RTX reported Q1 2026 sales of $22.1 billion, up 9% year over year, with adjusted EPS of $1.78 comfortably ahead of expectations around $1.51–$1.52. Strong free cash flow, a record $271 billion backlog, and a raised 2026 outlook drove a positive stock reaction of roughly 3% in pre‑market trading.

About RTX

RTX Corporation (NYSE: RTX) is a large US aerospace and defense company formed from the merger of Raytheon Company and United Technologies in 2020, with roots going back to early 20th‑century industrial and defense businesses. Headquartered in Arlington, Virginia, RTX develops and manufactures commercial aircraft engines, avionics, defense missiles, radars, and space systems used by airlines and governments worldwide.

The company operates through three main segments that roughly correspond to commercial engines and services, defense systems, and aerospace components, supported by a record $271 billion backlog that includes $162 billion in commercial and $109 billion in defense commitments.

RTX employs well over 150,000 people globally and continues to benefit from rising defense spending and steady commercial aerospace demand, which together support its earnings growth outlook through 2026. Public filings and market data services place RTX’s equity value firmly in the large‑cap range, with valuation metrics such as P/E and dividend yield reflecting its profile as a mature, cash‑generative defense and aerospace leader.

Top Financial Highlights

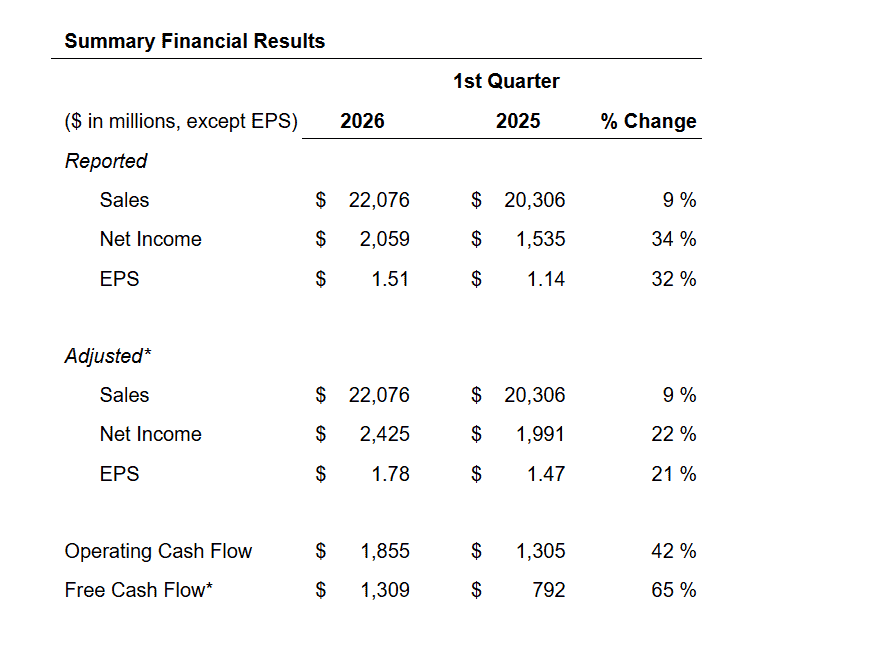

- Q1 2026 sales were $22.1 billion, up 9% year over year and 10% organically.

- Net income attributable to common shareowners was $2.1 billion, up from about $1.5 billion a year earlier.

- GAAP EPS came in at $1.51, including $0.27 of acquisition accounting adjustments.

- Adjusted EPS was $1.78, up 21% versus the prior year and well above consensus expectations.

- Operating cash flow reached $1.9 billion, with capital expenditures of about $0.5 billion, resulting in free cash flow of $1.3 billion.

- Company backlog hit a record $271 billion, split between $162 billion of commercial and $109 billion of defense work.

- Management raised 2026 adjusted sales guidance to $92.5-$93.5 billion from $92.0-$93.0 billion.

- The 2026 adjusted EPS outlook was lifted to $6.70-$6.90 from $6.60-$6.80, with free cash flow guidance reaffirmed at $8.25-$8.75 billion.

- Segment results showed Raytheon‑branded defense sales around $6.9 billion, up roughly 10% on strong land and air defense demand.

- Across all three segments, adjusted segment operating profit increased, supported by execution, productivity gains, and a favorable mix.

- Organic revenue growth of about 10% highlighted broad-based strength in commercial original equipment, commercial aftermarket, and defense programs.

- Free cash flow improved significantly year on year, with one source indicating a jump of about 65% to $1.3 billion.

- Management described Q1 as a “very strong start to 2026” and linked earnings growth directly to conversion from the growing backlog.

Beat or Miss?

| Metric | Reported | Difference/Analysis |

| Revenue | $22.1 billion | Above consensus of about $21.4–$21.5 billion, a beat of roughly 3%. |

| Adjusted EPS | $1.78 | Beat expectations around $1.51–$1.52 by about 17–18%, reflecting strong margin execution. |

| GAAP EPS | $1.51 | Includes $0.27 of acquisition accounting adjustments; still compares favorably with prior‑year GAAP EPS. |

| Free cash flow | $1.3 billion | Well ahead of last year and supports confidence in unchanged 2026 free cash flow guidance. |

What Leadership Is Saying?

“RTX delivered a very strong start to 2026 with organic sales and adjusted operating profit growth across all three segments, driven by our continued focus on execution and delivering our backlog. Our differentiated products across RTX are well positioned to support our customers’ needs and we’re making significant investments to increase output and accelerate the fielding of new capabilities. Given our first quarter performance and the strength we’re seeing in our defense business, we are increasing adjusted sales and EPS in our full year outlook.” – Chris Calio, Chairman and CEO, RTX

“Adjusted segment operating profit rose 14% to $2.9 billion… drop-through on higher volume, favorable defense mix, and improved productivity. RTX expanded consolidated segment margin by 70 basis points, more than offsetting a year-over-year tariff headwind, while headcount increased just 1% despite double-digit growth in sales and profit.” – Neil Mitchill, CFO, RTX

Historical Performance (YoY)

RTX: Q1 2026 vs. Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | $22,076M | $20,306M | 8.70% |

| Net Income (GAAP) | $2,059M | $1,535M | 34.10% |

| Adjusted Net Income | $2,425M | $1,991M | 21.80% |

| GAAP EPS (Diluted) | $1.51 | $1.14 | 32.50% |

| Adjusted EPS | $1.78 | $1.47 | 21.10% |

| Operating Cash Flow | $1,855M | $1,305M | 42.10% |

| Free Cash Flow | $1,309M | $792M | 65.30% |

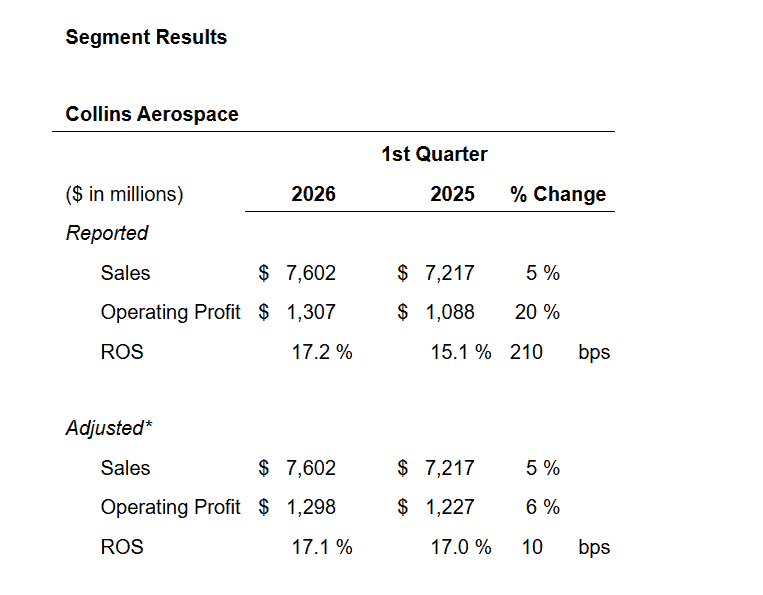

| Collins Aerospace Revenue | $7,602M | $7,217M | 5.30% |

| Pratt & Whitney Revenue | $8,173M | $7,366M | 11.00% |

| Raytheon Revenue | $6,945M | $6,340M | 9.50% |

| Total Costs & Expenses | $19,585M | $18,275M | 7.20% |

Competitor Revenue Comparison

Q1 2026 vs. Q1 2025

| Company | Q1 2026 Revenue | Q1 2025 Revenue | Change (%) |

| RTX (NYSE: RTX) | $22.08B | $20.31B | 8.70% |

| Northrop Grumman (NYSE: NOC) | $9.88B | $9.47B | 4.30% |

| Lockheed Martin (NYSE: LMT) | Q1 2026 results due Apr 23, 2026 | $17.19B (Q1 2025) | N/A |

| General Dynamics (NYSE: GD) | Q1 2026 results due Apr 29, 2026 | ~$11.8B (Q1 2025) | N/A |

Northrop Grumman Q1 2026 Snapshot

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $9.88B | $9.47B | 4.30% |

| Net Income | $875M | $481M | 81.90% |

| Adjusted EPS | $6.14 | $6.06 | 1.30% |

Northrop Grumman also beat consensus estimates, posting Q1 2026 revenue of $9.88 billion versus analyst expectations of $9.79 billion, and adjusted EPS of $6.14 versus the $6.08 estimate. The company reaffirmed its full-year 2026 sales outlook of $43.5 to $44.0 billion, with free cash flow guidance of $3.1 to $3.5 billion. Lockheed Martin and General Dynamics were not yet reporting at the time of RTX’s announcement, scheduled for April 23 and April 29, 2026 respectively.

How the Market Reacted?

Shares of RTX initially jumped on the earnings beat, with the stock trading up approximately 2.1% to $200.00 immediately after reporting before pulling back during the regular session.

The pre-market reaction was similarly positive, with RTX rising 1.12% to $197.99 ahead of the open, reflecting investor confidence in the strong EPS beat and raised guidance. However, the stock later gave back some gains, with Barron’s noting that RTX “popped, then dropped” as traders weighed the full-year revenue guidance midpoint coming in slightly below Street consensus and concern around a reported Air Force cancellation of an RTX GPS satellite ground-control program.

Over the prior 12 months, RTX shares had delivered a return of approximately 51% to 58%, and analysts maintain a consensus “Buy” rating with a 12-month price target of $205.00.