Infosys reported adjusted EPS of ₹18.53 (surpassing expectations) with $5.1B in revenue, driven by $4.8B in large deal wins. Despite one-time labour code provisions impacting reported profits, the company raised full-year FY26 revenue guidance to 3.0%-3.5%, signaling strong underlying demand. Stock surged 5.45% domestically and 8.6% in US ADR trading, rewarding the company’s AI-led positioning and robust deal momentum.

About Infosys

Infosys Limited (NSE: INFY, BSE: INFY, NYSE: INFY) is India’s second-largest information technology services company, headquartered in Bengaluru. Founded in 1981 by N.R. Narayana Murthy and colleagues, Infosys has evolved into a global leader in next-generation digital services and consulting. With a market capitalization of approximately ₹6.87 trillion ($87 billion USD) as of early February 2026, and over 330,000 employees serving clients across 63 countries, the company specializes in enterprise transformation driven by cloud, AI, and digital innovation. The company trades at a P/E ratio of 23.34 and offers a dividend yield of 2.72%, reflecting strong shareholder returns despite recent market corrections that have reduced the stock price approximately 11% over the past year. Infosys Topaz, the company’s AI-first platform, has become central to its value proposition, positioning the organization as a strategic transformation partner for enterprises navigating digital and AI-powered change.

Top Financial Highlights

Q3 FY2025-26 Performance:

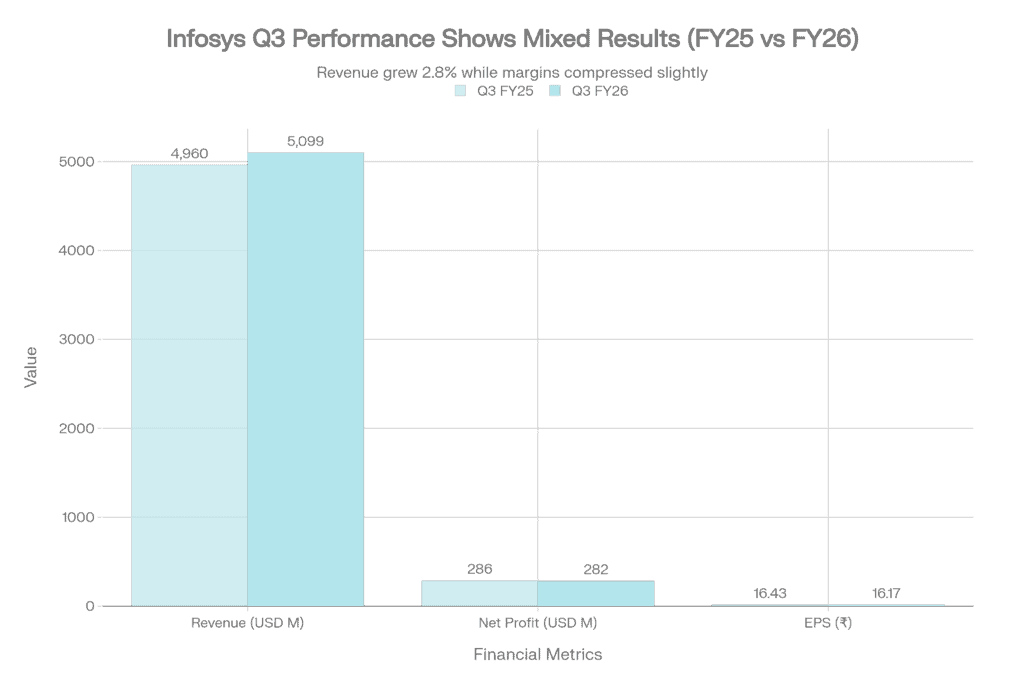

- Revenue: $5,099 million (₹45,479 crore), up 8.9% year-on-year on a reported basis, reflecting strong growth despite currency headwinds.

- Constant Currency Revenue Growth: 1.7% YoY and 0.6% QoQ, indicating cautious global demand environment.

- Reported Operating Margin: 18.4% (IFRS basis); Adjusted Operating Margin: 21.2% (+0.2% QoQ), benefiting from operational leverage.

- Reported Net Profit: ₹6,654 crore (~$282 million); impacted by ₹1,289 crore provision for new labour code obligations.

- Adjusted Net Profit: ₹7,625 crore (~$325 million), reflecting true operational performance without one-time charges.

- Reported EPS: ₹16.17; Adjusted EPS: ₹18.53 (surpassed consensus estimate of ₹16-18 range).

- Free Cash Flow: ₹8,176 crore ($915 million), with Adjusted FCF: ₹8,626 crore at 113.1% of adjusted net profit.

- Large Deal Total Contract Value (TCV): $4.8 billion with 57% net new business, significantly exceeding quarterly expectations.

- Headcount Growth: +5,043 employees, bringing total workforce to 330,000+ employees globally.

- Cash and Equivalents: ₹19,915 crore as of December 31, 2025 (down from ₹24,455 crore as of March 31, 2025), reflecting capital deployment through ₹18,000 crore share buyback.

Nine-Month YTD (Apr-Dec 2025) Cumulative Performance:

- Revenue Growth: 2.8% YoY in constant currency, demonstrating consistent, albeit moderate, growth trajectory

- Reported Operating Margin: 20.0% (IFRS); Adjusted Operating Margin: 21.0% (excluding labour code adjustments)

- Operating Cash Flow: ₹27,157 crore with Adjusted FCF: ₹25,836 crore at 117.8% of adjusted net profit

- YTD Basic EPS: ₹50.64 (reported); Adjusted Basic EPS: ₹52.99, up 6.6% and 11.5% respectively YoY

Beat or Miss?

| Metric | Reported | Estimate/Prior | Analysis |

| Revenue ($) | $5,099M | $5,080M consensus | Beat – Exceeded analyst expectations by $19M; constant currency growth modest at 1.7% YoY, reflecting selective global IT spending |

| Adjusted EPS (₹) | ₹18.53 | ₹16-18 range expected | Beat – Surpassed consensus estimate range; adjusted basis strips ₹1,289 crore one-time labour code provision, revealing stronger core operations |

| Operating Margin (Adjusted) | 21.20% | 21.0% expected | Inline – Achieved guidance midpoint; +0.2% QoQ expansion demonstrates margin resilience despite wage inflation |

| Large Deal TCV | $4.8B (57% net new) | $4.0-4.5B typical range | Beat – Substantially exceeded typical quarterly bookings; 57% net new component indicates strong pipeline replenishment and market share gains |

| Free Cash Flow | $915M reported ($965M adjusted) | ~$850-900M typical | Beat – Strong conversion at 113.1% of adjusted net profit, exceeding historical average and reflecting operational efficiency |

| Guidance Revision | FY26: 3.0%-3.5% CC growth | Prior: 2.5%-3.0% | Upside – Raised guidance 50 bps midpoint, signaling increased confidence in H2 FY26 demand momentum driven by AI services traction |

Leadership Perspectives

“Infosys delivered a strong Q3 performance demonstrating how our differentiated value propositions in enterprise AI, through Infosys Topaz, are consistently driving higher market share. Clients increasingly view Infosys as their AI partner with demonstrated expertise, innovation capabilities and strong delivery credentials. This has helped them unlock business potential and enhanced value realization. Central to this journey is our commitment to reskill, transform and empower our dedicated human resource pool to drive success in an AI augmented world.” – — Salil Parekh, Chief Executive Officer and Managing Director, Infosys

“Our performance was broad-based in Q3 with 0.6% sequential revenue growth, 0.2% adjusted operating margin expansion, stellar large deal wins at $4.8 billion and robust adjusted free cash generation at $965 million in a seasonally weak quarter. In line with our capital allocation policy, we successfully completed the largest ever buyback of ₹18,000 crore and paid out interim dividend to shareholders.” — Jayesh Sanghrajka, Chief Financial Officer, Infosys

Q3 FY26 Performance Metrics (Infosys vs. Expectations)

Historical Performance: Infosys Q3 YoY Comparison

| Metric | Q3 FY26 | Q3 FY25 | Change (%) | Interpretation |

| Revenue (USD) | $5,099M | $4,960M | +2.80% | Solid YoY growth in absolute terms; constant currency growth of 1.7% reflects currency translation gains on reported basis |

| Revenue (INR) | ₹45,479 Cr | ₹41,764 Cr | +8.90% | INR depreciation significantly boosted reported growth; underlying operational growth more subdued |

| Net Profit | ₹6,654 Cr | ₹6,806 Cr | -2.20% | Reported profit declined due to ₹1,289 Cr labour code provision; adjusted basis shows +12.0% growth, indicating stronger underlying profitability |

| Adjusted Net Profit | ₹7,625 Cr | ₹6,806 Cr | +12.00% | Strong operational profit growth; demonstrates benefit of reskilling investments and AI service expansion |

| Operating Margin (Reported) | 18.40% | 21.30% | -290 bps | Decline entirely attributable to one-time labour code adjustment; adjusted margin demonstrates margin stability |

| Operating Margin (Adjusted) | 21.20% | 21.30% | -10 bps | Essentially flat YoY, reflecting balanced headwind (wage inflation) and tailwind (AI service premiums and operational leverage) |

| EPS (Reported) | ₹16.17 | ₹16.43 | -1.60% | Minimal impact to EPS despite significant provision, due to tax benefit and lower share count from buybacks |

| EPS (Adjusted) | ₹18.53 | ₹16.43 | +12.80% | Robust earnings growth; demonstrates core business strength and capital management discipline |

| Free Cash Flow | ₹8,176 Cr | ₹10,647 Cr | -23.20% | Reported FCF declined; reflects timing of capital deployment; adjusted FCF of ₹8,626 Cr still strong at 113.1% of profit |

| Large Deal TCV | $4.8B | $3.2B (estimated Q3 FY25) | +50.00% | Exceptional quarter-to-quarter growth; significant acceleration in enterprise AI-led transformation deals |

Q3 FY26 reflects a bifurcated performance—reported metrics weighed down by one-time labour code provisions (totaling ₹1,289 crore across operations, impacting gratuity and leave liabilities), while adjusted metrics reveal underlying business strength with 12% adjusted profit growth and nearly flat margins despite wage inflation pressures. The 50% surge in large deal TCV signals market share gains in strategic AI and digital transformation engagements.

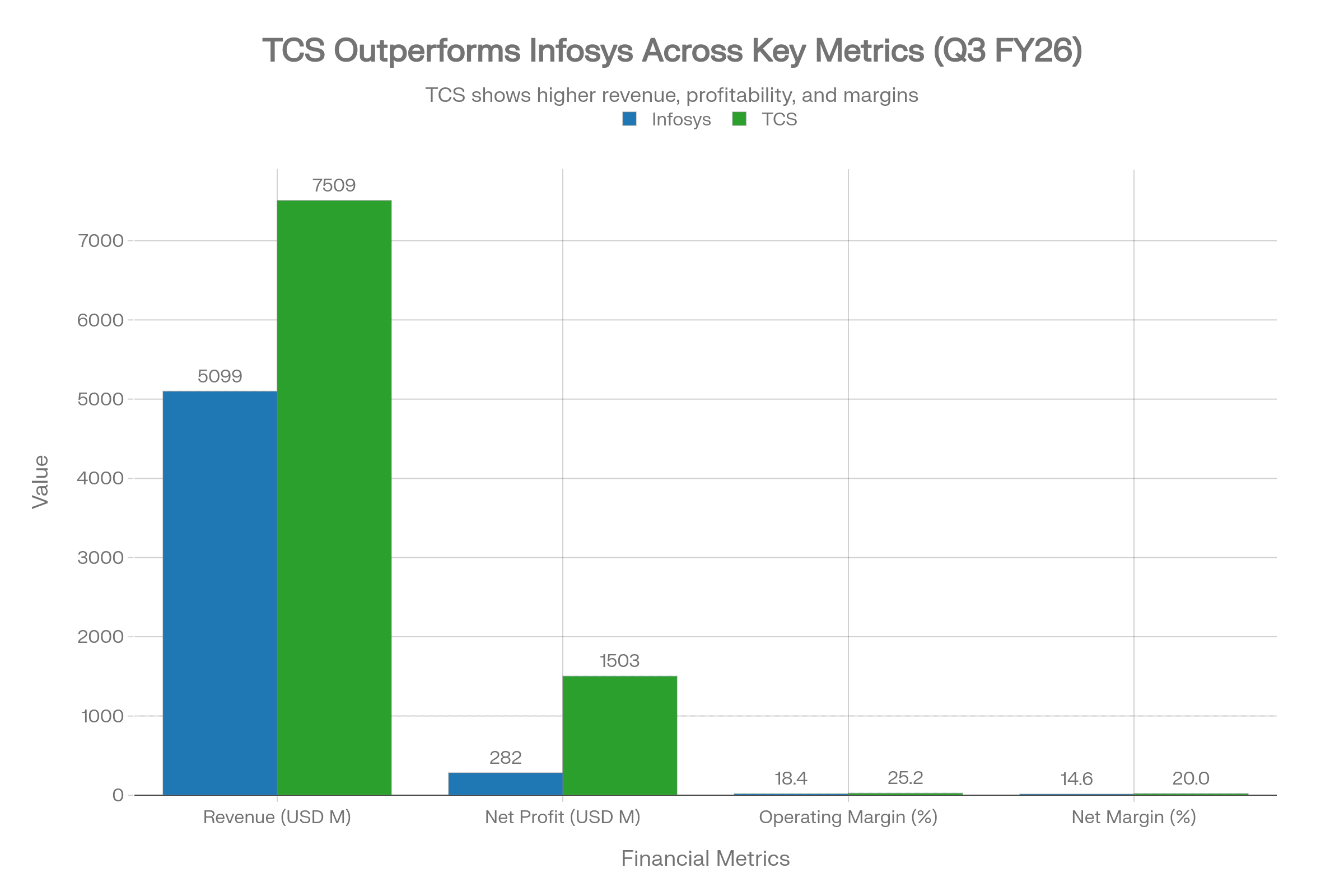

Competitor Comparison: Infosys vs. TCS Q3 FY26

| Metric | Infosys Q3 FY26 | TCS Q3 FY26 | Difference | Market Position |

| Revenue (USD) | $5,099M | $7,509M | -$2,410M (-32%) | TCS larger but Infosys growing faster in constant currency (1.7% vs. -2.6% CC decline for TCS) |

| Revenue (INR) | ₹45,479 Cr | ₹67,087 Cr | -₹21,608 Cr (-32%) | TCS maintains ~1.5x revenue scale; consolidation of India’s IT industry around two mega-players evident |

| Net Profit (USD) | $282M | $1,503M | -$1,221M (-81%) | TCS net profit significantly higher; reflects TCS premium positioning in BFSI/large accounts and superior margins |

| Operating Margin | 18.4% (21.2% adj.) | 25.20% | +370 bps (410 bps adj.) | TCS margin leadership substantial; reflects service mix (higher-margin banking/BFSI: 30.5% of TCS), client scale leverage, and onshore efficiency |

| Net Margin | 14.6% (16.8% adj.) | 20.00% | +540 bps (330 bps adj.) | TCS’s net margin significantly superior; benefits from market leadership, account concentration with larger enterprises, and lower selling costs |

| Large Deal TCV | $4.8B | $9.3B | -$4.5B (-49%) | TCS substantially outpaced Infosys; $9.3B TCV (vs. $4.8B) reflects mega-deal closures including North America BFSI (TCS: $4.9B NA exposure vs. Infosys strategic pipeline focus) |

| Deal Quality (Net New) | 57% net new | Not disclosed | TCS data unavailable | Infosys’s 57% net new component indicates pipeline replenishment and share gains vs. account defense posture |

| Operating Cash Flow (%) | 113.1% FCF/profit (adj.) | 130.4% of net profit | -17.3 bps | Both strong cash generators; TCS slightly superior cash conversion underscores working capital discipline and lower DSO |

| Reported EPS (Constant Ccy) | ₹16.17 | Comparable EPS data not directly disclosed | — | Infosys EPS impacted by labour code; TCS reported EPS lower due to exceptional items (₹3,391 Cr provision) |

| AI Services Annualized Revenue | $1.5B+ (Topaz-led, estimated) | $1.8B | -$0.3B (-17%) | TCS leads in disclosed AI services revenue; Infosys emphasizes solution-led positioning (Topaz platforms) vs. line-item reporting |

| Dividend Payout | Interim dividend + ₹18,000 Cr buyback | ₹57/share (3x interim + special) | TCS more aggressive shareholder returns | TCS payout ratio higher (~3-4x interim); reflects confidence in FY26-27 growth and strong balance sheet |

Strategic Takeaways

- Scale Gap Persisting: TCS maintains ~1.5x revenue and >3x net profit scale, reflecting its positioning as India’s largest IT services exporter and anchor in BFSI (30.5% of revenue)

- Growth Momentum Asymmetry: Infosys’s 1.7% constant currency YoY growth outpaces TCS’s -2.6% CC decline, signaling Infosys’s ability to gain share in higher-growth digital/AI segments despite TCS’s baseline size advantage

- Margin Compression is Structural: Infosys’s 18.4%-21.2% margin band (vs. TCS’s 25.2%) reflects service mix skew toward transformation/implementation (lower margin) vs. TCS’s BFSI account leverage and premium consulting margins. Wage inflation and India labour code provisions affect both but weigh more heavily on Infosys’s lower-margin business

- Deal Pipeline Divergence: TCS’s $9.3B TCV reflects closing of mega-deals (notably one “mega deal” from North America in Q3); Infosys’s $4.8B with 57% net new suggests a broader set of mid-market and emerging vertical deals, indicating portfolio rebalancing away from legacy accounts

- AI Services: Strategic Differentiation: While TCS reports $1.8B annualized AI services revenue (higher absolute), Infosys’s emphasis on Topaz fabric, agentic AI, and industry-specific GenAI solutions reflects a distinct competitive positioning focused on AI platform utilization vs. TCS’s infrastructure-oriented approach

How the Market Reacted?

Infosys’s stock market reaction was decidedly bullish despite the reported profit decline. On the domestic front, Infosys shares rallied 5.45% to ₹1,686.90 on January 16, 2026 (two trading days post-announcement), reflecting strong investor appetite for the company’s revised guidance and robust deal wins. In US trading, American Depositary Receipts (ADRs) surged as much as 8.6% to $19.03, indicating powerful international investor confidence in the company’s AI-led transformation narrative.

The market’s sharp focus on adjusted metrics (which strip out the ₹1,289 crore one-time labour code provision), large deal momentum, and the 50-basis-point upward revision of FY26 full-year guidance to 3.0%-3.5% constant currency growth—up from the prior 2.5%-3.0% range—signaled that investors view the quarter as a turning point toward acceleration in the second half of FY26. The decision to complete the largest-ever ₹18,000 crore share buyback in lockstep with the results announcement further catalyzed confidence, underscoring management’s conviction in valuation recovery and cash generation durability.

Collectively, the market reaction suggests that investors have recalibrated their view of Infosys from a cyclical IT services commodity player to an AI-platform beneficiary with structural pricing power and margin-expansion potential in high-growth digital transformation engagements—a narrative reinforced by the 57% net new component of the $4.8B deal TCV and Infosys Topaz’s emerging penetration across the BFSI, enterprise operations, and customer experience verticals.

Looking Ahead: FY26 Guidance and Outlook

Infosys FY26 Revised Guidance:

- Revenue Growth: 3.0%-3.5% in constant currency (revised up from 2.5%-3.0%), implying $19.9-20.1B in annual revenues.

- Operating Margin: 20%-22% (guidance range maintained; labour code adjustment of ₹1,289 crore explicitly excluded from guidance band).

- H2 FY26 Acceleration: Guidance revision signals management confidence in demand uptick from Q4 onwards, underpinned by AI services ramp and ongoing large deal conversions.

Key Strategic Drivers:

- Infosys Topaz Momentum: Client wins with Metro Bank (Workday finance transformation), Lufthansa Systems (GCC-AI model), NHS Business Services Authority (workforce management), and Barry Callebaut (AI-powered digital transformation) exemplify traction in Topaz fabric deployment across diverse verticals and geographies.

- Reskilling and Capacity: Commitment to reskill workforce for AI-first operations—evidenced by headcount growth of 5,043 in Q3—coupled with operational efficiency initiatives (margin expansion of 0.2% adjusted QoQ despite seasonally weak quarter) positions Infosys for sustainable margin recovery.

- Capital Allocation Discipline: Completion of ₹18,000 crore buyback (largest in company history) and interim dividend payout demonstrate balance between growth investment (reskilling, AI infrastructure) and shareholder returns, reinforcing shareholder value thesis.

- Competitive Positioning: AI service leadership (Infosys Topaz annualized revenue estimated at $1.5B+) and diverse deal pipeline (57% net new, $4.8B TCV) contrast with TCS’s larger but slower-growth account base, suggesting Infosys is well-positioned to capture incremental digital transformation wallet in mid-market and strategic accounts.

Conclusion

Infosys’s Q3 FY2025-26 results underscore a company in transition: from a traditional IT services model struggling with demand cyclicality to an AI-platform-driven transformation partner capturing premium-priced digital services engagements. While reported metrics were temporarily weighed down by ₹1,289 crore in one-time labour code provisions, the company’s adjusted profitability (up 12% YoY), stellar large deal wins ($4.8B TCV with 57% net new), and 50-basis-point upward revision of annual guidance demonstrate underlying business momentum. The market’s enthusiastic response—5.45% domestic and 8.6% ADR rally—reflects investor recognition that Infosys has successfully reoriented its portfolio toward higher-growth, higher-margin AI-led services at a moment when global enterprises are accelerating digital and generative AI investments.

For investors, the key forward-looking metric is execution of the H2 FY26 guidance upgrade: delivery of the revised 3.0%-3.5% constant currency growth and maintenance of the 20%-22% operating margin band will validate management’s bullish posture and support re-rating toward its historical forward P/E multiples. Conversely, execution slippage or continued global IT spending moderation could pressure the stock back toward recent lows.