Introduction to the Drug Reference Apps Market

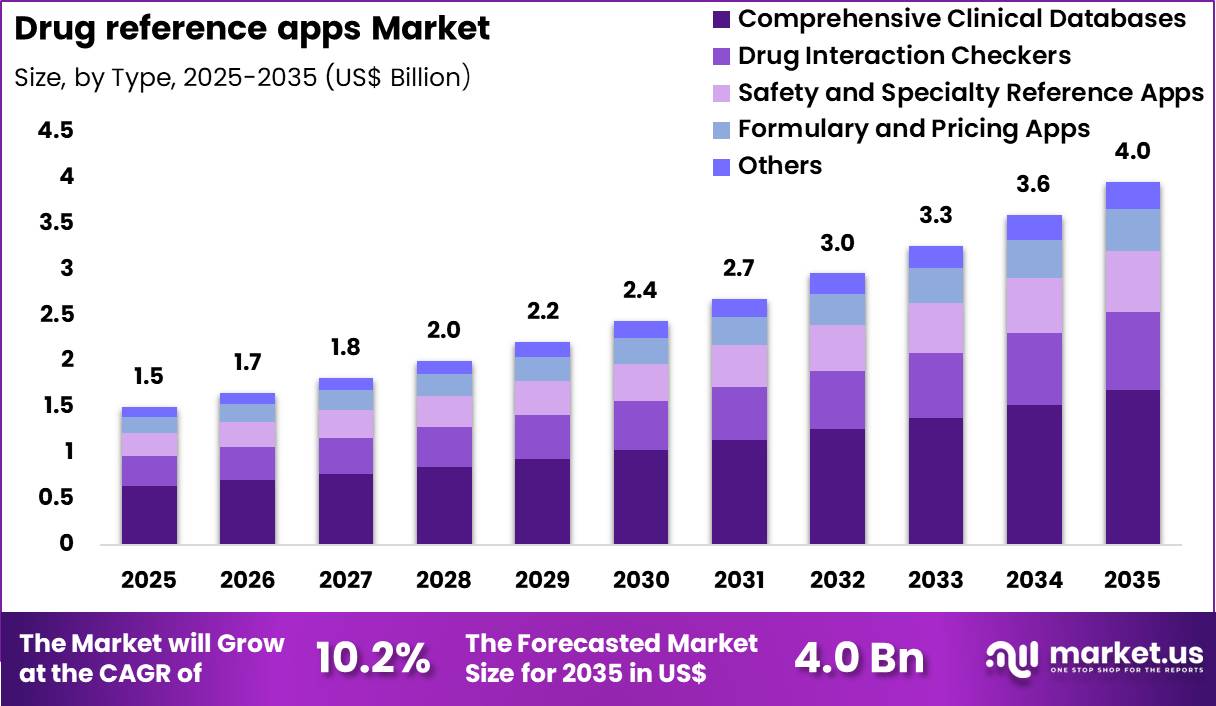

The Global Drug Reference Apps Market is projected to rise from US$ 1.5 Billion in 2025 to about US$ 4.0 Billion by 2035, registering a robust CAGR of 10.2% during 2026–2035. North America currently leads with approximately 41.2% share, reflecting strong digital health maturity and deep electronic health record (EHR) integration. Increasing smartphone penetration, rising polypharmacy, and growing demand for real-time, evidence-based prescribing support are driving adoption among physicians, pharmacists, nurses, and patients. Comprehensive clinical databases command nearly 42.5% of type-based share, underscoring the market’s shift toward all-in-one clinical decision support ecosystems.

Get lastest insights and updates at @ https://market.us/report/drug-reference-apps-market/free-sample/

Key Takeaways

- The market is forecast to grow from US$ 1.5 billion (2025) to US$ 4.0 billion by 2035 at 10.2% CAGR.

- North America currently leads with around 41.2% share, supported by strong EHR integration and digital literacy.

- Comprehensive clinical databases and healthcare professionals are the dominant type and end-user segments, respectively.

- Key growth drivers include rising mobile health adoption, polypharmacy complexity, and focus on reducing medication errors.

- Concerns around data accuracy and reliability, along with macroeconomic pressures, remain major restraints.

- Integration with hospital EHR systems and open-access drug databases present significant new opportunities.

How Growth Is Impacting the Economy ?

Rapid expansion of drug reference apps is reinforcing the broader digital health economy by pushing investments into health IT infrastructure, cloud-based platforms, and interoperable EHR ecosystems. Hospitals and clinics are reallocating budgets toward subscription-based clinical decision support tools that reduce medication errors, thereby lowering downstream costs related to adverse drug events and hospital readmissions. As mobile-first workflows scale, productivity gains for clinicians translate into more efficient patient throughput and optimized resource utilization, especially in high-acuity and telehealth settings.

This market also stimulates job creation in health informatics, clinical content development, cybersecurity, and AI-driven analytics, expanding the knowledge-intensive segment of the healthcare workforce. Macroeconomic pressures like inflation and higher interest rates can temporarily constrain smaller providers’ IT spending, but long-term cost avoidance from safer prescribing sustains structural demand. By fostering data-driven medication management, drug reference apps support healthier populations and more resilient healthcare systems, indirectly bolstering national productivity and economic stability.

Strategies for Businesses

To capitalize on the drug reference apps market, businesses should prioritize evidence-based, continuously updated content validated through collaborations with academic medical centers and regulatory bodies. Integrating apps natively with EHRs, e-prescribing systems, and telehealth platforms is essential to embed decision support into daily clinician workflows. Enterprises can differentiate via AI-powered interaction checkers, personalized risk scoring, and clinical calculators that address complex polypharmacy and specialty therapies.

A tiered SaaS model combining freemium access with premium institutional licenses helps reach both individual practitioners and large health systems. Strong data security, offline capability, multilingual support, and region-specific formularies are vital for global scale. Vendors should also invest in user experience design, voice interfaces, and gamified education modules to drive engagement among trainees and non-specialist users. Continual measurement of impact on prescribing accuracy and medication error reduction will support value-based procurement discussions with payers and providers.

Analyst Viewpoint

From a present-day perspective, the drug reference apps market is transitioning from standalone, consumer-grade tools to enterprise-grade, clinically integrated platforms that underpin safe prescribing and medication management. Usage is especially high in North America and growing steadily in Europe and Asia Pacific, where digital health infrastructure is maturing and telehealth volumes are rising. Despite concerns about app accuracy and uneven data validation, leading vendors are investing heavily in evidence-based content and regulatory alignment, strengthening clinician trust.

Looking ahead, analysts expect double-digit growth through 2035 as smartphone penetration, digital literacy, and AI capabilities accelerate across healthcare systems. Asia Pacific is poised for the fastest CAGR, supported by national e-health initiatives and expanding middle-class demand for mHealth services. Future apps will increasingly feature AI-driven decision support, advanced interoperability with EHRs and wearables, and localized multilingual content, positioning them as core infrastructure for precision prescribing and chronic disease management.

Report Scope

| Report Features | Description |

| Market Value (2025) | US$ 1.5 Billion |

| Forecast Revenue (2035) | US$ 4.0 Billion |

| CAGR (2026-2035) | 10.20% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Comprehensive Clinical Databases (All-in-One), Drug Interaction Checkers, Safety and Specialty Reference Apps, Formulary and Pricing Apps and Others), By End User (Healthcare Professionals, Patients, Pharmacists, Researchers and Educators and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Epocrates, Medscape, Micromedex (Merative US L.P.), PillPack, Pill Identifier & Med Scanner, Mango Health, Drugs.com, MDCalc, Medisafe, MyTherapy, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Regional Analysis

North America remains the leading region, holding around 41.2% of the global drug reference apps market, buoyed by high smartphone penetration, advanced EHR infrastructure, and strong institutional uptake of decision support tools. In the United States, growing use of apps to access health records reflects broader comfort with mobile health utilities that extend naturally to drug information platforms. Europe shows solid growth driven by digital health policies, increasing e-prescribing, and cross-country efforts to standardize medication safety practices.

Asia Pacific is expected to record the highest CAGR through 2035, supported by rapid digital transformation in healthcare, expanding mHealth ecosystems, and rising middle-class adoption in China, India, and Southeast Asia. National e-health programs and interoperability investments are improving integration of apps with hospital IT systems. Latin America and the Middle East & Africa are growing from smaller bases but benefit from rising smartphone ownership, localized language support, and government-backed e-health initiatives, creating long-term upside.

Business Opportunities

The evolving drug reference apps landscape unlocks multiple business opportunities across the health IT value chain. Vendors can develop enterprise-grade SaaS platforms tailored to hospitals, integrated delivery networks, and retail pharmacy chains, emphasizing EHR interoperability, role-based access, and analytics dashboards. There is substantial potential in offering localized, multilingual databases and region-specific formularies for emerging markets in Asia Pacific, Latin America, and the Middle East & Africa.

Open-access databases and collaboration with academic centers create opportunities for sponsored education, clinical trial recruitment, and data-driven research partnerships. App developers can also monetize premium modules such as offline access, advanced interaction engines, AI-based risk scoring, and integration with wearables for adherence tracking. Consulting and implementation services around digital health literacy, workflow redesign, and change management represent adjacent revenue pools for tech and advisory firms.

Key Segmentation

The drug reference apps market is segmented primarily by type and end user, enabling targeted product and go-to-market strategies. By type, offerings include comprehensive clinical databases (all-in-one solutions), drug interaction checkers, safety and specialty reference apps, formulary and pricing tools, and other niche applications. Comprehensive databases currently dominate with about 42.5% share, reflecting clinician preference for integrated content and calculators in a single interface.

By end user, segments span healthcare professionals, patients, pharmacists, researchers and educators, and other stakeholders such as payers and health IT teams. Healthcare professionals account for roughly 41.0% of market share, as physicians, nurses, and allied staff rely heavily on mobile decision support at the point of care. Additional segmentation by region underscores strong demand in North America and fast-growing opportunities in Asia Pacific, while Europe, Latin America, and the Middle East & Africa form important secondary clusters for localization and partnership-driven expansion.

Key Player Analysis

Leading participants in the drug reference apps market are focusing on strengthening clinical content quality, real-time updates, and AI-enhanced functionality to maintain clinician trust and differentiate their platforms. They invest in continuous database curation, regulatory alignment, and integration of sophisticated interaction checkers, dosage calculators, and guideline-linked recommendations. Many providers pursue enterprise subscription models with hospitals, pharmacy chains, and health systems to secure recurring revenue and embedded usage.

Strategically, players are collaborating with academic medical centers, professional societies, and EHR vendors to validate content and integrate seamlessly into clinical workflows. Multilingual capabilities, region-specific formularies, and offline access help unlock emerging markets where connectivity may be inconsistent. By combining robust clinical decision support with user-friendly mobile interfaces and analytics, these companies are building durable competitive moats and long-term contracts across the global drug reference apps ecosystem.

Top Key Players

- Epocrates

- Medscape

- Micromedex (Merative US L.P.)

- PillPack

- Pill Identifier & Med Scanner

- Mango Health

- com

- MDCalc

- Medisafe

- MyTherapy

- Others

Recent Developments

- In September 2025, a major diabetes data and digital health company moved to expand its hospital-based diabetes care capabilities by acquiring a firm specializing in insulin dosing software for inpatient management.

- This acquisition aims to strengthen glucose management for the 30–40% of hospitalized patients who typically require insulin therapy to maintain glycemic control.

- In March 2025, a prominent healthcare information provider integrated its drug reference content into an AI-powered clinical assistant platform to support real-time, evidence-based medication guidance.

- The launch in 2025 of open-access, comprehensive drug databases by academic centers has significantly broadened free, peer-reviewed drug information access for clinicians and researchers globally.

- Regulatory and academic endorsements of these open-access databases in 2025 have accelerated adoption and fostered collaborations to improve usability and search functionality.

Conclusion

The drug reference apps market is evolving into a critical pillar of digital medication management, underpinned by strong growth, EHR integration, and rising mobile health adoption worldwide. Organizations that prioritize evidence-based content, interoperability, and clinician-centric design will be best positioned to capture long-term value as healthcare continues its digital transformation.

Which section of this draft do you want to refine or expand first: growth drivers, regional analysis, or strategies for businesses?