Introduction

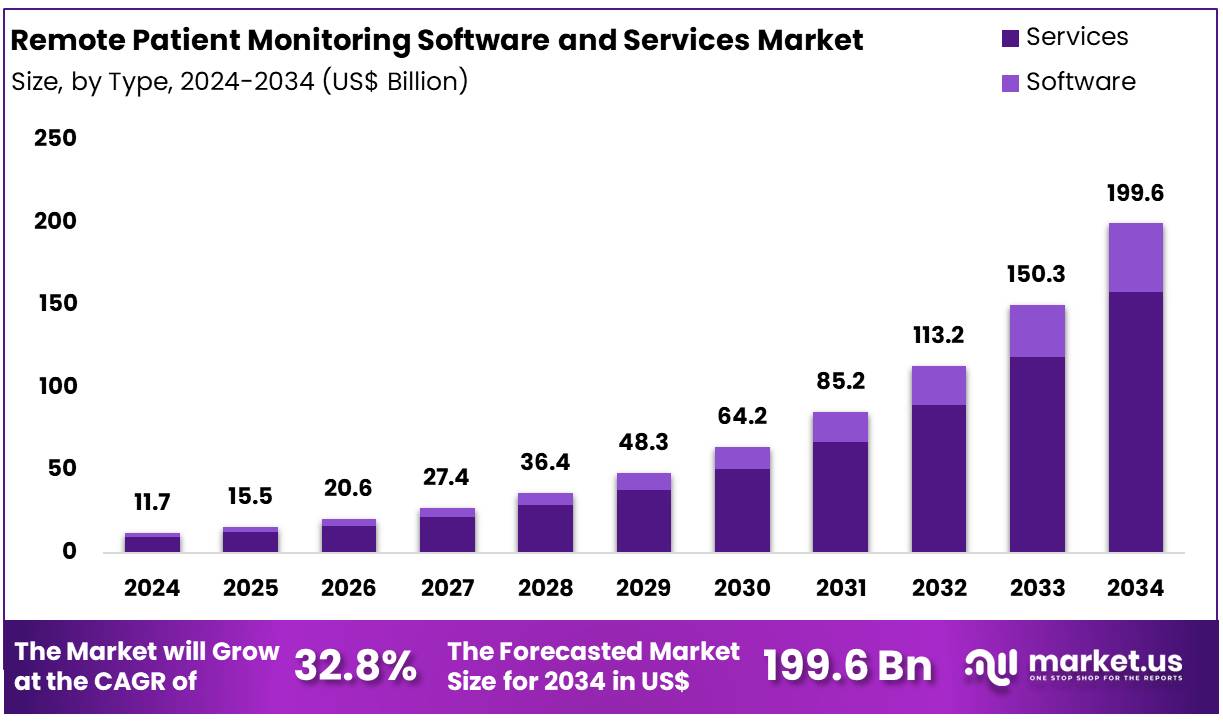

The Global Remote Patient Monitoring (RPM) Software and Services Market is experiencing strong expansion driven by digital healthcare adoption. The market was valued at US$ 11.7 Billion in 2024 and is projected to reach US$ 199.6 Billion by 2034, registering a CAGR of 32.8% during 2025–2034. Services accounted for 79.1% share in 2024, while healthcare providers held 45.6% of total revenue. Cardiovascular applications represented 15.8% share, highlighting growing chronic disease management demand. North America dominated with 48.5% share in 2024, supported by high digital health penetration and regulatory support. Rising demand for cost-effective care and hospital-at-home models continues to accelerate adoption globally.

Get lastest insights and updates at @ https://market.us/report/remote-patient-monitoring-software-and-services-market/free-sample/

Key Takeaways

- The Remote Patient Monitoring (RPM) Software and Services Market is projected to reach US$ 199.6 billion by 2034, increasing from US$ 11.7 billion in 2024.

- The market is expected to expand at a CAGR of 32.8% during the forecast period 2025–2034.

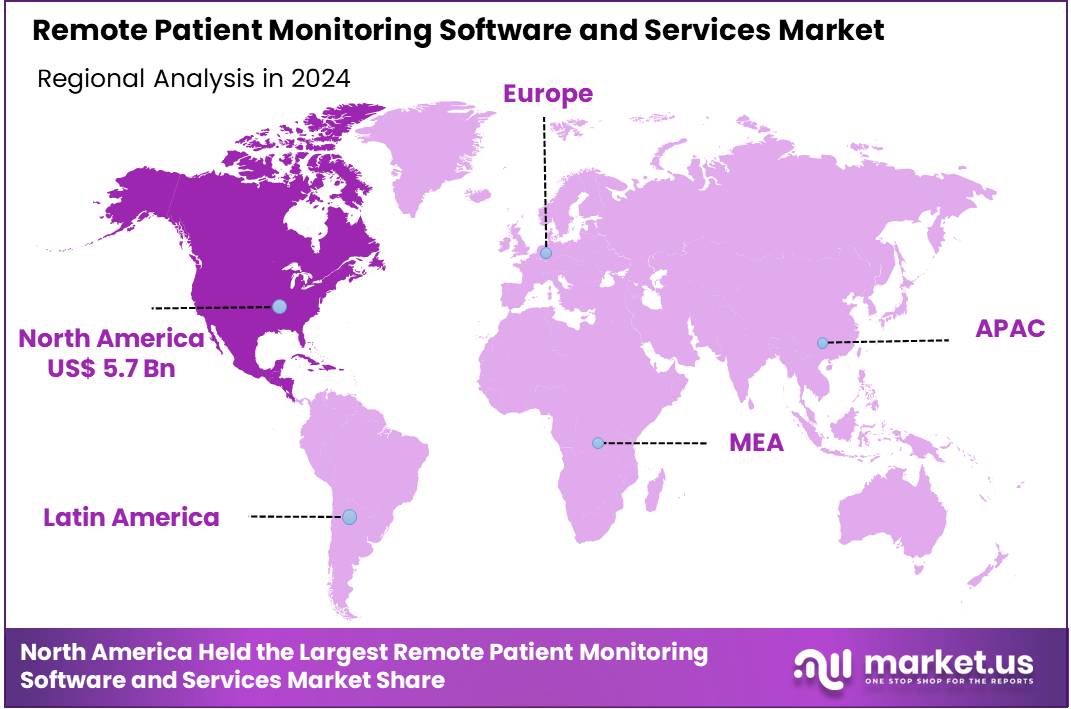

- North America dominated the market in 2024, accounting for over 48.5% share, with revenue reaching US$ 5.7 billion.

- Globally, approximately 1.28 billion individuals aged 30–79 years are living with hypertension, with nearly two-thirds located in low- and middle-income countries.

- Nearly 46% of adults with hypertension remain unaware of their condition.

- Only 42% of individuals with hypertension are diagnosed and receiving treatment.

- According to the International Diabetes Federation (IDF) Diabetes Atlas 2025, around 11.1% of adults aged 20–79, equivalent to 1 in 9 individuals, are living with diabetes, with more than 40% undiagnosed.

- IDF projections indicate that by 2050, approximately 1 in 8 adults, or 853 million people, will have diabetes, representing a 46% increase.

How Growth is Impacting the Economy

Rapid growth in remote patient monitoring software and services is reshaping healthcare economics and broader investment in digital infrastructure. The transition from traditional hospital-based care to home-based monitoring reduces hospitalization costs, improves care efficiency, and optimizes workforce utilization.

Remote monitoring programs significantly reduce emergency visits and hospital readmissions, resulting in measurable cost savings for healthcare systems. Increased integration with electronic health records and telehealth platforms is driving investments in cloud computing, AI analytics, and connected medical devices.

The expanding RPM ecosystem is also stimulating employment across software development, clinical monitoring services, analytics, and remote care management. Healthcare providers are increasingly adopting hospital-at-home models, improving bed utilization and operational efficiency.

The rising prevalence of chronic diseases, such as cardiovascular disorders and diabetes, is further driving the adoption of continuous monitoring systems, thereby improving long-term healthcare productivity. Additionally, payer organizations benefit from reduced claims costs due to early detection and preventive care delivery. Overall, the RPM market contributes to digital transformation in healthcare, enhances accessibility in rural areas, and supports value-based care models that improve the economic sustainability of healthcare systems globally.

Impact on Global Businesses

Rising demand for RPM platforms is increasing investment requirements in cloud infrastructure, cybersecurity, and connected device ecosystems. Businesses must manage higher operational costs associated with data storage, interoperability, and regulatory compliance. Supply chains are shifting toward integrated digital healthcare solutions combining software, analytics, and service delivery models.

Sector-specific impacts are significant across healthcare providers, insurers, and technology firms. Hospitals are investing in remote monitoring dashboards and care coordination platforms, while insurance providers are integrating RPM into reimbursement models.

Technology vendors are expanding device compatibility and AI-based predictive analytics capabilities. Pharmaceutical companies are adopting remote monitoring for clinical trials and chronic therapy management. Home healthcare providers are also expanding remote care services to reduce patient visits and improve operational efficiency. These structural shifts are accelerating digital healthcare convergence across industries.

Analyst Viewpoint

The remote patient monitoring software and services market is currently experiencing accelerated adoption driven by the digital healthcare transformation and the rising chronic disease burden. Integration with electronic health records, telehealth platforms, and AI analytics is strengthening operational efficiency and patient outcomes. The current market landscape shows strong demand among healthcare providers for cost-effective care delivery models.

Future outlook remains highly positive as healthcare systems transition toward value-based care and decentralized monitoring. Increasing adoption of wearable devices, cloud-based platforms, and predictive analytics is expected to enhance clinical decision-making. Expansion of reimbursement policies and remote care infrastructure will further support long-term growth. Continued innovation in real-time monitoring and patient engagement platforms is expected to drive sustained adoption across developed and emerging markets.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 11.7 Billion |

| Forecast Revenue (2034) | US$ 199.6 Billion |

| CAGR (2025-2034) | 32.80% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Software- On-premise, Cloud-based; Services), By Application (Cancer, Cardiovascular Disease, Diabetes, Sleep Disorder, Neurological Disorders, Respiratory Diseases, Mental Health, Others), By End-User (Healthcare Providers- Hospitals, Ambulatory Care Centers, Long-term Care and Assisted Living Facilities, Others; Healthcare Payers; Patients) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Teladoc Health, Inc., Medtronic Plc., GE Healthcare, Siemens Healthineers, Philips Healthcare, Caretaker Medical, OMRON Healthcare, BioIntelliSense, ScienceSoft USA Corporation, Athelas, Biofourmis, iHealth Labs, Oracle, ResMed |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Regional Analysis

North America dominated the global RPM software and services market with 48.5% share in 2024, supported by strong healthcare IT infrastructure and high adoption of digital monitoring technologies. Approximately 50 million users in the United States use remote patient monitoring devices, while 80% of Americans support integrating RPM into healthcare delivery. Europe is witnessing steady growth driven by regulatory support and digital health initiatives.

Asia Pacific is expected to experience rapid expansion due to increasing healthcare digitization, growing chronic disease burden, and expanding telehealth adoption. Latin America and Middle East & Africa are gradually adopting RPM solutions to improve healthcare accessibility and reduce infrastructure gaps.

Business Opportunities

Significant business opportunities are emerging across software platforms, analytics services, and integrated monitoring ecosystems. Demand for cloud-based RPM solutions is increasing due to scalability and real-time data accessibility. Healthcare providers are seeking subscription-based remote monitoring services to reduce operational costs and improve patient outcomes.

Growth in wearable devices and IoT-enabled monitoring systems is creating opportunities for technology vendors. Additionally, remote clinical trials and home-based care programs are expanding addressable market potential. Integration of AI-driven predictive analytics and population health management platforms is further creating value. Emerging markets present opportunities due to rising digital healthcare investments and improving connectivity infrastructure.

Key Segmentation

- Type Analysis: RPM services dominated the market with a 79.1% revenue share in 2024, driven by demand for cost-effective care and continuous monitoring. Services include clinical monitoring, medication management, billing support, and data analytics. Remote therapeutic monitoring and wireless device-based titration improve treatment adherence, medication adjustment, and patient outcomes.

- Application Analysis: Cardiovascular disease accounted for 15.8% market share in 2024, supported by rising mortality and chronic disease prevalence. Telemonitoring adoption is increasing for heart failure management, though concerns remain regarding wearable accuracy, data complexity, and EMR integration, prompting the development of standardized data quality frameworks.

- End-User Analysis: Healthcare providers captured a 45.6% share in 2024, supported by hospital-at-home and post-discharge RPM programs. Studies reported 77% fewer deaths and 87% fewer hospitalizations with remote monitoring. Widespread EHR adoption, including 96% hospitals, enables integration of continuous patient data and coordinated care delivery.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Key Player Analysis

Market participants are focusing on cloud-based monitoring platforms, integrated analytics, and subscription-based service delivery. Companies are investing in AI-powered predictive monitoring and interoperability with electronic health records. Strategic partnerships with hospitals and telehealth providers are expanding service adoption.

Market players are also enhancing device compatibility and remote data management capabilities. Expansion into home healthcare and chronic disease management platforms is a key competitive strategy. Vendors are differentiating through real-time alerts, patient engagement dashboards, and scalable monitoring services. Increasing R&D investment in wearable monitoring and digital therapeutics is further strengthening competitive positioning.

Top Key Players

- Teladoc Health, Inc.

- Medtronic Plc.

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Caretaker Medical

- OMRON Healthcare

- BioIntelliSense

- ScienceSoft USA Corporation

- Athelas

- Biofourmis

- iHealth Labs

- Oracle

- ResMed

Recent Developments

- Medtronic Plc. (March 2026): announced a multi-year renewal and expansion of its global strategic alliance with GE HealthCare to accelerate next-generation patient monitoring, anesthesia, and wearable technologies across hospital environments. The collaboration is intended to enhance integrated clinical workflows and improve real-time patient care delivery.

- Teladoc Health, Inc.(January 2026): highlighted 2026 as an “execution year,” with expanded insurance acceptance for its mental-health platform and increased use of artificial intelligence across virtual care and chronic disease management programs.

- GE HealthCare (November 2025): announced plans to acquire Intelerad for approximately $2.3 billion to expand cloud-based imaging capabilities and strengthen its presence in outpatient enterprise imaging markets, with deal completion expected in 2026.

- Philips Healthcare (October 2025): Entered a strategic collaboration with Hoag Health System to standardize patient monitoring using its EMaaS and PIC iX central monitoring platform, supporting digital transformation across acute care hospitals.

Conclusion

The remote patient monitoring software and services market is experiencing substantial growth, driven by digital healthcare transformation, the rising chronic disease burden, and the increasing adoption of home-based care models. The shift toward value-based care, combined with AI analytics, cloud platforms, and connected medical devices, is improving clinical efficiency and reducing hospitalization costs.

North America maintains leadership, while Asia Pacific is expected to record rapid growth due to expanding digital infrastructure. Service-based RPM solutions continue to dominate, with healthcare providers remaining the primary adopters. Ongoing partnerships, acquisitions, and product innovation by key players are expected to strengthen competitive dynamics and support sustained market growth through 2034.