Nokia posted Q1 2026 comparable EPS of €0.05 (reported EPS: €0.02), with comparable net sales of €4.50 billion (+4% in constant currency). Comparable operating profit surged 54% to €281 million, beating a ~€250 million analyst consensus. Shares rose nearly 7% in Helsinki, touching a 16-year high after the earnings beat.

About Nokia Corporation

Nokia Corporation (NYSE: NOK, Helsinki: NOKIA) is a Finnish global technology leader in connectivity infrastructure for the AI era. Founded in 1865 and headquartered in Espoo, Finland, Nokia provides fixed, mobile, and transport networking equipment, software, and services to telecom operators, enterprises, and hyperscale cloud and data-center customers worldwide.

As of April 2026, Nokia carries a market capitalization of approximately $58.74 billion on the NYSE, with its share price hitting levels unseen since 2010 following the Q1 beat. The stock trades at a trailing P/E of around 66-70x, reflecting renewed AI-driven growth expectations. Nokia has approximately 78,000 employees and pays a forward dividend authorization of up to €0.14 per share for 2025, implying a dividend yield in the mid-1% range. R&D investment in Q1 alone stood at €1.24 billion (reported), underscoring Nokia’s technology-forward positioning in optical, IP, and AI-RAN solutions.

Top Financial Highlights

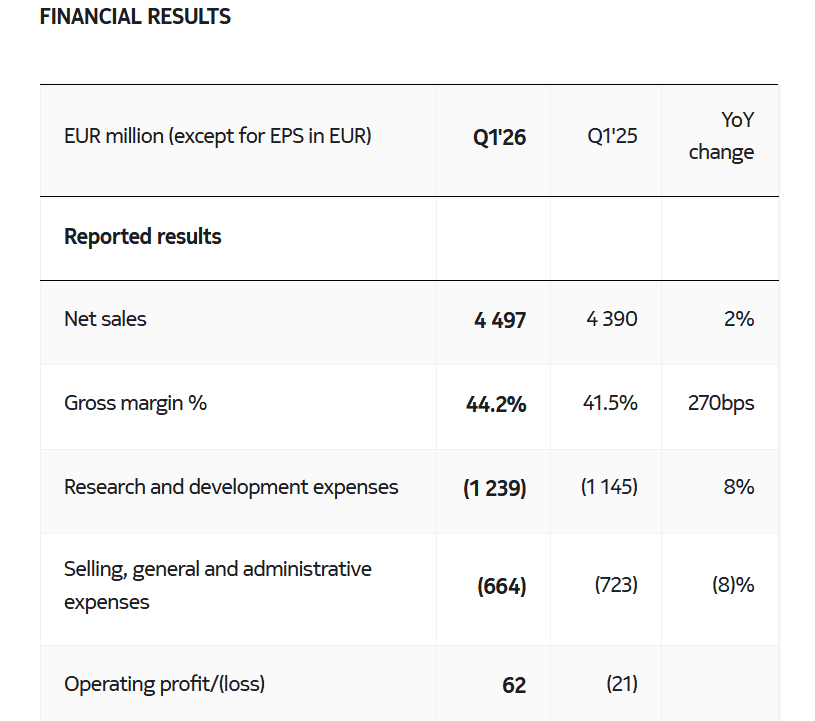

- Total net sales reached €4,497 million, increasing 2% year over year, while comparable net sales were approximately €4,500 million, reflecting 3% reported growth and 4% growth on a constant currency basis.

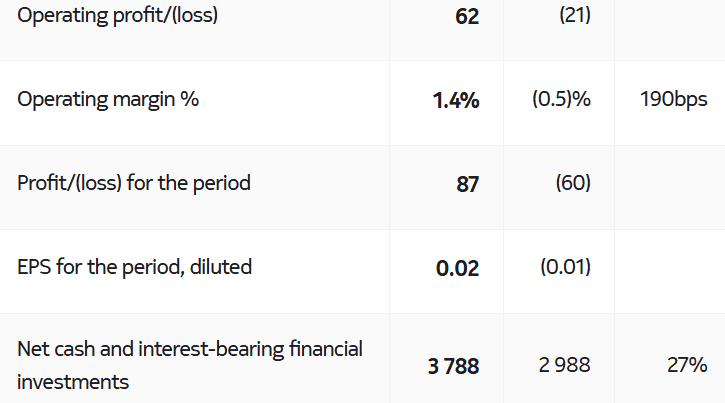

- Net income was €87 million, improving from a €60 million loss in Q1 2025, while comparable profit rose 93% to €295 million.

- Comparable diluted EPS stood at €0.05, up 67% year over year, while reported diluted EPS was €0.02 compared to -€0.01 a year earlier.

- Gross margin expanded to 44.2%, increasing by 270 basis points, with comparable gross margin reaching 45.5%, up 320 basis points.

- Comparable operating profit was €281 million, rising 54% from €183 million and exceeding analyst expectations.

- Comparable operating margin improved to 6.2%, up 200 basis points from 4.2%.

- Free cash flow totaled €0.6 billion during the quarter, reflecting solid cash generation.

- Net cash on hand reached €3.788 billion, increasing 27% from €2.988 billion in the prior year.

- Network infrastructure revenue was €1,829 million, growing 12% reported and 6% in constant currency, with optical networks rising 20% and AI and cloud net sales increasing 49%.

- Mobile infrastructure revenue was approximately €2,495 million, with 3% growth in constant currency, supported by core software growth of 5% and technology standards growth of 10%, while operating margin improved to 8.9%.

- AI and cloud orders booked reached €1.0 billion in Q1, representing 8% of total group sales.

- A dividend of €0.04 per share has been approved, with an additional authorization of €0.10 per share remaining.

- Full-year 2026 guidance remains unchanged, with comparable operating profit expected between €2.0 billion and €2.5 billion, while network infrastructure revenue growth outlook has been raised to 12% to 14%.

Beat or Miss?

| Metric | Reported | Analyst Estimate | Difference / Analysis |

| Comparable Net Sales | €4.50 billion | €4.53 billion (Infront avg.) | Slight miss on top-line by ~€30 million; in-line per Reuters |

| Comparable Operating Profit | €281 million | ~€250 million | Beat by ~€31 million; +12% upside to consensus |

| Comparable Operating Margin | 6.20% | Mid-single-digit implied | 200 bps expansion above prior guidance profile |

| Comparable Diluted EPS | €0.05 (~$0.06 per ADR) | $0.06 (Zacks consensus) | Matched analyst estimates on EPS |

| Free Cash Flow | €0.6 billion | N/A | Strong seasonal FCF; supports 55-75% FY2026 conversion target |

| Net Cash | €3.788 billion | N/A | Up 27% YoY, ahead of expectations |

What Leadership Is Saying?

CEO Justin Hotard on strategy and growth momentum:

We delivered a solid start to the year, with net sales growing 4%, gross margin expanding 320bps and operating margin expanding 200bps in the first quarter. Demand continued to be strong, particularly in AI & Cloud, where net sales grew 49% and now account for 8% of group sales. We are increasing our growth assumption for Optical and IP Networks and we are investing to capture accelerating demand from AI & Cloud customers.

CFO Marco Wiren on financial discipline and capital allocation:

Q1 was a solid start to 2026, with net sales of €4.5bn, gross margin of 45.5%, operating margin of 6.2%, free cash flow of €0.6bn and net cash of €3.8bn.

Nokia Historical Performance

YoY comparison for Nokia Group (Q1 2026 vs. Q1 2025):

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Net Sales (Reported) | €4,497 million | €4,390 million | +2% |

| Net Sales (Comparable) | €4,500 million | €4,390 million | +3% (4% constant currency) |

| Net Income (Reported) | €87 million | -€60 million | Swing from loss to profit |

| Net Income (Comparable) | €295 million | €153 million | +93% |

| Operating Expenses (R&D + SG&A, Comparable) | €1,758 million | €1,697 million | +4% |

| Gross Margin (Comparable) | 45.50% | 42.30% | +320 bps |

| Operating Margin (Comparable) | 6.20% | 4.20% | +200 bps |

Competitor Performance

YoY comparison for Ericsson (Nokia’s primary global rival), Q1 2026 vs. Q1 2025:

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Net Sales (Reported) | SEK 49.3 billion | SEK 55.0 billion | -10% reported; +6% organic |

| Net Income | SEK 0.9 billion | SEK 4.2 billion | -79% (restructuring + FX drag) |

| Adjusted EBITA | SEK 5.6 billion (11.3% margin) | SEK 6.9 billion (12.6% margin) | -20%; margin -130 bps |

| Gross Margin (Adjusted) | 48.10% | 48.50% | -40 bps |

| Free Cash Flow (before M&A) | SEK 5.9 billion | SEK 2.7 billion | +119% YoY |

Ericsson’s Q1 2026 showed organic sales growth of 6% across all segments but a 10% reported revenue decline driven by a SEK 7.8 billion negative currency impact and divestments. Net income dropped sharply due to SEK 3.8 billion in restructuring charges. By contrast, Nokia delivered positive reported revenue growth and margin expansion with no comparable one-off restructuring drag, giving Nokia cleaner earnings optics for Q1 2026.

How the Market Reacted?

Nokia shares in Helsinki surged nearly 7% in early trading on April 23, 2026, reaching their highest level since April 2010, when the company was still primarily known as a mobile phone manufacturer. On the NYSE, NOK shares rose 4.77% on earnings day to close at $10.33, after touching an intraday high of $10.86, with pre-market movement as high as +12.08% reflecting initial investor enthusiasm.

The rally was driven by Nokia beating the ~€250 million consensus on comparable operating profit, raising its Network Infrastructure net sales growth guidance to 12-14%, and boosting the AI & Cloud addressable market CAGR estimate to 27% (2025-2028) from 16%. Overall market sentiment on the report was strongly bullish, with the operating profit beat, clean balance sheet (€3.8 billion net cash), and accelerating AI data-center orders collectively validating Nokia’s pivot toward optical and IP infrastructure for the AI era.