Introduction

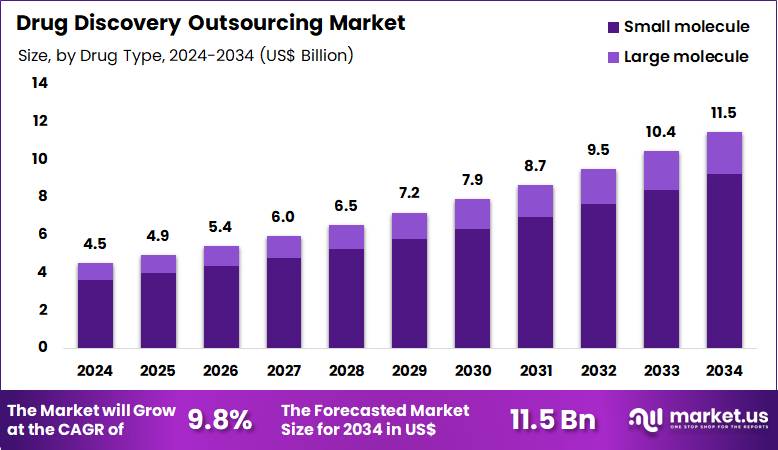

The Global Drug Discovery Outsourcing Market is projected to grow from US$4.5 billion in 2024 to US$11.5 billion by 2034, registering a CAGR of 9.8% as pharmaceutical and biotechnology companies increasingly externalize R&D-intensive discovery activities to specialized contract research organizations.

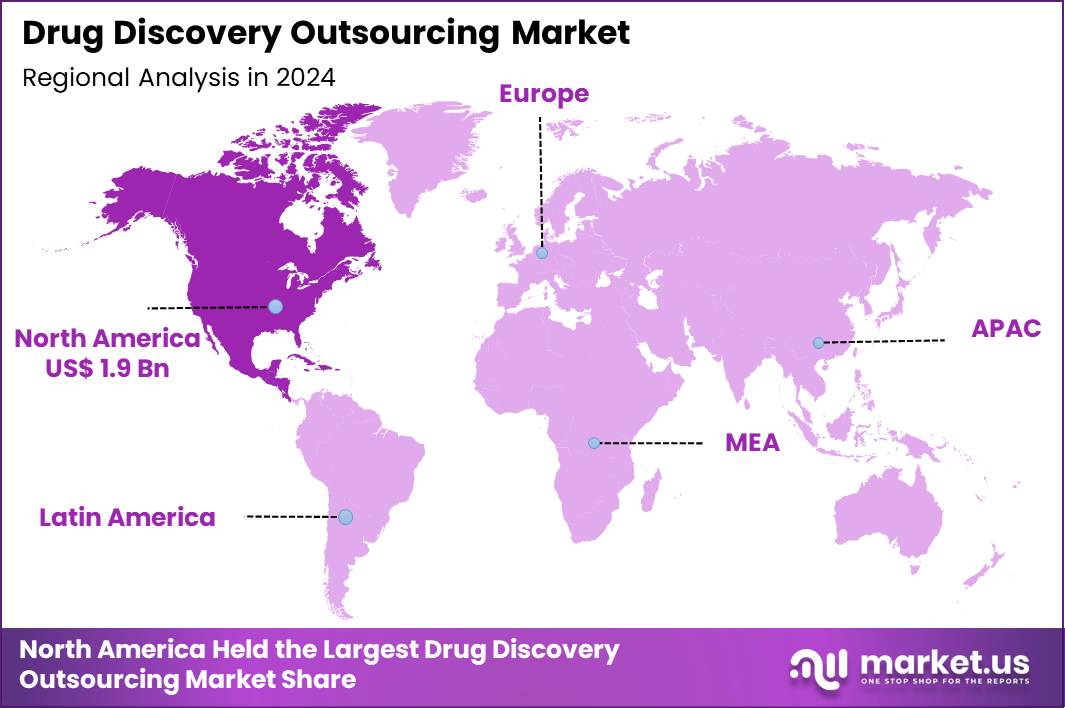

Small molecules account for about 80.4% of outsourced discovery revenue, while oncology leads therapeutic demand with a 27.9% share, underscoring the sector’s focus on high-value, innovation-driven pipelines. North America dominates with 42.3% of market revenue, supported by robust FDA approval volumes and deep capital markets that incentivize lean, outsourced models for early-stage research.

Request For Latest Sample Report @ https://market.us/report/global-drug-discovery-outsourcing-market/free-sample/

Key Takeaways

- In 2024, the market generated revenue of US$ 4.5 billion and is projected to reach US$ 11.5 billion by 2034, expanding at a CAGR of 9.8% during the forecast period.

- Based on drug type, the market is categorized into small-molecule and large-molecule drugs. The small-molecule segment dominated in 2024, accounting for 80.4% of the total market share.

- By service type, the market is segmented into target identification & screening, target discovery & validation, hit identification/high-throughput screening, hit-to-lead development, lead optimization, preclinical testing services, and others. Among these, lead optimization accounted for 30.1%.

- In terms of therapeutic area, the market is classified into oncology, neurology/CNS disorders, infectious diseases, cardiovascular diseases, immunology & inflammatory disorders, metabolic & endocrine disorders, respiratory diseases, gastrointestinal disorders, rare/orphan diseases, ophthalmology diseases, dermatology diseases, and others. Oncology emerged as the leading segment, capturing 27.9% of the market revenue.

- Based on end user, the market is divided into pharmaceutical & biotechnology companies and academic & research institutes. The pharmaceutical & biotechnology companies segment led the market, accounting for 83.1% of revenue.

- Regionally, North America dominated the market, holding a 42.3% share in 2024.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 4.5 Billion |

| Forecast Revenue (2034) | US$ 11.5 Billion |

| CAGR (2025-2034) | 9.80% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Small Molecule and Large Molecule), By Service Type (Target Identification & Screening, Target Discovery & Validation, Hit Identification/High-Throughput Screening, Hit-to-Lead Development, Lead Optimization, Preclinical Testing Services and Others), By Therapeutic Area (Oncology, Neurology/CNS Disorders, Infectious Diseases, Cardiovascular Diseases, Immunology & Inflammatory Disorders, Metabolic & Endocrine Disorders, Respiratory Diseases, Gastrointestinal Disorders, Rare/Orphan Diseases, Ophthalmology Diseases, Dermatology Diseases and Others), By End-User (Pharmaceutical & Biotechnology Companies and Academic & Research Institutes) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IQVIA, ICON plc, Syneos Health, Charles River Laboratories, Labcorp, WuXi AppTec, Parexel, Albany Molecular Research Inc., EVOTEC, GenScript, Thermo Fisher Scientific Inc., Merck & Co., Inc., Dalton Pharma Services, Oncodesign, Jubilant Biosys, DiscoverX Corp., QIAGEN, Eurofins SE, Syngene International Limited, Pharmaron Beijing Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

How Growth Is Impacting the Economy ?

Rising investment in drug discovery outsourcing is stimulating broader economic activity by channeling capital into high-skill research employment, advanced laboratory infrastructure, and AI-enabled platforms across key hubs in North America, Europe, and Asia Pacific. As pharmaceutical and biotech companies reduce fixed in-house R&D footprints, they shift toward variable-cost outsourcing models that free cash for late-stage development, commercialization, and M&A, thereby amplifying value creation across the healthcare ecosystem.

This structural shift supports a global network of contract research organizations, boosting demand for chemists, data scientists, bioinformaticians, and regulatory specialists, and promoting technology transfer into emerging markets.

At the same time, macroeconomic pressures such as inflation and tariffs raise input costs for reagents and specialized equipment, nudging sponsors to diversify outsourcing destinations and encouraging regional capacity build-out, which further distributes economic benefits geographically.

Key Segmentation

Drug discovery outsourcing demand is heavily concentrated in small-molecule programs, which account for over 80% of market share, reflecting their favorable manufacturability and mature regulatory pathways. On the service side, lead optimization represents the largest segment at about 30.1%, followed by target identification, validation, high-throughput screening, hit-to-lead, and preclinical testing, each addressing different stages of the discovery funnel.

Therapeutic segmentation is led by oncology at 27.9%, with significant activity in neurology/CNS, infectious, cardiovascular, metabolic, respiratory, and immunology indications. End users are predominantly pharmaceutical and biotechnology companies, which represent roughly 83.1% of revenue, while academic and research institutes form a smaller but influential share through collaborative discovery programs.

Sector-Specific Impacts

- Pharmaceutical and biotech: Heavy users of outsourced hit-to-lead, lead optimization, and ADME-Tox profiling to compress timelines and de-risk pipelines in oncology, CNS, and rare diseases.

- Technology and AI firms: Benefiting from demand for cloud-based platforms, generative AI, and machine learning models integrated into virtual screening and predictive toxicology.

- Academic and research institutes: Leveraging CRO partnerships for complex assays and multi-omics analytics, increasingly positioned as innovation feeders into commercial drug programs.

- Logistics and equipment suppliers: Experiencing higher demand for lab automation, robotics, and specialized instruments as outsourcing centers scale capacity globally.

Analyst Viewpoint

At present, the drug discovery outsourcing market reflects a resilient growth story anchored in rising novel drug approvals, complex biology, and mounting pressure on internal R&D productivity, prompting both large pharma and emerging biotechs to deepen long-term partnerships with specialized providers.

Over the next decade, analysts anticipate that AI-native CROs, integrated discovery platforms, and regional hubs in Asia Pacific will further accelerate time-to-candidate while spreading high-value scientific employment across geographies.

As regulatory frameworks for AI validation and cross-border data sharing mature, transparency and trust should improve, enabling richer model training and more predictive discovery engines. Overall, the market’s trajectory appears structurally positive, with expanded opportunities in rare diseases, precision medicine, and novel modalities likely to sustain premium growth and incremental margin expansion for best-in-class outsourcing partners.

Regional Analysis

North America currently holds around 42.3% of the global drug discovery outsourcing market, supported by dense clusters of pharmaceutical headquarters, venture-backed biotechs, and advanced CRO infrastructure. The region benefits from strong FDA throughput and sustained funding for oncology, rare diseases, and novel modalities, which translates into steady demand for target identification, hit-to-lead, and preclinical services.

Europe contributes through established regulatory frameworks and specialized disease expertise, while Asia Pacific is expected to post the fastest CAGR as China, India, and Singapore expand cost-competitive, technologically sophisticated discovery capabilities. Latin America and the Middle East & Africa remain smaller but are gradually integrating into global networks through niche service offerings and regional clinical-development linkages.

Business Opportunities

Expanding pipelines in oncology, neurology, and immunology create rich opportunities for discovery platforms that combine disease-specific models, biomarker strategies, and translational expertise, allowing providers to command premium pricing. AI-first outsourcing firms that offer generative design, active learning, and closed-loop experimentation will be well-positioned to win share as sponsors seek step-changes in R&D productivity.

The push into rare and orphan diseases opens high-value, low-competition niches for contract organizations with genetic, enzyme-replacement, and RNA-modality capabilities. Additional upside exists in building regional centers of excellence in Asia Pacific that can serve as global hubs for organoid models, high-content imaging, and in silico ADMET, tightly integrated with multinational sponsors’ digital R&D ecosystems.

Engage with Our Expert Team at [email protected] for Data-Driven Solutions

Key Player Analysis

Leading providers in the drug discovery outsourcing market differentiate themselves by offering end-to-end capabilities that span target discovery through IND-enabling preclinical packages, enabling clients to minimize handoffs and accelerate development. These organizations invest heavily in AI-enhanced screening, advanced bioinformatics, and high-throughput platforms to improve hit quality, shorten optimization cycles, and increase probability of technical success.

Many have built global laboratory networks with presence in North America, Europe, and Asia Pacific, allowing sponsors to tap specialized expertise and cost structures while managing geopolitical and supply risks. Strategic partnerships with both large pharma and emerging biotechs, often structured around multi-year, milestone-based engagements, embed these players deeply into clients’ pipelines and secure recurring, high-margin revenue streams.

Top Key Players

- IQVIA

- ICON plc

- Syneos Health

- Charles River Laboratories

- Labcorp

- WuXi AppTec

- Parexel

- Albany Molecular Research Inc.

- EVOTEC

- GenScript

- Thermo Fisher Scientific Inc.

- Merck & Co., Inc.

- Dalton Pharma Services

- Oncodesign

- Jubilant Biosys

- DiscoverX Corp.

- QIAGEN

- Eurofins SE

- Syngene International Limited

- Pharmaron Beijing Co., Ltd.

Recent Developments

- IQVIA acquisition (February 2026): IQVIA announced an agreement to acquire selected drug discovery assets from Charles River Laboratories to strengthen early-stage discovery capabilities. The transaction is expected to enhance end-to-end services across target identification, hit-to-lead, and lead optimization, improving support for oncology, neurology, and rare disease programs.

- Charles River divestment strategy (February 2026): Charles River Laboratories agreed to sell portions of its European drug discovery business to IQVIA for approximately $145 million, with additional milestone payments. The move is aligned with portfolio optimization and margin expansion initiatives.

- IQVIA strategic collaboration (January 2026): IQVIA entered a long-term collaboration with Boehringer Ingelheim to deploy Data-as-a-Service platforms for global data harmonization and analytics transformation, supporting AI-enabled drug development and commercialization workflows.

- WuXi AppTec financial expansion (March 2026): WuXi AppTec reported RMB 45.46 billion total revenue for 2025, with backlog increasing 28.8%, indicating strong demand for outsourced discovery and development services.

Conclusion

Drug discovery outsourcing is positioned for sustained expansion, driven by rising pipeline complexity, cost pressures, and growing reliance on specialized CRO capabilities. Small molecules dominate demand, while oncology and lead optimization services capture the largest shares, reflecting focus on high-value innovation.

Pharmaceutical and biotechnology companies remain primary customers, reinforcing recurring outsourcing models. North America leads revenue, with Asia Pacific emerging as the fastest-growing region.

Investment in AI-enabled discovery, global laboratory networks, and integrated platforms is accelerating timelines and improving success rates. Strategic collaborations, acquisitions, and capacity expansion are expected to enhance competitiveness, broaden access to expertise, and support market growth.