Introduction

Small Satellite Statistics: The global small satellite business has just, sort of, entered a phase of expansion in 2026 that feels unprecedented, mostly because there’s more and more appetite for Earth observation, broadband connectivity, defense surveillance, IoT services, and also direct-to-device communications. Small satellites, usually described as spacecraft under 500 kilograms or so, have changed the space economics in a big way by lowering manufacturing costs, speeding up development cycles, and letting operators build large-scale constellations.

On top of that, miniaturized electronics, AI-driven onboard processing, reusable launch vehicles, and rideshare launch services have moved everything along faster, maybe even quicker than expected. Governments, commercial players, and academic teams are leaning harder on small satellites for cheaper, practical space capabilities, so this part of the industry is turning into one of the fastest-moving areas across the whole global space economy.

Editor’s Choice

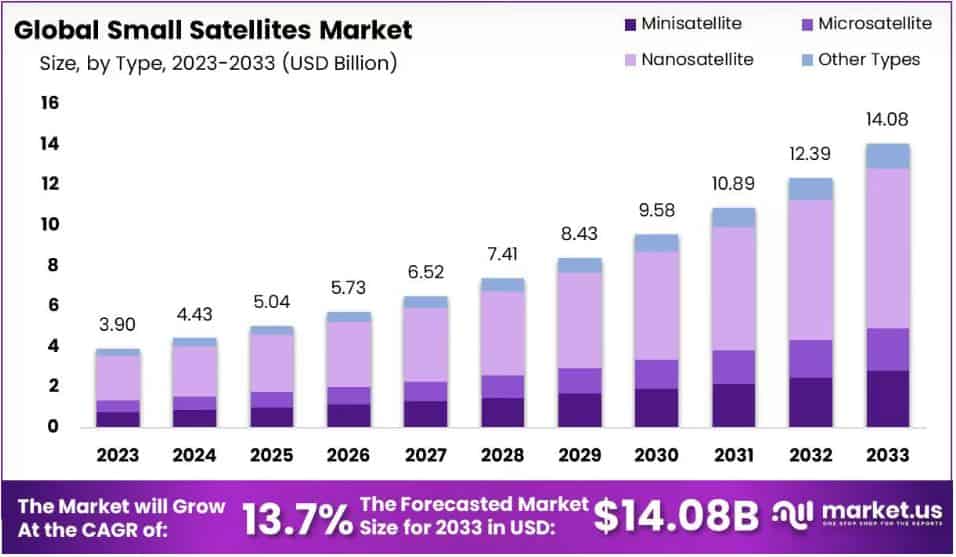

- The global small satellite market is expected to climb from USD 4.43 billion in 2024 to USD 14.08 billion by 2033, which is more than triple overall.

- A strong 13.7% CAGR points to the fact that the sector stays among the fastest-growing segments in the space economy.

- Small satellites have become the main spacecraft category, making up around 94% of all spacecraft launched worldwide by 2021.

- The industry is forecasted to place, basically, 16,900 small satellites into orbit between 2026 and 2035, showing a long stretch of consistent launch momentum.

- During 2026–2035, smallsats should account for roughly 33% of all satellites launched globally, even while they only contribute about 6% of total satellite mass.

- Investor confidence is still solid, with USD 11.5 billion in private funding landing in small satellite programs across 2025.

- Minisatellites generated 45.69% of total market revenue in 2025, making them the largest revenue-producing segment.

- Microsatellites are forecast to grow at an impressive 24.52% CAGR through 2031, driven by advances in imaging and sensor technologies.

- The nanosatellite and microsatellite market reached approximately USD 3.3 billion in 2023 and is expected to grow at more than 15% annually through 2032.

- Electric propulsion captured around 42% of global satellite propulsion revenue in 2024 and can reduce mission costs by 30–40%, making it a key technology for next-generation small satellites.

(Source: market.us)

- According to market.us, the small satellite market is at USD 4.43 billion in 2024, and it’s expected to climb all the way up to USD 14.08 billion by 2033.

- This market should expand at a CAGR of 13.7% over the forecast period, 2024 to 2033.

Small Satellites – The Fastest-Growing Force In The Space Industry

- NASA’s “Small Spacecraft Technology State-of-the-Art” report kind of shows how small satellites went from experimental platforms into an actual backbone of the modern space industry.

- Back when NASA put out the very first edition in 2013, there were only 247 CubeSats and 105 non-CubeSat small spacecraft, weighing under 50 kg, that had been launched worldwide.

- In total, they accounted for less than 2% of the overall mass put into orbit, which kind of proves how limited that small satellite market was at the time.

- NASA states that small spacecraft are now the main route to reach space for commercial players, government agencies, universities, and research organizations.

- Starting in 2023, the market saw a jump in mini-class satellites in the 201–600 kg range.

- At the same time, a newer class of constellations started showing up in the 600–1,200 kg bracket. These heftier platforms bring more power, more payload capability, and better operational flexibility, while still keeping a lot of the cost benefits people usually associate with small spacecraft.

- The report also points toward a bigger appetite for Orbital Maneuvering Vehicles (OMVs) and Orbital Transfer Vehicles (OTVs), which help satellites move into very specialized orbital paths after launch.

- Meanwhile, onboard autonomy, plus more mature data-processing capabilities, are getting close to “must-have” status because satellite constellations are creating larger volumes of info, and operators depend less and less on ground control systems.

- Looking back at historical launch data, you can see the whole shift becoming real. For example, NASA data indicates that by 2021, around 94% of all spacecraft launched worldwide had masses below 600 kg, so it basically confirms that small satellites are now the dominant spacecraft category in terms of launch activity.

- From a market-analysis angle, the stats show a pretty clear industry transition: small satellites went from being under 2% of orbital launch mass in 2013 to becoming the leading spacecraft class globally.

- The quick growth of 201 to 1,200 kg constellations, plus higher launch cadence, along with autonomous operations, suggests small satellites will keep acting as one of the most influential drivers of space industry growth for the rest of this decade.

Small Satellite Boom To Transform The Space Industry By 2035

- The global small satellite (smallsat) sector is entering a new phase of almost large-scale growth.

- Novaspace is forecasting something like 16,900 small satellites, weighing under 500 kilograms, being launched between 2026 and 2035.

- The forecast ends up looking like an average deployment pace near 230 metric tons of small satellites each year, like about 640 kilograms lifted into orbit every day for the whole decade.

- That kind of steady launch tempo points to a rising appetite for sovereign satellite constellations, and it also lines up with the ongoing expansion of commercial space networks.

- Even if mega-constellations still drive a lot of the demand, national and regional space efforts are getting more noticeable as they become key momentum behind market growth.

- Novaspace puts it that smallsats should represent roughly 33% of all satellites flying globally from 2026 to 2035, but they only add around 6% of the total satellite mass.

- Investment activity stays lively too across the whole field. In 2025, private funding aimed at small satellite programs reportedly hit about USD 11.5 billion, backing next-generation constellations, stronger manufacturing know-how, and various deployment programs. This level of capital movement basically signals solid investor confidence in both scaling up and the long-term commercial value of smallsat technologies.

- The projection of 16,900 satellites and USD 11.5 billion per year in annual investment, plus the fact that the launch share is about one-third of all satellites worldwide, really shows that it won’t just be ideas anymore.

- Execution, manufacturing scale, and long-term customer demand will matter more and more, and they’ll end up deciding who leads.

- The next decade probably won’t be about who can design small satellites; it’ll be about who can deploy them efficiently and at scale.

Small Satellite Market Segmentation – Nano, Micro, and Mini-Satellites

- Looking at the global small satellite market in 2026, you get this two-speed industry, almost like parallel tracks.

- On one side, minisatellites (100–1,000 kg) bring in the biggest chunk of market revenue, mainly because they can support broadband communications and high-resolution Earth observation missions.

- On the other hand, nanosatellites and CubeSats (1–10 kg) are the fastest-growing slice, driven by lower costs, faster deployment cycles, and more adoption in education, defense, IoT, plus technology demonstration programs.

- Market segmentation data also makes it pretty clear that minisatellites were responsible for 45.69% of the total small satellite market value in 2025, so they’re the top revenue generator.

- Meanwhile, microsatellites are forecast to rise at a 24.52% CAGR through 2031, which lines up with how advanced sensors and imaging systems that used to need 400–500 kg spacecraft can now work on platforms in the 50–100 kg range.

- The nanosatellite and microsatellite segment hit about USD 3.3 billion in market value in 2023 and is set to keep growing at more than 15% each year through 2032.

- Hardware stays the big revenue source, making up over 59% of total market value, so you can see ongoing investment in satellite buses, power systems, avionics, and propulsion tech.

- Deployment statistics kind of tell another story compared with the revenue rankings. If you fold in big constellations like Starlink and OneWeb, minisatellites end up holding the largest portion of deployed small-satellite mass.

- NASA says launches of satellites in the 11–600 kg band rose roughly 10% in 2025. That suggests demand is getting stronger for bigger micro and mini-class craft.

- The message is reinforced by the “official small-spacecraft” definition expanding in 2023 from 600 kg to 1,200 kg, which basically reflects industry appetite for more capable platforms with extra payload capacity and added power generation.

- Looking ahead, industry forecasts suggest minisatellites will claim the largest revenue slice in 2026, while nanosatellites are expected to show the strongest CAGR from 2026 to 2036.

- Overall, this suggests a market where larger satellites bring in commercial returns, whereas smaller satellites keep fueling experiments, novelty, and faster deployment growth.

- Electric propulsion made up roughly 42% of the worldwide satellite propulsion revenue in 2024, and it can cut mission costs by something like 30–40% thanks to better fuel efficiency plus lower launch mass requirements.

- Electric propulsion is getting pretty much standard on mini- and micro-satellites that are built for multi-year operations.

- Nanosatellites still take the lead in launch volume, while minisatellites bring in more revenue and also show stronger operational capability.

Conclusion

Small satellites have moved from oddball experimental spacecraft into the backbone of today’s space infrastructure. Their capacity to enable budget-friendly communications, Earth observation, defense use cases, IoT services, and scientific tasks makes them pretty hard to replace for both governments and commercial operators. With fast market growth, solid private investment, and the plan (plus reality) of deploying thousands of satellites during the next decade, the sector’s influence keeps getting bigger.

And even if minisatellites keep producing the biggest portion of industry revenue, nanosatellites and microsatellites are still the ones pushing innovation and increasing launch volume. With propulsion systems, onboard autonomy, and constellation designs continuing to get better, small satellites will stay right at the center of future growth in the global space economy.

FAQ

The global small satellite market is expected to reach about USD 14.08 billion by 2033.

Industry forecasts suggest roughly 16,900 small satellites will be launched worldwide.

Small satellites made up around 94% of all spacecraft launches worldwide in 2021.

Minisatellites lead the market, representing 45.69% of total revenue in 2025.

Electric propulsion helps cut mission costs by around 30–40%, while also boosting efficiency and extending operational life.