Russel Metals (TSX: RUS) posted record quarterly revenue of C$1.42 billion in Q1 2026, up 21% year-over-year, with EPS of C$1.30 versus C$0.75 in Q1 2025 and net income of C$71.8 million. The stock hit a fresh 52-week high of C$53.74 on the day of the announcement, signaling strong after-hours and next-day market approval.

About Russel Metals

Russel Metals Inc. (TSX: RUS) is one of the largest metals distribution companies in North America, founded in 1929 and headquartered in Mississauga, Ontario, Canada. The company distributes steel and other metal products through three core segments: Metals Service Centers, Energy Field Stores, and Steel Distributors, serving customers across Canada and the United States. As of May 5, 2026, the company trades at C$53.48, carrying a market capitalization of approximately C$2.90 billion and an enterprise value of C$3.27 billion.

The company’s trailing P/E ratio stands at 17.77, with a trailing EPS of C$3.01. Russel Metals has made strategic inroads into the U.S. market, with American operations growing from 39% of revenues in 2024 to 53% in Q1 2026, largely driven by the December 2025 acquisition of seven Kloeckner Metals branches.

Top Financial Highlights

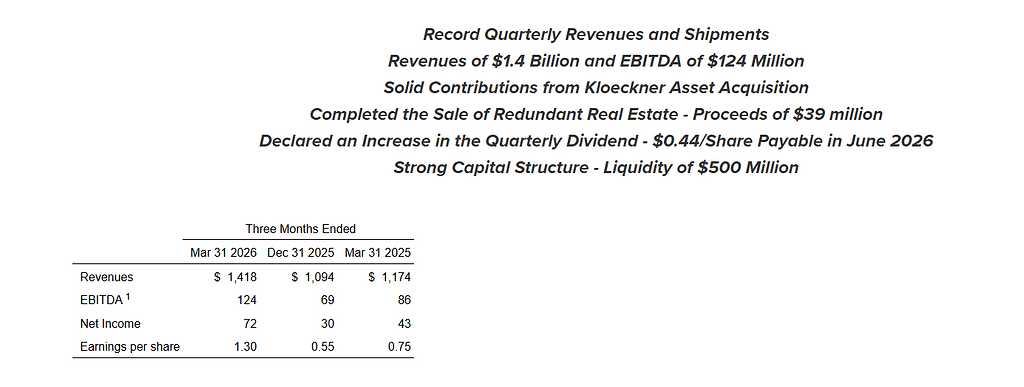

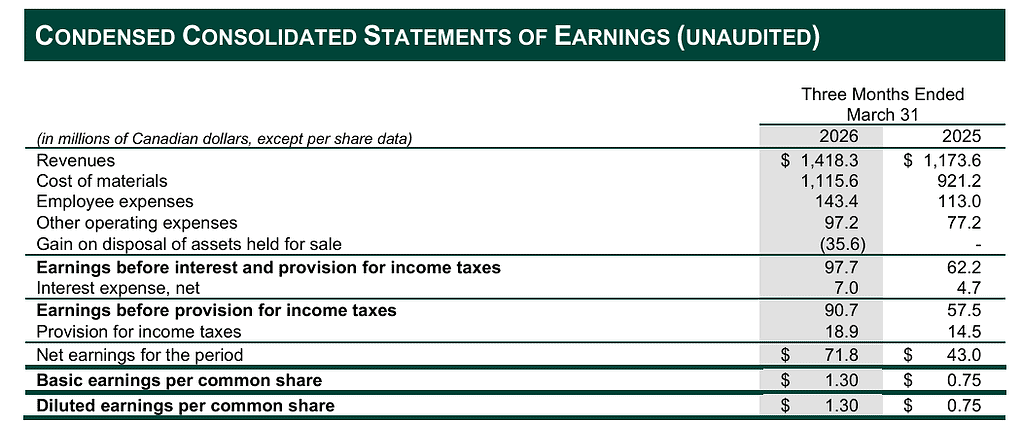

- Total Revenue reached a record C$1,418.3 million in Q1 2026, a 21% increase versus Q1 2025 and a 30% increase versus Q4 2025

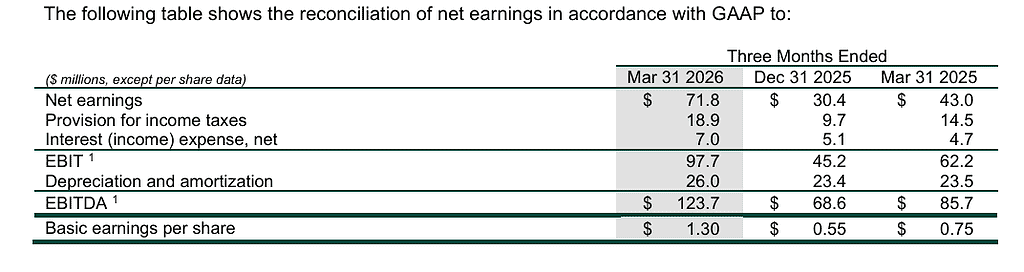

- Net Income was C$71.8 million, up from C$43.0 million in Q1 2025, a 67% year-over-year increase

- Basic EPS was C$1.30, compared to C$0.75 in Q1 2025 and C$0.55 in Q4 2025

- EBITDA reached C$123.7 million, a 44% increase over Q1 2025 and an 80% surge versus Q4 2025

- Comparable EBITDA (excluding the C$36 million Delta property gain and stock-based comp adjustments) was C$93 million

- Average Gross Margin was 21.3%, a slight improvement over Q4 2025 despite dilutive Kloeckner margins

- Cash from operating activities before working capital changes came in at C$78.4 million

- Cash and cash equivalents at quarter-end stood at C$128.1 million; total liquidity was C$500 million

- Kloeckner branches contributed C$183 million in revenue and C$8 million in EBITDA in Q1 2026

- Metal Service Centers segment posted record shipments, with tons shipped up 32% versus Q4 2025 and 18% versus Q1 2025

- U.S. operations represented 53% of revenues and 58% of segment operating profits in Q1 2026

- The company returned C$31 million to shareholders via dividends and share buybacks

- Quarterly dividend increased to C$0.44 per share, payable June 15, 2026, marking the fourth consecutive annual increase

- Net debt stood at C$170 million; DBRS Morningstar reaffirmed investment-grade credit rating of BBB (low) with stable trend

- Annualized return on capital reached 22%, up from 15% in Q1 2025

Beat or Miss?

| Metric | Reported | Prior Year (Q1 2025) | Analysis |

| Revenue | C$1,418.3M | C$1,173.6M | +21% YoY; record quarter |

| Net Income | C$71.8M | C$43.0M | +67% YoY |

| EPS (Basic) | C$1.30 | C$0.75 | +73% YoY |

| EBITDA | C$123.7M | C$85.7M | +44% YoY |

| Gross Margin | 21.3% | ~21% (implied) | Slight improvement despite Kloeckner drag |

| Consensus Estimates | N/A | N/A | Reuters confirmed revenue beat estimates |

What Leadership Is Saying?

The investor conference call was hosted on May 6, 2026 by CEO John G. Reid and CFO Martin L. Juravsky. While verbatim executive quotes were not published in the press release itself, the company’s MD&A commentary attributed to management included the following key statements:

From the CEO (John G. Reid) regarding strategy and vision:

“Our first quarter 2026 results reflected a continuation of improving trend line metrics as a result of favourable market conditions and the realization of benefits from our strategic initiatives. Over the medium-term, we expect to benefit from further rebuilding of the U.S. industrial manufacturing base, Canadian nation building projects, as well as infrastructure related investments in areas such as data centers. In addition, we are positioned to gain market share through our ongoing investments in value-added equipment, facility modernizations and acquisitions.”

From the CFO (Martin L. Juravsky) regarding financials and capital structure:

“We ended the quarter with net debt of C$170 million and total available liquidity of C$500 million. In the first quarter of 2026, we generated C$78 million of cash from operating activities before non-cash working capital, invested C$18 million of capital expenditures to further our internal growth initiatives and returned C$31 million of capital to our shareholders through share repurchases and dividends.”

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | C$1,418.3M | C$1,173.6M | +20.8% |

| Net Income | C$71.8M | C$43.0M | +67.0% |

| EBITDA | C$123.7M | C$85.7M | +44.3% |

| EPS (Basic) | C$1.30 | C$0.75 | +73.3% |

| Cost of Materials | C$1,115.6M | C$921.2M | 21.10% |

| Employee Expenses | C$143.4M | C$113.0M | 26.90% |

| Cash from Operations (pre-WC) | C$78.4M | C$81.9M | -4.30% |

Competitor Historical Performance

Russel Metals operates in the North American metals distribution sector alongside larger U.S.-listed peers such as Reliance, Inc. (NYSE: RS). Reliance posted Q1 2026 net sales of US$4.03 billion, up 15% year-over-year, with EPS of US$5.16, a 37% year-over-year increase. Reliance’s Q1 2026 pretax income reached US$349.5 million, up 33% year-over-year, and record tons sold increased 2.7% YoY and 9.4% sequentially. Both companies benefited from the same broad tailwinds: tariff-driven steel price increases, solid industrial demand, and shipment volume growth.

| Category | Reliance Q1 2026 | Reliance Q1 2025 (est.) | Change (%) |

| Net Sales | US$4.03B | ~US$3.5B | +15% |

| Net Income | US$264.9M | ~US$199.7M | +32.6% |

| EPS (Non-GAAP) | US$5.16 | US$3.77 | 37% |

Note: Russel Metals figures are in Canadian dollars; Reliance figures are in U.S. dollars. Direct comparison requires currency adjustment.

How the Market Reacted?

Shares of Russel Metals (TSX: RUS) reached a new 52-week high of C$53.74 on May 5, 2026, the day earnings were released, closing at C$53.48, up 0.83% on the day from the prior close of C$52.83. The stock had already gained 22.1% since the start of 2026, rising from C$43.80 at the beginning of the year.

Analyst sentiment was broadly bullish following the results, with TD Securities raising its price target from C$50.00 to C$57.00 with a Buy rating, Royal Bank of Canada lifting its target to C$55.00 with an Outperform rating, and Scotiabank maintaining an Outperform with a C$54.00 target. The combination of record revenues, a dividend hike, a C$39 million real estate sale, and improving U.S. margins painted a bullish picture that the market responded to positively.