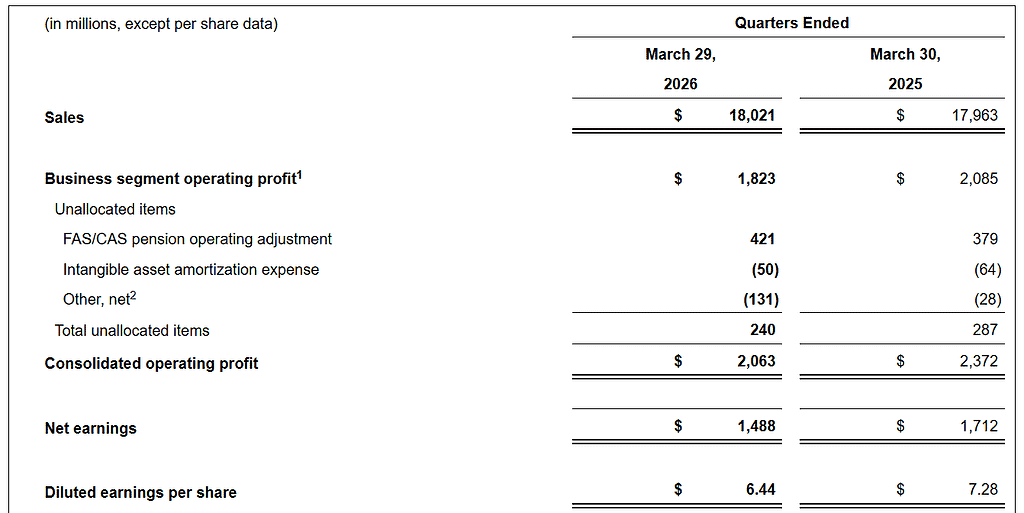

Lockheed Martin (NYSE: LMT) reported Q1 2026 diluted EPS of $6.44, missing the consensus estimate of $6.77 by $0.33, on revenue of $18.0 billion that also fell short of the $18.4 billion estimate. Net earnings declined 13% year-over-year to $1.5 billion, and free cash flow turned negative at $(291) million. Shares opened sharply lower on earnings day, falling approximately 6.3%.

About Lockheed Martin

Lockheed Martin Corporation (NYSE: LMT), headquartered in Bethesda, Maryland, is the world’s largest defense contractor by revenue. Founded in 1995 through the merger of Lockheed Corporation and Martin Marietta, the company designs, manufactures, and integrates advanced defense systems, aircraft, missiles, and space solutions for governments worldwide.

As of April 22, 2026, the company’s market capitalization stood at approximately $131.7 billion. Lockheed operates across four core segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS), and Space.

The company is also a key contractor in NASA’s Artemis program, having built the Orion spacecraft that recently completed the historic Artemis II crewed lunar mission. Lockheed employs approximately 120,000 people globally and pays an annual dividend of $13.80 per share, representing a yield of approximately 2.48%.

Top Financial Highlights

- Total revenue reached $18.021 billion, remaining broadly flat compared to $17.963 billion in Q1 2025.

- Net earnings were $1.488 billion, declining 13% from $1.712 billion in the prior year period.

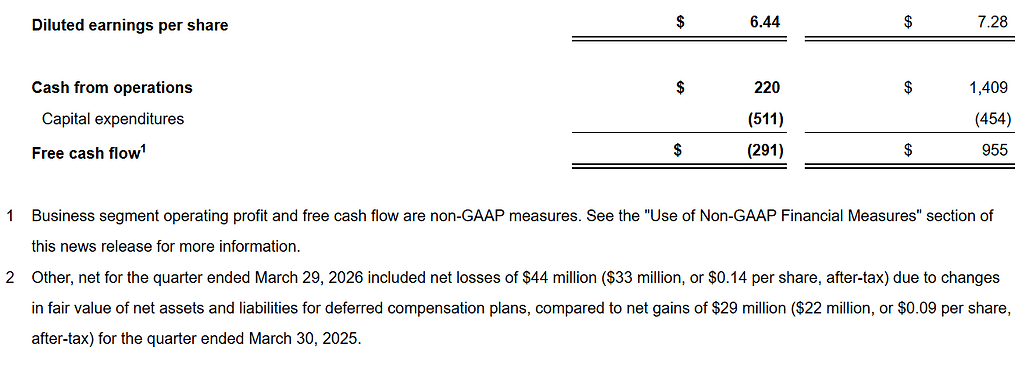

- Diluted EPS stood at $6.44, down 11.5% from $7.28 in Q1 2025.

- Consolidated operating profit totaled $2.063 billion, decreasing 13% from $2.372 billion a year earlier.

- Gross profit was $2.078 billion, compared to $2.323 billion in the previous year.

- Cash from operations declined to $220 million, significantly lower than $1.409 billion in Q1 2025.

- Free cash flow was negative at $291 million, compared to $955 million in the prior year period.

- Capital expenditures increased to $511 million, up from $454 million in Q1 2025.

- Dividends paid totaled $816 million, alongside $1.0 billion in long-term debt repayment.

- Cash and equivalents stood at $1.894 billion, down from $4.121 billion at the end of 2025.

- Total backlog was $186.4 billion, declining from $193.6 billion at December 31, 2025.

- Aeronautics generated $6.953 billion in revenue, while Missiles and Fire Control recorded $3.649 billion with 8% growth, and Space contributed $3.428 billion with 7% growth.

- Full-year 2026 guidance has been reaffirmed, with expected sales between $77.5 billion and $80.0 billion, diluted EPS in the range of $29.35 to $30.25, and free cash flow projected between $6.5 billion and $6.8 billion.

Beat or Miss?

| Metric | Reported | Estimated | Difference / Analysis |

| Diluted EPS | $6.44 | $6.77 | Miss by $0.33 (-4.9%); driven by lower profit booking rates, F-16 and C-130J challenges |

| Total Revenue | $18.021B | $18.426B | Miss by ~$405M (-2.2%); flat YoY growth dragged by lower Aeronautics and RMS volumes |

| Cash from Operations | $220M | N/A | Far below Q1 2025’s $1.409B; attributed to billing timing and working capital increase |

| Free Cash Flow | $(291)M | N/A | Negative vs. $955M in Q1 2025; significant swing due to contract asset build-up |

| Full-Year EPS Guidance | $29.35-$30.25 | ~$29.94 | Midpoint slightly below consensus; management expressed confidence in H2 recovery |

| Full-Year Revenue Guidance | $77.5B-$80.0B | ~$79.1B | Midpoint of $78.75B in line with but slightly below street consensus |

What Leadership Is Saying?

CEO Jim Taiclet on Strategy and Vision

“Lockheed Martin’s superior capabilities in delivering advanced defense technology and systems and in space exploration have been proven again and again in 2026. Our Orion spacecraft safely carried the crew farther from Earth than ever before during NASA’s historic Artemis II mission… Our superior fifth generation fighter jets, the F-35 and F-22, continue to operate with great effectiveness in contested and difficult missions. Additionally, our layered missile defense architecture, including phased array radars, Aegis integrated command and control system, and the THAAD and advanced Patriot Missile interceptors, protected both military assets and civilians.”

“We anticipate that these groundbreaking [framework] agreements will benefit both industry and the government and serve as the example for future contracting initiatives. The multi-year demand commitments defined in these framework agreements will in turn support strategic investments in production infrastructure, bolster our supply chain, and enhance our workforce to increase production rates of these critical systems by 3-4 times current rates.”

CFO on Financials and Guidance

“Our first quarter revenue of more than $18 billion, segment operating profit of $1.8 billion, and substantial backlog were a result of both strong customer demand, our continued commitment to operational performance and focused risk management. We reaffirm our 2026 full year guidance with anticipated sales and operating profit growth of approximately 5% and 25% year-over-year, respectively, and expected free cash flow between $6.5 and $6.8 billion.”

Historical Performance

LMT Q1 2026 vs. Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | $18.021B | $17.963B | 0.30% |

| Net Earnings | $1.488B | $1.712B | -13.10% |

| Diluted EPS | $6.44 | $7.28 | -11.50% |

| Consolidated Operating Profit | $2.063B | $2.372B | -13.00% |

| Cash from Operations | $220M | $1.409B | -84.40% |

| Free Cash Flow | $(291)M | $955M | NM |

| Aeronautics Revenue | $6.953B | $7.057B | -1.50% |

| MFC Revenue | $3.649B | $3.373B | 8.20% |

| RMS Revenue | $3.991B | $4.328B | -7.80% |

| Space Revenue | $3.428B | $3.205B | 7.00% |

| Business Segment Operating Margin | 10.10% | 11.60% | -150 bps |

| Total Backlog | $186.4B | N/A | N/A |

Key drivers of change: Aeronautics profit fell 14% due to a $125 million unfavorable F-16 adjustment and $55 million in C-130J challenges. RMS declined 19% on lower radar program volume and helicopter headwinds. Space operating profit dropped 26% due to the absence of favorable one-time completions that boosted Q1 2025. MFC was the bright spot, growing both revenue (+8%) and operating profit (+8%) on strong PAC-3, JASSM, and PrSM demand

Competitor Comparison

Q1 2026 vs. Q1 2025

| Company | Q1 2026 Revenue | Q1 2025 Revenue | Change (%) | Q1 2026 Net Income | Q1 2025 Net Income | Net Income Change (%) |

| Lockheed Martin (LMT) | $18.021B | $17.963B | 0.30% | $1.488B | $1.712B | -13.10% |

| RTX Corp (RTX) | $22.076B | $20.306B | 8.70% | $2.059B | $1.535B | 34.10% |

| Northrop Grumman (NOC) | $9.881B | $9.468B | 4.40% | $875M | $481M | 81.90% |

Among the three major defense contractors reporting Q1 2026, RTX and Northrop Grumman outperformed Lockheed Martin on both revenue growth and profitability improvement. RTX raised its full-year guidance after delivering 9% revenue growth and 21% adjusted EPS growth, while Northrop’s net income surged 82% as it recovered from the B-21 program losses that depressed Q1 2025 results.

Lockheed’s flat revenue and declining profits reflect execution challenges in its Aeronautics and RMS segments rather than any structural demand weakness, as its reaffirmed outlook and $186 billion backlog suggest.

How the Market Reacted?

Lockheed Martin shares opened at $556.01 on April 23, 2026, a sharp decline from the prior close, as the market reacted negatively to the EPS and revenue misses. The stock fell approximately 6.3% on the day of the earnings announcement, with Yahoo Finance reporting that shares dropped following the company’s failure to meet Wall Street targets on both earnings and revenue.

This reaction was notably steeper than the company’s historical average post-earnings move of approximately -2.12% over the previous five earnings releases. The bearish market sentiment was amplified by the significant free cash flow deterioration, which swung from $955 million positive in Q1 2025 to negative $291 million, even as management attributed the swing primarily to billing timing and reiterated confidence in the full-year free cash flow target of $6.5-$6.8 billion.