Samsung Biologics posted its strongest-ever opening quarter with revenue of KRW 1,257 billion (~$850M) and net income of KRW 469.2 billion, up 41.6% YoY. No per-share EPS figure was disclosed in the press release. Shares closed at KRW 1,567,000 on the earnings date, down 1.32% on the day amid a looming labor strike threat, but the stock is up ~52.8% year-to-date.

About Samsung Biologics

Samsung Biologics (KRX: 207940.KS) is the world’s largest biopharmaceutical contract development and manufacturing organization (CDMO), headquartered in Incheon, South Korea. Founded in 2011 as part of the Samsung Group, the company offers end-to-end integrated services ranging from late discovery through commercial manufacturing, across modalities including monoclonal antibodies, antibody-drug conjugates (ADCs), fusion proteins, and mRNA therapeutics.

As of April 2026, Samsung Biologics carries a market capitalization of approximately $47.72 billion USD (approximately KRW 70.73 trillion), making it one of the most valuable life sciences companies in Asia. With a combined biomanufacturing capacity of 845,000 liters across its Korean Bio Campus I and II and the newly acquired Rockville, Maryland facility, the company holds the largest installed biologics manufacturing capacity globally. Cumulative regulatory approvals have surpassed 440, reflecting its quality and compliance track record.

Top Financial Highlights

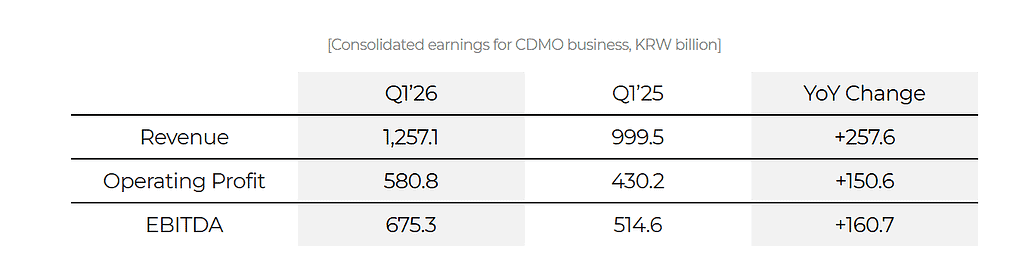

- Revenue reached KRW 1,257.1 billion (~$850M), up 25.8% YoY from KRW 999.5 billion in Q1 2025

- Operating profit climbed to KRW 580.8 billion, a 35.0% YoY increase from KRW 430.2 billion

- Net income surged to KRW 469.2 billion (~$317.7M), up 41.6% YoY from KRW 331.3 billion

- EBITDA reached KRW 675.3 billion, up from KRW 514.6 billion in Q1 2025 (+31.2% YoY)

- Operating margin expanded to 46.2% from 43.0% a year earlier, reflecting scale advantages from full plant utilization

- Net margin for the quarter came in at approximately 37.3%, showing significant profitability leverage

- Full utilization maintained across Plants 1 through 4 at Bio Campus I drove the top-line growth

- Cumulative contract value exceeded USD 21.4 billion, reflecting sustained global client demand

- First commercial-scale engineering run completed at the dedicated antibody-drug conjugate (ADC) facility

- 2026 annual revenue growth guidance maintained at 15% to 20%, excluding contributions from the newly acquired Rockville, U.S. facility

- Acquisition of Rockville, Maryland manufacturing facility completed for USD 353 million in March 2026, adding 60,000 liters of capacity

- Strategic partnerships announced with CEPI (epidemic preparedness) and Eli Lilly and Company for open innovation

Beat or Miss?

| Metric | Reported | Analyst Estimate | Difference / Analysis |

| Revenue | KRW 1,257.1B | KRW 1,281.3B | -1.9% miss vs. Kiwoom Securities estimate; operating profit aligned with market consensus per Yonhap Infom survey |

| Operating Profit | KRW 580.8B | KRW 581.3B | Essentially in line (-0.1%); described as meeting the average analyst projection |

| Net Income | KRW 469.2B | N/A | Beat implied expectations; consensus net profit estimates were not publicly disclosed |

| EBITDA | KRW 675.3B | N/A | N/A |

| Revenue Growth (YoY) | 25.80% | ~+28% (Kiwoom) | Slightly below the upper-end estimate; volumes deferred from Q4 2025 boosted the quarter’s share |

| Operating Margin | 46.20% | ~44.2% (Hana Securities) | Beat on margin; Hana had penciled in 44.2% OPM for the quarter |

What Leadership Is Saying?

“In the first quarter, Samsung Biologics delivered stable growth, supported by consistent execution across our manufacturing network and continued demand from clients. With full operations in plants at our Bio Campus I and Plant 5 ramp-up underway, we are further strengthening manufacturing readiness and service capacity to support evolving client needs. As our global footprint continues to expand, we remain focused on quality excellence, operational consistency, and strategic investment to support sustainable long-term growth.” – John Rim, President and CEO, Samsung Biologics

Samsung Biologics remains on track to meet its 2026 guidance, supported by continued operations across Plants 1 through 4 and the progressive ramp-up of Plant 5. The company also continues to evaluate strategic investments to further diversify its manufacturing network and support clients seeking regional supply alignment amid an evolving global operating environment. CFO / IR Statement (from official earnings release)

Historical Performance (YoY)

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue (KRW billion) | 1,257.10 | 999.5 | +25.8% |

| Operating Profit (KRW billion) | 580.8 | 430.2 | +35.0% |

| EBITDA (KRW billion) | 675.3 | 514.6 | +31.2% |

| Net Income (KRW billion) | 469.2 | 331.3 | +41.6% |

| Operating Margin (%) | 46.20% | 43.00% | +320 bps |

Competitor Performance (YoY Comparison)

| Company | Metric | Q1 2026 / Most Recent Period | Prior Year Period | Change (%) |

| Samsung Biologics | Revenue | KRW 1,257.1B (~$850M) | KRW 999.5B (~$676M) | +25.8% |

| Samsung Biologics | Operating Profit | KRW 580.8B | KRW 430.2B | +35.0% |

| WuXi Biologics | Revenue (FY2025) | RMB 21.79B (~$3.0B) | RMB 18.68B | +16.7% |

| WuXi Biologics | Net Profit (FY2025) | RMB 5.73B | RMB 3.95B | +45.1% |

| Lonza Group | Revenue (FY2025) | CHF 6.53B (~$8.6B annual) | CHF 5.49B | +19.2% |

| Lonza Group | Core EBITDA Margin (FY2025) | 30.60% | ~28.7% | +190 bps |

How the Market Reacted?

Samsung Biologics shares closed at KRW 1,567,000 on April 22, 2026, the day of the earnings announcement, declining 1.32% from the previous session despite the record quarterly performance. The muted and slightly negative reaction reflects a classic “buy the rumor, sell the news” dynamic, as the strong Q1 print was widely anticipated by analysts and had largely been priced in ahead of the report.

Adding downward pressure was the company’s first-ever labor dispute: the union, representing roughly 75% of the workforce, held a rally outside the Songdo campus on the same day and threatened a walkout from June 1, raising concerns about potential production disruptions worth an estimated KRW 640 billion in losses.

Despite this near-term overhang, the stock remains up approximately 52.8% year-to-date as of April 24, 2026, underpinned by the company’s dominant global CDMO position, U.S. expansion milestones, and maintained 15-20% full-year revenue growth guidance.