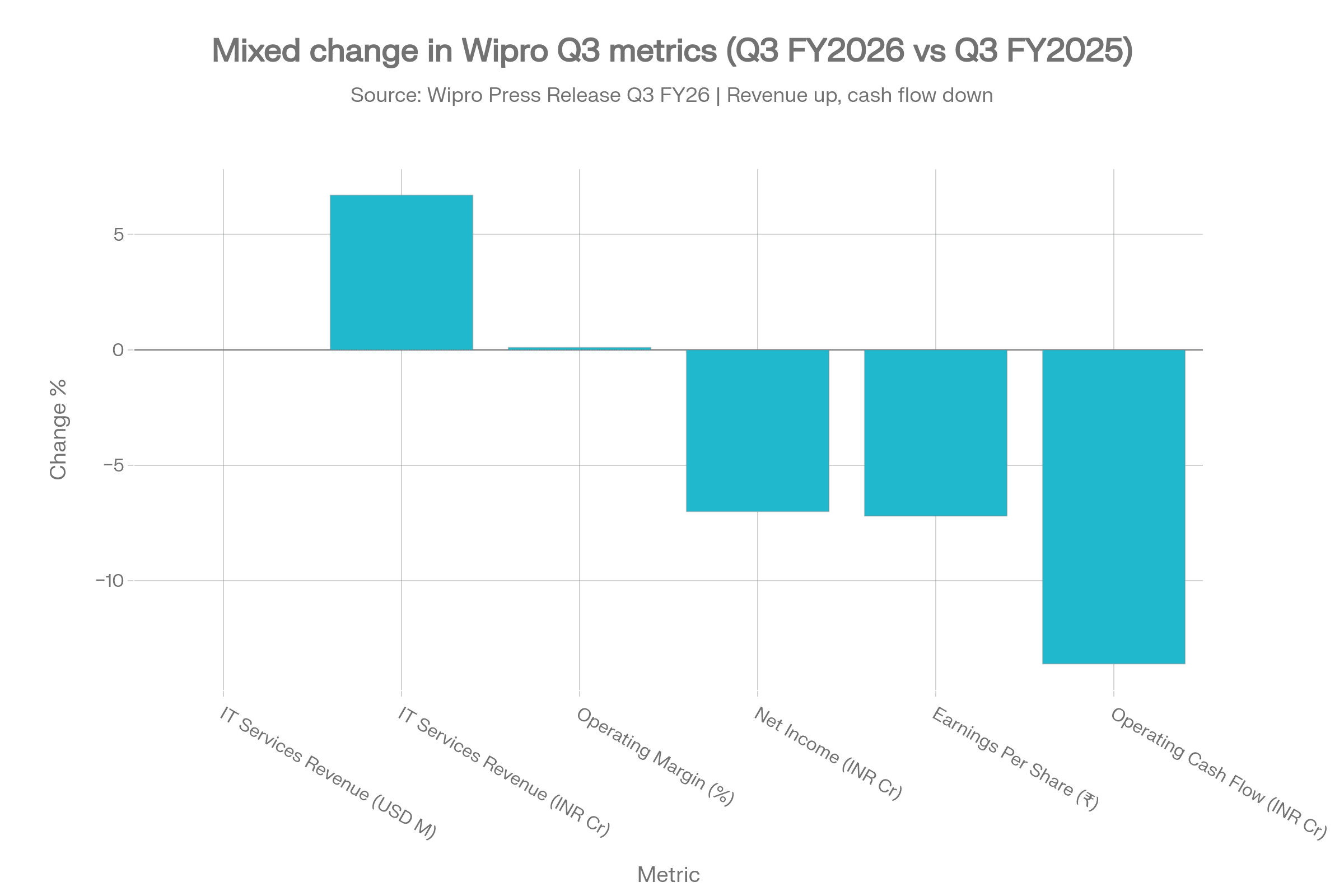

Wipro reported Q3 FY26 revenue of $2,622 million (₹235.6 billion), up 5.5% year-on-year, with operating margins expanding 40 basis points to 17.6%. However, net profit fell 7% YoY to ₹31.2 billion due to a one-time labour code impact of ₹3,028 crore. On an adjusted basis, net income rose 3.6% QoQ, but weak forward guidance of 0% to 2% sequential growth for Q4 disappointed investors, triggering a 7% share price decline.

About Wipro Limited

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO) is a global AI-powered technology services and consulting company headquartered in Bangalore, India, with significant operations in 65 countries. Founded in 1945 as a chemical company and pivoted to IT services in 1980, Wipro is the fourth-largest IT services company in India, trailing TCS, Infosys, and HCL Technologies. As of February 2026, the company holds a market capitalization of ₹2.47 trillion (approximately $27.5 billion USD), with over 230,000 employees and business partners worldwide.

The company operates under a consulting-led service model, leveraging its proprietary Wipro Intelligence™ suite of AI-powered platforms. With a current stock price near ₹242 per share, Wipro trades at a P/E ratio of 19.2x and offers a dividend yield of 4.54%, positioning it as a value play among India’s IT majors despite recent share price weakness.

Key Financial Highlights

- Gross Revenue: $2,622.0 million (₹235.6 billion), increasing 5.5% year-on-year and 3.8% sequentially.

- IT Services Segment Revenue: $2,635.4 million, up 1.2% sequentially and flat year-on-year; constant currency growth of 1.4% QoQ and decline of 1.2% YoY.

- Operating Margin: 17.6%, expanding 90 basis points sequentially and 10 basis points year-on-year—the company’s best margin performance in recent years.

- Net Income: ₹31.2 billion ($347.2 million), declining 3.9% sequentially and 7% year-on-year; adjusted net income (excluding labour code impact) of ₹33.6 billion showed 3.6% sequential growth.

- Earnings Per Share: ₹2.98 ($0.031), down 3.9% QoQ and 7.2% YoY; adjusted EPS of ₹3.21 was flat year-on-year.

- Total Deal Bookings: $3,335 million (down 5.7% YoY); Large Deal Bookings of $871 million (down 8.4% YoY).

- Operating Cash Flow: ₹42.6 billion ($474.1 million), up 25.7% QoQ but down 13.6% YoY; representing a strong 135.4% of net income.

- IT Products Revenue: ₹2.6 billion ($28.6 million).

- Voluntary Attrition: 14.2% on a trailing 12-month basis.

- Dividend Declared: ₹6 per share interim dividend, bringing total payout for FY26 to $1.3 billion.

Performance vs. Expectations

| Metric | Reported | Expected/Consensus | Performance |

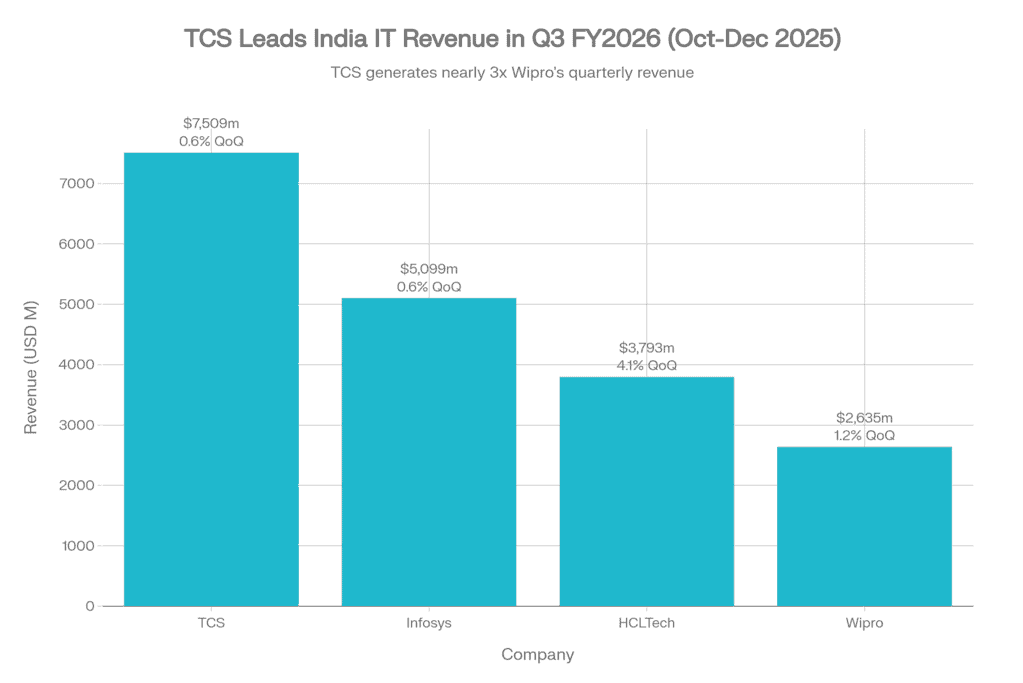

| IT Services Revenue (USD M) | $2,635.4 | $2,640 | Marginally below consensus by ~0.2% |

| Revenue Growth CC (QoQ) | +1.40% | +1.60% | Slightly below estimates |

| Operating Margin | 17.60% | 17.40% | Beat expectations by 20 bps |

| Net Income (₹ Cr) | 31,190 (adjusted: 33,628) | 32,500–33,000 | Below on IFRS basis due to labour code impact |

| Large Deal Bookings (USD M) | $871 | $950–$1,000 | Below pipeline expectations |

| Q4 FY26 Guidance (CC Growth) | 0%–2.0% | 1.5%–2.5% | Cautious guidance disappointed Street |

The company’s revenue performance aligned with internal guidance but fell slightly short of consensus estimates on absolute growth metrics. The strength in operating margins was offset by the disappointment on deal bookings and conservative Q4 forward guidance, which became the primary driver of negative market sentiment.

Leadership Perspectives

“In Q3, we delivered broad-based growth in line with our expectations. As AI becomes a strategic imperative, Wipro Intelligence is emerging as a differentiator and contributed to several wins this quarter. We saw greater adoption of our AI-enabled platforms and solutions, scaled AI-led delivery through WINGS and WEGA, and expanded our innovation network across global locations.” — Srini Pallia, CEO and Managing Director, Wipro Limited

“Our IT services operating margins at 17.6% expanded both sequentially and on a year-on-year basis. This is our best margin performance in last few years. Our continued focus on execution rigour also reflects in our strong operating cash flow of 135% of net income in Q3. We are also pleased to share that the Board has declared an interim dividend of ₹6 per share which will take the total payout for the year to $1.3 Bn.” — Aparna Iyer, Chief Financial Officer, Wipro Limited

Year-on-Year Performance (Q3 FY26 vs. Q3 FY25)

The sequential comparison reveals mixed signals: while IT services revenue remained essentially flat year-on-year in reported terms, the operating margin expanded modestly. The decline in net income and EPS reflects the one-time impact from India’s new labour code amendments, which required companies to recalculate gratuity liabilities retrospectively. On an adjusted basis, excluding the ₹3,028 crore labour code charge, net income growth would have been 0.3% year-on-year, demonstrating the underlying operational resilience but also the headwind from regulatory changes.

Competitive Landscape: Wipro vs. India’s IT Majors

Among India’s top four IT services companies, Wipro faces significant competitive pressure on margins and profitability despite its operational stability. TCS maintains commanding leadership with a 25.2% operating margin and ₹67,087 crore in quarterly revenue, while Infosys and HCLTech have achieved tighter margins. Wipro’s 17.6% operating margin, while expanded from prior quarter, trails peers and reflects execution challenges and a smaller scale relative to TCS. The company’s net margin of 13.2% is the lowest among the four, constrained by higher cost structure and smaller deal size relative to TCS’s $9.3 billion in Q3 TCV versus Wipro’s $3.3 billion.

HCLTech achieved the highest sequential growth at 4.1% (CC basis) during Q3, driven by seasonal strength in its products business and aggressive AI-led modernization wins. Infosys matched Wipro’s sequentially modest growth at 0.6% in constant currency but maintained a higher net margin at 14.7%. TCS, despite facing BSNL headwinds, posted stable growth at 0.6% QoQ and commanding margins, reinforcing its position as the sector’s profit and valuation leader.

Strategic Wins and AI Momentum

Wipro secured 12 significant strategic deal wins during Q3, totaling $3.3 billion in bookings, with a focus on AI-led transformation across multiple industry verticals. Notable wins include:

- Trust & Safety Platform Renewal with a global technology leader, deploying thousands of AI and ML specialists to refine content policies

- Healthcare Insurance Expansion with a US national health insurance organization using Wipro’s proprietary PayerAI solution for member enrollment and intelligent automation

- Enterprise Modernization with a North American household furnishings manufacturer to embed AI at scale and set up Centers of Excellence

- Hybrid Cloud Transformation with a major European insurance provider leveraging AI for observability and automation

- Agentic AI Implementations with global communications and software development lifecycle companies, utilizing Wipro’s WEGA orchestration platform

These wins underscore Wipro’s positioning in the high-growth AI services segment, where annualized AI revenue contribution is expanding. However, the absolute deal value of $871 million in large deals (>$30M) represents an 8.4% year-on-year decline, signalling softer pipeline momentum relative to TCS’s $9.3 billion Q3 TCV.

Analyst Recognition and Market Positioning

Wipro received recognition across 12 major analyst frameworks during Q3 FY26, including positions as:

- Leader in Avasant’s Generative AI Services 2025 RadarView™

- Leader in Gartner® Magic Quadrant™ for Service Integration and Management Services, Data Center Outsourcing Services, and Outsourced Digital Workplace Services

- Leader in Everest Group’s PEAK Matrix® Assessments for ServiceNow Services, Talent Readiness for Data & AI, and Banking Operations

- Leader in IDC MarketScape for Manufacturing Intelligence Transformation

- Leader in ISG Provider Lens™ for AWS Ecosystem Partners

These certifications validate Wipro’s capabilities in AI and cloud services but have failed to translate into margin-leading positioning relative to peers or outsized deal wins.

Segment and Geographic Performance

Wipro’s IT Services revenue breakdown by geographic market in Q3 FY26:

| Region | Revenue (₹ Cr) | YoY Growth (%) | QoQ Growth (%) |

| Americas 1 | 77,809 | 8.10% | 4.00% |

| Americas 2 | 67,708 | -0.60% | 1.00% |

| Europe | 62,405 | 5.20% | 4.80% |

| APMEA | 25,859 | 10.10% | 3.30% |

| Total IT Services | 233,781 | 5.00% | 3.80% |

The Americas region (combined Americas 1 and 2, representing 62% of total revenue) showed divergent trends, with Americas 1 accelerating at 8.1% YoY but Americas 2 contracting 0.6% YoY. Europe posted solid 5.2% YoY growth, and the APMEA region led growth at 10.1% YoY, driven by emerging market demand and India operations. This geographic diversification provides a hedge against regional economic cycles but also masks underlying weakness in the strategic North American financial services and energy verticals within Americas 2.

Forward Guidance and Market Implications

Wipro’s guidance for Q4 FY26 (quarter ending March 31, 2026) is notably cautious:

- IT Services Revenue Guidance: $2,635 million to $2,688 million, representing 0% to 2% sequential growth in constant currency terms

- Exchange Rate Assumptions: GBP/USD at 1.33, EUR/USD at 1.17, AUD/USD at 0.65, USD/INR at 88.85, CAD/USD at 0.72

This flat-to-low growth guidance, following a modest Q3 performance, signals management’s conservative view of demand traction in Q4, traditionally the strongest quarter due to calendar-year-end budget implementations and additional billing days. The guidance range of 0% to 2% CC growth—below Street consensus of 1.5% to 2.5% – suggests either ongoing deal realization challenges, seasonal demand weakness extending beyond typical seasonality, or conservative positioning ahead of potential macro headwinds in Q4 FY26. This cautious stance contrasts with Infosys’s upward revision of FY26 growth guidance to 3%–3.5% (from 2%–3%) and HCLTech’s reaffirmed 4%–4.5% FY26 guidance, both underpinned by stronger deal pipelines and AI momentum.

Labour Code Impact and Margin Sustainability

A significant headwind in Q3 results came from India’s new unified labour code amendments, which required retrospective recalculation of employee gratuity liabilities. Wipro took a one-time charge of ₹3,028 crore ($33.7 million) during Q3, reducing reported net profit to ₹31.2 billion. However, adjusted net income (excluding this impact) rose 3.6% QoQ to ₹33.6 billion, demonstrating underlying operational strength.

The labour code will have a recurring annual impact of approximately 10–15 basis points on operating margins going forward, according to management guidance shared across the industry. This recurring drag on margins, combined with the company’s inability to expand margins beyond the current 17.6% level despite scale investments, raises questions about Wipro’s long-term margin trajectory relative to TCS (25.2%) and Infosys (21.2% adjusted). To sustain margin expansion, Wipro must accelerate AI-led service delivery (through WEGA and WINGS platforms) and shift its mix toward higher-value consulting engagements.

Cash Flow and Capital Allocation

Operating cash flow of ₹42.6 billion represents a strong 135.4% conversion of net income, indicating robust working capital management and cash generation capability despite the profitability headwind. The sequential improvement of 25.7% QoQ in operating cash flow reflects better cash collection and disciplined receivables management, a positive signal for capital return and balance sheet strength.

Free cash flow (defined as operating cash flow minus capex) came in at ₹38 billion for Q3, representing 120.8% of net income, demonstrating capital-light operations. With ₹118.9 billion in cash and equivalents as of December 31, 2025 (versus ₹121.9 billion on March 31, 2025), Wipro maintains a fortress balance sheet with minimal debt. The company’s board approved an interim dividend of ₹6 per share, with the record date set for January 28, 2026, and payment by February 15. This brings the total dividend payout for FY26 to $1.3 billion, representing a 48% payout ratio on FY26 projected earnings.

Workforce Dynamics and Attrition

Voluntary attrition moderated to 14.2% on a trailing 12-month basis, down from elevated levels seen in prior periods but still above the 12% target indicated by management. The company added 5,659 employees during the quarter, reflecting selective hiring aligned with AI transformation initiatives and client delivery requirements. Unlike TCS, which saw headcount reduction of 11,151 in Q3, Wipro maintained hiring discipline while managing wage inflation from the new labour code adjustments. The focus on quality hiring for elite AI engineering talent, similar to peer strategies, underscores the sector-wide shift toward higher-value resource profiles.

Market Reaction and Valuation Implications

Wipro shares declined 7% following the Q3 earnings announcement on January 16–17, 2026, as investors digested the weak guidance and below-consensus deal bookings despite operational margin expansion. The stock has declined approximately 20.7% over the past 12 months as of February 2026, underperforming TCS and broadly tracking Infosys weakness. The current valuation of 19.2x forward P/E (based on FY27 estimates) and 3.5x Price-to-Book ratio places Wipro in the middle range of Indian IT majors, below TCS’s 22.6x P/E but above mid-tier companies like Tech Mahindra at 35x.

The sell-off reflects three structural concerns: (1) margin expansion has stalled relative to TCS’s consistent 25%+ EBIT margins, (2) deal productivity (deal size and TCV) lags competitors despite similar deal count, and (3) weak Q4 guidance suggests demand uncertainty persists into the calendar year 2026 budget cycle when discretionary IT spending typically accelerates. Nomura maintained a Buy rating post-earnings with a ₹290 price target, citing valuation comfort and dividend yield support, but acknowledged that EPS estimates for FY27–FY28 required downward revision due to the labour code recurring impact.

Conclusions

Wipro’s Q3 FY26 results demonstrate operational resilience with revenue growth of 5.5% YoY and margin expansion to 17.6%—the company’s best margin performance in years. However, the narrative is constrained by three headwinds: (1) a 7% year-on-year decline in reported net profit due to labour code amendments, (2) soft deal bookings at $3.3 billion (down 5.7% YoY) signalling slower deal momentum relative to peers, and (3) cautious Q4 guidance of 0%–2% sequential growth, disappointing Street expectations.

The company’s strength in AI-led deal wins, investor recognition in analyst frameworks, and strong cash flow generation (135% of net income) provide confidence in execution and shareholder returns. However, the inability to expand margins beyond 17.6% despite scale and the persistent margin gap versus TCS (25.2%) and Infosys (21.2% adjusted) raises concerns about Wipro’s competitive positioning in a market shifting toward higher-value AI and transformation services.

For investors, Wipro represents a defensive IT services play with stable dividends (4.54% yield) and reasonable valuation, but growth remains subdued relative to peers. The company’s success hinges on accelerating AI-led service delivery productivity and securing larger-deal wins to improve margin mix—critical for re-rating the stock from its current valuation of 19.2x P/E toward the premium multiples commanded by TCS. Management’s guidance for Q4 FY26, combined with FY26 earnings trajectory, will be crucial in determining whether Wipro can execute on AI transformation momentum or faces further valuation compression amid sector-wide competition.