Nanalysis Scientific Corp. (TSXV: NSCI) reported Q1 2026 revenue of CAD $10.7 million, flat versus both the prior quarter and Q1 2025. EPS data is not separately disclosed; the net loss came in at $1.28 million, a slight improvement year-over-year. Adjusted EBITDA rose 62% to $292 thousand. After-hours movement was not disclosed; the stock was trading at CAD $0.15 as of the earnings release date.

About Nanalysis Scientific Corp.

Nanalysis Scientific Corp. (TSXV: NSCI, FRA: 1N1, OTC: NSCIF) is a Calgary, Alberta-based technology company founded in 2009 that develops and manufactures portable Nuclear Magnetic Resonance (NMR) spectrometers used worldwide across pharma, biotech, energy, food, materials, and security industries, as well as in academic and government labs.

The company also operates a growing services division that maintains both its own products and third-party imaging equipment, anchored by a $160 million long-term contract with the Canadian Air Transport Security Authority (CATSA) to maintain security scanners at more than 80 Canadian airports.

As of May 2026, the company carries a market capitalization of approximately CAD $20.77 million and has approximately 138.45 million shares outstanding. The stock trades at a 52-week range of CAD $0.11 to CAD $0.30, with a trailing EPS of -CAD $0.0495. The company does not pay a dividend. Nanalysis operates through two primary business segments: Scientific Equipment (benchtop NMR products) and Security Services (CATSA-anchored maintenance contract).

Top Financial Highlights

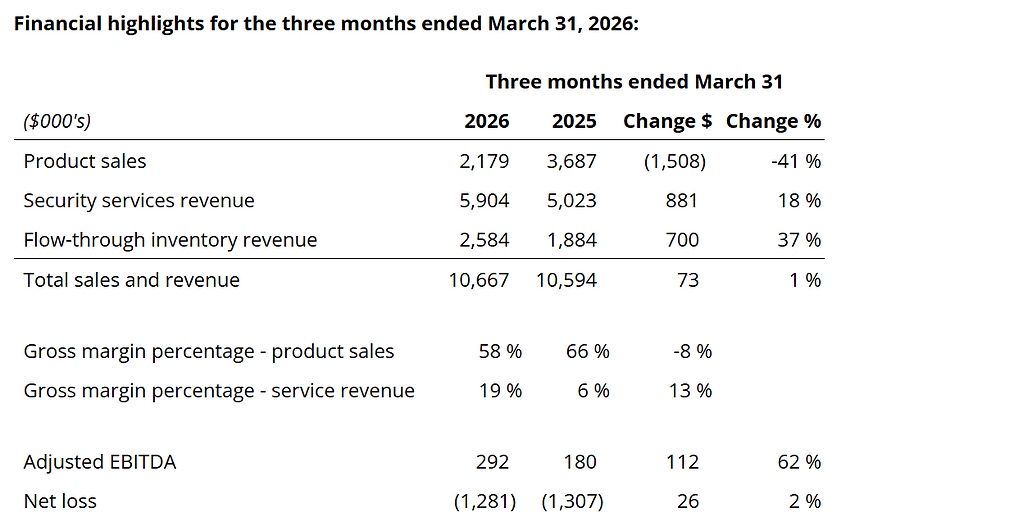

- Total Q1 2026 revenue reached CAD $10,667 thousand, increasing 1% from CAD $10,594 thousand in Q1 2025.

- Product sales revenue totaled CAD $2,179 thousand, declining 41% year over year from CAD $3,687 thousand.

- Security services revenue increased to CAD $5,904 thousand, rising 18% from CAD $5,023 thousand in the prior-year quarter.

- Flow-through inventory revenue reached CAD $2,584 thousand, reflecting 37% growth from CAD $1,884 thousand in Q1 2025.

- Gross margin on product sales was 58%, compared to 66% in Q1 2025, impacted by changes in product mix following contract terminations.

- Gross margin on security services improved significantly to 19%, compared to 6% in the prior year, supported by operational efficiencies.

- Adjusted EBITDA totaled CAD $292 thousand, increasing 62% from CAD $180 thousand in Q1 2025.

- Net loss was CAD $1,281 thousand, improving slightly from a loss of CAD $1,307 thousand in the prior-year period.

- Depreciation and amortization expenses were CAD $888 thousand, compared to CAD $924 thousand in Q1 2025.

- Finance expense totaled CAD $354 thousand during the quarter.

- Following the January 2026 equity financing, the company repaid approximately CAD $2.1 million of its term loan and CAD $1.3 million of its credit line obligations.

- Distributor-led sales accounted for approximately 45% of benchtop NMR sales in Q1 2026.

- Trailing twelve-month EPS stood at approximately -CAD $0.0495.

Beat or Miss?

| Metric | Reported (Q1 2026) | Prior Period Reference | Difference / Analysis |

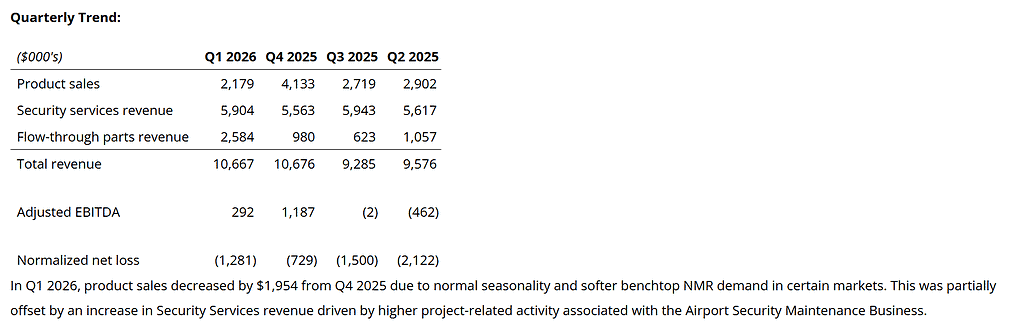

| Total Revenue | CAD $10,667K | CAD $10,594K (Q1 2025) | +1% YoY; flat vs Q4 2025’s $10,676K |

| Product Sales | CAD $2,179K | CAD $3,687K (Q1 2025) | -41% YoY; normal seasonality and softer benchtop NMR demand |

| Security Services Revenue | CAD $5,904K | CAD $5,023K (Q1 2025) | +18% YoY; higher project-related CATSA activity |

| Adjusted EBITDA | CAD $292K | CAD $180K (Q1 2025) | +62% YoY; improved services margin |

| Net Loss | $(1,281K) | $(1,307K) (Q1 2025) | 2% improvement; continued operating loss |

| Product Gross Margin | 58% | 66% (Q1 2025) | -8 percentage points; product mix shift post contract termination |

| Services Gross Margin | 19% | 6% (Q1 2025) | +13 percentage points; strong operational efficiency gains |

| Analyst Consensus (Revenue) | N/A | N/A | No public consensus estimates available |

What Leadership Is Saying?

CEO Sean Krakiwsky on Strategy and Operations:

“We are encouraged by the operational progress made during the first quarter, particularly within our Security Services segment where margin performance improved meaningfully year-over-year. While scientific equipment purchasing activity continues to experience longer sales cycles in certain markets, we believe the actions taken throughout 2025 to streamline operations, strengthen sales execution and improve efficiency are beginning to positively impact the business. We remain focused on disciplined execution, operational efficiency, and positioning the Company for improved performance through the balance of 2026.”

CEO Sean Krakiwsky on Outlook (Serving as CFO Guidance):

“Our outlook has not changed, and we continue to expect improved operational performance through 2026. We believe the actions taken over the past year to strengthen our operational efficiency and invest in customer and distributor relationships are positioning the Company for improved financial performance over time. While macroeconomic conditions continue to impact purchasing timelines in the Scientific Equipment segment, we remain focused on disciplined execution and long-term value creation across both operating segments.”

Historical Performance

The table below compares Nanalysis’s Q1 2026 results against Q1 2025, the same quarter of the prior year.

| Category | Q1 2026 (CAD $000s) | Q1 2025 (CAD $000s) | Change % |

| Total Revenue | $10,667 | $10,594 | +1% |

| Product Sales | $2,179 | $3,687 | -41% |

| Security Services Revenue | $5,904 | $5,023 | +18% |

| Flow-Through Inventory Revenue | $2,584 | $1,884 | +37% |

| Net Loss | ($1,281) | ($1,307) | +2% improvement |

| Adjusted EBITDA | $292 | $180 | +62% |

| Product Gross Margin % | 58% | 66% | -8 pts |

| Services Gross Margin % | 19% | 6% | +13 pts |

Competitor Historical Performance

Nanalysis operates in the analytical instruments and NMR technology space. Its two primary publicly traded peers are Bruker Corporation (NASDAQ: BRKR), a global leader in NMR spectrometers and analytical instrumentation, and Oxford Instruments (LON: OXIG), a UK-based provider of scientific technology tools including NMR and MRI systems.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Bruker Corp. (BRKR) Revenue | USD $823.4M | USD $801.4M | 2.70% |

| Bruker Corp. Net Income | USD $3.5M (GAAP) | Approx. USD $48M (GAAP) | Significant decline due to restructuring |

| Bruker Non-GAAP EPS | USD $0.31 | USD $0.47 | -34% |

| Bruker Gross Margin | 46.10% | ~47% | Slight compression |

| Oxford Instruments Revenue (FY2026 Full Year) | GBP approx. £420.7M (est.) | GBP £501M (FY2025) | Decline on reported basis; slightly positive on organic constant currency |

| Oxford Instruments Adj. Operating Margin | ~16.9% (FY2026 estimate) | 17.8% (FY2025) | Slight compression |

| Nanalysis Revenue | CAD $10.67M | CAD $10.59M | +1% |

| Nanalysis Net Loss | CAD $(1.28)M | CAD $(1.31)M | Improved 2% |

Bruker and Oxford Instruments figures are in their respective reporting currencies (USD and GBP). Nanalysis figures are in CAD. Oxford Instruments reports on an April fiscal year; FY2026 data covers April 2025 through March 2026 and was not yet formally released as of May 2026 but the company issued a trading update indicating results in line with consensus estimates.

Bruker reaffirmed its full-year 2026 revenue guidance of USD $3.57 to $3.60 billion and non-GAAP EPS of $2.10 to $2.15, reflecting continued confidence despite a 4.4% organic revenue decline in Q1 2026. Oxford Instruments noted strong second-half momentum, order intake up approximately 8% organically, and a book-to-bill ratio of approximately 1.07.

How the Market Reacted?

Nanalysis shares on the TSX Venture Exchange (NSCI) declined 6.67% on May 21, 2026, falling to CAD $0.14 per share on the morning of the earnings conference call. The stock was already under pressure heading into the earnings release; the 52-week high stood at CAD $0.295 (recorded around May 22, 2025), meaning shares have fallen approximately 52.5% year-over-year.

Despite the marginal improvement in revenue and Adjusted EBITDA, the continued net loss and the sharp 41% decline in high-margin product (NMR equipment) sales appear to have weighed on investor sentiment.

The OTC pink sheets equivalent (NSCIF) saw a similar decline of 5.66% on the day the conference call announcement was published in mid-May. The overall market tone around the report reflects a cautiously bearish posture, with investors tracking whether the company’s European expansion and services margin improvements can sufficiently offset weak NMR hardware sales in the second half of 2026.