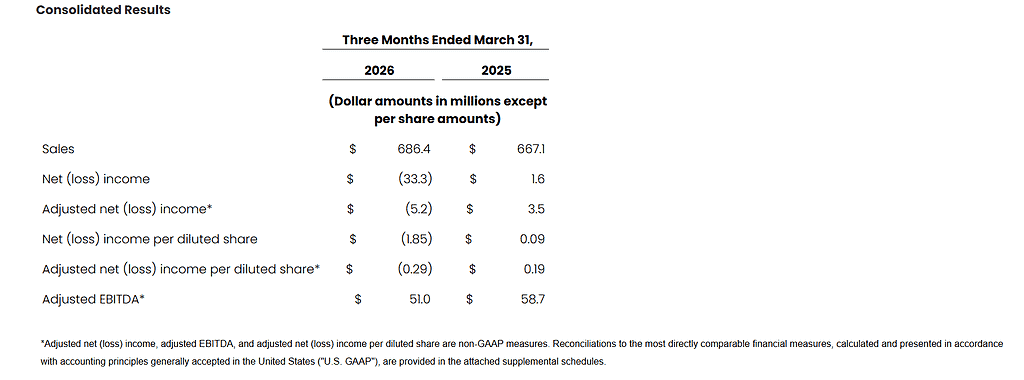

Cooper Standard reported Q1 2026 sales of $686.4 million, up 2.9% year over year, with a GAAP net loss of $33.3 million or $(1.85) per share and adjusted loss of $(0.29) per share. The stock moved higher in after-hours trading as investors reacted to solid sales growth, strong new business wins, and reaffirmed confidence in achieving or exceeding 2026 plans.

About Cooper Standard

Cooper Standard Holdings Inc. is listed on the NYSE under the ticker CPS and had a recent share price around $30 to $31 before its Q1 2026 earnings release. That implies an equity value in the mid hundred million dollar range, reflecting its position as a smaller mid cap auto supplier. Founded in 1960 and headquartered in Northville, Michigan, the company is a leading global supplier of sealing and fluid handling systems and components for light vehicles and industrial applications.

Cooper Standard operates in more than 20 countries and employs approximately 22,000 people, including contingent workers. The company focuses on engineered solutions that leverage materials science and manufacturing expertise to serve both traditional internal combustion and growing hybrid and battery electric vehicle platforms. While the press release does not disclose a current P/E ratio or dividend yield, the negative net income in Q1 2026 means the trailing P/E would not be meaningful for valuation analysis.

Top Financial Highlights

- Q1 2026 sales reached $686.4 million, up 2.9% from $667.1 million in Q1 2025.

- Gross profit improved to $82.4 million, a 6.8% increase from $77.2 million a year earlier.

- GAAP net loss was $33.3 million, versus net income of $1.6 million in Q1 2025.

- GAAP diluted EPS came in at $(1.85), compared with $0.09 per diluted share in the prior year quarter.

- Adjusted net loss was $5.2 million, versus adjusted net income of $3.5 million a year ago.

- Adjusted diluted EPS was $(0.29), down from $0.19 in Q1 2025.

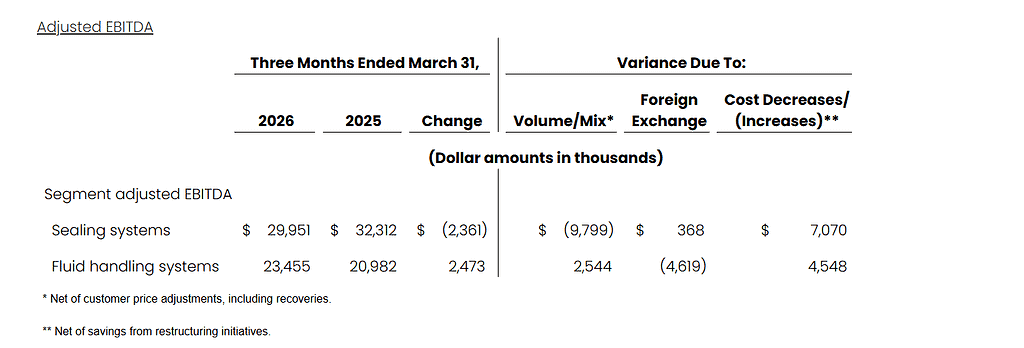

- Adjusted EBITDA was $51.0 million, down from $58.7 million, representing an adjusted EBITDA margin of 7.4% versus 8.8% last year.

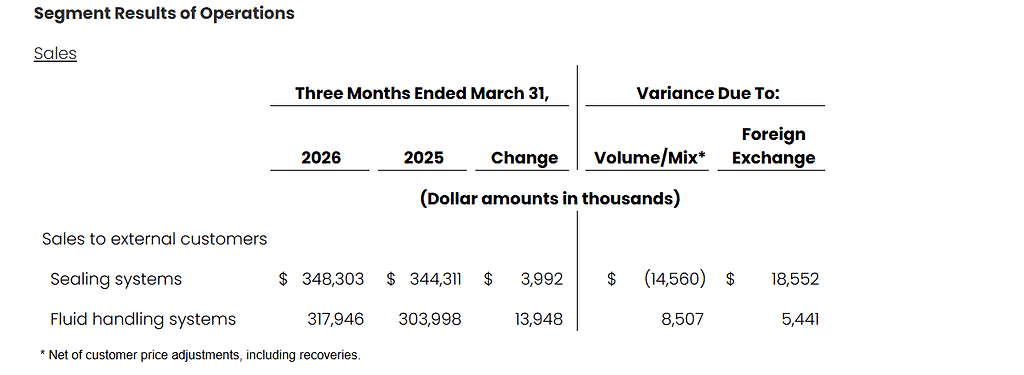

- Sealing systems segment sales were $348.3 million, up from $344.3 million, with segment adjusted EBITDA of $30.0 million.

- Fluid handling systems segment sales were $317.9 million, up from $304.0 million, with segment adjusted EBITDA of $23.5 million.

- Net new business awards totaled $127.9 million in anticipated incremental annual sales, including $31.8 million tied to battery electric or full hybrid platforms.

- Cash and cash equivalents were $118.5 million at March 31, 2026, with total liquidity of $285.8 million including the asset based revolving credit facility.

- Net cash used in operating activities was $69.2 million, compared with $14.9 million used in Q1 2025.

- Capital expenditures were $24.0 million, resulting in free cash flow of $(93.2) million versus $(32.4) million a year earlier.

- The reported net loss included $24.2 million of loss on refinancing and extinguishment of debt plus $4.6 million of restructuring charges and other special items.

- Management reiterated that the company remains on track to achieve or exceed its 2026 sales and profitability guidance issued in February.

Beat or Miss?

Cooper Standard does not disclose explicit consensus EPS and revenue estimates in the press release, but external data point to revenue expectations around $660 million. Using that reference, Q1 revenue appears to have modestly exceeded expectations, while EPS was a loss and cannot be directly compared due to missing consensus figures.

| Metric | Reported | Difference/Analysis |

| Revenue | $686.4 million | Above an implied expectation of about $660 million, suggesting a top line beat. |

| GAAP EPS | ($1.85) | Loss driven mainly by $24.2 million debt refinancing loss and $4.6 million restructuring. |

| Adjusted EPS | ($0.29) | Weaker than prior year $0.19, reflects lower adjusted EBITDA and higher costs. |

| Adjusted EBITDA | $51.0 million | Down from $58.7 million, showing margin pressure despite sales growth. |

| Net New Business | $127.9 million | Healthy pipeline, supports management confidence in full year targets. |

What Leadership Is Saying?

“Our teams delivered results in the quarter that were consistent with our plans and expectations. By maintaining focus on operational excellence and our strategic execution, we are effectively managing current market dynamics and believe we are on track to achieve or exceed our sales and profitability targets for the full year. – Jeffrey Edwards, Chairman and CEO

“Net loss for the first quarter of 2026 was $33.3 million, including restructuring charges of $4.6 million, a loss of $24.2 million related to the successful debt refinancing completed during the quarter, and other special items. Excluding these special items and their related tax impact, adjusted net loss was $5.2 million compared to adjusted net income of $3.5 million in the first quarter of 2025.” – From the company’s detailed financial discussion, reflecting CFO level commentary on margins and special items

Historical Performance

The year over year comparison shows modest sales growth but a swing from profit to loss, largely driven by refinancing related charges, inflation and volume or mix headwinds.

| Category | Q1 2026 | Q1 2025 | Change % |

| Revenue | $686.4 million | $667.1 million | +2.9% sales growth |

| Net income (loss) | $(33.3) million | $1.6 million | Large negative swing >100% |

| Adjusted net income | $(5.2) million | $3.5 million | Deterioration of about 8.7 million |

| Operating income | $24.1 million | $22.3 million | Increase of about 8% |

| Adjusted EBITDA | $51.0 million | $58.7 million | Decline of about 13% |

| Free cash flow | $(93.2) million | $(32.4) million | Significantly more negative |

Change % for net income and some items is described qualitatively because of the swing from a small profit to a sizable loss.

How the Market Reacted?

Market data show Cooper Standard shares closing around $30.95 on May 6, 2026, up about 2.1% during regular trading. In extended hours after the earnings release, the stock traded near $34.25, an increase of roughly 10.7% from the close. That after hours move signals a bullish reaction, with investors rewarding the combination of revenue growth, strong new business awards and management’s reaffirmed confidence in meeting or beating full year 2026 plans despite a reported GAAP loss.