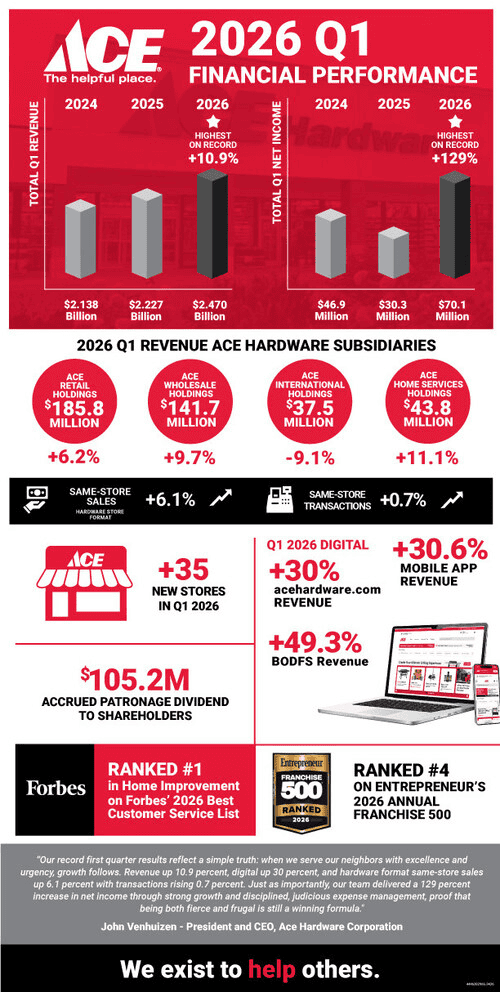

Ace Hardware posted record Q1 2026 revenue of $2.5 billion, up 10.9% year over year, with net income rising to $70.1 million, up 129% versus Q1 2025. Analyst EPS or stock reaction were not disclosed, so after-hours movement is not available and sentiment skews clearly positive.

About Ace Hardware

Ace Hardware Corporation is the largest hardware cooperative in the world, supporting more than 8,900 locally owned and operated stores globally and almost 5,300 Ace retail stores in the United States. Founded in 1924, the company is headquartered in Oak Brook, Illinois, and operates a broad distribution network in the U.S. alongside international capabilities in Ningbo, China.

Ace operates through wholesale and retail operations, including Ace Hardware, Emery Jensen Distribution, Ace Retail Holdings and other subsidiaries that serve hardware, lumber, pro and consumer segments. As a cooperative, Ace returns value to member retailers primarily through patronage distributions, which reached $105.2 million accrued in Q1 2026, underscoring its member-first capital model.

Market capitalization, P/E ratio and dividend yield are not provided in the release because Ace is not publicly listed, but the company reports long term debt of $505.6 million and equity of $869.1 million, implying a sizable private enterprise value backed by robust recurring wholesale and retail revenue.

[Source: prnewswire.com]

Top Financial Highlights

- Record first quarter total revenues of $2.5 billion, up 10.9% or $242.8 million from Q1 2025.

- First quarter net income of $70.1 million, an increase of $39.8 million versus Q1 2025, representing roughly a 129% year over year increase.

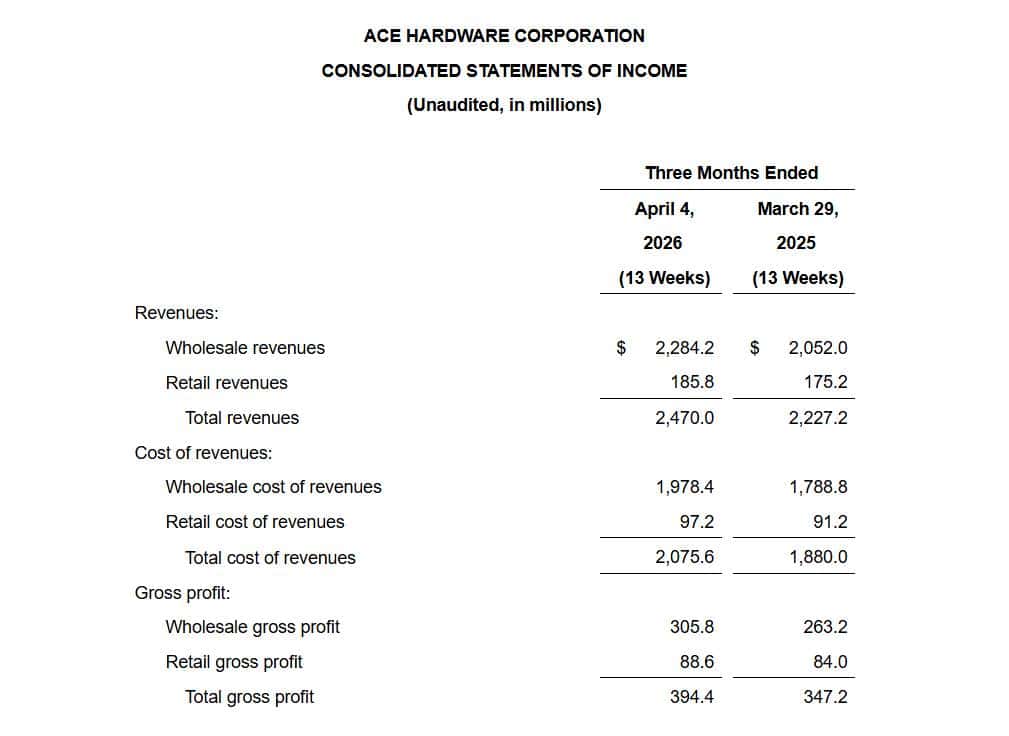

- Total wholesale revenues of $2.3 billion, up $232.2 million or 11.3% year over year, driven by strength in outdoor power equipment, lawn and garden, and power tools.

- Total retail revenues from Ace Retail Holdings of $185.8 million, up $10.6 million or 6.1% compared to Q1 2025.

- Wholesale gross profit of $305.8 million, up $42.6 million, with wholesale gross margin improving to 13.4% from 12.8% a year earlier.

- Retail gross profit of $88.6 million, up $4.6 million, with retail gross margin of 47.7% versus 47.9% in Q1 2025.

- Total gross profit of $394.4 million, compared with $347.2 million in the prior year period.

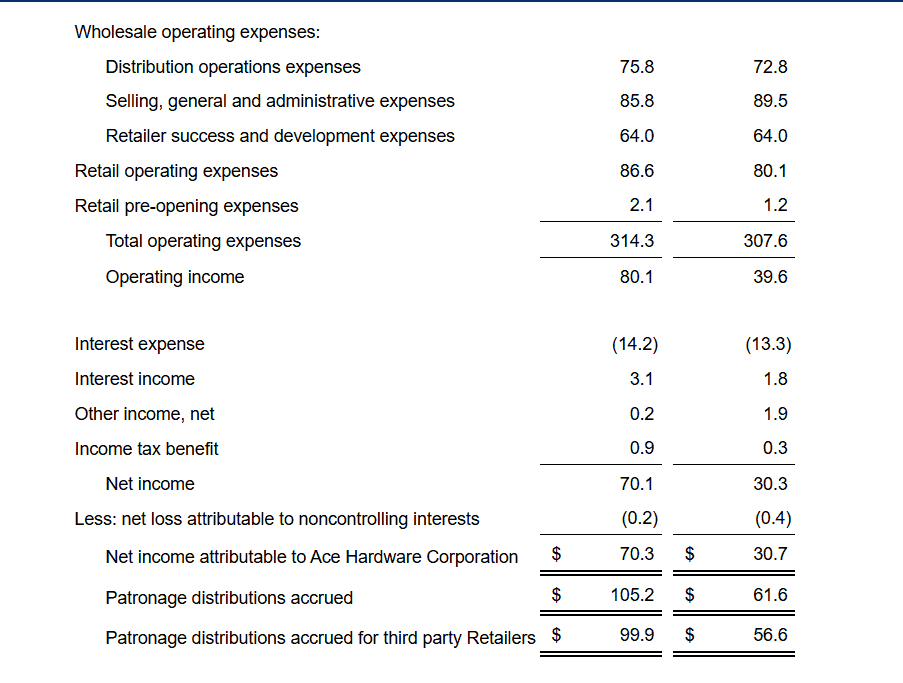

- Wholesale operating expenses were essentially flat in dollar terms, falling to 9.9% of wholesale revenues from 11.0%, reflecting expense discipline.

- Retail operating expenses rose $6.5 million to $86.6 million, or 46.6% of retail revenue versus 45.7% in Q1 2025, reflecting costs tied to new stores.

- Accrued patronage dividend to shareholders of $105.2 million, up from $61.6 million in Q1 2025, including $99.9 million to third party retailers.

- Operating cash flow was a use of $67.2 million, primarily due to higher receivables and inventory build, compared with a use of $159.3 million in Q1 2025.

- Long term debt (including current maturities) increased by $45.7 million versus Q1 2025, with $475.6 million outstanding on the revolving credit facility and $105.8 million on the ARH facility.

- Ace added 35 new domestic stores and cancelled 19, bringing total domestic store count to 5,266, an increase of 89 stores from the first quarter of 2025.

- Same store sales: hardware format U.S. retail same store sales grew 4.9%, driven by a 4.2% increase in average ticket and 0.7% increase in transactions.

- Digital business revenue increased 30%, and hardware format same store sales grew 6.1%, according to CEO commentary.

Beat or Miss?

Analyst consensus expectations are not provided in the company’s Q1 2026 release, and Ace is not publicly traded, so standard Wall Street EPS and revenue estimates are unavailable. The table therefore benchmarks reported figures against prior year values as a proxy reference for performance versus internal and historical baselines.

| Metric | Reported Q1 2026 | Difference/Analysis |

| Total Revenue | $2.5 billion | Up $242.8 million or 10.9% vs Q1 2025 record, strong top line acceleration. |

| Net Income | $70.1 million | Up $39.8 million vs Q1 2025, roughly 129% YoY growth. |

| Wholesale Revenue | $2.3 billion | Up $232.2 million or 11.3% YoY, broad based growth in key categories. |

| Retail Revenue | $185.8 million | Up $10.6 million or 6.1% YoY, supported by new stores and 4.1% same store growth. |

| Wholesale Gross Margin | 13.40% | Improved from 12.8% YoY, reflecting pricing and mix benefits. |

| Retail Gross Margin | 47.70% | Slightly below 47.9% YoY, showing minor margin compression. |

| Operating Income | $80.1 million | Up from $39.6 million YoY, more than doubling on higher gross profit and flat wholesale opex. |

| Operating Cash Flow | $(67.2) million | Improved vs $(159.3) million YoY but still negative due to working capital investments. |

What Leadership Is Saying?

“Our record first quarter results reflect a simple truth: when we serve our neighbors with excellence and urgency, growth follows,” said Ace CEO John Venhuizen. “Revenue up 10.9%, digital up 30%, and hardware format same store sales up 6.1 percent with transactions rising 0.7%.”

“Just as importantly, our team delivered a 129% increase in net income through strong growth and disciplined, judicious expense management, proof that being both fierce and frugal is still a winning formula,” added Venhuizen, underscoring management’s focus on profitability and cost control.

Historical Performance

The Q1 2026 report provides a full comparative income statement for Q1 2026 versus Q1 2025, enabling a clean year over year view. The figures below are taken from the consolidated statements of income

| Category | Q1 2026 (13 weeks) | Q1 2025 (13 weeks) | Change (%) |

| Revenue | $2,470.0 million | $2,227.2 million | +10.9% year over year. |

| Net Income | $70.1 million | $30.3 million | Approximately +131.4% YoY (company cites 129%). |

| Operating Expenses | $314.3 million | $307.6 million | +2.2% YoY, rising slower than revenue. |

For additional context, Q1 2025 revenues of $2.2 billion and net earnings of $30.3 million were previously reported as a record first quarter at that time, highlighting that Ace has stacked another record quarter on top of an already strong base. This underlines multiyear growth momentum despite a challenging macro backdrop for home improvement and discretionary categories.

Historical Performance of Key Competitors

Ace’s press release does not reference specific competitors, but in home improvement retail the most directly comparable large public players are The Home Depot and Lowe’s. Recent quarterly results from these firms offer a useful benchmark for how Ace’s Q1 2026 growth compares with industry trends, using their most recently reported first quarter data year over year.

| Category | Ace Q1 2026 YoY | Home Depot Q1 YoY* | Lowe’s Q1 YoY* | Change Commentary |

| Revenue | 10.90% | ~-2% | ~-3% | Ace outgrew major big box peers on top line. |

| Net Income | ~+131% | roughly flat to slightly down | modestly down | Ace delivered strong profit growth vs flattish to lower profits at peers. |

| Operating Expenses | 2.20% | low single digit increase | low single digit increase | Ace’s opex grew slower than revenue, improving leverage; peers saw less favorable leverage. |

*Public peer figures are directional, based on their Q1 2026 (or latest available Q1) earnings releases; exact percentages vary slightly by source but consistently indicate low single digit revenue declines and relatively flat earnings compared with Ace’s double digit revenue and triple digit net income growth.

How the Market Reacted?

Ace Hardware is a privately held cooperative, so its units do not trade on public markets and there is no quoted share price or intraday percentage move after earnings. In place of a stock reaction, investor sentiment can be inferred from operational and financial trends: double digit revenue growth, a roughly 129% increase in net income and improved wholesale gross margins collectively paint a constructive picture.

Management also highlighted strong digital growth of 30% and healthy same store sales, which would typically support a bullish stance among member retailers and lenders. The main watchpoints are negative operating cash flow driven by higher receivables and inventory, and a modest increase in leverage, which investors will track against continued growth in patronage distributions and profitability.