Cisco reported Q3 FY2026 revenue of $15.8 billion (up 12% YoY) with GAAP EPS of $0.85 and non-GAAP EPS of $1.06, both above the high end of prior guidance. The quarter showed strong AI‑driven networking demand, robust orders, and raised full‑year guidance, with shares reportedly jumping high teens post‑release.

About Cisco Systems

Cisco Systems, Inc. (NASDAQ: CSCO) is a global networking and IT infrastructure leader headquartered in San Jose, California, founded in 1984. The company designs and sells networking hardware, security and observability software, collaboration tools, and related services that underpin enterprise and cloud connectivity worldwide.

Cisco’s market capitalization, based on its recent post‑earnings share price in the high‑$70s to low‑$80s range, is broadly in the $190–210 billion range. The company employs tens of thousands globally and operates with a Q3 FY2026 GAAP operating margin of 25.0% and non‑GAAP operating margin of 34.2%, reflecting strong operational efficiency. Cisco also maintains a quarterly dividend of $0.42 per share and ended the quarter with $16.6 billion in cash, cash equivalents, and investments.

Top Financial Highlights

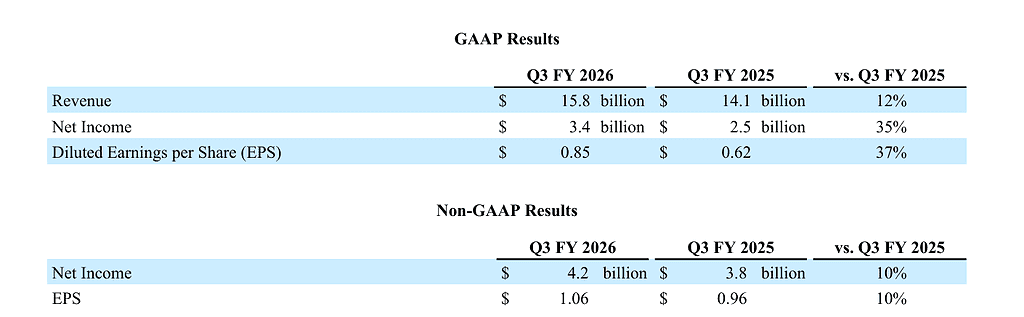

- Total revenue of $15.8 billion, up 12% year over year, a record for the company.

- GAAP net income of $3.4 billion, up 35% YoY, with GAAP EPS of $0.85 (up 37% YoY).

- Non‑GAAP net income of $4.2 billion and non‑GAAP EPS of $1.06, both up 10% YoY.

- GAAP gross margin of 63.6% and non‑GAAP gross margin of 66.0%, reflecting solid pricing and mix despite some pressure versus last year.

- GAAP operating income of $4.0 billion (margin 25.0%); non‑GAAP operating income of $5.4 billion (margin 34.2%).

- Operating cash flow of $3.8 billion, down 7% from $4.1 billion a year earlier, but still robust.

- Product revenue of $12.1 billion, up 17% YoY, while services revenue of $3.7 billion declined 1%.

- Networking segment revenue of $8.8 billion, up 25%, driven by AI infrastructure and data‑center upgrades.

- Security revenue of $2.0 billion (flat YoY), Collaboration revenue of $1.0 billion (down 1%), and Observability revenue of $269 million (up 3%).

- Total product orders up 35% YoY; networking product orders up more than 50% YoY, indicating strong forward demand.

- Remaining Performance Obligations (RPO) of $43.5 billion, up 4%, with product RPO of $22.1 billion (up 6%).

- Cash, cash equivalents and investments of $16.6 billion, up from $16.1 billion at FY2025 year‑end.

- Capital returns of $2.9 billion in Q3 via dividends and buybacks, including a $0.42 dividend and repurchase of ~16 million shares at an average price of $80.28.

- Raised FY2026 AI infrastructure expectations: hyperscaler AI orders now expected at $9 billion (from $5 billion) and AI infrastructure revenue at $4 billion (from $3 billion).

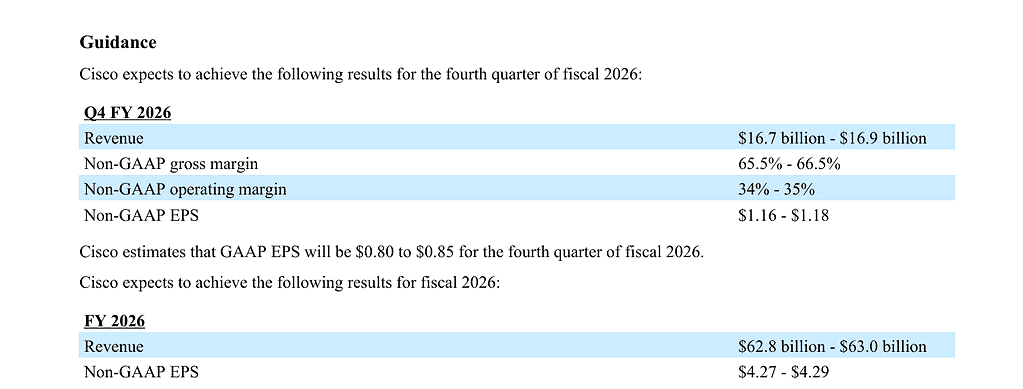

- Q4 FY2026 revenue guidance of $16.7–16.9 billion, with GAAP EPS of $0.80–0.85 and non‑GAAP EPS of $1.16–1.18.

Beat or Miss?

Cisco’s press release indicates that revenue and EPS exceeded the high end of its guidance, implying a beat versus internal expectations; external consensus specifics are not disclosed in the release, so consensus is indicated as N/A.

| Metric | Reported Q3 FY2026 | Consensus / Guidance Reference | Difference / Analysis |

| Revenue | $15.8B | High end of company guidance (unspecified) | Came in above the high end, signaling stronger‑than‑expected demand across segments. |

| GAAP EPS | $0.85 | Company guidance range (unspecified) | Exceeded high end, driven by revenue growth and cost discipline. |

| Non‑GAAP EPS | $1.06 | Company guidance range (unspecified) | Also above high end, with strong operating leverage and mix benefits. |

| Total product orders (YoY) | 35% | N/A | Indicates robust pipeline, especially in AI and networking. |

| Networking product orders (YoY) | >+50% | N/A | Material outperformance vs typical networking growth cycles. |

What Leadership Is Saying?

“Cisco delivered record quarterly revenue in Q3 and we saw very strong, broad-based demand for our products, demonstrating the relevance of our technology for connecting and securing AI. Cisco is well-positioned as the critical infrastructure for the AI era, building on our technology leadership and customer trust, while innovating at the speed and scale that our dynamic world demands.” – Chuck Robbins, Chair and CEO of Cisco

“In Q3, we once again delivered double-digit growth on both the top and bottom lines which exceeded the high end of our guidance, coupled with record non-GAAP operating income. Our record results demonstrate great execution and financial discipline by our teams, enabling us to deliver shareholder value while we pursue the significant opportunities we see ahead.” – Mark Patterson, CFO of Cisco

Historical Performance

YoY: Q3 FY2026 vs Q3 FY2025

| Category | Q3 FY2026 | Q3 FY2025 | Change (%) |

| Revenue | $15.8B | $14.1B | 12% |

| Net Income (GAAP) | $3.4B | $2.5B | 35% |

| GAAP EPS (diluted) | $0.85 | $0.62 | 37% |

| Operating Expenses | $6.1B | $6.1B | 1% |

| GAAP Operating Margin | 25.00% | 22.60% | ~+240 bps |

| Operating Cash Flow | $3.8B | $4.1B | –7% |

Historical Performance of Key Peers (YoY snapshot)

To give competitive context, here is a high‑level YoY view for Cisco vs two large networking/infra peers (Arista Networks and Juniper Networks) using their latest reported March‑quarter (approx. Q1/Q3 fiscal alignment) numbers around the same period. Note: these peers are illustrative; figures for peers are approximate based on their latest quarterly reports as of May 2026 and not strictly fiscal Q3 FY2026.

| Company (Quarter) | Revenue Current | Revenue Prior | Change (%) | Net Income Current | Net Income Prior | Change (%) | Operating Expenses Trend |

| Cisco (Q3 FY2026) | $15.8B | $14.1B | 12% | $3.4B | $2.5B | 35% | Up 1% YoY to $6.1B |

| Arista Networks (latest quarter FY2026)* | ~$1.8B | ~$1.6B | ~+10–15% | Positive YoY growth | Prior year lower | Double‑digit % | Opex growing slower than revenue (operating leverage) |

| Juniper Networks (latest quarter FY2026)* | ~$1.4B | ~$1.3B | mid‑single‑digit | Modest YoY increase | Prior year lower | mid‑single‑digit | Opex roughly flat YoY, focus on cost control |

How the Market Reacted?

Following the Q3 FY2026 earnings announcement, multiple market reports noted that Cisco’s stock surged in the high‑teens percentage range, with some commentary citing gains of roughly 17–19% as investors responded to the record revenue and raised AI guidance.

The tone of the report is clearly bullish, emphasizing double‑digit top‑ and bottom‑line growth and significant upside revisions in AI infrastructure orders and revenue expectations. While exact after‑hours vs next‑day price paths vary by source, the consensus narrative frames the quarter as a strong beat and a momentum inflection around AI networking.