Introduction

Aston Martin Statistics: Aston Martin walked into 2026 with what feels like one of the most critical stretches in its 113-year history. Even if the British ultra-luxury automaker stays, still, one of those most recognizable performance nameplates around the world, the firm is trying to juggle major financial pressure with an ambitious lineup push led by the Valhalla plug-in hybrid supercar, plus refreshed Vantage and DBX variations, and then more growth in its tailor-made personalization programs.

Even with lower sales quantities and revenue easing off during 2025, management says it expects a real shift toward stronger profitability in 2026. That rebound, they argue, depends on more high-margin cars, a better-tuned product mix, and tighter control of how production is run.

This article explores Aston Martin statistics, including its financial performance, production trends, and position in the global luxury automotive market.

Editor’s Choice

- Aston Martin’s Q1 2026 wholesale volumes held fairly steady at 939 vehicles, down only 1% year over year

- Aston Martin’s global market share sat around 0.006% by volume in 2025

- Revenue rose 16% to £270.4 million (USD 360.4 million), even though vehicle volumes were weaker

- Gross profit jumped 44% to £93.9 million (USD 125.1 million) in Q1 2026

- Gross margin widened from 27.9% to 34.7%, up 680 basis points.

- Operating loss shrank 87% from £67.3 million to £8.9 million (USD 11.9 million).

- Loss before tax improved 18% year over year to £65.5 million (USD 87.3 million).

- Net debt climbed 15% to £1.46 billion (USD 1.95 billion), underscoring the balance-sheet strain that’s still there

- Deliveries of the Specials model went up from 14 units to 103 units, more than a sevenfold increase

- The Americas turned into Aston Martin’s biggest market, with 354 deliveries, up 11%

- The total average selling price rose 17% to £252,000 (USD 335,866) per vehicle.

- Vehicle revenue jumped 16% to £237.8 million (USD 316.9 million).

- Brand and Motorsport revenue surged 72% to £4.3 million (USD 5.7 million).

- Aston Martin is aiming to deliver around 500 Valhalla supercars during FY 2026, to back margin expansion, in the future.

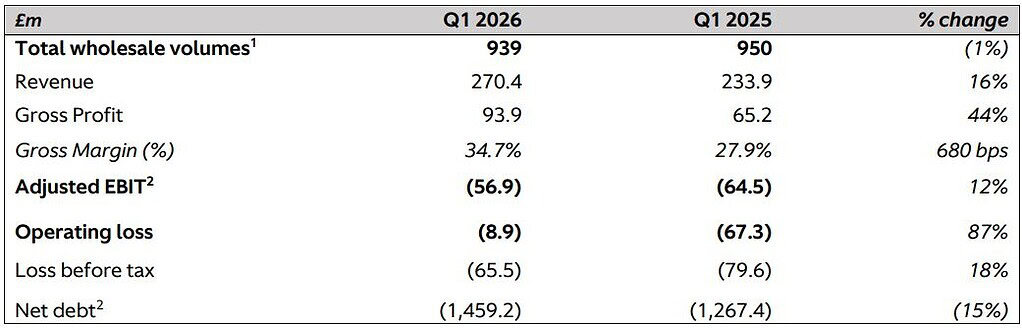

Aston Martin Financial Performance Q1 2026

(Source: astonmartin.com)

- Aston Martin’s first-quarter 2026 results kinda show a clearer picture of operations getting better, even if profitability is still proving difficult.

- The most standout bit is how revenue quality has moved up, and margins have strengthened, while vehicle volumes stay about the same, give or take.

- In Q1 2026, total wholesale volumes came in at 939 vehicles versus 950 vehicles in Q1 2025, so that’s a slight 1% dip.

- Still, revenue went up hard to £270.4 million, from £233.9 million the year before, which is a 16% year over year jump. That sort of suggests higher value sales plus an improved product mix helped to cushion the small drop in units.

- Gross profit also jumped, rising to £93.9 million, compared with £65.2 million in Q1 2025.

- That’s a very solid 44% increase. With that, gross margin moved from 27.9% to 34.7%, an increase of 680 basis points, which points to stronger pricing and better profitability per car sold.

- The operating loss shrank from £67.3 million in Q1 2025 down to £8.9 million in Q1 2026, an 87% improvement.

- Meanwhile, adjusted EBIT improved from –£64.5 million to –£56.9 million, basically meaning losses fell by about 12%.

- Loss before tax followed a similar path, improving from £79.6 million to £65.5 million, which is an 18% improvement year over year.

- Net debt rose to £1.46 billion, up from £1.27 billion a year earlier. That’s roughly a 15% increase, so balance sheet management is still a major watch item for investors and stakeholders.

- The brand delivered 5,448 wholesale units globally in FY 2025, a 10% decline year-over-year against a global light vehicle market of approximately 91.7 million units in 2025.

- Aston Martin’s global market share is roughly 0.006% by volume, a deliberately micro footprint consistent with its ultra-luxury positioning strategy.

- Overall, Q1 2026 shows Aston Martin generating higher revenue, stronger margins, and significantly lower operating losses while maintaining stable sales volumes.

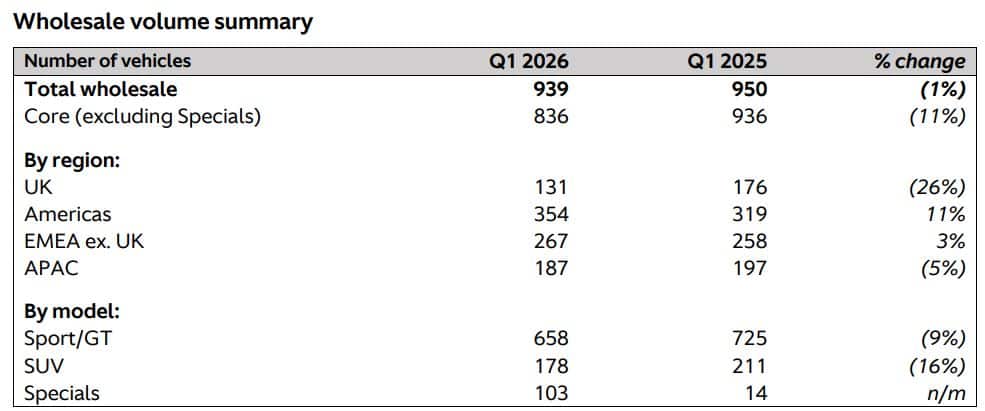

Aston Martin Vehicles Volume

(Source: astonmartin.com)

- Aston Martin kicked off 2026 with a fairly disciplined approach to making and handling inventory, which then showed up in total wholesale volumes of 939 vehicles in Q1 2026. This compares to 950 vehicles in Q1 2025, so you get about a modest 1% decline.

- Even though the overall volumes looked steady, the mix of sales kind of shifted across product categories and regions, in a noticeable way.

- If you look at the core wholesale volumes, meaning excluding Specials, those came in at 836 units, down from 936 units the year before, that’s an 11% decrease.

- The Specials segment, where wholesale deliveries jumped from 14 vehicles to 103 vehicles. It kinda signals that these ultra-exclusive models are taking on a larger share in Aston Martin’s business mix.

- Regionally, performance stayed broad, not all in one place. The Americas ended up as the biggest market with 354 vehicles, up 11% from 319 units in Q1 2025.

- EMEA, excluding the UK, recorded 267 vehicles, increasing 3% year over year. At the same time, the UK market slipped 26% from 176 to 131 units.

- Meanwhile, Asia-Pacific (APAC) volumes fell 5% to 187 vehicles. Together, the Americas and EMEA ex-UK made up roughly 66% of total wholesale deliveries, and it also shows how wide the brand’s international footprint really is.

- Looking at model categories, Sport/GT stayed the largest segment with 658 deliveries, although volumes were down 9% compared to 725 units.

- SUV sales totalled 178 units, down 16% versus 211 units a year earlier.

- The rise in Specials sorta offset those weaker numbers, and it helped improve the overall product mix a bit.

- Looking ahead, Aston Martin keeps stretching its high-performance range, with more deliveries of the DBX S, Vantage S, and DB12 S.

- At the same time, the company is pencilling in about 500 Valhalla units for FY 2026.

- Current Valhalla bookings already run into Q4 2026, which kind of suggests the market really wants what comes next, for these next-generation speed-focused machines.

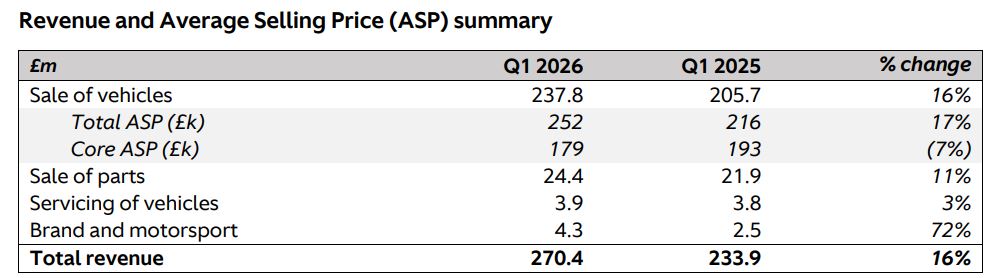

Aston Martin Sales Revenue

(Source: astonmartin.com)

- Aston Martin’s Q1 2026 revenue picture also points to the durability of its premium product approach.

- Even with wholesale volumes that look relatively steady, total revenue reached £270.4 million, up from £233.9 million in Q1 2025. So that’s a pretty clear 16% year over year jump, not bad at all.

- Vehicle sales stayed the main engine here, bringing in £237.8 million, versus £205.7 million a year earlier.

- Alongside that, the company’s overall average selling price, or ASP, climbed to £252,000 per vehicle, from £216,000. That’s 17% higher, and it basically signals more mix coming from higher value derivatives, plus those exclusive special models.

- The core ASP slipped, dropping from £193,000 to £179,000, which is a 7% decline. That suggests the rise in total ASP owes more to the increasing share of ultra-luxury Specials, rather than any broad-based uplift in pricing across the core lineup.

- Beyond just vehicle sales, some of the other income streams were also moving in a positive direction, with some momentum.

- Parts sales climbed to £24.4 million, up 11% compared with £21.9 million. Vehicle servicing revenue ticked higher too, rising 3%, to £3.9 million.

- At the same time, the Brand and Motorsport division really stood out, posting the strongest percentage jump, up 72% from £2.5 million to £4.3 million. This also points to the rising commercial value tied to Aston Martin’s motorsport plus brand-related work.

- The main takeaway is that Aston Martin’s revenue growth is increasingly being powered by product mix and more valuable vehicle categories, rather than trying to grow by volume alone.

- The mix of a 17% higher total ASP, 16% revenue growth, and that 72% growth in brand and motorsport income shows the company’s strategy is working, basically prioritizing value and exclusivity, not just more units sold.

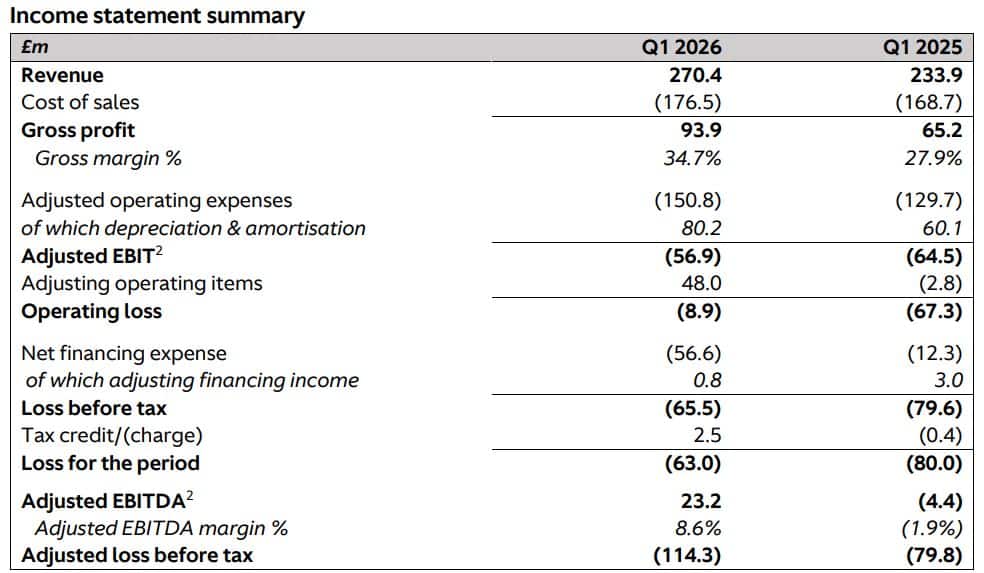

Aston Martin Income Statement

(Source: astonmartin.com)

- Aston Martin saw a notably stronger profit picture in Q1 2026, mostly because higher-value vehicle deliveries came through, and operational efficiency got better too.

- The company is still juggling financing and investment-related pressures, and the financial report makes it clear that revenue quality improved quite a lot despite that.

- Gross profit rose 44% year over year, to £94 million from £65 million in Q1 2025. A big part of that came from more deliveries of high-value Specials models, especially in the Americas.

- The gross margin moved up from 28% to 35%, which is a 7 percentage point jump.

- On the earnings front, Adjusted EBITDA flipped sharply, going from a £4 million loss in Q1 2025 to a £23 million profit in Q1 2026. That’s essentially a positive swing of £27 million.

- Alongside that, Adjusted EBITDA margin also improved, moving from –2% to 9%, which signals better operating effectiveness and stronger profitability per vehicle sold.

- Adjusted EBIT moved in the right direction as well, improving 12% from –£65 million to –£57 million.

- The company’s progress wasn’t clean, because depreciation and amortization got more expensive; those charges climbed 33% to £80 million, versus £60 million in the prior year period.

- The largest financial drag showed up in financing costs. Adjusted net financing costs jumped to £57 million, up from £15 million a year earlier, roughly a 280% increase. Much of this was tied to U.S. dollar debt revaluation effects.

- As a result, adjusted loss before tax widened to £114 million, compared with an £80 million loss in Q1 2025.

- Taken together, the above figures suggest the business is producing stronger margins and a better operating stance, though it still stays heavily exposed to financing costs and other debt-related expenses.

Aston Martin Cash Flows

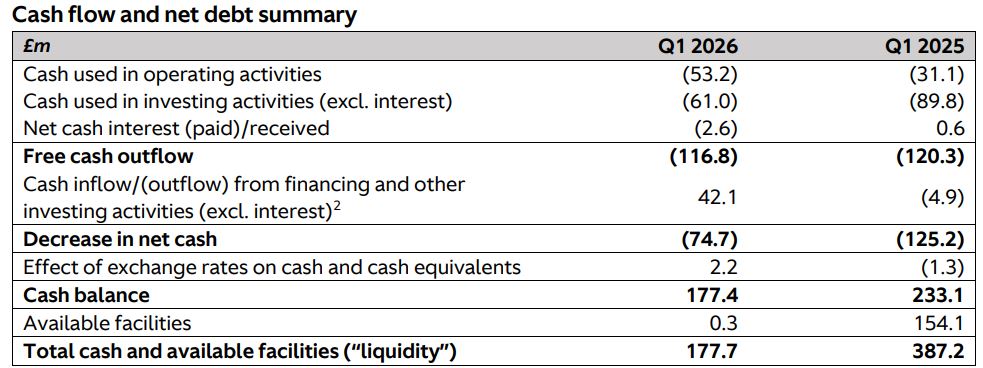

(Source: astonmartin.com)

- Aston Martin’s first quarter 2026 financials show a company still going all-in on future growth, but with a tighter grip on capital spending, kind of, yeah.

- Net cash outflow from operating activities moved to £53 million, versus £31 million in Q1 2025, so that’s a £22 million step down year over year. The main reason seems to be a working capital outflow of £63 million, which is way above the £21 million outflow from the same quarter last year.

- Inventory investment came in as the biggest piece, climbing £42 million against £20 million in Q1 2025, mainly because the company was preparing for higher DB12 S and Valhalla deliveries.

- Receivables were up £14 million, while they had fallen by £6 million in Q1 2025.

- Deposits were down £10 million, too, as Valhalla deliveries actually moved forward.

- To be fair, these cash drains were only partially balanced by a £4 million lift in payables, improving from a £26 million decrease in Q1 2025.

- Even with the working capital pressure building up, Aston Martin reduced capital expenditure to £61 million, down 32% from £90 million in Q1 2025, which points to a more controlled investment stance, aligned with its updated business plan.

- The free cash outflow improved to £117 million, compared with £120 million in the prior- year quarter.

- Liquidity sat at £178 million at 31 March 2026, down from £250 million at the end of 2025.

- All in all, the numbers suggest Aston Martin is still in an investment phase, though lower capex and extra funding support could help it show stronger cash performance during FY 2026.

The Valhalla and Aston Martin’s Adjusted EV Timeline

- Aston Martin’s updated electrification plan seems to be getting less centered on postponing electric cars and more on squeezing the best profitability out of the whole shift phase.

- At first, they talked about bringing out their first battery electric vehicle, or BEV, in 2025.

- Later, that went to 2026, then the schedule stretched again, now it’s basically “before 2030”, and full electrification is being pencilled in between 2035 and 2040.

- Instead of sprinting into a maybe soft luxury EV market, Aston Martin is using the Valhalla plug-in hybrid supercar as a sort of cash bridging tool. It’s limited to 999 units and sits around the USD 1 million mark.

- The setup pairs a 4.0-litre twin-turbo V8 with three electric motors, and the total output lands at 1,079 PS.

- Aston Martin also wholesaled 152 Valhalla units in Q4 2025, which helped push a 47% step up, in total wholesale volumes, on a sequential basis.

- Looking forward, Aston Martin expects roughly 500 Valhalla deliveries across FY 2026, which is more than triple what they delivered during the model’s early production run.

- On top of that, management is guiding gross margins to move into the high-30% zone, versus 29% in FY 2025.

- Management feels this should be a real driver, helping lift gross margins into the high 30% zone, while also giving the company enough financial muscle to back its future electric vehicle plans.

Aston Martin FY 2026 Outlook

- For FY 2026, Aston Martin’s outlook is basically built around one main goal: to improve profitability but keep vehicle volumes steady.

- The company expects overall wholesale deliveries to be broadly flat, roughly 5,448 vehicles, in line with FY 2025. But the twist is that the sales “feel” should be better, thanks to a richer product mix and higher value unit deliveries.

- The planned delivery of around 500 Valhalla supercars across FY 2026, plus a production rhythm that’s more balanced and starts in Q2 2026. These higher ticket vehicles are expected to boost revenue and back margin expansion as the year moves along, not just at the start.

- Aston Martin expects gross margin to climb into the high-30% range, versus 29% in FY 2025.

- That improvement is linked to more efficient manufacturing, a broader stream of derivative offerings, and having Valhalla deliveries in full for the year.

- On top of that, Aston Martin has also toned down its long-term capital investment programme to £1.7 billion across FY 2026 to FY 2030, against the prior £2.0 billion target.

- After a £410 million free cash outflow in FY 2025, management is looking for a noticeable improvement in FY 2026, and most of the annual cash outflow is already expected to happen in Q1 2026.

- Net interest costs are forecast to stay near £150 million.

- Even with outside uncertainties like U.S. tariffs, trade quotas, and general economic swings, Aston Martin’s outlook seems to point to a year that leans into higher-margin products, less capital intensity, and a slow but steady move back toward sustainable profitability.

Conclusion

Aston Martin kicked off 2026 with improving profitability really being the main point, more mix tuning than just chasing more units, yes, volume growth. In Q1 2026, the group showed real momentum, higher revenue, better margins, and operating losses that shrank a lot, even while wholesale volumes stayed almost flat. The rise of those ultra-exclusive Specials, the average selling price moving up, and an improving EBITDA picture really do suggest the luxury-first approach is working.

Still, debt levels are higher, and financing costs keep creeping, so those are the big headaches. Going forward, the Valhalla supercar debut, disciplined capex, and a goal for gross margins in the high 30% band give Aston Martin a path toward a more gradual upswing and firmer financial results during all of 2026.

FAQ

Aston Martin delivered 939 wholesale vehicles in Q1 2026, down 1% compared with Q1 2025.

The firm generated £270.4 million in revenue, which is up 16% year on year.

Average selling price rose 17% to around £252,000 per vehicle.

Aston Martin expects to deliver roughly 500 Valhalla plug-in hybrid supercars across FY 2026.

The company is looking for steady volumes, gross margins in the high-30% range, reduced capital spending, improved cash flow, and continued progress toward profitability.