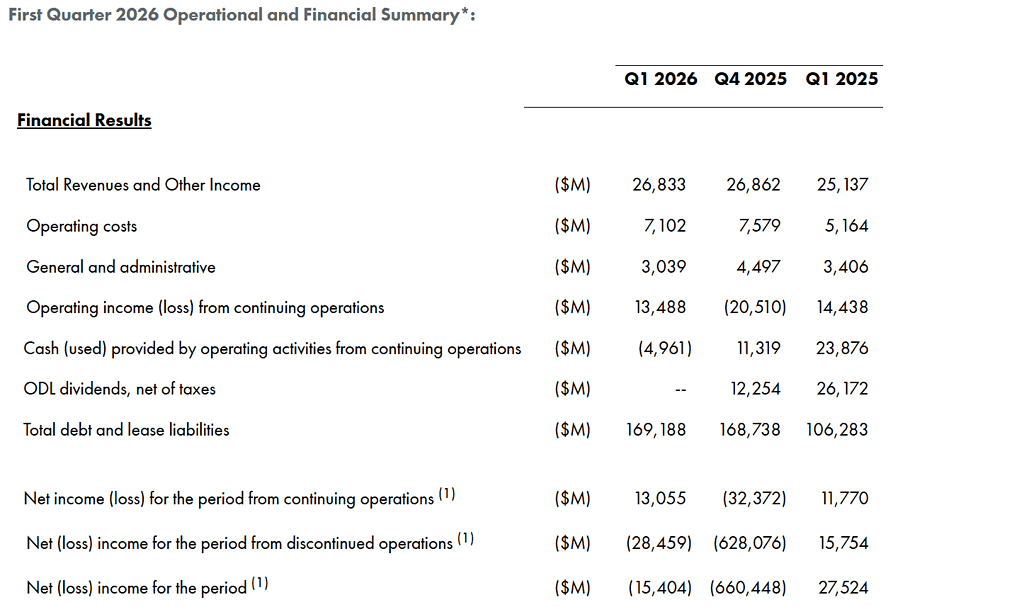

Frontera Energy Corporation reported Q1 2026 total revenues and other income of $26.8 million from its continuing infrastructure operations, with net income from continuing operations of $13.1 million and diluted EPS of $0.18. Adjusted EBITDA reached $28.5 million, showing resilient cash generation as the company pivots to a pure-play infrastructure model.

Shares have rallied sharply in recent months on the pending Parex asset sale, with the stock around the mid‑teens in Canadian dollars and a market cap near CAD 950–980 million; after-hours movement around this specific release is not disclosed, so stock reaction is best characterized as aligned with the already bullish rerating into the closing of the Parex transaction.

About Frontera Energy Corporation

Frontera Energy Corporation (TSX: FEC, OTCQX: FECCF) is a Canadian public company focused on energy infrastructure and related investments in South America. The company is headquartered in Calgary, Alberta, and has historically combined upstream oil and gas operations in Colombia and Guyana with midstream assets such as the Puerto Bahía port and the ODL crude oil pipeline in Colombia.

Following shareholder approval of a plan of arrangement with Parex Resources to divest its Colombian E&P assets for $750 million in enterprise value, Frontera is repositioning as a standalone infrastructure platform anchored by its 35% interest in the ODL pipeline and 99.97% interest in Puerto Bahía. As of early May 2026, Frontera’s equity value is in the CAD 950–980 million range, implying a market cap around ₹71.5 billion and reflecting strong investor anticipation of the asset sale and capital return.

The company generated approximately $77 million of infrastructure distributable cash flow in 2025 and reported last‑twelve‑months infrastructure distributable cash flow of $51.1 million to March 31, 2026, illustrating the cash-generative nature of its core assets. Frontera employs about 857 people across its operations and remains committed to safety and responsible environmental and social practices.

Top Financial Highlights

- Total revenues and other income from continuing operations were $26.8 million in Q1 2026, broadly flat versus $26.9 million in Q4 2025 and up from $25.1 million in Q1 2025.

- Port revenues at Puerto Bahía were $12.7 million versus $12.8 million in Q4 2025 and $10.0 million in Q1 2025, driven by strong general cargo volumes.

- Net income from continuing operations was $13.1 million, up from $11.8 million in Q1 2025, supported by operating income of $13.5 million and $6.8 million of foreign exchange income.

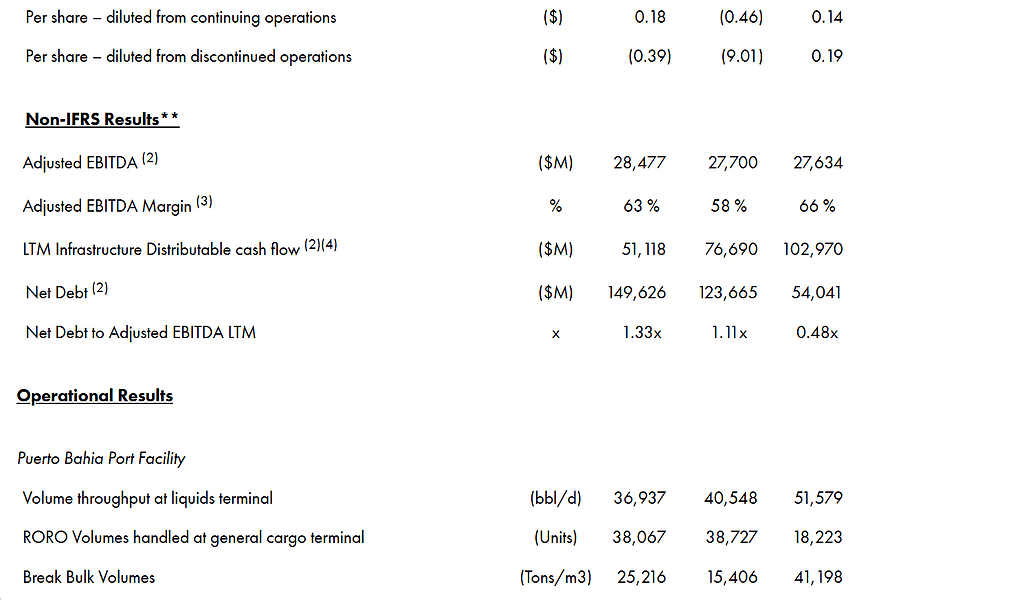

- Diluted EPS from continuing operations came in at $0.18, compared with $0.14 in Q1 2025, reflecting the improved bottom line.

- Net loss from discontinued operations (Colombian E&P assets) was $28.5 million, versus net income of $15.8 million a year earlier, leading to a total net loss for the period of $15.4 million.

- Adjusted EBITDA from continuing operations was $28.5 million, modestly above $27.7 million in Q4 2025 and $27.6 million in Q1 2025, with an Adjusted EBITDA margin of 63% versus 66% in Q1 2025.

- Adjusted revenues (port plus ODL revenue attributable to Frontera) were $45.0 million, up from $42.1 million in Q1 2025.

- Adjusted operating costs were $11.8 million, higher than $9.4 million a year ago, reflecting increased maintenance and higher operating activity.

- Adjusted general and administrative expenses were $4.8 million, slightly below $5.1 million in Q1 2025, indicating some cost discipline.

- ODL net income (100%) was $40.5 million, with ODL EBITDA at $74.2 million; Frontera’s share of income from ODL was $14.2 million.

- ODL volumes transported averaged 233,875 bbl/d, slightly below 236,387 bbl/d in Q1 2025, while the average transportation tariff remained around $4.70 per barrel.

- Puerto Bahía’s RORO volumes rose to 38,067 units, up about 109% year over year, and containers handled increased to 3,851 TEUs from 1,256 TEUs in Q1 2025, underscoring strong general cargo growth.

- Total operating costs at the port were $7.1 million in Q1 2026 versus $5.0 million in Q1 2025, mainly due to higher maintenance and higher operating volumes.

- Capital expenditures from continuing operations were low at $1.0 million, down from $2.1 million in Q1 2025, reflecting a disciplined capital allocation approach.

- Total debt and lease liabilities were $169.2 million, with net debt of $149.6 million, and management expects long‑term debt to decline to about $131 million by year‑end 2026 through scheduled amortizations and cash sweeps.

- The company expects an “expected post-closing cash balance” of approximately $50 million after the Parex transaction, alongside the planned return of up to $470 million of capital to shareholders.

Beat or Miss?

There is no explicit mention of analyst EPS or revenue consensus for Q1 2026 in the press release; external sites track historical EPS but do not yet show a clear Q1 2026 consensus, so comparison is necessarily qualitative.

The results were broadly stable, with modest year‑over‑year revenue and adjusted EBITDA growth in the infrastructure business and stronger general cargo activity, suggesting operational performance at or slightly above typical expectations for these assets. Given the large strategic transaction with Parex, investor focus is likely more on deal execution, capital returns and de‑leveraging trajectory than on marginal quarterly variances.

Reported vs. Expected (Qualitative)

| Metric | Reported (Q1 2026) | Difference/Analysis |

| Total revenues & other income | $26.8 million | No published consensus in release; essentially flat QoQ and up YoY, seen as steady. |

| Net income from continuing ops | $13.1 million | Higher than Q1 2025; supports thesis of resilient infrastructure cash flows. |

| Diluted EPS (continuing) | $0.18 | No explicit consensus; improvement vs. $0.14 YoY appears constructive. |

| Adjusted EBITDA | $28.5 million | Up modestly YoY; margin still strong at 63% despite higher costs. |

| ODL dividends (2026 declared) | $64.7 million | Above $52.9 million in 2025; supportive for future distributions. |

| LTM infrastructure distributable CF | $51.1 million | Down vs. prior periods due to timing of distributions, not operations. |

What Leadership Is Saying?

“In the first quarter of 2026, Frontera delivered solid infrastructure performance, supported by contributions from Puerto Bahía and our equity interest in ODL, which generated an Adjusted EBITDA for the quarter of $28.5 million. Additionally, Frontera expects to receive, proportional to the Company’s 35% equity interest in ODL, approximately $65 million in dividends in 2026.” – Orlando Cabrales, Chief Executive Officer, Frontera Energy Corporation

“Frontera achieved an important milestone with shareholder approval of the plan of arrangement and return of capital, related to the sale of its Colombian E&P asset to Parex Resources. Subject to closing, the Company expects to return up to $470 million to shareholders, representing a substantial return of capital, while retaining approximately $50 million of cash to support the growth opportunities of its high‑quality infrastructure business.” – Gabriel de Alba, Chairman of the Board of Directors, speaking to strategic and capital allocation priorities

Historical Performance

The company now presents results with Colombian E&P assets as discontinued operations, so the core YoY analysis centers on continuing infrastructure operations: revenues, income and expenses tied to Puerto Bahía and ODL. Key metrics show stable to slightly higher revenues and adjusted EBITDA, alongside higher operating costs from increased activity and maintenance.

Frontera – Q1 2026 vs Q1 2025

| Category | Q1 2026 (Continuing) | Q1 2025 (Continuing) | Change (%) |

| Total revenues & other income | $26.8 million | $25.1 million | ≈ +6.8%, driven mainly by port growth. |

| Net income from continuing ops | $13.1 million | $11.8 million | ≈ +11%, aided by FX income. |

| Operating income (continuing) | $13.5 million | $14.4 million | ≈ −6%, as higher costs offset revenues. |

| Adjusted EBITDA | $28.5 million | $27.6 million | ≈ +3%, with a still‑high 63% margin. |

| Port revenues | $12.7 million | $10.0 million | ≈ +26%, on stronger RORO/containers. |

| Port operating cost | $7.1 million | $5.0 million | ≈ +42%, due to maintenance and volume. |

For completeness, discontinued operations (Colombian E&P) swung from a $15.8 million profit to a $28.5 million loss, driven by one‑time impacts and the reclassification associated with the Parex transaction, resulting in a consolidated net loss of $15.4 million in Q1 2026 versus net income of $27.5 million a year earlier.

How the Market Reacted?

The Q1 2026 numbers themselves were steady and largely in line with the company’s recent run‑rate, so market attention has been focused on execution of the Parex transaction and the sizeable planned capital return of up to $470 million rather than on quarterly variances. In the weeks leading up to and around the announcement, Frontera’s share price climbed into the mid‑teens in Canadian dollars, implying a near‑doubling versus levels seen in 2025 and pushing market capitalization toward CAD 950–980 million, which suggests that investors broadly endorse the strategic repositioning and de‑leveraging trajectory.

The earnings release itself does not specify intraday or after‑hours price moves, so we can characterize the immediate reaction as embedded within an already bullish rerating trend driven by the Parex deal and infrastructure‑only future. Overall sentiment appears constructive, with the market rewarding the clearer infrastructure focus and strong cash‑return narrative despite headline net losses from discontinued operations.