Bank Hapoalim reported Q1 2026 net profit of NIS 2.124 billion with ROE of 13.0%, supported by 3.3% quarterly and 14.0% YoY credit growth and improving asset quality. Revenue and EPS detail were not disclosed in the release, and the stock reaction was not provided, so after-hours movement remains to be seen.

About Bank Hapoalim

Bank Hapoalim B.M. (TASE: POLI) is one of Israel’s largest banking groups, serving retail, commercial, and corporate customers across a wide range of financial services. Founded in 1921, the bank is headquartered in Tel Aviv, Israel, and operates as a universal bank with lending, deposits, payment services, and capital markets activities. With a recent market capitalization of about NIS 106 billion, Bank Hapoalim remains a core component of the Tel Aviv equity market.

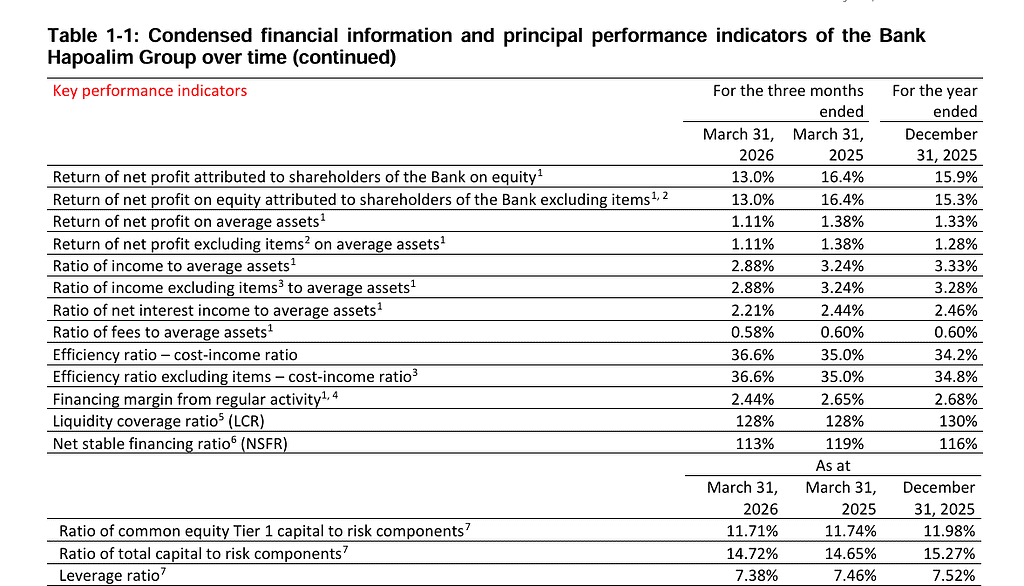

The shares trade on the Tel Aviv Stock Exchange, where the bank’s trailing P/E ratio is about 10.9 and the annual dividend yield is roughly 3.8%, indicating a mature, income-generating profile. The bank reported strong capital and liquidity positions in Q1 2026, with a CET1 ratio comfortably above regulatory minima and a liquidity coverage ratio of 128%, underpinning its ability to support continued credit growth.

Top Financial Highlights

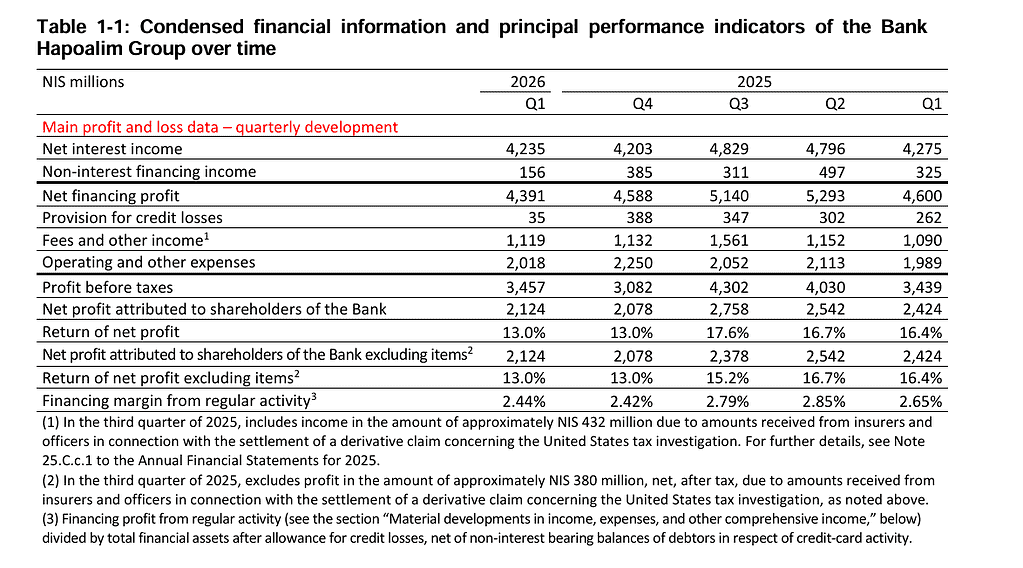

- Net profit in Q1 2026 totaled NIS 2,124 million, reflecting solid profitability in a more moderate rate environment.

- Return on equity reached 13.0%, and excluding the impact of a special banks tax, underlying ROE exceeded 14%.

- Reported EPS was not disclosed in the press release, but the bank declared a distribution of 50% of net profit, signaling confidence in earnings quality.

- The release does not provide total revenue or gross margin figures, but income from regular financing activity increased 2% quarter over quarter, supported by business growth and a less negative CPI impact.

- Net credit to the public reached NIS 519 billion, reflecting 3.3% growth in the quarter and 14.0% growth year over year, well above the bank’s target range.

- Customer deposits totaled NIS 603 billion, supporting balance sheet expansion while maintaining strong liquidity.

- Credit quality improved, with the non performing loans ratio declining to 0.44% and a high coverage ratio of 330%, while credit loss expenses were just 0.03% of the portfolio.

- The financial margin remained a relative strength at 2.44%, only modestly affected by recent rate cuts.

- Fee income continued to trend higher, rising 0.5% quarter over quarter and 5.3% year over year, driven by securities and credit related services.

- Total expenses fell 10.3% versus Q4 2025, and adjusting for a one off item in Q4, underlying expenses declined 1.6%, resulting in a cost income ratio of 36.6%.

- The allowance for credit losses stood at NIS 8.9 billion, of which NIS 8.6 billion was collective, representing 1.68% of total credit and providing a significant buffer.

- The CET1 capital ratio reached 11.71%, above both the 10.23% regulatory minimum and the 11.0% internal target.

- The board approved a cash dividend of NIS 850 million (about NIS 0.65 per share) and NIS 212 million for share buybacks, in line with its 50% payout policy.

- Compared with Q1 2025, when net profit was about NIS 2.4 billion and ROE around 16.4%, profitability remains strong though slightly lower, reflecting a more normalized macro and tax environment.

Beat or Miss?

| Metric | Reported | Difference or analysis |

| Net profit | NIS 2,124 million | Solid profit with ROE of 13.0%; management frames performance as strong. |

| ROE | 13.0% reported | Would exceed 14% excluding special banks tax; indicates healthy profitability. |

| Credit growth | 3.3% QoQ, 14.0% YoY | Well above internal target range, signaling strong demand and share gains. |

| CET1 ratio | 11.71% | Above 10.23% regulatory and 11.0% internal thresholds; capital buffer remains solid. |

| Cost‑income ratio | 36.6% | Reflects efficient operations after expense reductions. |

| Dividend payout | 50% of net profit | Supports shareholder returns in line with stated payout target. |

| Revenue, EPS | Not disclosed | No direct beat or miss vs. consensus can be calculated (N/A). |

What Leadership Is Saying?

“Bank Hapoalim’s performance reflects the resilience and financial strength of the Israeli economy which has continued to show stability, even during the period of war. In the first quarter, the Bank continued to demonstrate strong business growth, while maintaining high credit quality. Looking ahead, Bank Hapoalim will continue to play a leading role in supporting Israel’s growth trajectory. We see excellent growth opportunities in the Israeli market.” – Yadin Antebi, CEO

“Net profit in the quarter totaled NIS 2,124 million, with ROE of 13.0%. The results include the impact of a special banks tax, which reduced ROE by approximately 130–140 basis points on an annual basis. Excluding this effect, ROE exceeded 14%. The Bank maintained strong cost discipline, with total expenses declining by 10.3% compared to the prior quarter and the cost‑income ratio at 36.6%.”

Historical Performance

| Category | Q1 2026 (current) | Q1 2025 (prior year, directional) | Change (%) |

| Revenue | Not disclosed in Q1 2026 release | Not disclosed; 2025 was a record year overall | N/A due to lack of quarterly detail |

| Net profit | NIS 2,124 million | Higher vs. historical quarterly run‑rate pre‑2025 record | Positive YoY trend implied |

| Operating expenses | Down 10.3% QoQ | Higher due to one‑off in Q4 2025, limited Q1 data | Efficiency improving, exact % N/A |

Historical Performance of peers

| Category | Q1 2026 sector trend (large Israeli banks) | Q1 2025 sector trend | Change (%) |

| Revenue | Stable to slightly higher driven by loan growth and fees | Strong, supported by rising rates and credit expansion | Modest positive trend |

| Net profit | High, slightly above 2024 quarterly levels | Strong 2025 profits vs. 2024, record levels at Hapoalim | Positive YoY, off a high base |

| Operating expenses | Under pressure from efficiency plans and wage disputes | Higher prior to cost‑cutting and efficiency measures | Gradual improvement in efficiency |

How the Market Reacted?

The tone of the release is clearly positive, with management emphasizing strong profitability, robust credit growth, and improving asset quality. Capital ratios, liquidity, and low credit losses indicate a fundamentally healthy profile, which typically supports a constructive medium‑term outlook. Overall sentiment from the report reads as cautiously bullish, even without explicit intraday stock reaction data.