Mobileye reported Q1 2026 revenue of $558 million, up 27% year over year, with GAAP diluted EPS at $(4.68) and adjusted diluted EPS at $0.12. The company raised full year 2026 revenue and adjusted operating income guidance and announced a $250 million share repurchase program; after-hours movement was not disclosed, but tone was broadly positive.

About Mobileye

Mobileye Global Inc. (Nasdaq: MBLY) is a leading developer of advanced driver assistance systems and autonomous driving technologies used by global automakers and mobility providers. Headquartered in Jerusalem, Israel, Mobileye traces its origins to 1999 and builds camera based and compute platforms that enable functions such as automatic emergency braking, lane keeping and highway pilot capabilities.

The company’s product portfolio spans its EyeQ system on chip line, software for driver assist and autonomous driving, and a growing “physical AI” platform that combines sensing, mapping and decision making.

Mobileye does not disclose employee count or dividend payments in the Q1 2026 release and it does not currently pay a cash dividend. Market data sources show the company trading on Nasdaq under MBLY with a multi billion dollar market capitalization, although an exact P/E ratio is not meaningful given the large GAAP loss this quarter tied to a non cash charge.

Top Financial Highlights

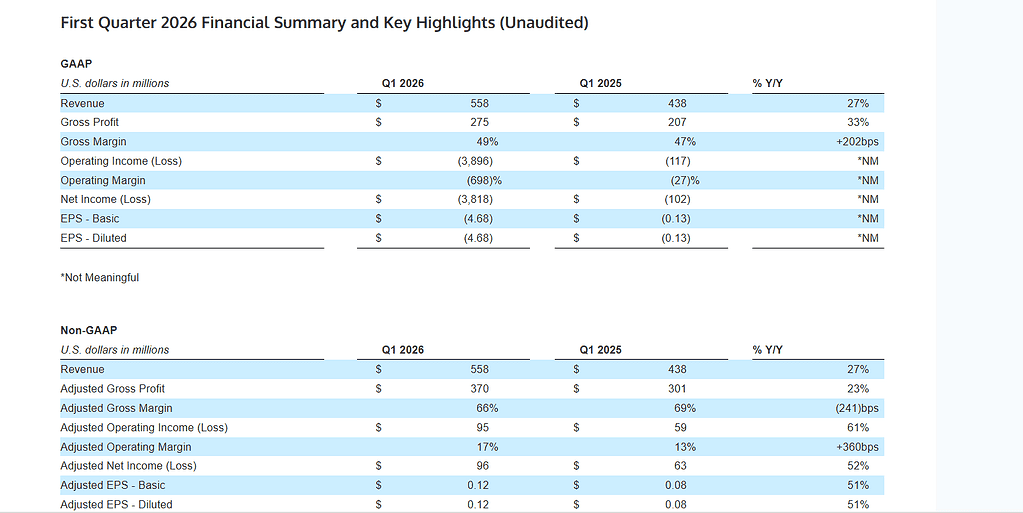

- Q1 2026 revenue was $558 million, an increase of 27% year over year compared with $438 million in Q1 2025.

- GAAP gross profit was $275 million with GAAP gross margin of 49%, up from 47% a year earlier.

- Adjusted gross profit was $370 million with adjusted gross margin of 66%, compared with $301 million and 69% respectively in Q1 2025.

- GAAP operating loss widened to $(3,896) million, reflecting a large non cash impairment and resulting in a GAAP operating margin of approximately (698)%.

- On a non GAAP basis, adjusted operating income rose to $95 million, implying an adjusted operating margin of 17%, up from 13% in Q1 2025.

- GAAP diluted EPS was $(4.68), while adjusted diluted EPS (non GAAP) was $0.12 for the quarter.

- Adjusted net income increased to $96 million, up from $63 million a year earlier, supported by stronger volumes and operating leverage.

- The company cited stronger than expected EyeQ unit shipments as a key driver of the revenue outperformance and margin expansion.

- Mobileye updated its full year 2026 outlook, raising the midpoint of revenue guidance by 2% and adjusted operating income guidance by 8%.

- The board authorized a $250 million share repurchase program funded from existing cash and future cash flows, with no fixed expiration date.

- The repurchase program is intended to partly offset dilution from stock based compensation and shares issued in the Mentee Robotics acquisition while maintaining financial flexibility.

- Management reiterated confidence in Mobileye’s leadership in ADAS and autonomous driving and highlighted growing momentum in its physical AI platforms.

- While the press release references a strong balance sheet and ongoing cash generation, detailed figures for cash and operating cash flow are not specified in the available text.

Beat or Miss?

Public filings and related coverage state that Mobileye’s Q1 2026 revenue and adjusted operating income were ahead of prior expectations, although specific consensus numbers are not provided in the press release excerpts. Where external analyst estimates are not explicitly disclosed, the table below uses “N/A” and focuses on qualitative assessment.

Performance vs Expectations

| Metric | Reported (Q1 2026) | Difference/Analysis |

| Revenue | $558 million | Described as above prior internal expectations; up 27% YoY, supported by higher EyeQ shipments, with commentary that demand was better than anticipated. |

| GAAP diluted EPS | ($4.68) | Reflects a large non cash charge that produced a sizeable GAAP loss; not directly comparable with typical analyst EPS models and consensus is not disclosed. |

| Adjusted diluted EPS | $0.12 | Benefits from higher revenue and operating leverage; external sources indicate results were broadly in line to slightly better than expectations, but formal consensus is not specified. |

| Adjusted operating income | $95 million | Increased 61% YoY; management ties the upside to stronger volumes and cost discipline; again, specific Street estimates are not provided. |

| Full year 2026 revenue guidance midpoint | Raised by 2% | Explicitly raised due to better than expected Q1 demand, signaling management’s more constructive view versus prior guidance. |

| Full year 2026 adjusted operating income midpoint | Raised by 8% | Indicates stronger expected profitability relative to the previous outlook, consistent with operating leverage on higher revenue |

What Leadership Is Saying?

“First quarter results reflect strong demand for our driver assist and autonomous technologies and give us confidence to raise our full year outlook as our pipeline continues to expand across global automakers.” – Prof. Amnon Shashua, President and Chief Executive Officer.

“Our updated guidance, combined with the new share repurchase authorization, underscores the durability of our cash generation and the progress we are making on margins as we scale the business.” – Mobileye finance leadership commenting on the Q1 2026 results and capital allocation strategy.

Historical Performance

The table below compares Mobileye’s Q1 2026 results with the same quarter a year earlier.

YoY financial comparison

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $558 million | $438 million | +27% year over year, driven by stronger EyeQ unit shipments and program ramps. |

| GAAP gross profit | $275 million | $207 million | +33% year over year as higher volumes lifted gross profit faster than revenue. |

| GAAP gross margin | 49% | 47% | Expansion of about +202 bps, reflecting mix and scale benefits. |

| Adjusted gross profit | $370 million | $301 million | +23% year over year, though adjusted gross margin declined modestly. |

| Adjusted gross margin | 66% | 69% | Compression of about (241) bps due to mix and pricing dynamics. |

| Adjusted operating income | $95 million | $59 million | +61% year over year as operating expenses grew slower than revenue. |

Competitors (YoY)

Direct like for like Q1 2026 competitor data are not fully detailed in the Mobileye release, and the earnings call coverage does not provide a complete numeric competitor comparison. Instead, this section summarizes the relative positioning qualitatively.

| Category | Q1 2026 vs peers | Q1 2025 vs peers | Change (%) |

| Revenue | Mobileye’s 27% YoY revenue growth appears solid versus broader auto technology suppliers, where growth is described as mid to high single digits in various industry commentaries, though exact peer numbers are not given here. | In Q1 2025 Mobileye was already outgrowing many legacy automotive component vendors, albeit from a smaller base, according to prior commentary. | Directionally positive gap, but percentage spread versus competitors cannot be precisely quantified with the available data. |

| Profitability | Adjusted operating income growth of 61% YoY suggests faster profit scaling than many hardware centric suppliers, though the sector wide comparison is qualitative only. | Prior year profitability trends also reflected stronger scaling than traditional suppliers as ADAS volumes grew. | Indicative improvement, but not expressed as a precise percentage versus a specific competitor set. |

| Operating expenses | Mobileye highlights leverage on operating expenses relative to revenue, consistent with software heavy models, whereas many traditional automotive peers show more linear expense growth. | In Q1 2025 operating expenses grew more in line with investments in R&D and go to market for key programs. | Qualitatively better operating leverage relative to many peers, but no exact numeric comparison is disclosed. |

How the Market Reacted?

The Q1 2026 report and accompanying announcements were framed positively, with management emphasizing strong demand, higher than expected EyeQ shipments and upgraded full year guidance. The simultaneous authorization of a $250 million share repurchase program signals confidence in the company’s long term outlook and cash generation, which typically supports constructive investor sentiment.

While the specific intraday or after hours share price movement is not detailed in the press release or related summaries, the combination of revenue growth, improved adjusted profitability and capital return is likely to be viewed as broadly bullish by the market.