Market Overview

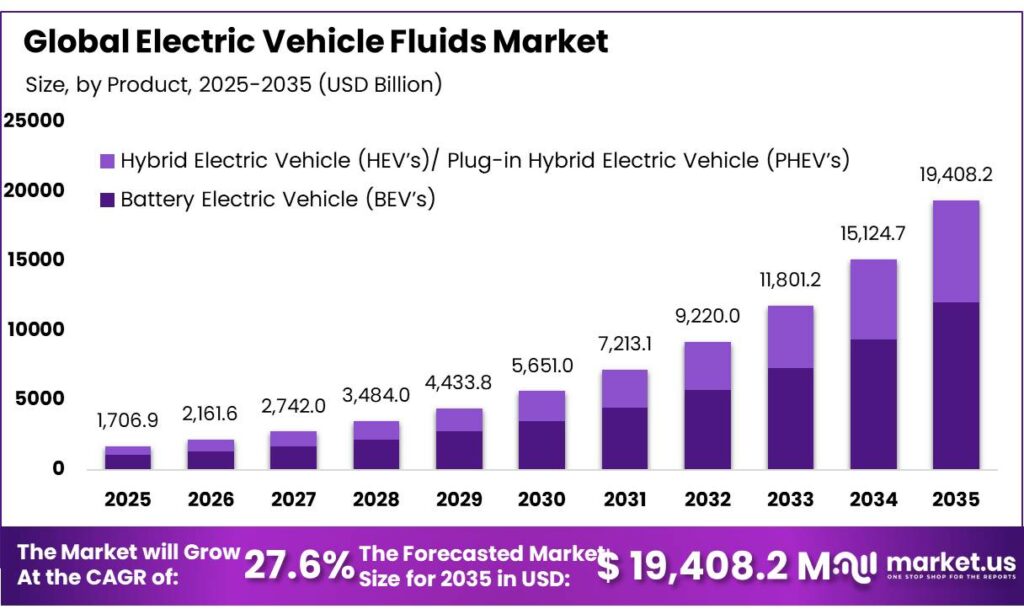

The global electric vehicle (EV) fluids market is projected to grow significantly, rising from USD 1,706.9 million in 2025 to nearly USD 19,408.2 million by 2035, registering a strong CAGR of 27.6%. Among all regions, Asia Pacific leads the market with a 51.7% share, accounting for approximately USD 882.4 million, driven by rapid EV adoption and strong manufacturing ecosystems.

EV fluids are becoming an essential part of the automotive chemicals industry. Unlike conventional vehicles that depend on engine oils, EVs require specialized e-axle lubricants, dielectric coolants, thermal fluids, greases, and transmission fluids. These advanced fluids are designed to improve heat management, protect high-speed electric motors, and ensure safety in high-voltage battery systems.

Grasp more about the additional trends impacting the future and the positive and negative consequences on the businesses, download a sample report.

Market demand is closely linked to the rapid rise in EV sales worldwide. Global electric car sales crossed 17 million units in 2024 and are expected to exceed 20 million in 2025, with EVs likely to account for more than 40% of global car sales by 2030. China remains the dominant market, contributing over 11 million annual EV sales, while the United States reached 1.56 million EV sales in 2024, representing around 10% of all new light-duty vehicle sales.

Government regulations and sustainability initiatives are strongly supporting this growth. Countries such as Canada, the UK, the US, China, India, and the European Union are introducing strict zero-emission targets, battery recycling rules, and coolant safety standards. These policies are directly increasing the demand for high-performance dielectric and thermal management fluids in EVs.

In India, policy support is especially strong through programs like FAME-II and PM e-DRIVE. With combined investments of over ₹22,000 crore, these schemes have already supported the sale of more than 36 lakh EVs and accelerated the installation of tens of thousands of public charging stations, creating long-term growth opportunities for the EV fluids market.

Key Takeaways

- Electric Vehicle Fluids Market is expected to be worth around USD 19408.2 Million by 2035, up from USD 1706.9 Million in 2025, at a CAGR of 27.6%.

- Coolant held a dominant market position, capturing more than a 41.6% share.

- Battery Electric Vehicle (BEV’s) held a dominant market position, capturing more than a 62.1% share.

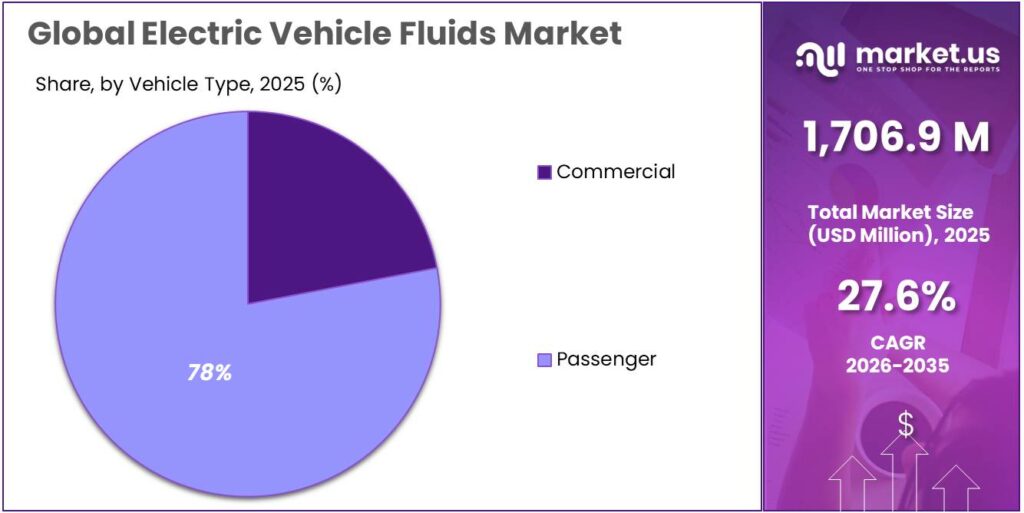

- Passenger vehicles held a dominant market position, capturing more than a 78.3% share.

- Asia Pacific is the clear leader in the Electric Vehicle Fluids Market, dominating around 51.7% of global demand, valued at roughly USD 882.4 million.

Report Scope

| Report Features | Description |

| Market Value (2025) | USD 1706.9 Mn |

| Forecast Revenue (2035) | USD 19408.2 Mn |

| CAGR (2026-2035) | 27.60% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Engine Oil, Coolant, Transmission Fluids, Greases), By Propulsion Type (Battery Electric Vehicle (BEV’s), Hybrid Electric Vehicle (HEV’s)/ Plug-in Hybrid Electric Vehicle (PHEV’s)), By Vehicle Type (Commercial, Passenger) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BP Plc, Shell Plc, FUCHS, TotalEnergies, Petroliam Nasional Berhad (PETRONAS), Saudi Arabian Oil Co., Repsol, ENEOS Corp., Gulf Oil International Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

By Product Analysis

In 2024, the coolant segment emerged as the leading product category, accounting for over 41.6% of the EV fluids market. Its strong position is mainly driven by the increasing need for effective thermal management in battery packs, electric motors, and inverters. As EVs continue to adopt high-density batteries and ultra-fast charging systems, advanced coolants have become essential for efficient heat dissipation, dielectric protection, and long-term system stability.

By Propulsion Type Analysis

The Battery Electric Vehicle (BEV) segment dominated the market with a 62.1% share in 2024, highlighting its role as the main driver of full vehicle electrification. This dominance is supported by the global transition toward zero-emission transportation, along with continuous improvements in battery range and charging infrastructure. BEVs require specialized fluids such as battery coolants, e-axle lubricants, and dielectric fluids to maintain battery efficiency, control operating temperatures, and ensure smooth power transmission.

By Vehicle Type Analysis

In 2024, passenger vehicles held the largest share of 78.3% in the EV fluids market, making them the most dominant vehicle category. This growth is fueled by the rapid adoption of electric passenger cars across both mass-market and premium segments, supported by better battery performance, declining battery costs, and a growing number of available EV models. These vehicles depend on high-performance coolants, e-motor greases, and transmission fluids to improve heat control, reduce wear, and maintain long-term efficiency.

Regional Insights

The Asia Pacific region leads the global EV fluids market, holding a dominant 51.7% share, which is valued at approximately USD 882.4 million. This leadership is largely supported by the region’s strong electric vehicle manufacturing ecosystem and the rapid pace of EV adoption across major countries.

China remains the key growth engine of the region. In 2024, the country recorded more than 9 million electric car sales, with EVs contributing over 40% of all new car sales, making it responsible for more than half of global EV sales. This massive production scale and expanding on-road EV fleet are driving substantial demand for advanced coolants, e-axle lubricants, and dielectric thermal fluids, both for factory-fill applications and aftersales servicing.

Competitive Landscape

Shell Plc is one of the key players in the EV fluids market, offering advanced solutions through its e-fluids and thermal management portfolio. Operating in more than 100 countries with over 93,000 employees, the company generated around USD 323 billion in revenue. Its EV-Plus thermal fluids are specially developed to support ultra-fast charging and high-density battery systems. With a network of 40,000+ public charging points worldwide, Shell is also able to test and commercialize advanced coolants, dielectric liquids, and e-lubricants under real-world EV operating conditions.

TotalEnergies is another major participant, providing specialized EV fluid solutions through its Quartz EV range and dedicated thermal management products. The company has operations in over 130 countries, employs more than 100,000 people, and reported USD 237 billion in revenue in 2023. Its EV fluid technologies focus on strong dielectric performance, long thermal life, and compatibility with compact electric drivetrains. Supported by over 40,000 charging points globally, TotalEnergies validates its fluid performance in demanding environments, especially in high-temperature regions such as Asia and the Middle East.

PETRONAS is strengthening its presence in the EV fluids industry through its PETRONAS Iona product range. Active in more than 50 countries, the company recorded RM 343 billion (around USD 72 billion) in revenue in 2023. Its research centers focus on developing battery-cooling fluids, e-transmission lubricants, and dielectric solutions optimized for high-efficiency EV systems. These innovations improve heat transfer efficiency and reduce power losses in high-speed electric drivetrains, making PETRONAS an important supplier for OEMs across the rapidly growing Asia Pacific EV market.

Market Size

| Company | Latest Revenue / Market Size |

| BP plc | USD 189.2 Billion |

| Shell plc | USD 284.3 Billion |

| FUCHS SE | ~EUR 3.5 Billion (latest lubricant-focused revenue estimate) |

| TotalEnergies SE | USD 195.6 Billion |

| Petroliam Nasional Berhad (PETRONAS) | USD 72 Billion (2023 reported equivalent) |

| Saudi Arabian Oil Co. (Aramco) | USD 510 Billion |

| Repsol S.A. | ~USD 70–75 Billion (recent annual revenue range) |

| ENEOS Corp. | ~USD 85–90 Billion (recent annual revenue range) |

| Gulf Oil International Ltd. | ~USD 3–4 Billion (private estimate) |

Recent Developments

In 2025, Shell introduced and demonstrated its new EV-Plus thermal fluid technology, designed to significantly improve ultra-fast charging performance. The advanced fluid enables a 34 kWh battery pack to charge from 10% to 80% in less than 10 minutes by enhancing heat transfer and maintaining battery cells within a safe temperature range during high-current charging. This innovation highlights Shell’s focus on solving one of the biggest EV challenges—faster charging without compromising battery safety or lifespan.

In July 2024, TotalEnergies partnered with SSE to launch “Source,” a 50:50 joint venture in the UK and Ireland focused on expanding high-power EV charging infrastructure. The venture plans to install up to 3,000 fast-charging points rated at 150 kW or higher, organized into nearly 300 charging hubs over the next five years. With this expansion, the company aims to capture around 20% of the fast-charging market in these regions, strengthening its role in supporting EV adoption and the associated thermal-fluid technologies.