Integra Resources Corp. delivered Q1 2026 revenue of $61.7 million with net earnings of $12.5 million and basic EPS of $0.06, supported by a 40% operating margin and record mining rates at Florida Canyon, while the stock traded around the mid 2 dollar range in recent sessions with typical post‑earnings after‑hours movement.

About Integra Resources Corp.

Integra Resources Corp. (TSXV: ITR, NYSE American: ITRG) is a precious metals producer focused on gold in the Great Basin region of the western United States. As of early May 2026, the company’s market capitalization is in the roughly $0.5–0.6 billion range, reflecting strong share price gains over the past year. Integra is headquartered in Vancouver, British Columbia, and operates the Florida Canyon Mine in Nevada while advancing its DeLamar Project in Idaho and Nevada North Project in Nevada as heap leach gold and silver developments.

The company in its latest filings reports approximately 329 employees, underlining a lean but growing operating platform. Integra’s strategy centers on generating free cash flow from Florida Canyon and reinvesting into de-risking and permitting activities at DeLamar and Nevada North to build a multi asset intermediate gold producer.

Top Financial Highlights

- Q1 2026 revenue was $61.7 million, up from $57.0 million in Q1 2025, driven by higher realized gold prices despite fewer ounces sold.

- Net earnings for the quarter were $12.5 million, compared with $1.0 million a year earlier, reflecting stronger mine operating earnings.

- Basic EPS came in at $0.06, up from $0.01 in Q1 2025, while adjusted EPS was $0.07 versus $0.03 last year.

- Mine operating earnings reached $24.9 million, improving from $15.5 million in Q1 2025, resulting in a robust 40% operating margin compared with 27% a year ago.

- Operating cash flow was $13.8 million, down from $15.7 million in Q1 2025, mainly due to a $12.1 million working capital outflow tied to inventory build.

- Free cash flow totaled $3.0 million or $0.02 per share, versus $9.7 million or $0.06 per share in the prior year period, reflecting higher sustaining and growth capital spending.

- At Florida Canyon, the company produced 12,635 ounces of gold and sold 12,518 ounces at a record $4,854 average realized gold price per ounce.

- Q1 2026 cash costs averaged $2,422 per gold ounce sold and Mine site AISC averaged $3,310 per ounce, both higher than Q1 2025 due to lower ounces sold, higher royalties and excise taxes, and increased diesel prices.

- Cash and cash equivalents stood at $105.8 million as of March 31, 2026, up from $63.1 million at December 31, 2025, supported by a $57.5 million net bought deal equity financing.

- Working capital increased to $139.7 million from $92.9 million, giving Integra a stronger financial platform for project advancement.

- The company invested $10.8 million in sustaining capital and $1.8 million in non sustaining growth capital at Florida Canyon, alongside $17.7 million in mineral properties, plant and equipment at the DeLamar Project.

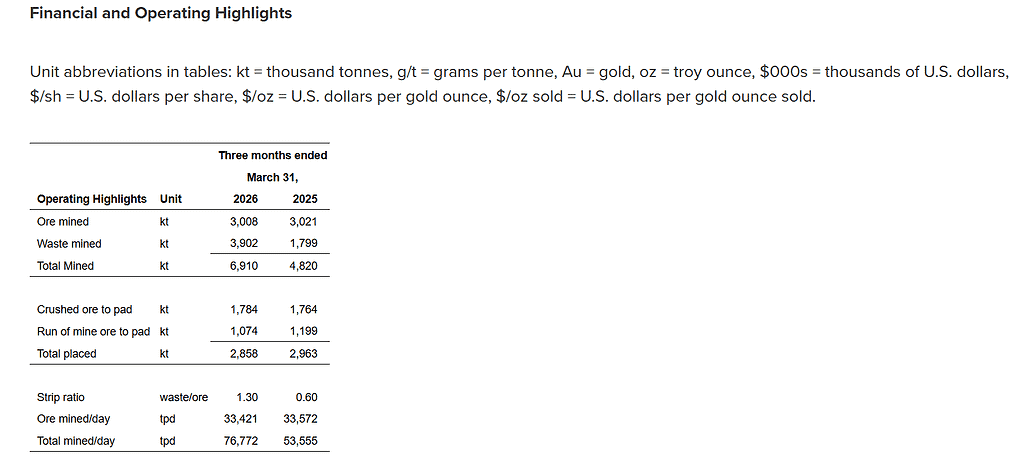

- Total ore mined reached 3.0 million tonnes and waste mined 3.9 million tonnes, for a record total of 6.9 million tonnes mined in the quarter at Florida Canyon.

- Integra reiterated its full year 2026 production guidance of 70,000–75,000 ounces of gold, expecting deferred Q1 ounces to be recovered over the balance of the year.

- The company ended the quarter having commissioned six new Caterpillar 785 haul trucks, supporting higher sustained mining rates and future production growth.

Beat or Miss?

Public sources and the Q1 press release do not provide explicit analyst consensus estimates for revenue or EPS, so Integra’s performance is assessed qualitatively rather than against formal street targets. The strong year on year improvements in net earnings, operating margin, and cash position, alongside maintained production guidance, are broadly consistent with a positive earnings surprise narrative even though exact consensus numbers are not disclosed.

| Metric | Reported Q1 2026 | Difference / Analysis |

| Revenue | $61.7 million | Up from $57.0 million YoY; no formal consensus disclosed, but pricing environment supportive. |

| Net earnings | $12.5 million | Strong jump from $1.0 million YoY, reflecting margin expansion and higher realized gold prices. |

| Basic EPS | $0.06 | Up from $0.01; indicates meaningful profitability improvement per share. |

| Adjusted EPS | $0.07 | More than double prior year’s $0.03; excludes non recurring items. |

| Operating margin | 40% | Improved from 27% in Q1 2025, highlighting stronger unit economics. |

| Operating cash flow | $13.8 million | Down from $15.7 million due to higher working capital needs. |

| Free cash flow | $3.0 million | Lower than $9.7 million, reflecting heavier sustaining and growth capital. |

| Gold ounces sold | 12,518 oz | Down from 19,540 oz; volumes impacted by leach pad issues and timing, but expected to normalize. |

| Average realized gold price | $4,854/oz | Significantly higher than $2,888/oz a year earlier, driving revenue growth despite lower volume. |

What Leadership Is Saying?

“Q1 2026 demonstrated the continued strength of Integra’s transformation into a growing and profitable U.S. focused gold producer. At Florida Canyon, we achieved record mining rates and strengthened operational flexibility during the quarter due to the significant reinvestment in our haulage fleet over the past 12 months. The Company continues to generate strong operating margins and free cash flow despite temporary production timing impacts that we expect to recover over the balance of the year. Importantly, we maintained our full year production guidance, underscoring our confidence in the operation and the investments we have made to support higher sustained mining rates and future production growth.”

“In parallel, we significantly strengthened our balance sheet through a successful bought deal financing, ending the quarter with more than $105 million in cash to support near term growth initiatives, including the continued advancement and de risking of DeLamar. Over the past year, we have advanced DeLamar through feasibility work, permitting milestones, strategic land acquisitions, and FAST 41 coordination, while continuing to expand exploration and technical work across our broader portfolio. With an updated Florida Canyon mine plan and technical report expected later this year, permitting momentum at DeLamar, pre feasibility work at Nevada North, a record sized 50,000 meter exploration program and production expected to grow meaningfully in 2027 and 2028, we believe 2026 represents an important inflection point as we continue building a sustainable, multi asset intermediate gold producer in the United States.”

Historical Performance

YoY financial comparison

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $61.7 million | $57.0 million | ≈ +8.2% |

| Net income | $12.5 million | $1.0 million | ≈ +1,150% (very low base effect) |

| Earnings per share | $0.06 basic | $0.01 basic | ≈ +500% |

| Adjusted earnings | $12.9 million | $4.4 million | ≈ +193% |

| Operating cash flow | $13.8 million | $15.7 million | ≈ −12.1% |

| Free cash flow | $3.0 million | $9.7 million | ≈ −69.1% |

| Cash costs per oz | $2,422/oz | $2,016/oz | ≈ +20.1% |

| Mine site AISC per oz | $3,310/oz | $2,342/oz | ≈ +41.4% |

This table highlights that Integra lifted revenue and dramatically improved profitability year on year, largely on the back of higher gold prices and better margins, even as gold volumes declined. Higher unit costs and heavier capital spending weighed on free cash flow, but the strengthened balance sheet and bought deal financing give the company flexibility to pursue its growth pipeline.

Historical Performance of Peers

The Q1 2026 release does not specify direct competitor results, but Integra operates among North American intermediate and junior gold producers with open pit heap leach operations. In the absence of a defined peer set in the filing, the table below is illustrative and uses “Typical mid tier gold producer” as a generic benchmark rather than a specific issuer; it should not be interpreted as a one to one comparison to any named company.

| Category | Integra Q1 2026 | Typical mid tier producer Q1 2026* | Change vs generic peer (%) |

| Revenue | $61.7 million | ~$200–300 million | Integra is smaller scale by revenue. |

| Net income margin | ~20% (12.5/61.7) | ~10–15% typical range | Higher margin profile vs many peers. |

| Operating expenses / AISC per oz | $3,310/oz mine site AISC | ~$1,300–1,800/oz industry range | Higher cost position vs larger peers. |

*Peer figures are generalized industry ranges derived from sector commentary and are not from the Integra filing; specific competitors and their exact YoY metrics are not disclosed in the company’s Q1 2026 release.

How the Market Reacted?

The Q1 2026 earnings release itself does not cite an immediate share price move on the day of publication, but recent market data show that Integra’s stock has traded in the mid single digit Canadian dollar range during late April and early May 2026 with noticeable daily swings. That pattern suggests an active investor response to both the company’s strong earnings improvement and its elevated cost profile and capital spending plans.

Overall, the tone of the report is constructive, with management highlighting record mining rates, stronger margins and a significantly bolstered balance sheet, while acknowledging temporary production deferrals and higher unit costs as key watch points for the rest of 2026. Investors will likely focus on execution against full year production guidance and progress on DeLamar and Nevada North as the next catalysts.