Market Overview

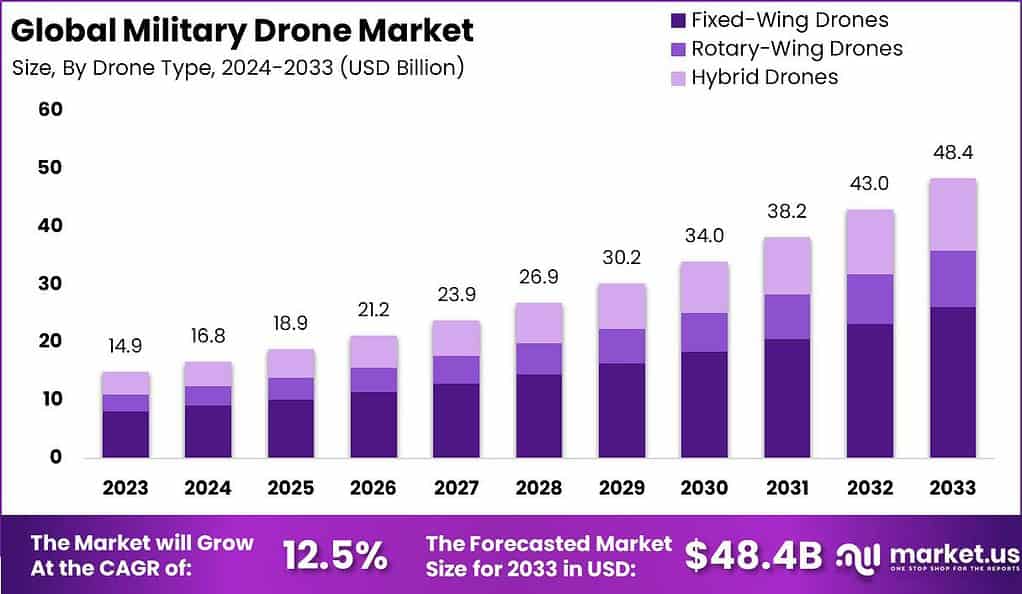

The global military drone market reached USD 14.9 billion in 2023 and is projected to attain USD 48.4 billion by 2033, expanding at a robust CAGR of 12.5% from 2024–2033. This strong trajectory reflects sustained defense spending, rising demand for unmanned systems, and continuous modernization of battlefield capabilities worldwide.

Military drones, or unmanned aerial vehicles, are remotely operated or autonomous aircraft used by armed forces for surveillance, reconnaissance, target acquisition, and precision strike missions. Defense organizations deploy these platforms to gather real-time intelligence, monitor borders, support combat operations, and reduce risk to pilots in hostile or contested environments.

Defense ministries across the globe increasingly use military drones in intelligence, surveillance, and reconnaissance missions, logistics support, and combat operations. Armed forces rely on these systems for border monitoring, battlefield awareness, and supply delivery in dangerous zones, which improves mission effectiveness and enables faster, data-driven decisions during complex operations.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Advanced technologies such as artificial intelligence, improved sensors, and secure communication links significantly enhance military drone performance and autonomy. These innovations enable better navigation, longer endurance, and more precise targeting, while AI-driven analytics support faster interpretation of collected data and more effective mission planning in dynamic combat environments.

Defense policies, rising budgets, and supportive regulations for unmanned aerial systems encourage wider deployment of military drones. Clear frameworks for airspace integration, testing corridors, and procurement programs help armed forces adopt new unmanned platforms more quickly, while export rules and alliances shape international acquisition and collaborative development.

Key Takeaways

- The global military drone market will reach about USD 48.4 billion by 2033, up from roughly USD 14.9 billion in 2023, at a CAGR of around 12.5% from 2024–2033.

- The fixed-wing drone type dominated in 2023, accounting for more than 54.1% share, driven by long endurance, high payload capacity, and suitability for extended surveillance missions.

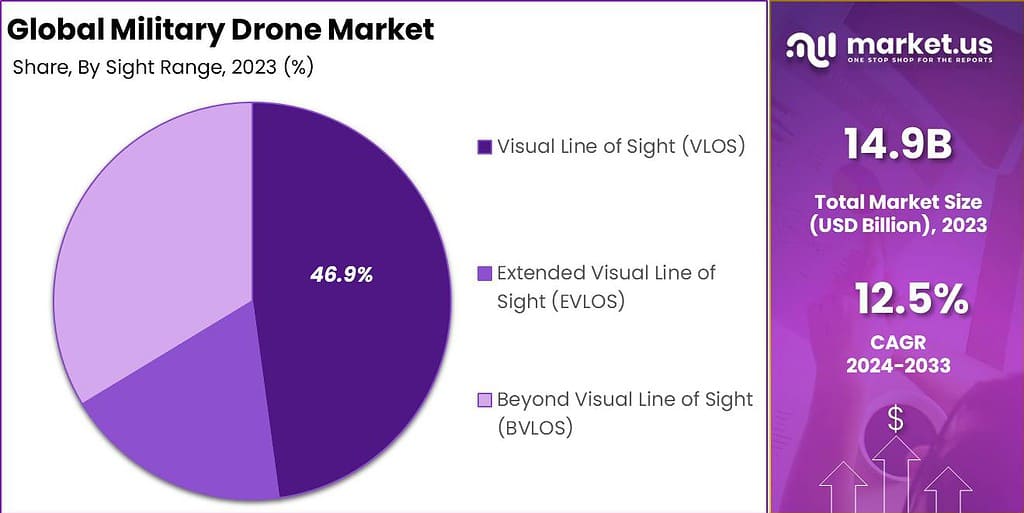

- The visual line of sight segment led the sight range category with over 46.9% share in 2023, supported by regulatory clarity and strong adoption in close-range tactical operations.

- Remote-piloted drones held more than 69.5% share in 2023, reflecting defense preferences for strong human control and immediate decision-making in sensitive missions.

- The intelligence, surveillance, and reconnaissance segment captured above 60.8% share in 2023, underscoring the critical role of real-time situational awareness in modern defense strategies.

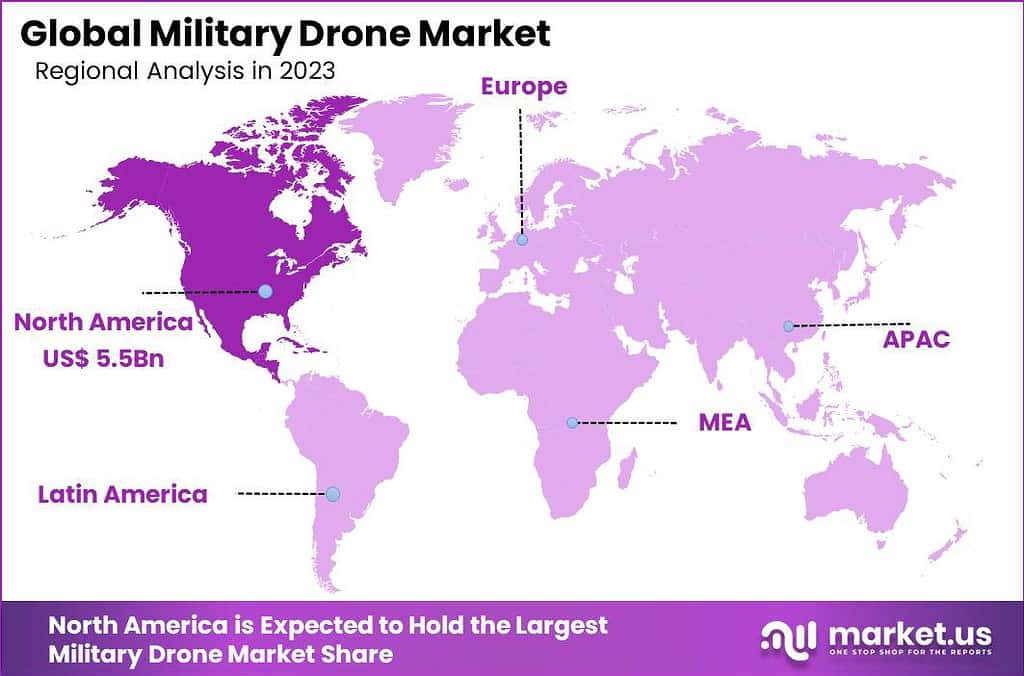

- North America led the global market with over 37.2% share and approximately USD 5.5 billion revenue in 2023, supported by high U.S. defense spending and advanced industry players.

Market Segmentation Overview

The fixed-wing drone category contributed more than 54.1% of global revenue in 2023, reflecting strong suitability for long-range surveillance and intelligence missions. Defense agencies favor these platforms for high endurance, greater payload capacity, and ability to carry sophisticated sensors and communication systems over extended distances.

Moreover, rotary-wing and hybrid drones address vertical takeoff, maneuverability, and flexible mission profiles in confined or urban environments. These designs serve tactical units that require hover capabilities, rapid repositioning, and close support, complementing fixed-wing fleets in diverse combat and support operations.

Within sight range, visual line of sight operations represented more than 46.9% share in 2023, supported by straightforward control requirements and established safety regulations. Commanders rely on these missions for close-in surveillance and rapid-response tasks where direct operator oversight remains vital for mission assurance.

Additionally, extended visual line of sight and beyond visual line of sight segments continue to expand as militaries deploy drones for deep reconnaissance and wide-area monitoring. These modes enable coverage of broader theaters and border regions, leveraging advanced communication links and autonomy to operate far from ground controllers.

By application, intelligence, surveillance, and reconnaissance dominated with more than 60.8% share in 2023, highlighting the central importance of continuous battlefield awareness. Forces deploy ISR drones to track enemy movement, protect troops, and support precision targeting, which strengthens operational planning and reduces mission risk.

Furthermore, logistics, supply, and combat operations segments provide additional momentum as militaries test drone-based resupply, precision strike, and multi-role mission concepts. These uses broaden the value of unmanned systems, integrating them into everyday military workflows beyond traditional observation roles.

On the basis of operation, remote-piloted drones accounted for more than 69.5% share in 2023, because commanders prioritize direct human control in critical engagements. This structure supports precise maneuvering, real-time decisions, and adherence to complex rules of engagement during sensitive missions.

Consequently, semi-autonomous and fully autonomous platforms are gradually gaining share as AI improves navigation, targeting support, and mission management. These systems can lighten operator workload, extend operational reach, and enable swarming tactics, though ethical and regulatory considerations still shape deployment pace.

Drivers

Increasing government funding and modernization programs strongly drive demand for military drones across major defense powers. Governments allocate larger budgets to unmanned systems to enhance intelligence collection, reduce pilot risk, and strengthen rapid-response capabilities, which accelerates procurement and long-term fleet expansion.

Additionally, rapid technological advancement, especially in artificial intelligence and advanced sensors, boosts drone functionality and mission effectiveness. These innovations support autonomous navigation, improved targeting, and more efficient data processing, encouraging defense agencies to upgrade legacy systems and adopt next-generation unmanned platforms.

Use Cases

Modern militaries deploy drones extensively for intelligence, surveillance, and reconnaissance, using them to monitor borders, track hostile movements, and safeguard critical assets. These missions deliver continuous real-time imagery and signals data, which improves situational awareness and helps commanders coordinate ground, air, and naval operations more effectively.

Moreover, armed forces increasingly test drones for logistics and combat roles, including resupply of remote units and precision strike missions. These applications reduce exposure of personnel to hostile fire, support sustained operations in contested areas, and enable faster, targeted responses during high-intensity engagements.

Major Challenges

Regulatory and ethical concerns present a significant challenge for military drone deployment, particularly for semi-autonomous and autonomous systems. Policymakers must address accountability, airspace integration, and rules of engagement, and these debates can slow adoption, restrict experimentation, and shape how aggressively forces field advanced platforms.

However, technological complexity and dependence on advanced components also create vulnerabilities, including cyber risks and potential system failures. Defense organizations must invest continuously in cybersecurity, redundancy, and maintenance to ensure drone fleets remain reliable and secure during critical missions in contested environments.

Business Opportunities

Expansion into new defense applications, such as border surveillance, disaster response, and humanitarian support, offers attractive opportunities for drone manufacturers. These missions leverage unmanned platforms in harsh or dangerous conditions, opening additional revenue streams and encouraging tailored solutions for governments facing diverse security challenges.

Additionally, rising security needs in developing regions, particularly in Asia Pacific and parts of the Middle East, create strong prospects for new contracts. Vendors that offer cost-effective, modular, and easily integrated drone systems can build long-term partnerships with emerging defense customers modernizing their forces.

Regional Analysis

North America dominated the military drone landscape in 2023, capturing more than 37.2% share and around USD 5.5 billion in revenue. Strong U.S. defense spending, advanced industrial capabilities, and robust research programs underpin leadership in ISR, combat drones, and related support systems.

Furthermore, Asia Pacific is emerging as a dynamic growth region as countries such as China, India, Japan, and South Korea expand defense budgets and unmanned capabilities. Regional tensions, border security priorities, and modernization agendas drive investment in surveillance and combat drones, supporting sustained market expansion.

Recent Developments

- May 2024 — AeroVironment was selected by DARPA under the ANCILLARY program to develop advanced VTOL drone technologies, aiming to improve launch and recovery performance for challenging missions.

- February 2024 — The U.S. Air Force chose General Atomics’ Gambit drone for the next phase of the CCA program, targeting collaborative combat roles including air-to-air engagements.

- December 2023 — General Atomics began flight tests for DARPA’s LongShot program, developing a drone that can launch missiles from crewed aircraft to extend engagement ranges and reduce pilot risk.

Conclusion

The military drone market is set for strong expansion through 2033, supported by rising defense budgets, modernization priorities, and growing reliance on unmanned capabilities. Governments pursue enhanced situational awareness, reduced personnel risk, and greater mission flexibility, which will keep demand for advanced drones on a firmly upward trajectory.

Key segments such as fixed-wing platforms, ISR applications, and remote-piloted operations currently dominate global revenue, reflecting operational preferences for endurance, intelligence gathering, and tight human oversight. North America holds a leading position, while Asia Pacific and other regions increasingly accelerate procurement to strengthen their defense postures.

Companies that innovate in AI-enabled autonomy, secure communications, and multi-mission payloads will be best positioned to capture emerging contracts and long-term partnerships. Vendors aligning portfolios with evolving defense doctrines and collaborative combat concepts can share in a market expected to reach about USD 48.4 billion by 2033.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at [email protected]

To tailor future releases more closely to your needs, do you want upcoming versions to lean more on technical defense language or stay focused on plain business framing for a broader audience?