas Industry held a dominant market position, capturing more than a 49.8% share.

- Asia-Pacific (APAC) region emerged as a dominant force in the off-grid remote sensing power system market, capturing around 43.6% of the global share and contributing an estimated USD 0.6 billion.

Scope and Research Methodology

The scope of the off-grid remote sensing power system market covers autonomous energy solutions used to power remote sensors, telemetry units, data loggers, communication gateways, and edge monitoring devices in locations without reliable grid access. The study includes power technologies such as solar PV, wind-assisted systems, battery-backed hybrid systems, fuel cells, and micro-hydro-supported remote units. Major applications considered under the scope include agriculture monitoring, environmental sensing, weather stations, wildlife tracking, oil & gas field monitoring, mining sites, telecom towers, border surveillance, and humanitarian logistics.

The initial phase includes extensive review of public-domain sources, government publications, multilateral agencies, academic papers, industry white papers, energy statistics, and company annual reports. Trusted sources such as the IEA, FAO, GSMA, SEforALL, EU Copernicus, WFP, and national renewable energy agencies are used to validate macro trends including rural electrification gaps, food cold-chain monitoring, IoT expansion, and solar deployment growth. A bottom-up model is used by estimating the number of deployed remote sensing nodes across agriculture, weather, industrial, and environmental use cases, then multiplying by average system ASP.

By Type Analysis

In 2024, solar energy emerged as the leading power source in the off-grid remote sensing power system market, accounting for 48.2% of total share. Its dominance is primarily driven by high reliability, zero fuel dependency, and strong suitability for isolated deployment environments. Solar-powered systems are extensively used in weather stations, environmental monitoring units, border surveillance systems, agricultural telemetry, and remote communication nodes, where grid electricity is either unavailable or highly unreliable. The segment’s strong market position is further supported by declining solar module prices, improved battery integration, and minimal maintenance requirements, making it a cost-effective long-term solution.

By Application Analysis

By application, the oil and gas industry led the off-grid remote sensing power system market in 2024 with a 49.8% share, driven by the sector’s need for continuous monitoring across remote drilling sites, pipelines, and field assets. These systems are widely deployed in upstream and midstream environments to support leak detection, pressure measurement, seismic monitoring, corrosion tracking, and equipment health diagnostics. Because many exploration and transportation sites are located far from conventional power infrastructure, off-grid remote sensing power systems are essential for stable energy supply and uninterrupted real-time data transmission.

Regional Analysis: Asia Pacific

The Asia-Pacific region continues to lead the global off-grid remote sensing power system market, accounting for 43.6% of total share and generating approximately USD 0.6 billion in revenue by 2025. This strong regional position is primarily supported by the rapid deployment of renewable-powered sensing infrastructure, expanding rural electrification programs, and increasing demand for autonomous monitoring systems across agriculture, environment, and infrastructure sectors.

During 2024–2025, APAC emerged as the most dynamic regional market, driven by rising investments in solar-powered and hybrid off-grid energy solutions used to support remote weather stations, environmental telemetry, smart irrigation, wildlife tracking, and critical infrastructure sensing networks. Government-backed renewable energy expansion, combined with digital transformation initiatives across developing economies, has significantly accelerated adoption.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Top Key Players

- Siemens AG

- Schneider Electric

- General Electric

- ABB Ltd.

- Enphase Energy

- SunPower Corporation

- Canadian Solar Inc.

- Tesla, Inc.

Recent Developments

In 2025, Siemens reported group revenue of €78.9 billion, reflecting continued expansion across its smart infrastructure, electrification, and automation businesses. This strong scale highlights Siemens’ growing role in hybrid microgrids, distributed energy management, and intelligent automation systems, all of which are highly relevant for supporting autonomous power supplies in remote sensing installations and off-grid monitoring networks.

Similarly, Schneider Electric reported €38.15 billion in 2024 revenue, supported by strong performance in its energy management segment, which grew organically by 11.5% to €31.13 billion. This business strength reflects rising demand for distributed energy systems, microgrids, battery-backed backup solutions, and off-grid power management technologies, which are increasingly used in remote telemetry, industrial sensing, and decentralized monitoring applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.4 Bn |

| Forecast Revenue (2034) | USD 4.2 Bn |

| CAGR (2025-2034) | 11.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Natural Gas, Fuel Cell, Solar Energy), By Application (Oil and Gas Industry, Weather Monitoring Stations, Wind Power Industry, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Siemens AG, Schneider Electric, General Electric, ABB Ltd., Enphase Energy, SunPower Corporation, Canadian Solar Inc., Tesla, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |