Introduction

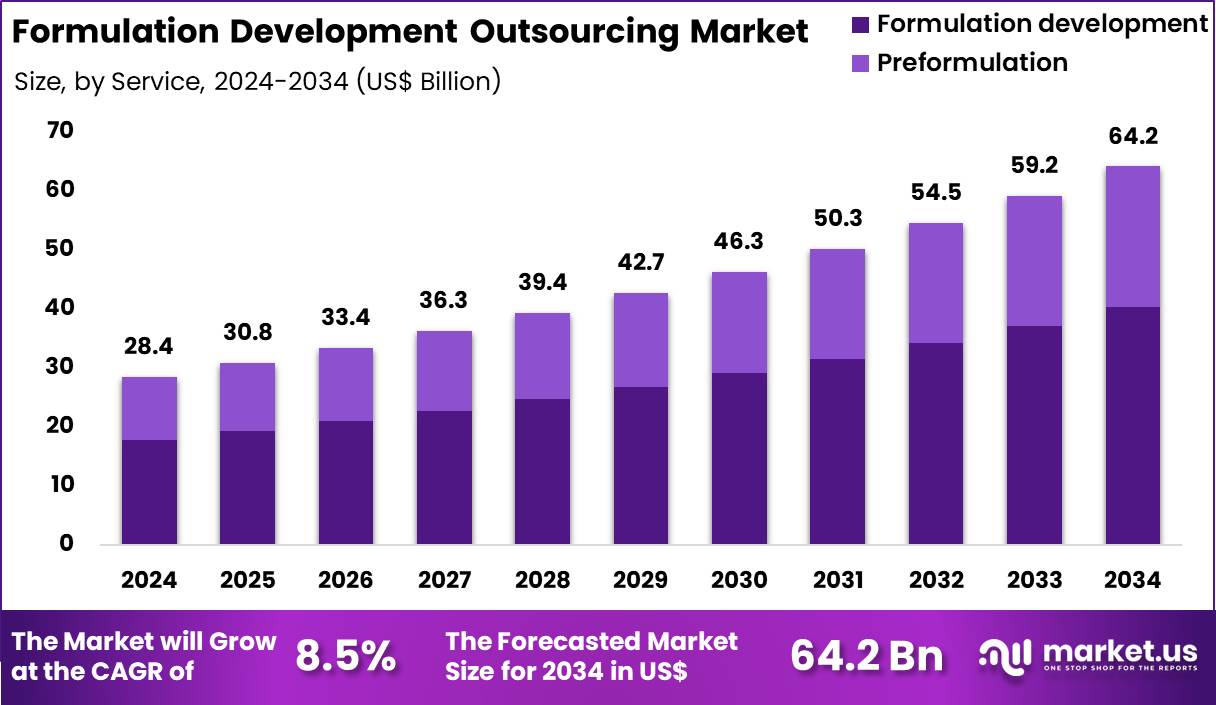

The Global Formulation Development Outsourcing Market is projected to surge from US$28.4 billion in 2024 to US$64.2 billion by 2034, registering a robust CAGR of 8.5%. This growth is fueled by complex drug pipelines, rising biologics, and strong demand for solubility and bioavailability enhancement across oral and injectable dosage forms.

North America dominates with 43.7% share, reflecting heavy reliance on contract partners for oncology, cardiovascular, and specialty formulations. Expanding oncology pipelines, higher regulatory scrutiny, and cost-optimized R&D models are accelerating outsourcing as pharma and biotech seek faster, de-risked paths from preformulation to clinical and commercial stages.

Get the latest insights and updates at @ https://market.us/report/formulation-development-outsourcing-market/free-sample/

Key Takeaways

- Market to reach US$ 64.2 billion by 2034 at an 8.5% CAGR, underscoring strong structural demand.

- North America leads with 43.7% share, while Asia Pacific is set for the fastest CAGR.

- Oncology (41.7% share) and oral formulations (48.6% share) are dominant growth axes.

- Regulatory complexity and IP risk restrain some outsourcing but create opportunities for high-compliance providers.

- AI adoption, biologics focus, and integrated CDMO models are key competitive levers.

Sector-Specific Impacts

- Oncology: With oncology accounting for 41.7% of therapeutic-area revenue, cancer pipelines heavily rely on outsourcing for complex delivery systems, targeted formulations, and stability under stressed conditions, enabling faster progression through accelerated approval pathways.

- Biologics and Biosimilars: Biologics developers outsource lyophilization, nanoparticle, and liposomal systems, while biosimilar programs depend on CDMOs for comparability, bioavailability, and continuous manufacturing-compatible formulations.

- Generics and 505(b)(2): Generic and 505(b)(2) sponsors leverage reformulation, modified-release designs, and taste-masked pediatric forms to differentiate products and extend lifecycles without heavy capital expenditure.

- SME Biotech: Small and mid-size biopharma entities, often with lean internal R&D, rely almost entirely on external partners from preformulation through early clinical batches, enabling rapid proof-of-concept with limited upfront investment.

Strategies for Businesses

Global pharma, biotech, and CDMOs should prioritize end-to-end service models that integrate preformulation, analytical development, scale-up, and clinical supply to capture more value per molecule and simplify sponsor interfaces. Investing in AI-driven formulation design, predictive stability modeling, and high-throughput screening can cut trial-and-error cycles and position providers as technology leaders.

Sponsors need dual-sourcing and multi-region vendor strategies to mitigate geopolitical, tariff, and supply-chain shocks, especially in API-intensive programs. Building specialized capabilities in oncology, biologics, and pediatric formulations, alongside continuous manufacturing compatibility, will differentiate players in the fastest-growing, highest-margin segments. Robust quality systems, data integrity frameworks, and regulatory intelligence are essential for navigating complex, multi-jurisdictional GMP expectations and strengthening long-term client trust.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 28.4 Billion |

| Forecast Revenue (2034) | US$ 64.2 Billion |

| CAGR (2025-2034) | 8.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service (Formulation Development and Preformulation), By Formulation Type (Oral, Injectable, Topical and Others), By Therapeutic Area (Oncology, Cardiovascular, Dermatology, Genetic Disorders and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Catalent, Inc., Patheon (Thermo Fisher Scientific), PCI Pharma Services, Recipharm AB, Lonza Group, Samsung Bioepis, FUJIFILM Diosynth Biotechnologies, Parexel International, Charles River Laboratories, WuXi AppTec |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Analyst Viewpoint

At present, the formulation development outsourcing market is in a strong upcycle, supported by robust approvals of novel drugs, robust oncology and biologics pipelines, and a clear shift toward asset-light R&D strategies across pharma and biotech. Regulatory pressures and solubility challenges, rather than acting purely as constraints, are driving sponsors toward expert partners with validated technologies and global networks. Over the next decade, analysts expect sustained high-single-digit growth as AI-enabled design, continuous manufacturing, and advanced delivery systems deepen the value proposition of outsourcing.

Asia Pacific is likely to emerge as a co-equal hub alongside North America and Europe, as governments promote innovation-friendly ecosystems and harmonize standards. Despite periodic macroeconomic volatility, the structural need to convert complex molecules into stable, patient-centric products positions this market as a long-term positive play for investors and innovators alike.

Regional Analysis

North America currently leads the formulation development outsourcing market with a 43.7% share, underpinned by a mature pharma ecosystem, stringent FDA expectations, and strong demand for advanced solubility, bioavailability, and patient-centric formulations. The region’s outsourcing intensity is amplified by talent shortages in internal R&D and competitive pressures around biosimilars and specialty drugs. Europe remains a major hub, driven by active clinical trial networks and established CDMO presence across Germany, the UK, and other key countries.

Asia Pacific is projected to deliver the highest CAGR, supported by pro-innovation policies, tax incentives, and fast-growing chronic disease burdens in China, India, and Southeast Asia. Latin America and the Middle East & Africa are emerging as secondary destinations, benefiting from localization strategies and early-stage investments in GMP capabilities.

Business Opportunities

The market offers significant business opportunities for CDMOs and new entrants that can specialize in high-value niches such as nanoparticle delivery, liposomal systems, and pediatric-friendly dosage forms. Biopharmaceutical outsourcing around monoclonal antibodies and complex biologics is expanding rapidly, creating room for providers that bring integrated formulation, analytical, and scale-up expertise. AI-enabled formulation platforms open SaaS-like revenue models and data-driven service offerings, differentiating players beyond traditional lab capacity.

Regional opportunities are pronounced in Asia Pacific, where government incentives, rising NMPA approvals, and growing clinical trial activity are drawing global sponsors toward local partners. Additionally, strategic M&A such as acquisitions that broaden small-molecule expertise or oral dosage capabilitiesallows companies to quickly fill portfolio gaps and cross-sell end-to-end solutions.

Key Segmentation

Service Analysis: Formulation development accounted for 62.8% of service growth, driven by increasing molecular complexity and regulatory expectations. Sponsors outsource to access specialized expertise, scalable resources, and advanced equipment, improving bioavailability, reducing failures, enabling multiple dosage forms, and optimizing development timelines and costs.

Formulation Type Analysis: Oral formulations accounted for 48.6% of growth in formulations, driven by strong small-molecule pipelines and high patient compliance. Outsourcing enhances solubility, bioavailability, and modified-release performance. Cost-effective manufacturing, generic development, and scale-up expertise support rapid prototyping, reformulation cycles, and tailored solutions globally.

Therapeutic Area Analysis: Oncology captured 41.7% of therapeutic growth, driven by expanding pipelines and complex molecules requiring advanced delivery strategies. Outsourcing provides expertise and customized formulations. Accelerated approvals, combination therapies, and personalized medicine increase iterations, while partners support trials, supply, and regulatory requirements.

Key Player Analysis

Leading market participants compete by offering integrated, science-driven solutions across the formulation lifecycle, from preformulation through commercial scale-up. They differentiate via deep expertise in complex small molecules, biologics, and advanced oral and injectable systems, supported by global development and manufacturing networks.

Strategic priorities include investing in AI-enhanced formulation design, expanding continuous manufacturing capabilities, and building specialized platforms for oncology and high-potency compounds. These companies focus on long-term, partnership-oriented models with small and mid-size biopharma clients that require flexible capacity and rapid timelines. Geographic expansion into high-growth regions such as Asia Pacific, coupled with strong regulatory compliance records and robust technology-transfer processes, underpins their competitive positioning.

Top Key Players

- Catalent, Inc.

- Patheon (Thermo Fisher Scientific)

- PCI Pharma Services

- Recipharm AB

- Lonza Group

- Samsung Bioepis

- FUJIFILM Diosynth Biotechnologies

- Parexel International

- Charles River Laboratories

- WuXi AppTec

How is Growth Impacting the Economy?

The expansion of formulation development outsourcing is reshaping the broader healthcare economy by shifting capital from fixed in-house infrastructure to flexible, specialized external capacity. Pharmaceutical and biotechnology firms increasingly leverage contract development and manufacturing organizations (CDMOs) to manage sophisticated solubility, stability, and modified-release challenges, which boosts high-skill employment and investment in advanced labs, analytics, and continuous manufacturing platforms. This growth supports faster commercialization of novel therapies, improving treatment access and creating downstream value in clinical trials, supply chains, and healthcare delivery.

At the same time, regulatory complexity and quality demands generate new business for compliance, validation, and audit services, strengthening ancillary professional services ecosystems. In emerging regions, particularly Asia Pacific, policy incentives and lower operating costs are attracting greenfield outsourcing investments, lifting local GDP contributions, exports, and technology transfer while diversifying global pharma production bases. Overall, the sector acts as an innovation multiplier, amplifying returns on R&D spending and supporting long-term health-economy resilience.

Recent Developments

- Catalent, Inc. (March 2026): Novo Holdings’ USD 16.5 billion takeover of Catalent reached full completion, including clearance of remaining antitrust questions, cementing Catalent’s position as a privately held, large -scale CDMO platform for complex formulation, development and fill-finish services in biologics and small molecules.

- Lonza Group (January 2026): Lonza reported 2025 revenues of CHF 6.5 billion with currency-adjusted growth of about 21.7% and a CORE EBITDA margin above 31%, underlining strong demand for outsourced biologics and complex modality services and giving the company fresh firepower to reinvest in formulation, drug product and advanced therapy capacity.

- WuXi AppTec (WuXi STA / WuXi TIDES) (March 2025): WuXi AppTec highlighted that its Changzhou and Taixing API sites passed US FDA inspections with no observations, while outlining a plan to expand total small-molecule API reactor volume to over 4,000,000 litres by the end of 2025, reinforcing the company’s role as a go-to partner for integrated API and formulation development mandates.

- FUJIFILM Diosynth Biotechnologies (February 2025): The company confirmed that phase one of its Hillerød, Denmark expansion was complete, adding six new mammalian cell bioreactors for a total of 12, and detailed plans for a follow-on USD 1.6 billion investment to bring another 8 bioreactors plus two downstream processing trains online, alongside plans to double the Hillerød biomanufacturing footprint.

Conclusion

The formulation development outsourcing market is set for sustained, innovation-driven expansion as complex pipelines, biologics, and regulatory intensity push sponsors toward specialized external partners. Players that combine deep scientific expertise, AI-enabled design, robust quality systems, and diversified regional footprints will be best positioned to capture long-term value in this rapidly evolving ecosystem.