Introduction

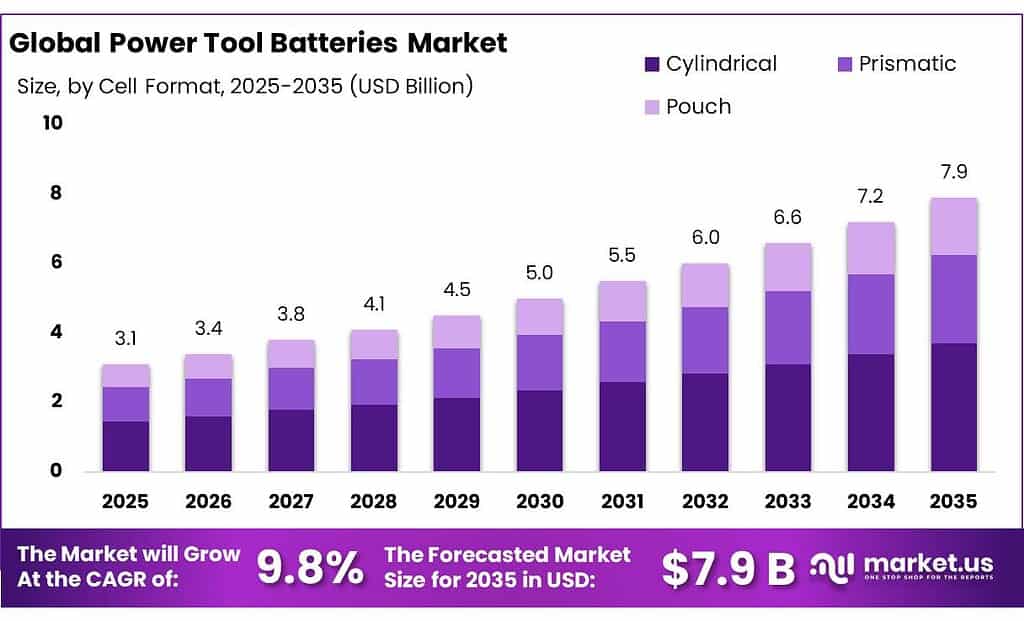

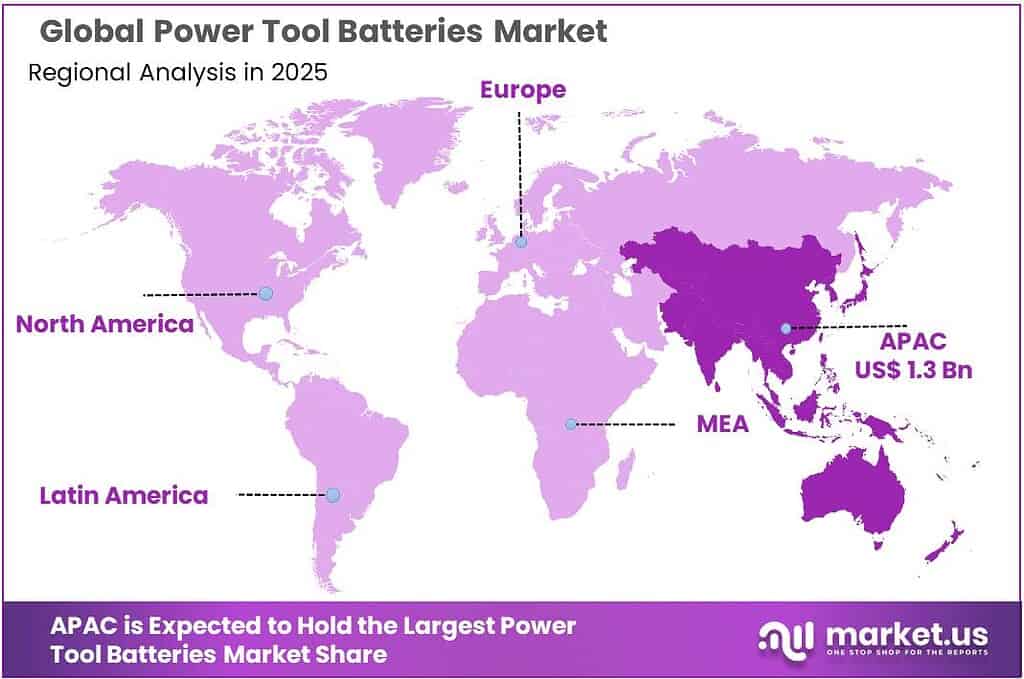

The global power tool batteries market is expected to reach USD 7.9 billion by 2035, growing from USD 3.1 billion in 2025 at a CAGR of 9.8% during 2026–2035. In 2025, Asia Pacific dominated the market, accounting for more than 44.8% share and generating around USD 1.3 billion in revenue. The region’s leadership is supported by strong manufacturing activity, rapid construction growth, and widespread adoption of cordless tools.

Power tool batteries are the core energy source for cordless tools, and the market is now increasingly shaped by lithium-ion technology, battery platform compatibility, and lifecycle efficiency rather than simple replacement demand. The broader battery industry is expanding at a large scale, which is improving cell availability, lowering input costs, and accelerating innovation. The International Energy Agency noted that lithium-ion battery pack prices dropped by 20% in 2024, the sharpest decline since 2017, creating cost advantages that also benefit cordless power tools.

Get a comprehensive report summary that describes the value and forecast along with methodology. Download the PDF brochure

A major trend in the market is the growing focus on cross-brand battery compatibility systems. For example, Bosch reported that its AMPShare platform has sold more than 85 million batteries, showing how interoperability is becoming a key competitive advantage in professional tools. At the same time, leading manufacturers continue to invest heavily in product development, with companies such as Bosch and Hilti expanding cordless portfolios and launching new battery-powered solutions.

The main factors driving demand include higher productivity, better mobility, labor efficiency, and improved workplace safety. Contractors increasingly prefer cordless tools because they reduce setup time, remove the need for temporary power access, and improve flexibility in confined or elevated job sites. This is making battery-powered systems more attractive across construction, industrial maintenance, and DIY applications.

Government regulations are also reshaping the market landscape, especially around battery recycling, traceability, and circular economy compliance. In the European Union, updated battery recycling rules require 65% recycling efficiency for lithium-based batteries by the end of 2025, increasing to 70% by 2030, while also setting ambitious material recovery targets for lithium and key metals.

In the United States, policy support is also strengthening the market outlook. The Department of Energy’s USD 25 million funding across 11 projects announced in late 2024 is aimed at advancing next-generation battery manufacturing technologies. These initiatives are expected to favor suppliers that can deliver high-cycle, recoverable, and regulation-compliant batteries with stronger traceability features, supporting long-term growth in the power tool batteries market.

Top Market Takeaways

- Power Tool Batteries Market size is expected to be worth around USD 7.9 Billion by 2035, from USD 3.1 Billion in 2025, growing at a CAGR of 9.8%.

- Lithium-ion held a dominant market position, capturing more than a 76.3% share.

- Cylindrical held a dominant market position, capturing more than a 47.4% share.

- 12 to 18 V held a dominant market position, capturing more than a 48.3% share.

- Industrial held a dominant market position, capturing more than a 39.1% share.

- Asia Pacific emerged as the dominant regional market in 2025, accounting for 44.8% of the global power tool batteries market, with an estimated value of USD 1.3 billion.

Scope and Research Methodology

The power tool batteries market report covers batteries used in cordless power tools such as drills, saws, grinders, impact drivers, and other industrial and household tools. The study mainly focuses on battery types such as lithium-ion, nickel-cadmium, and other rechargeable technologies, along with their use in professional, industrial, construction, and DIY applications.

The report examines important market areas including market size, growth rate, key trends, drivers, restraints, and future opportunities. It also studies demand by battery type, voltage range, tool application, end users, and regional markets such as Asia Pacific, North America, Europe, and other regions. The scope also includes analysis of technology advancements, battery life improvements, charging solutions, and recycling trends.

The power tool batteries market report covers batteries used in cordless power tools such as drills, saws, grinders, impact drivers, and other industrial and household tools. The study mainly focuses on battery types such as lithium-ion, nickel-cadmium, and other rechargeable technologies, along with their use in professional, industrial, construction, and DIY applications.

The report examines important market areas including market size, growth rate, key trends, drivers, restraints, and future opportunities. It also studies demand by battery type, voltage range, tool application, end users, and regional markets such as Asia Pacific, North America, Europe, and other regions. The scope also includes analysis of technology advancements, battery life improvements, charging solutions, and recycling trends.

By Type Analysis

In 2025, lithium-ion batteries dominated the power tool batteries market, accounting for more than 76.3% of the total share. Their leading position is mainly due to advantages such as longer runtime, lightweight design, fast charging, and stable power delivery. These benefits make lithium-ion batteries highly suitable for cordless tools used in drilling, cutting, fastening, and other heavy-duty tasks. Their ability to maintain strong performance during long working hours continues to make them the preferred choice among users.

By Cell Format Analysis

In 2025, the cylindrical cell format held the largest market share, capturing over 47.4%. This dominance is supported by its durable structure, strong thermal stability, and easy compatibility with cordless power tools. Manufacturers prefer cylindrical cells because they provide reliable energy output, better resistance to physical stress, and consistent performance in demanding job site conditions. Their standardized design also makes battery pack assembly easier and more cost-effective for mass production.

By Voltage Class Analysis

In 2025, the 12 to 18 V voltage class led the market with more than 48.3% share. This range is widely preferred because it offers the best balance between power, portability, and battery life. It is commonly used in drills, drivers, grinders, and saws, where users need sufficient power for everyday work without increasing tool weight. Both professional users and DIY consumers favor this voltage range for its ability to handle medium-duty as well as demanding applications efficiently.

By Application Analysis

In 2025, the industrial application segment dominated the power tool batteries market, holding over 39.1% share. This leadership comes from the heavy daily use of cordless power tools in manufacturing plants, construction sites, automotive workshops, and maintenance operations. Industrial users require batteries that offer long runtime, quick charging, and reliable power output to minimize downtime. The growing shift toward cordless tools in industrial environments is further increasing battery demand by improving worker mobility, convenience, and overall productivity.

Regional Analysis: Asia Pacific

In 2025, Asia Pacific led the global power tool batteries market, capturing 44.8% of the total share and reaching an estimated value of USD 1.3 billion. The region’s strong position is mainly driven by its large manufacturing base, rapid urbanization, and ongoing growth in construction and industrial activities. These factors continue to create strong demand for cordless power tools and their battery systems.

Major countries including China, India, Japan, and South Korea are key contributors to this growth, with rising usage of cordless drills, impact drivers, grinders, and demolition tools. These tools depend heavily on advanced lithium-ion battery packs for reliable performance. In addition, the fast expansion of residential and commercial infrastructure projects, combined with increasing factory automation, is driving higher demand for both battery replacements and new battery packs across the region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Top Key Players

- Bosch Ltd

- Hilti Corporation

- Hitachi Ltd

- Makita Corporation

- Panasonic Corporation

- Ryobi Limited

- Samsung SDI Co. Ltd

- Sony Group Corporation

- Stanley Black & Decker Inc.

- Techtronic Industries Company Limited

Recent Developments

In 2025, Bosch Ltd further strengthened its presence in the power tool batteries market through its advanced 18V and 12V lithium-ion battery platforms, which are widely used in both professional and DIY cordless tools. Its strong battery ecosystem continues to support reliable performance, fast charging, and cross-tool compatibility across a wide range of applications.

In the same year, Hilti Corporation enhanced its market position by expanding its 22V Nuron battery platform, which has become a key growth driver across professional construction and heavy-duty cordless tools. The platform’s focus on high performance, durability, and connected tool systems continues to support Hilti’s growth in the professional segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.1 Bn |

| Forecast Revenue (2035) | USD 7.9 Bn |

| CAGR (2026-2035) | 9.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Lithium-ion, Nickel-Cadmium, Nickel-Metal Hydride, Others), By Cell Format (Cylindrical, Prismatic, Pouch), By Voltage Class (Up to 12 V, 12 to 18 V, Above 18 V), By Application (Residential, Commercial, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bosch Ltd, Hilti Corporation, Hitachi Ltd, Makita Corporation, Panasonic Corporation, Ryobi Limited, Samsung SDI Co. Ltd, Sony Group Corporation, Stanley Black & Decker Inc., Techtronic Industries Company Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |