Seadrill Limited reported Q1 2026 revenue of $358 million and a net loss of $7 million, equal to diluted EPS of -$0.11. Adjusted EBITDA improved to $97 million, supported by higher dayrates and utilization, while guidance for 2026 revenue and EBITDA was raised, indicating a constructive outlook despite continued losses. After-hours movement is not disclosed in the company release, though pre market indications showed a modest positive reaction in extended trading around the earnings date.

About Seadrill Limited

Seadrill Limited is a leading offshore drilling contractor listed on the New York Stock Exchange under the ticker SDRL. The company provides deepwater and ultra deepwater drilling services to national, integrated, and independent oil and gas companies worldwide. Seadrill is headquartered in Hamilton, Bermuda, and is focused on operating a modern fleet of high specification floaters and jack ups that support complex offshore developments.

The business traces its modern corporate roots to 2005, when Seadrill emerged as a major consolidator in offshore drilling, although its operating heritage spans earlier rig operations. As of recent disclosures, Seadrill has a market capitalization of about $1.9 billion, a trailing P/E ratio around 25x, and an indicated employee base of roughly 3,300. The company does not currently pay a regular cash dividend, reflecting a capital allocation focus on fleet investment, maintenance, and balance sheet strength.

Top Financial Highlights

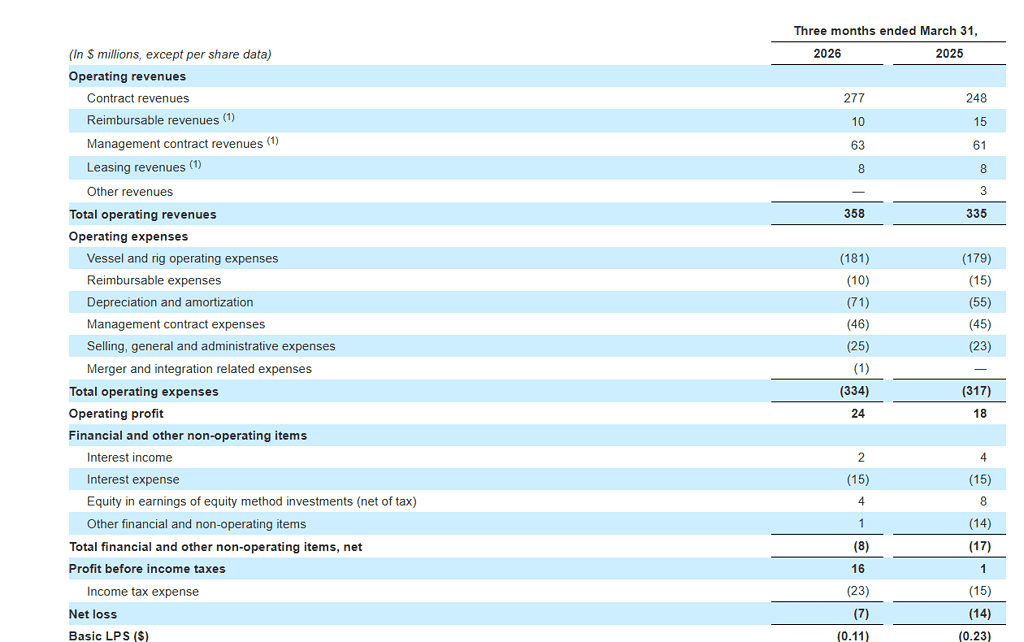

- Total operating revenues for Q1 2026 were $358 million, up from $335 million in Q1 2025.

- Contract revenues reached $277 million, compared with $248 million a year earlier, helped by higher average contractual dayrates and improved economic utilization.

- Management contract revenues contributed $63 million, while leasing revenues added $8 million and reimbursable revenues were $10 million in the quarter.

- Seadrill reported a net loss of $7 million, an improvement from a $14 million net loss in Q1 2025, reflecting better operating profit and lower adverse non operating items.

- Diluted loss per share was -$0.11, better than -$0.23 in the prior year quarter.

- Adjusted EBITDA increased to $97 million, up from $88 million in Q4 2025, implying an Adjusted EBITDA margin of 27.1% on total operating revenues.

- Adjusted EBITDA margin excluding reimbursables was 27.9%, demonstrating underlying operating efficiency improvements across the fleet.

- Total operating expenses were $334 million, compared with $317 million in Q1 2025, driven mainly by higher depreciation, management contract expenses, and selling, general and administrative costs.

- Operating profit came in at $24 million, up from $18 million a year earlier, as revenue growth outpaced cost increases.

- Net cash used in operating activities was $22 million, and net cash used in investing activities was $13 million, leading to negative Free Cash Flow of $35 million for the quarter.

- Cash, cash equivalents, and restricted cash at quarter end totaled $329 million, versus $430 million at March 31, 2025, leaving Seadrill with a net debt position of $296 million against gross principal debt of $625 million.

- The company maintained capital expenditure and long term maintenance guidance at $200 million to $240 million for 2026, while spending $51 million on capital additions and maintenance in Q1 2026.

- Seadrill increased its 2026 total operating revenue guidance range to $1.43 billion to $1.48 billion, excluding $50 million of reimbursable revenues.

- The company also raised its 2026 Adjusted EBITDA guidance to $370 million to $420 million, from a prior range of $350 million to $400 million, citing stronger dayrates and contract awards that expanded contract backlog to $3.1 billion.

Beat or Miss?

Public analyst consensus for Q1 2026 was limited, but available third party data suggested revenue expectations around the mid $320 million range, while EPS estimates were negative. The table below compares reported numbers with available or indicative expectations, using N/A where precise estimates are not disclosed.

| Metric | Reported | Difference or analysis |

| Revenue | $358 million | Above an indicative consensus near $327 million, pointing to a revenue beat. |

| Net income | -$7 million | Loss narrowed versus prior year, but still negative, in line with loss expectations. |

| Diluted EPS | ($0.11) | Better than previous -$0.23 and consistent with expectations for a modest loss. |

| Adjusted EBITDA | $97 million | Up sequentially from $88 million, reflecting stronger operations and higher dayrates. |

| Operating cash flow | -$22 million | Negative due to working capital and project timing, but expected to normalize in H2 2026. |

| 2026 revenue guide | $1.43–$1.48 billion | Raised from $1.40–$1.45 billion, signaling better than previously guided outlook. |

| 2026 EBITDA guide | $370–$420 million | Increased from $350–$400 million, highlighting improved profitability expectations. |

What Leadership Is Saying?

President and CEO Samir Ali: “Seadrill delivered a solid quarter financially and operationally, including the completion of two major projects ahead of schedule and on budget. These achievements, together with recent commercial success, enhance visibility toward higher earnings and Free Cash Flow in the second half of 2026 and into 2027.”

President and CEO Samir Ali: “Increasing demand for deepwater rigs is supported by multiple customers across multiple regions, and with a renewed global focus on energy security, we see growing tailwinds into 2027 to drive positive dayrate momentum.”

Historical Performance

Seadrill’s Q1 2026 results show modest year over year revenue growth and a smaller net loss compared with Q1 2025, driven by higher dayrates, strong utilization, and disciplined cost control. Operating expenses increased, but the company still expanded operating profit and improved Adjusted EBITDA margin.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $358 million | $335 million | 6.9% increase, reflecting stronger activity and pricing. |

| Net income | -$7 million | -$14 million | Loss improved by about 50.0%. |

| Operating expenses | $334 million | $317 million | 5.4% increase, due mainly to higher depreciation and SG&A. |

Historical Performance of competitors

Key offshore drilling peers reported Q1 2026 results earlier this month, showing mixed performance with revenue beats in most cases but varied profitability amid higher dayrates and backlog growth. Transocean and Noble posted revenue growth and positive Adjusted EBITDA, while Valaris saw a revenue decline but strong backlog additions.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Seadrill Revenue | $358 million | $335 million | 6.9% increase. |

| Transocean Revenue | $1.08 billion | N/A | Beat estimates by 5.5%; strong dayrates. |

| Noble Revenue | $786 million | $874 million | -10.1% decline. |

| Valaris Revenue | $465 million | N/A | Beat estimates by 5.6%, down YoY ~25%. |

| Seadrill Net Income | -$7 million | -$14 million | Loss narrowed 50.0%. |

| Transocean EPS | ($0.03) | N/A | Missed estimates by 142.9%. |

| Noble Net Income | $121 million | $108 million | 11.5% increase. |

| Valaris Net Income | -$18 million | N/A | GAAP loss of -$0.24 EPS. |

How the Market Reacted?

Ahead of the release, Seadrill’s shares closed at $48.27 on May 8, 2026, and traded up to about $50.72 in extended hours, indicating a roughly 5% positive move as investors anticipated the Q1 update. The higher revenue base, improving Adjusted EBITDA, and raised full year guidance appear supportive for sentiment despite ongoing net losses and negative Free Cash Flow in the quarter. The strong contract award activity, which lifted backlog to $3.1 billion, also underpins expectations for higher earnings and cash generation in the second half of 2026 and 2027. Overall, the tone of the report is constructive, with operational execution and backlog growth outweighing near term cash burn concerns.