Dauch Corporation (NYSE: DCH) reported Q1 2026 revenue of $2.38 billion, dramatically up 68.6% year over year, driven by the landmark Dowlais acquisition. Adjusted EPS came in at $0.34, crushing consensus estimates of -$0.04. GAAP diluted loss per share was $(0.52). In extended after-hours trading following the May 8 announcement, DCH shares rose approximately 6.7% to around $6.16, reflecting optimism about the Dowlais integration.

About Dauch Corporation

Dauch Corporation (NYSE: DCH; LSE: DCH), headquartered in Detroit, Michigan, is a premier global Driveline and Metal Forming supplier serving the automotive industry with a powertrain-agnostic product portfolio supporting electric, hybrid, and internal combustion vehicles.

Formerly known as American Axle and Manufacturing Holdings, Inc. (AAM), the company officially changed its name to Dauch Corporation in January 2026 following the completion of its transformational acquisition of Dowlais Group plc and its subsidiaries, GKN Automotive and GKN Powder Metallurgy, on February 3, 2026. The company operates across 24 countries with more than 175 locations globally.

As of May 2026, DCH carries a market capitalization of approximately $1.55 billion and a 52-week trading range of $3.94 to $9.25. Analysts rate the stock a consensus “Strong Buy” with a 12-month price target of $10.50, representing upside of roughly 60% from recent trading levels. The company employs tens of thousands of workers across its combined global footprint following the Dowlais combination.

Top Financial Highlights

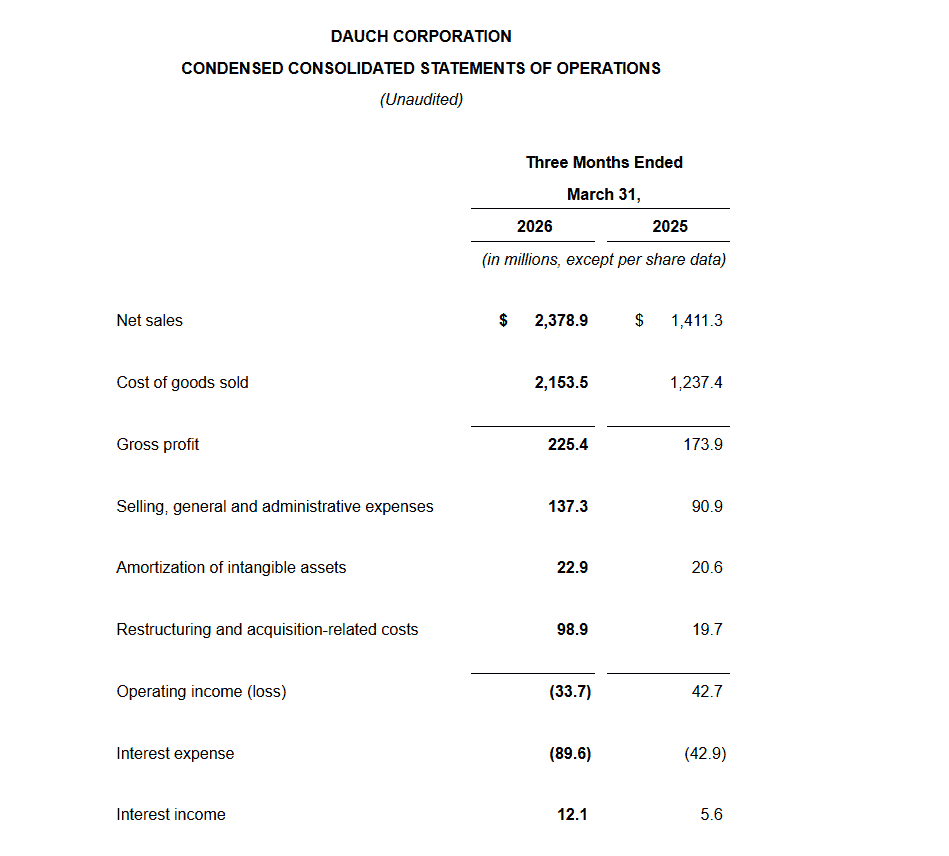

- Total revenue reached $2.38 billion, with net external sales of $2,378.9 million.

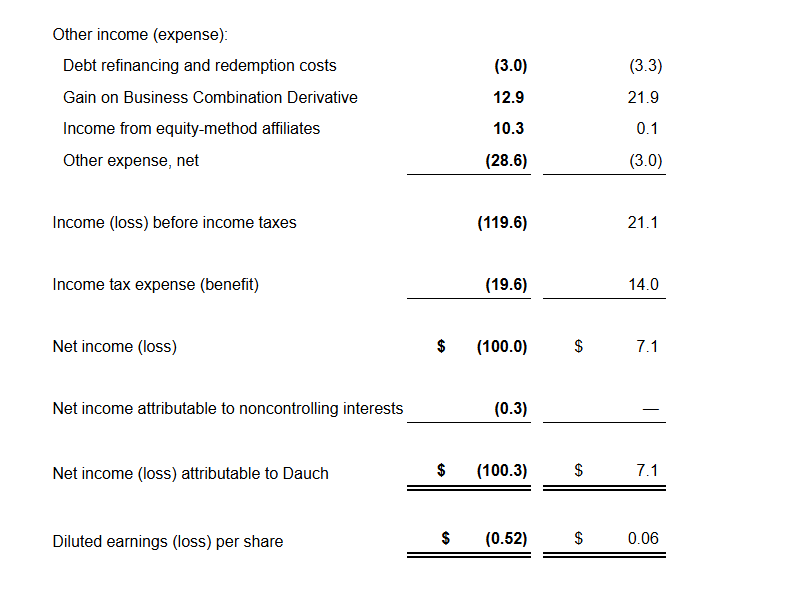

- Net loss attributable to the company was $100.3 million, representing 4.2% of sales.

- GAAP diluted loss per share stood at $0.52.

- Adjusted EPS was $0.34, improving from $0.22 in Q1 2025.

- Adjusted EBITDA reached $308.5 million, representing 13.0% of sales.

- Gross profit totaled $225.4 million, up from $173.9 million in Q1 2025.

- Net cash used in operating activities was $64.4 million.

- Adjusted free cash flow reflected a use of $40.8 million.

- Cash and cash equivalents stood at $1.008 billion at period end.

- Driveline segment sales reached $1,769.1 million, with adjusted EBITDA of $238.8 million.

- Metal forming segment sales totaled $726.2 million, with adjusted EBITDA of $69.7 million.

- Full-year 2026 sales guidance was raised to $10.3 billion to $10.8 billion.

- Full-year 2026 adjusted EBITDA guidance was increased to $1.3 billion to $1.425 billion.

- Full-year 2026 adjusted free cash flow guidance remained between $235 million and $325 million.

Beat or Miss?

| Metric | Reported | Estimated | Difference / Analysis |

| Revenue | $2.38 billion | $2.18 billion (FactSet) | Beat by ~$200 million; +9.2% above consensus |

| Adjusted EPS | $0.34 | -$0.04 (consensus) | Beat by $0.38; massive positive surprise |

| GAAP Diluted EPS | ($0.52) | N/A | Net loss driven by acquisition and restructuring costs |

| Adjusted EBITDA | $308.5 million (13.0% margin) | N/A | Significant expansion vs. 12.6% in Q1 2025 |

| Operating Cash Flow | $(64.4) million | N/A | Seasonal Q1 cash use, expected per management guidance |

What Leadership Is Saying?

CEO Quote (David C. Dauch, Chairman and Chief Executive Officer):

“The company’s first quarter results highlighted a strong start for the new Dauch Corporation. As we begin to capture integration synergies and leverage our combined operational strengths, we are excited about the compelling value and long-term strategic benefits of this transformational acquisition.”

CFO Quote (Christopher John May, Executive Vice President and Chief Financial Officer):

Drawn from the Q4 2025 earnings call in which May set expectations for Q1 2026:

“Due to meaningful January downtime at key customers and only a partial quarter for Dauch sales contributions, we anticipate the first quarter to be our weakest quarter. In addition, we expect normal seasonal cash outflow in the quarter.”

Historical Performance

The table below compares Q1 2026 results against Q1 2025 results on a year-over-year basis.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Net External Sales | $2,378.9 million | $1,411.3 million | 68.60% |

| Gross Profit | $225.4 million | $173.9 million | 29.60% |

| Net Income (Loss) | $(100.3) million | $7.1 million | N/A (swing to loss) |

| Adjusted EBITDA | $308.5 million | $177.7 million | 73.60% |

| Adjusted EPS | $0.34 | $0.22 | 54.50% |

| Operating Cash Flow | $(64.4) million | $55.9 million | N/A (swing to use) |

| Adjusted Free Cash Flow | $(40.8) million | $(3.9) million | -946% |

| Driveline Segment Sales | $1,769.1 million | $987.0 million | 79.20% |

| Metal Forming Segment Sales | $726.2 million | $525.5 million | 38.20% |

Competitor Historical Performance

The table below compares Dauch’s Q1 2026 performance against Dana Incorporated (NYSE: DAN), a direct peer in the global driveline and automotive supply space, using their respective Q1 2026 vs. Q1 2025 reported results.

| Category | Dauch Q1 2026 | Dauch Q1 2025 | Change (%) | Dana Q1 2026 | Dana Q1 2025 | Change (%) |

| Revenue | $2.38 billion | $1.41 billion | 68.60% | $1.87 billion | $1.78 billion | 5.10% |

| Adjusted EBITDA | $308.5 million | $177.7 million | 73.60% | $171 million | $93 million | 83.90% |

| Adjusted EBITDA Margin | 13.00% | 12.60% | +40 bps | 9.2% | 5.20% | +400 bps |

| Net Income (Loss) | $(100.3) million | $7.1 million | Swing to loss | N/A | N/A | N/A |

| Operating Cash Flow | $(64.4) million | $55.9 million | Swing to use | $(156) million | $(37) million | Worsened |

How the Market Reacted?

DCH shares were trading at $5.78 in regular market close on May 7, 2026, just ahead of the earnings release. In extended after-hours trading following the Q1 2026 announcement on May 8, DCH moved to approximately $6.16 to $6.21, a gain of roughly 6.7% to 7.5%, reflecting investor optimism around the revenue beat and raised full-year 2026 guidance.

The report carried a broadly bullish sentiment: adjusted EPS of $0.34 smashed the consensus estimate of -$0.04 by $0.38, and revenue of $2.38 billion came in well above the FactSet estimate of $2.18 billion. Analyst consensus stands at “Strong Buy” with a 12-month price target of $10.50, implying approximately 60% upside from recent levels, underscoring the market’s confidence in the Dauch integration thesis over the medium term.