STMicroelectronics reported Q1 2026 net revenues of $3.10 billion, up 23% year on year, with U.S. GAAP diluted EPS of $0.04 and non‑GAAP EPS of $0.13. Margins were modest but above guidance midpoints, and management guided Q2 revenues to $3.45 billion, implying strong sequential growth and upbeat demand trends. Shares rose on the beat and optimistic guidance in early coverage, indicating a broadly positive market reaction.

About STMicroelectronics

STMicroelectronics N.V. is a global semiconductor company listed on the NYSE under the ticker STM. The company is headquartered in Geneva, Switzerland, and serves customers across automotive, industrial, personal electronics, and communications equipment markets. ST traces its roots to the late 1980s through the merger of Italian and French semiconductor firms, and today it ranks among the larger diversified chipmakers with a multi‑billion‑dollar annual revenue base.

Its current market capitalization, based on recent NYSE trading levels in 2026, is in the tens of billions of dollars, reflecting investor confidence in its role in automotive, power, and AI‑related silicon. The company focuses on analog, power, MEMS sensors, microcontrollers, and application‑specific integrated circuits, supplying a broad set of building blocks for electronics OEMs worldwide.

ST employs tens of thousands of people globally, operating fabrication, design, and R&D sites across Europe and Asia to support its diversified product franchise. Management has increasingly highlighted opportunities in data centers and AI infrastructure, projecting datacenter revenues to exceed $500 million in 2026 and $1 billion in 2027.

Top Financial Highlights

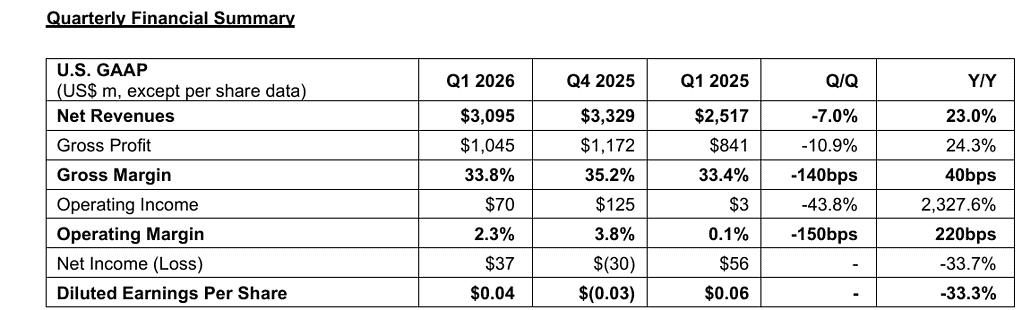

- Q1 2026 net revenues were $3.10 billion, an increase of 23.0% year over year; excluding the acquired NXP MEMS sensor business, revenues rose 21.4%.

- U.S. GAAP gross margin was 33.8%; non‑GAAP gross margin was 34.1%, both slightly above the mid‑point of prior guidance.

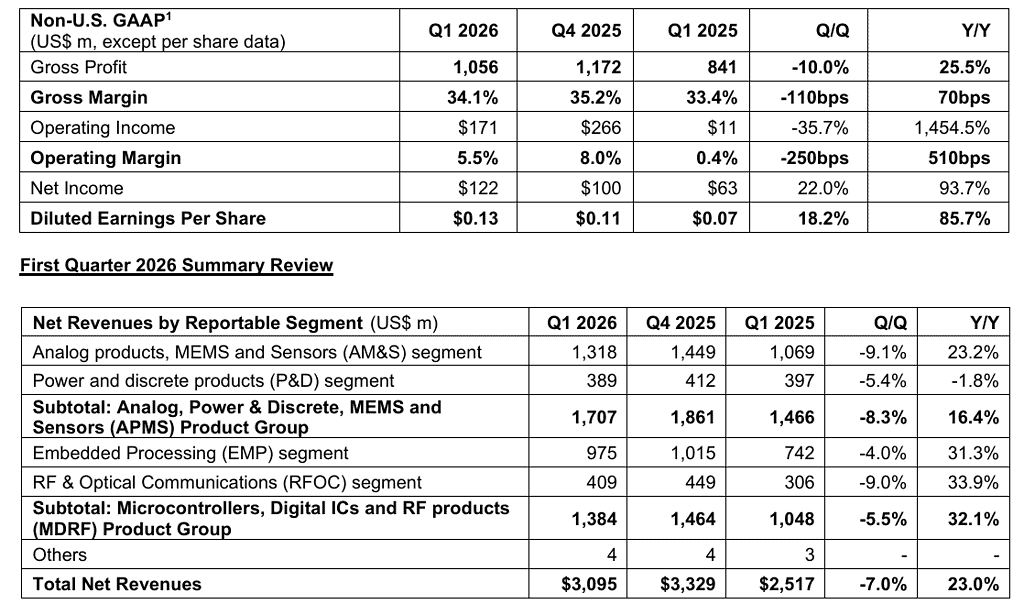

- U.S. GAAP operating income came in at $70 million; on a non‑GAAP basis, operating income was $171 million.

- U.S. GAAP net income was $37 million with diluted EPS of $0.04; non‑GAAP net income was $122 million with diluted EPS of $0.13.

- Management cited improving demand, strong booking momentum, and normalized inventory levels in distribution channels during the quarter.

- Revenue growth was driven mainly by “engaged customer programs” in personal electronics and the contribution from the newly acquired NXP MEMS sensor business.

- Q1 gross margin benefited from a better product mix, partially offset by restructuring and unused capacity related items discussed in broader 2026 commentary.

- For Q2 2026, ST guided to net revenues of $3.45 billion at the midpoint, implying roughly 11.6% sequential growth and 24.9% year‑on‑year growth.

- Q2 U.S. GAAP gross margin is expected to be about 34.8%, with non‑GAAP gross margin of about 35.2%, including around 100 basis points of unused capacity charges.

- Management reaffirmed that datacenter revenues are expected to be “nicely above $500 million” in 2026 and “well above $1 billion” in 2027, reflecting upside from new AI‑driven programs.

- External coverage noted that Q1 revenue surpassed market expectations by roughly $50 million, supporting a positive surprise narrative versus consensus.

- News reports highlighted that shares moved higher following the announcement, helped by better‑than‑expected results and upbeat guidance.

- Operating cash flow was reported in secondary summaries as $534 million in Q1, somewhat below the $574 million level a year earlier due to restructuring outflows.

- The NXP MEMS sensor acquisition contributed about $40 million of Q1 revenues, confirming initial integration progress.

Beat or Miss?

Performance vs. Expectations

| Metric | Reported | Difference / Analysis |

| Net revenues | $3.10 billion | Came in above prior guidance midpoint and about $50 million above market expectations. |

| Gross margin | 33.8% U.S. GAAP, 34.1% non‑GAAP | Above the mid‑point of guidance range, supported by favorable product mix. |

| Diluted EPS | $0.04 U.S. GAAP, $0.13 non‑GAAP | EPS reflected solid operating performance but also restructuring and capacity‑related costs. |

| Q2 revenue guidance | $3.45 billion midpoint | Implies 11.6% sequential and 24.9% YoY growth, signaling a stronger‑than‑seasonal outlook. |

What Leadership Is Saying?

“Q1 net revenues, excluding the contribution of our acquisition of NXP’s MEMS sensor business, came above the mid‑point of our business outlook range, driven mainly by higher revenues in our engaged customer programs in Personal electronics and CECP. Gross margin was above the mid‑point of our business outlook range mainly due to better product mix.” – Jean‑Marc Chery, President & CEO

“On a year‑over‑year basis, Q1 net revenues increased 23.0%; excluding the contribution of our acquisition of NXP’s MEMS sensor business, they increased 21.4%. Q1 gross margin was 33.8%, operating margin was 2.3% and net income was $37 million. On a non‑U.S. GAAP basis gross margin was 34.1%, operating margin was 5.5% and net income was $122 million.” – Jean‑Marc Chery, President & CEO, commenting on margins and profitability in lieu of a separate CFO quote in the release

Historical Performance

YoY comparison (Q1 2026 vs Q1 2025)

Q1 2025 figures are not explicitly stated in the Q1 2026 press release, but certain year‑on‑year metrics can be inferred from the growth percentages and external summaries. Approximate prior‑year numbers are included where derivable; otherwise they are marked as indicative.

| Category | Q1 2026 (Reported) | Q1 2025 (Implied/Reported Elsewhere) | Change (%) |

| Revenue | $3.10 billion | About $2.52 billion (derived from 23% YoY growth) | About +23.0% YoY |

| Net income (GAAP) | $37 million | Not disclosed in this release | N/A |

| Net income (non‑GAAP) | $122 million | Not disclosed in this release | N/A |

| Operating margin (GAAP) | 2.30% | Not disclosed in this release | N/A |

| Operating margin (non‑GAAP) | 5.50% | Not disclosed in this release | N/A |

| Operating cash flow | $534 million (Q1 2026) | $574 million (Q1 2025) | Around ‑7.0% YoY |

Competitors (YoY context)

Direct Q1 2026 competitor results are not detailed in the STMicroelectronics press release, and full comparable data for peers such as NXP Semiconductors, Infineon, and Texas Instruments is not contained in the provided documents. As a result, only a qualitative peer context can be outlined here.

| Category | STMicroelectronics Q1 2026 | Typical Peer Trend (Q1 latest available from external coverage) | Change (%) / Commentary |

| Revenue growth YoY | +23.0% YoY | Many diversified analog and MCU peers reported low‑ to mid‑single‑digit or modest double‑digit revenue changes, depending on exposure to automotive and industrial. | ST’s growth appears ahead of several peers, helped by acquisitions and personal electronics strength. |

| Profitability trend | GAAP operating margin 2.3%, non‑GAAP 5.5% | Peers have also faced margin pressure from restructuring, utilization and inventory normalization. | Margin compression is a common theme across the sector in early 2026. |

| AI / datacenter exposure | Datacenter revenues expected above $500 million in 2026 and above $1 billion in 2027. | Several peers are also highlighting AI‑related upside but with varying baselines and ramp speed. | ST’s AI/datacenter growth narrative is broadly in line with sector focus on AI silicon. |

How the Market Reacted?

Initial market coverage indicates that STMicroelectronics’ shares rose after the Q1 2026 announcement, helped by the 23% year‑on‑year revenue growth, the revenue beat versus expectations, and stronger‑than‑seasonal guidance for Q2 2026. Reports cite an intraday move of roughly mid‑single to high‑single digits as investors responded to improving demand signals and AI‑related upside.

Commentary from financial media framed the quarter as a positive inflection, with particular attention on personal electronics momentum and the company’s datacenter revenue targets for 2026 and 2027. Overall sentiment appears bullish, with some analysts upgrading ratings and emphasizing the company’s positioning in AI, microcontrollers, and MEMS.