Crown Holdings reported Q1 2026 revenue of $3.26 billion, beating analyst estimates by 7.8%, with adjusted diluted EPS of $1.86 (up 11% year-over-year), exceeding consensus of $1.75. Shares declined approximately 1.8% since the beginning of 2026 versus the S&P 500’s 4.7% gain.

About Crown Holdings, Inc.

Crown Holdings, Inc. (NYSE: CCK) is a worldwide leader in the design, manufacture, and sale of packaging products for consumer goods and industrial products, with world headquarters in Tampa, Florida.

The company operates across multiple segments including beverage cans (Americas, Europe, Asia Pacific), transit packaging, and North American tinplate businesses (food cans, aerosol cans, closures, and beverage tooling equipment).

With operations spanning over 70 manufacturing facilities globally and approximately 16,000 employees, Crown reported 2025 net sales of approximately $11.5 billion. The company maintains a market capitalization estimated at $13 billion, with a current adjusted net leverage ratio of 2.5x as of March 31, 2026.

Top Financial Highlights

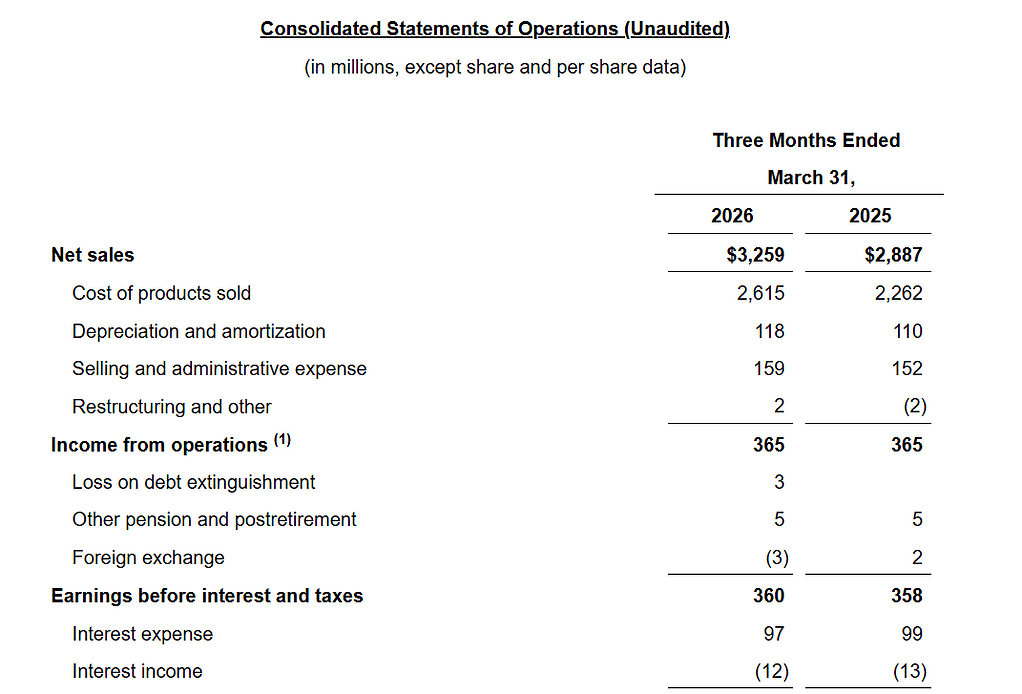

- Total revenue reached $3.26 billion, reflecting a 12.9% year over year increase from $2.89 billion.

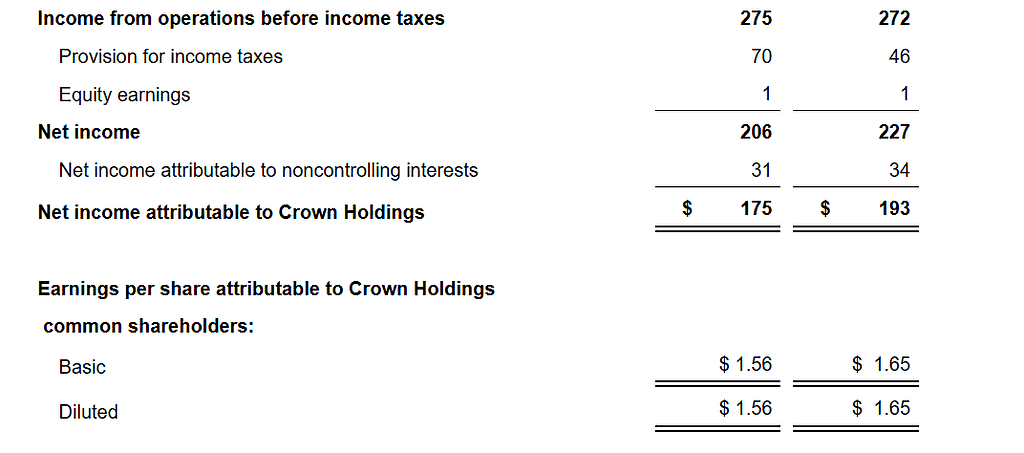

- Net income was reported at $175 million, compared to $193 million in Q1 2025.

- Adjusted net income improved to $209 million, up from $195 million in the previous year period.

- Diluted EPS stood at $1.56, compared to $1.65 in Q1 2025.

- Adjusted diluted EPS increased to $1.86, reflecting an 11% rise from $1.67.

- Segment income reached $405 million, compared to $398 million in Q1 2025.

- Adjusted EBITDA was recorded at $485 million, up from $473 million, with a 14.9% margin.

- Global beverage shipments increased by 5%, supported by strong growth in Europe and Asia Pacific regions.

- Cash and cash equivalents stood at $584 million as of March 31, 2026.

- The company returned $251 million to shareholders, including $39 million in dividends and $212 million through share repurchases.

- Net debt was reported at $5.67 billion, with an adjusted net leverage ratio of 2.7x.

- Adjusted free cash flow was negative at $129 million, compared to negative $6 million in Q1 2025.

- Full year 2026 guidance indicates adjusted diluted EPS in the range of $7.90 to $8.30, with free cash flow expected to be around $900 million.

- Q2 2026 guidance suggests adjusted diluted EPS between $2.10 and $2.20.

- Capital expenditures reached $87 million in Q1 2026, compared to $33 million in Q1 2025, with full year expectations of approximately $550 million.

Beat or Miss?

| Metric | Reported | Analyst Estimate | Difference |

| Revenue | $3.26 billion | $3.02 billion | Beat by 7.8% |

| Adjusted Diluted EPS | $1.86 | $1.75 | Beat by 6.3% (11 cents) |

| Adjusted EBITDA | $485 million | $480.3 million | Beat by 1% |

| Reported Diluted EPS | $1.56 | N/A | Down from $1.65 prior year |

What Leadership Is Saying?

“The Company got off to a solid start for the year, driven by strong results in our European and Asian beverage can businesses, beverage can equipment and our North American food can and closures businesses. Global beverage can volumes advanced 5%, led by robust shipments throughout Europe and Asia-Pacific. North American shipments advanced 1% in the quarter as a strong March, up 8% over the prior year, helped overcome a slow start to the year, the result of widespread winter storms in January.” – Timothy J. Donahue, Chairman, President & Chief Executive Officer

“With demand remaining firm across our global beverage businesses and considering our first quarter performance, the Company reaffirms its full year 2026 guidance of adjusted diluted earnings per share between $7.90 and $8.30, while recognizing the impact that volatility across aluminum, energy and transportation markets may have on input costs and consumer spending. Second quarter adjusted diluted earnings per share are expected to be in the range of $2.10 to $2.20. The Company expects to generate approximately $900 million in adjusted free cash flow in 2026 after capital spending of approximately $550 million, which includes initial spending related to the recently announced beverage can plant in India.” – Kevin C. Clothier, Senior Vice President and Chief Financial Officer

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $3,259 million | $2,887 million | +12.9% |

| Net Income | $175 million | $193 million | -9.3% |

| Adjusted Net Income | $209 million | $195 million | +7.2% |

| Segment Income | $405 million | $398 million | +1.8% |

| Operating Cash Flow | Negative $54 million | $14 million | N/A |

| Adjusted Free Cash Flow | Negative $129 million | Negative $6 million | N/A |

| Americas Beverage Revenue | $1,530 million | $1,320 million | +15.9% |

| European Beverage Revenue | $588 million | $512 million | +14.8% |

| Asia Pacific Revenue | $303 million | $279 million | +8.6% |

Competitor Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Ball Corporation (Not yet reported) | Expected May 5, 2026 | $3.10 billion revenue (Q1 2025) | Analyst forecast: +1.4% growth |

| Ardagh Metal Packaging Revenue | $1,504 million | $1,268 million | +18.6% |

| Ardagh Metal Packaging Adjusted EBITDA | $179 million | $155 million | +15.5% |

| Ardagh Group Adjusted EBITDA | $322 million | $290 million | +11.0% |

| Silgan Holdings Revenue (Not yet reported) | Expected April 29, 2026 | Forecast: $1.55 billion | Forecast: +5.5% from Q4 2025 |

How the Market Reacted?

Crown Holdings shares have declined approximately 1.8% since the beginning of 2026, underperforming the S&P 500’s 4.7% gain over the same period. The company reported strong operational performance with global beverage shipments increasing 5%, driven by robust demand in Europe and Asia-Pacific, while managing challenges from the Middle East conflict and winter storms in North America.

Crown announced plans to construct a new greenfield two-line beverage can plant in Northern India, marking its entry into one of the world’s fastest-growing beverage markets, with operations expected to commence in the second half of 2027. Despite beating revenue and adjusted earnings estimates, the company reaffirmed its full-year 2026 guidance range of $7.90 to $8.30 adjusted diluted EPS, which remains roughly in line with the consensus estimate of $8.21, contributing to muted stock performance.