Introduction

Microfinance Statistics: Microfinance is a financial service system that provides services to individuals who lack access to conventional banking services. The global microfinance industry has emerged as a crucial component of the financial ecosystem, serving as a lifeline for millions of underserved individuals and small businesses worldwide.

The sector has evolved beyond traditional lending, incorporating digital technologies that facilitate over 40% of all transactions. Microfinance Statistics can help us learn about essential aspects that holistically focus on this financial system.

Editor’s Choice

- India hosts 9,480 NBFCs, with NBFC-ND comprising 8,823 of the total companies.

- NBFC interest margins rose from 5.7% in 2018 to 6.6% in 2024

- Bajaj Finance leads Indian NBFCs with ₹4,451.33 billion market capitalization

- The gold sector shows the highest return on assets at 5.2% among NBFC types

- The housing sector dominates NBFC credit with a 27% market share

- Retail loans lead the NBFC credit sector with a 33% share

- The global microfinance market is valued at US$174 billion in 2023

- BRAC disbursed US$1.7 billion in loans, serving over 7 million people

- Women constitute 80% of global microfinance borrowers

- Digital transactions account for 40% of microfinance operations

- India represents 30% of the worldwide microfinance market

- Sub-Saharan Africa holds 15% of the global microfinance market share

- Non-performing loans increased to 7.5% in 2023

- Only 35% of MFIs met their funding targets in 2023

- Social impact investments in microfinance reached US$12 billion in 2023

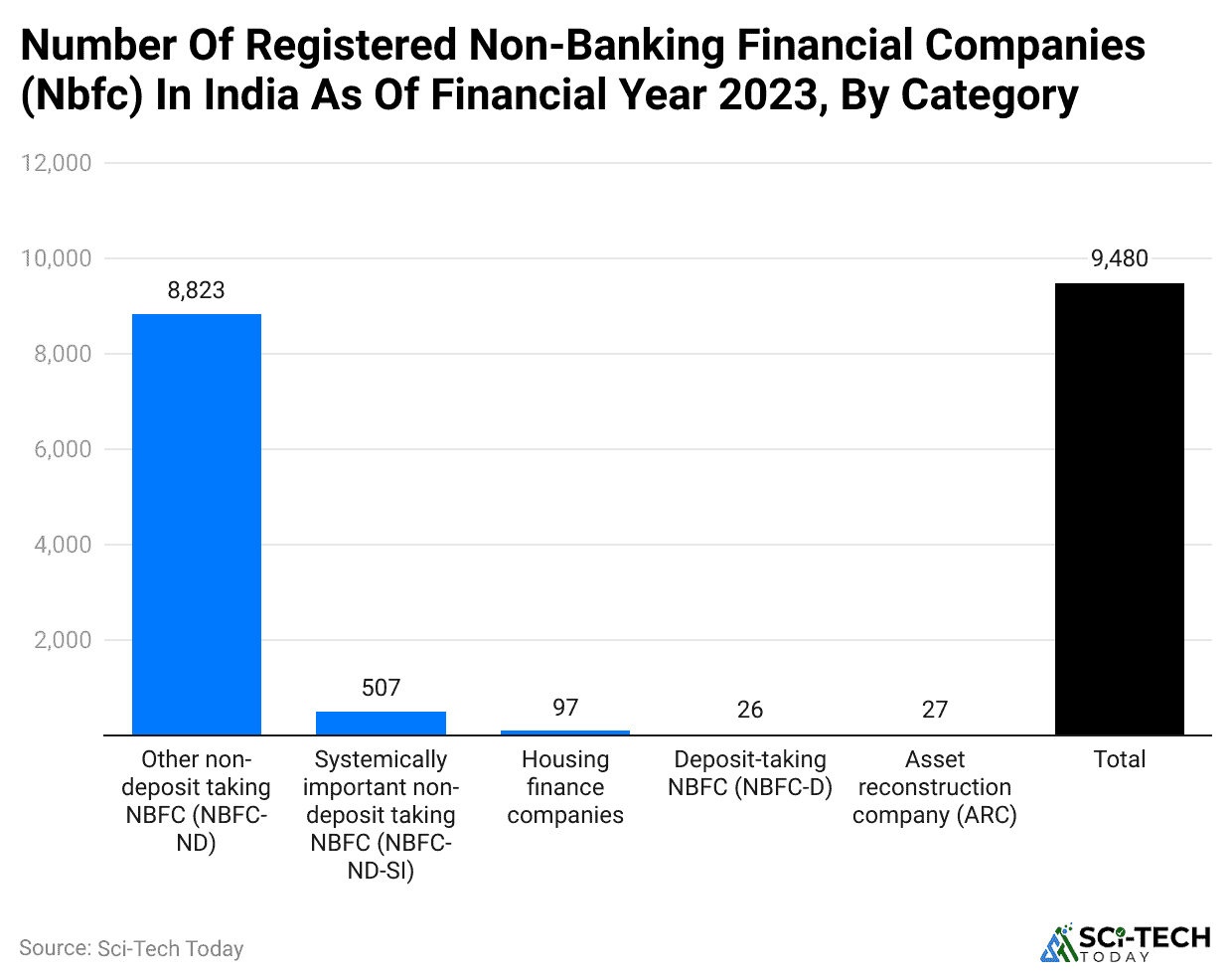

NBFC in India

(Reference: statista.com)

- Microfinance Statistics show that Deposit-taking NBFCs (NBFC-D), Asset reconstruction companies (ARC), Systemically important non-deposit-taking NBFCs (NBFC-ND-SI), and Housing finance companies are different types of registered NBFCs in India.

- Among the total of 9480 NBFCs, the breakup of different types of NBFCs is as follows: NBFC, Other non-deposit taking NBFCs (NBFC-ND) – 8,823, Systemically important non-deposit taking NBFCs (NBFC-ND-SI) – 507, Housing finance companies – 97, Asset reconstruction company (ARC) – 27, Deposit-taking NBFCs (NBFC-D) – 26.

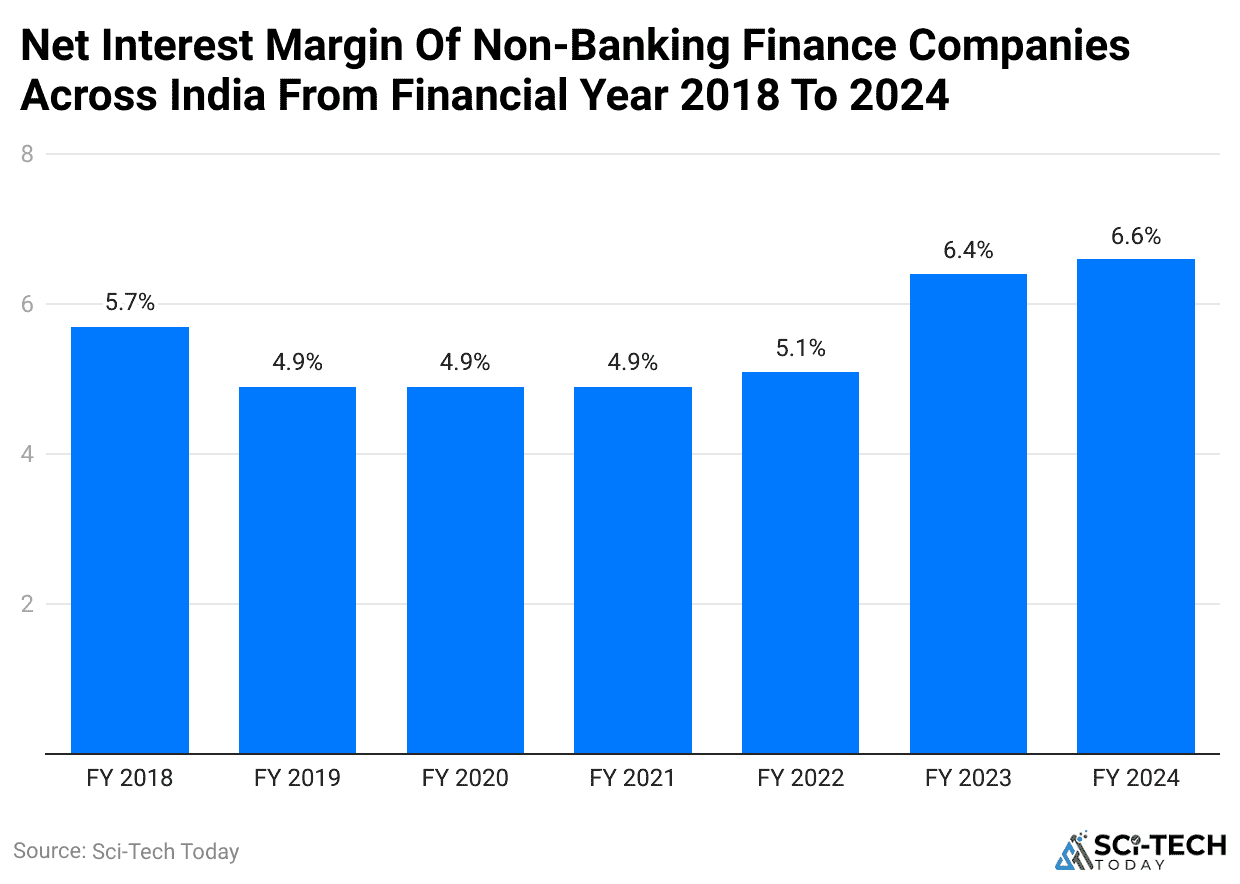

NBFC Interest Margin

(Reference: statista.com)

- Microfinance Statistics show that the interest margin of NBFC companies in India is increasing consistently.

- In 2018, the interest margin was 5.7%. It has increased to 6.6% by the end of 2024.

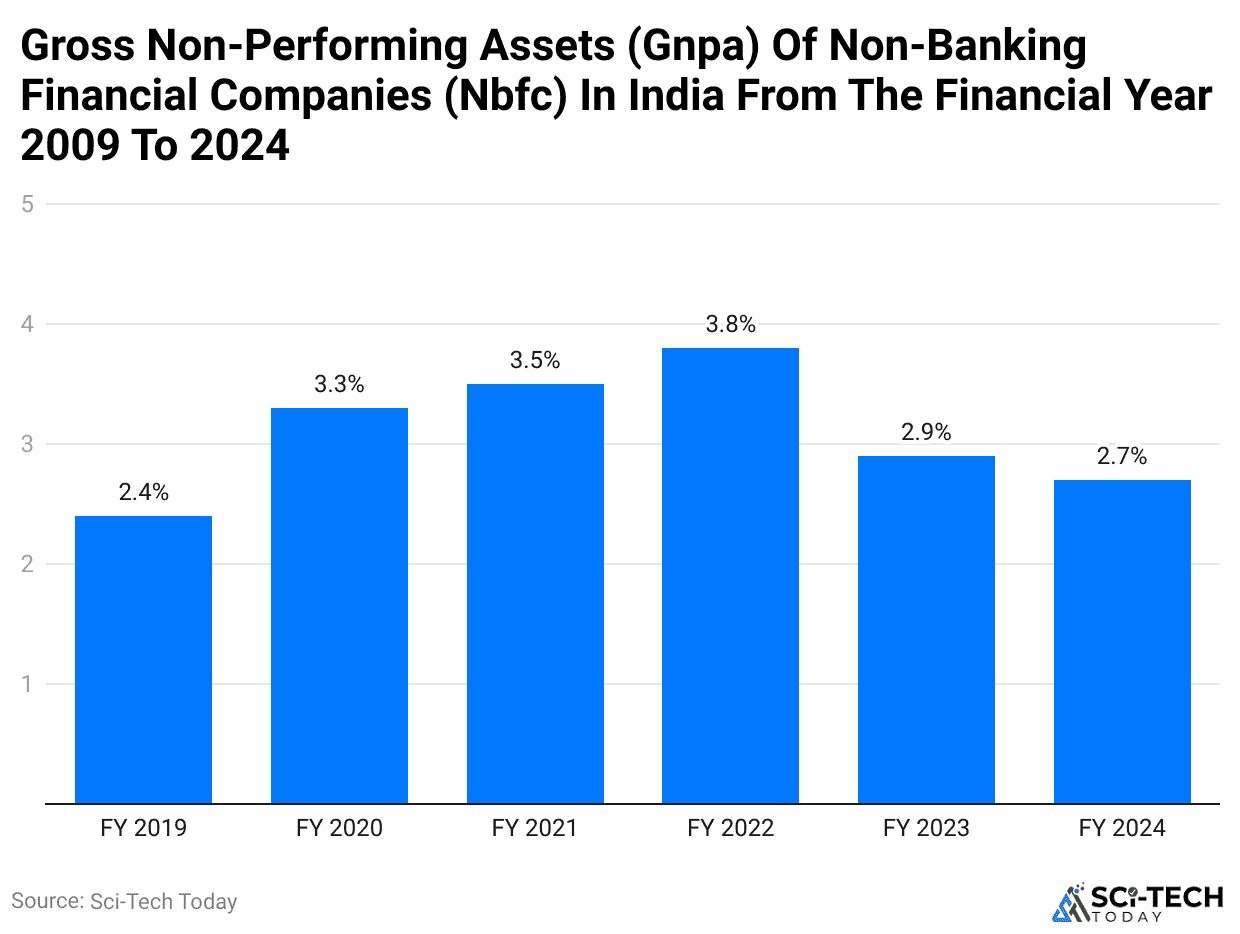

Non-Performing Assets of NBFC Companies

(Reference: statista.com)

- Microfinance Statistics show that the company’s non-performing assets have been volatile.

- In 2019, 2.4% of assets were non-performing; in FY 2024, the NPA was 2.7%.

- Between the period 2019 to FY 2024, the highest NPA was recorded in 2022 at 3.8%.

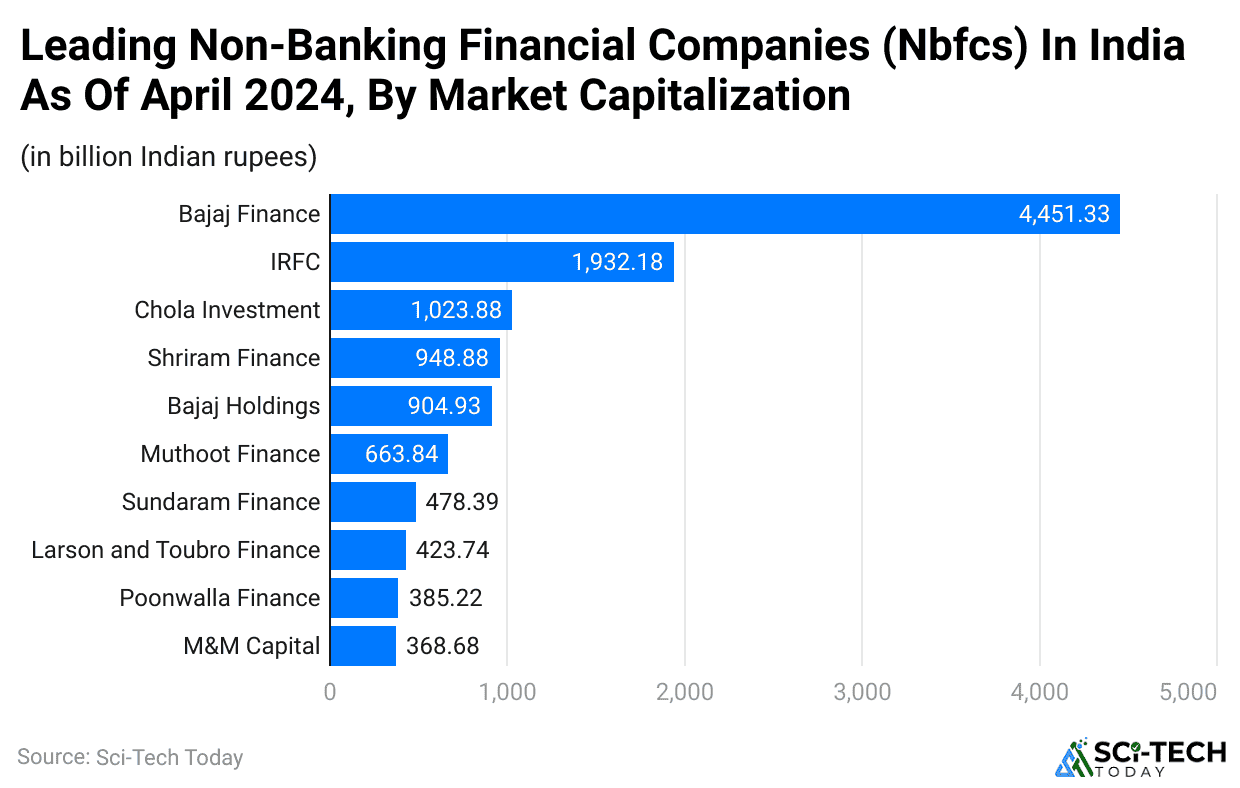

Leading Indian NBFC

(Reference: statista.com)

- Microfinance Statistics show that Chola Investment, Sundaram Finance, Shriram Finance, M&M Capital, Poonawalla Finance, Muthoot Finance, IRFC, Bajaj Holdings, Bajaj Finance, and Larsen and Toubro Finance are the top Indian NBFCs.

- Baja Finance has the highest market capitalization with ₹4451.33 billion, followed by IRFC with ₹1,932.18 billion market capitalization, Chola Investment with ₹1,023.88 billion market capitalization, Shriram Finance with ₹948.88 billion market capitalization, Bajaj Holdings with ₹904.93 billion market capitalization, Muthoot Finance with ₹663.84 billion market capitalization, Sundaram Finance with ₹478.39 billion market capitalization, Larson and Toubro Finance with ₹423.74 billion market capitalization, Poonawalla Finance with ₹385.22 billion market capitalization, M&M Capital with ₹368.68 billion market capitalization.

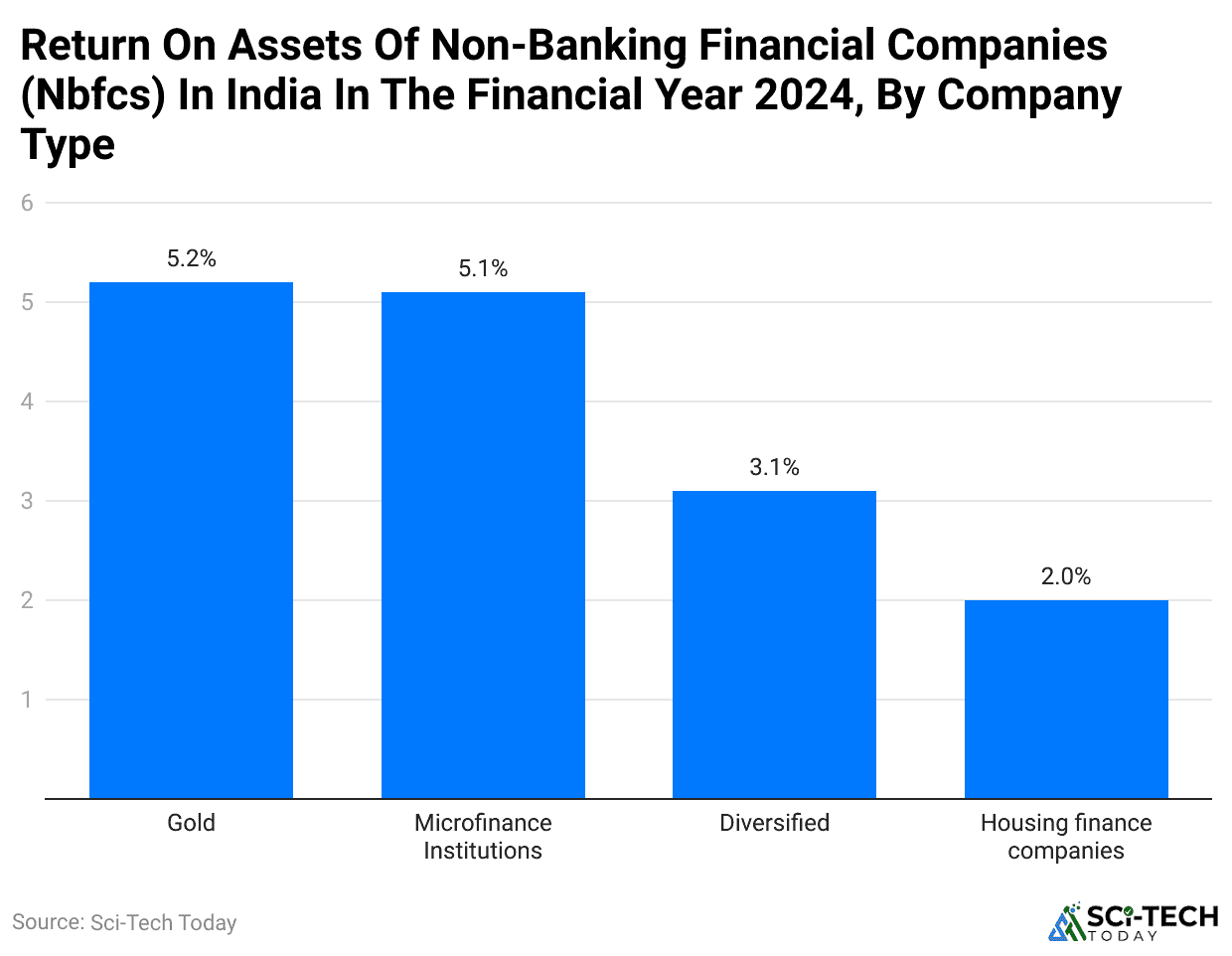

Return of Assets of NBFC By Company Type

(Reference: statista.com)

- Microfinance Statistics show that the return on assets can be categorized into the following company types: Microfinance institutions, Gold, Housing finance companies, and Diversified.

- Gold has the highest return on assets with 5.2%, followed by Microfinance institutions with a 5.1% return on investments, Diversified with a 3.1% return on assets, and Housing finance companies with a 2% return on assets.

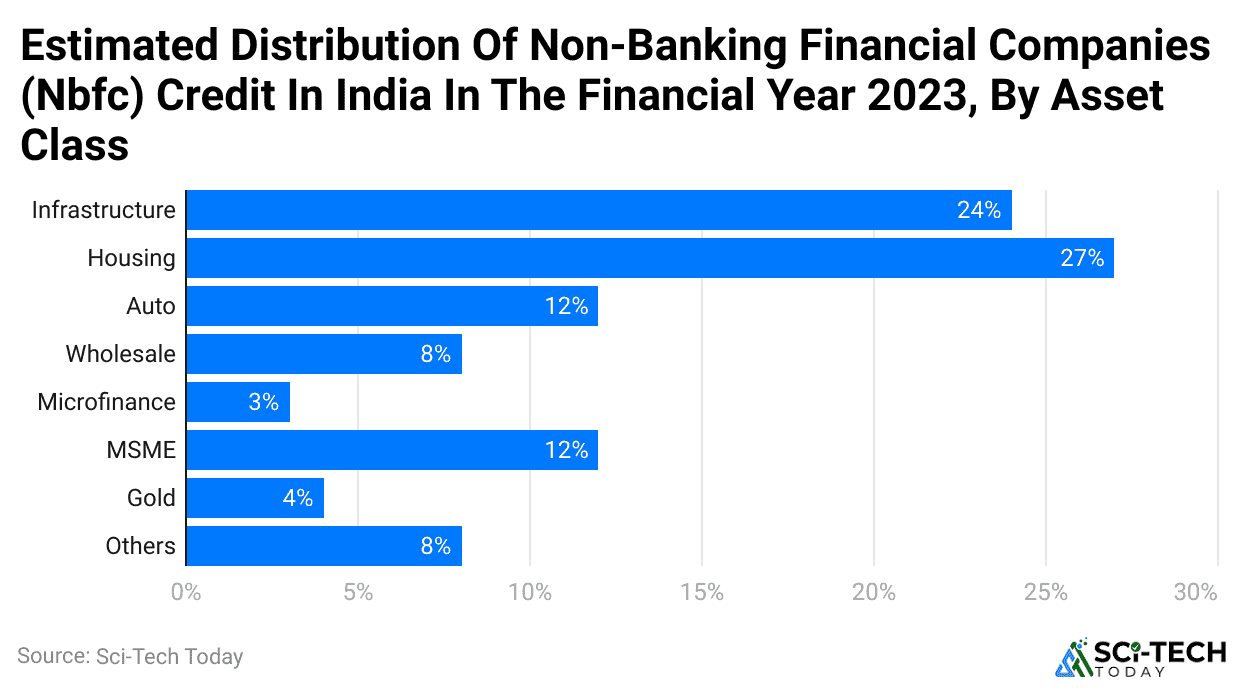

Distribution of NBFC By Asset Class

(Reference: statista.com)

- Microfinance Statistics show that NBFC credit in India is based on the following asset classes: Auto, Infrastructure, Others, MSME, Wholesale, Microfinance, Housing, and Gold.

- Housing has the highest NBFC credit with 27%, followed by Infrastructure with 24% credit, Auto at 12% credit, MSME with 12% credit, Others with 8% credit, Wholesale with 8% credit, and Microfinance with 3% credit.

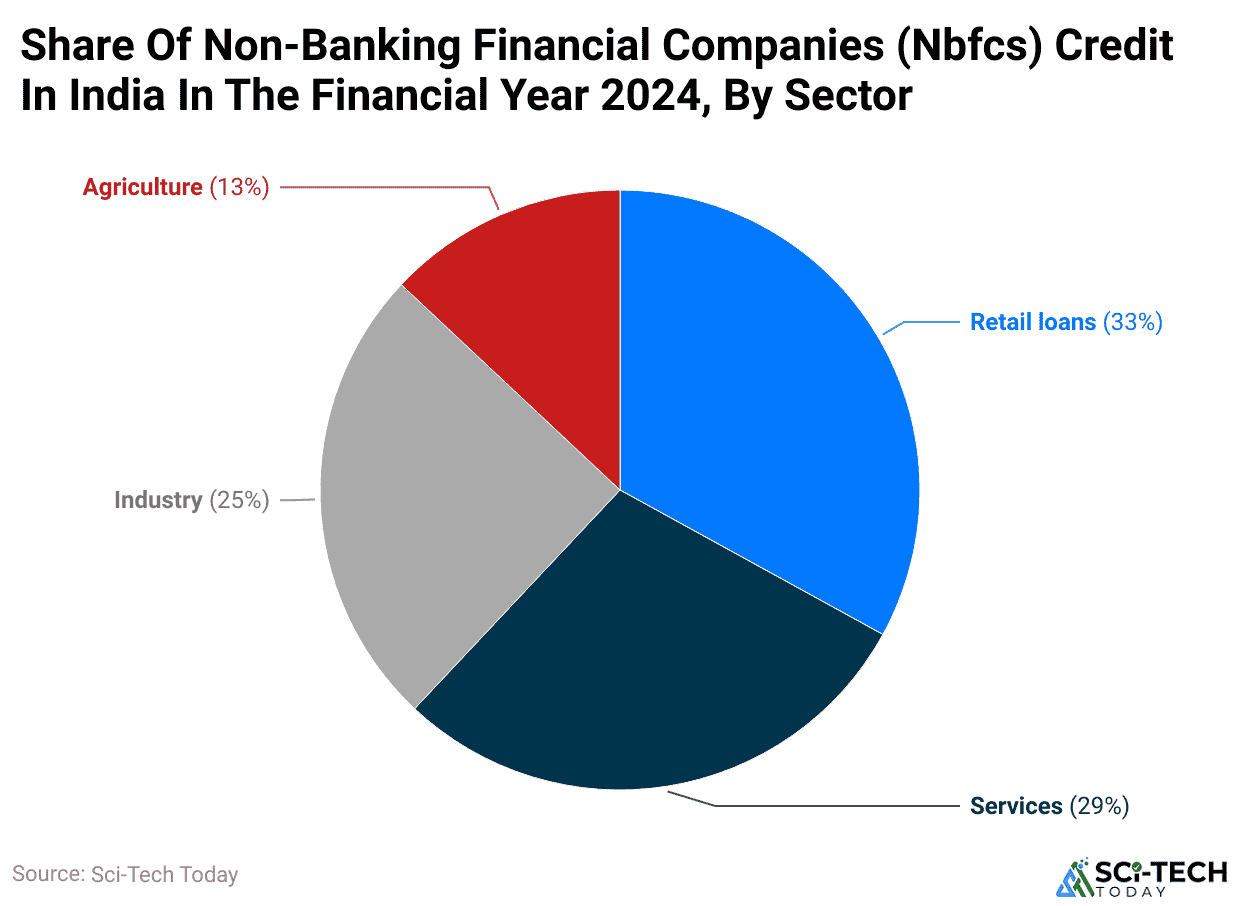

Share of NBFC Credit

(Reference: statista.com)

- Microfinance Statistics show that NBFC credit in India can be divided into the following sectors: Retail loans, Agriculture, Services, and Industry.

- Retail loans have the highest share with 33% credit, followed by Services with 29% credit share, Industry with 25% credit share, and Agriculture with 13% credit share.

List of Microfinance Companies

- FINCA Afghanistan

- Kashf Foundation

- Fundación Paraguaya

- Pegadaian

- Wizzit

- Hope International (Christian microfinance)

- Omidyar-Tufts Microfinance Fund

- Vittana

- Postal Savings Bank of China

- Self-Employed Women’s Association

- Bank Rakyat Indonesia

- Kiva (organization)

- Proshika

- ACLEDA Bank

- org

- Microcredit Summit Campaign

- Gamelan Council

- WWB Colombia

- Evolution Group (South Africa)

- UNDO

- Ford Foundation

- Bank Woori Saudara

- Hebrew Free Loan Society of Greater Philadelphia

- Women’s Development Bank

- Ubank

- Unitus Labs

- Microfinance Information Exchange

- BRAC (organization)

- Opportunity International

- Association for Social Advancement

- Energy in Common

- Rise Asset Development

- Community First Fund

- Aga Khan Agency for Microfinance

- Hebrew Free Loan Association of Northeast Ohio

- Lendwithcare

- World Relief

- FINCA International

- Responsibility investments

- Amanah Ikhtiar Malaysia

- One Acre Fund

- Dedebit Credit and Savings Institution SC

- Seven Bar Foundation

- Farmers’ Bank of Rustico

- Zidisha

- MYC4

- Al-Qard Al-Hasan Association

- List of microcredit lending websites

- Alliance for Financial Inclusion

- Small Enterprise Foundation

- MicroFinance Institutions Network

- Center for Community Self-Help

- Friends of Women’s World Banking

- United Nations Capital Development Fund

- Fredericks Foundation

- Financial Access Initiative

- South Pacific Business Development

- MicroInsurance Centre

- Entrepreneurs du Monde

- Working Women’s Forum

- Project Enterprise

- Freedom from Hunger

- YiNongDai

- Esperanza International

- Oikocredit

- Microenterprise Education Initiative

- Bank of Taizhou

- ACCION U.S. Network

- Microfinance Investment Support Facility for Afghanistan

- Zidisha

- Faulu Microfinance Bank Limited

- National Economic Empowerment Fund Limited of Malawi

- Yetu Microfinance

- SMEP Microfinance Bank

- Kenya Women Microfinance Bank

- Choice Microfinance Bank

- HBL Microfinance Bank

- Thengamara Mohila Sabuj Sangha

- First MicroFinance Bank (Afghanistan)

- IPR Microfinance Institution

- Grameen Bank

- First MicroFinance Bank (Tajikistan)

(Source: wikipedia.org)

Popular Cooperative Banking Companies

| Name | Country | Type | Notes |

| Raiffeisen Bank International | Austria | Bank (Public Aktiengesellschaft) | Owned by the regional Raiffeisen Bank of the Austrian states |

| Crédit Agricole SA | France | Bank (Public S.A.) | Individuals own the majority of the local banks in the group. |

| Islami Co-operative Bank Ltd. | Bangladesh | Central Co-Operative Bank | First Islamic and the largest Co-operative Bank in Bangladesh |

| Navy Federal Credit Union | US | Credit union | |

| Desjardins Group | Canada | Credit union federation | A leading bank in Quebec |

| Bank Rakyat | Malaysia | Islamic cooperative bank | The second national cooperative bank in Malaysia was founded in 1954 |

| DZ Bank | Germany | Bank | Owned by three-quarters of all German cooperative banks |

| Rabobank | Netherlands | Bank | Credit union federation |

| Crelan | Belgium | Bank | Independent from Crédit Agricole since 2015 |

| Nationwide Building Society | UK | Building society | World’s largest building society |

| Bank Australia | Australia | Bank | Australia’s first customer-owned bank |

| POP Pankki | Finland | Credit union federation | |

| Laboral Kutxa | Spain | Credit union | Part of Mondragon Corporation |

| Bank of Australia | Australia | Bank | Customer-owned bank |

| Nonghyup | South Korea | The banking division of the agricultural cooperative | Approximately US$230 billion in loans |

(Source: wikipedia.org)

Microfinance Overview

#1. Microfinance Statistics – Growth and Trends in 2023 and 2024

Microfinance has become essential to the global financial system, providing small loans and financial services to low-income individuals and businesses. In 2023 and 2024, microfinance institutions (MFIs) continued to expand their reach, particularly in developing countries. These institutions offer a way to support entrepreneurs who do not have access to traditional banking services, playing a significant role in economic growth and poverty reduction.

According to recent Microfinance Statistics, the global microfinance market was valued at approximately **US$174 billion** in 2023. This reflects an annual growth rate of around **5.8%** from the previous year. In 2024, the market is expected to grow, reaching **US$184 billion**. This steady growth is driven by increasing demand for financial inclusion, especially in regions like South Asia, Sub-Saharan Africa, and Latin America.

#2. Major Players in Microfinance

Several large institutions dominate microfinance, providing billions of US loans annually. In 2023, BRAC, one of the world’s largest MFIs, disbursed loans amounting to **US$1.7 billion**, helping over **7 million** people. Similarly, FINCA International provided microloans worth **US$1.1 billion**, targeting low-income individuals in 20 countries. These institutions are critical sector drivers, influencing Microfinance Statistics and trends globally.

In addition to the large players, smaller regional MFIs significantly impact the market. For instance, Grameen Bank in Bangladesh reported loans totaling **US$750 million** in 2023, while Ujjivan Small Finance Bank in India provided microloans worth **US$580 million**. These institutions contribute to the broader microfinance ecosystem, supporting individuals in rural areas with limited access to traditional banking.

#3. Regional Analysis

The demand for microfinance services varies across different regions. In South Asia, particularly in countries like India and Bangladesh, microfinance is crucial in poverty alleviation. In 2023, India alone accounted for approximately **30%** of the global microfinance market, with over **US$52 billion** in loans distributed. By 2024, this figure is expected to increase to **US$55 billion**, further reinforcing India’s position as a leader in microfinance.

In Sub-Saharan Africa, microfinance is expanding rapidly due to the high number of unbanked individuals. In 2023, the region represented around **15%** of the global market, with loans worth **US$26 billion** disbursed. By 2024, the market share in this region is projected to grow to **17%**, with loans reaching **US$31 billion**. Countries like Kenya, Nigeria, and Tanzania are seeing significant growth in microfinance institutions as more people seek financial independence through small businesses.

In Latin America, microfinance supports entrepreneurs in countries such as Mexico, Peru, and Bolivia. In 2023, the region’s microfinance market was valued at **US$29 billion**, accounting for **16%** of the global market. Projections for 2024 indicate a growth to **US$31 billion**, driven by increased demand for financial services among low-income populations.

#4. Key Market Trends

Several key trends are shaping the future of the microfinance industry. First, the adoption of digital technologies has transformed the sector. Mobile banking and digital lending platforms have made it easier for MFIs to reach clients in remote areas. In 2023, over **40%** of microfinance transactions were conducted digitally, a figure expected to rise to **45%** by 2024. This shift to digital platforms has reduced transaction costs and improved the efficiency of loan disbursement.

Another significant trend in the Microfinance Statistics 2023 is the increased focus on women’s empowerment. Women make up around **80%** of microfinance borrowers globally, and in 2023, MFIs directed over **US$100 billion** towards women-led businesses. This trend will continue in 2024, with more funding flowing into women-focused enterprises. MFIs recognize women’s critical role in economic development, especially in low-income households.

Moreover, the rise of social impact investing has influenced the microfinance sector. Investors increasingly seek opportunities that provide both financial returns and positive social outcomes. In 2023, social impact investments in microfinance totaled **US$12 billion**, a **10%** increase from the previous year. This trend will continue in 2024 as more investors seek ethical investment options supporting financial inclusion.

#5. Challenges in the Microfinance Sector

Despite the positive growth highlighted in Microfinance Statistics, the industry faces several challenges. One major issue is the rising number of non-performing loans (NPLs). In 2023, NPLs accounted for **7.5%** of total microfinance loans, up from **6.8%** in 2022. This increase is due to economic instability in several developing countries, making it harder for borrowers to repay their loans.

Another challenge is the regulatory environment. While some countries have developed robust frameworks to support microfinance, others need more regulations, making it easier for MFIs to operate. In 2023, regulatory challenges were particularly prevalent in Sub-Saharan Africa and Southeast Asia. These regulatory issues are expected to persist in 2024, potentially limiting the expansion of microfinance services in certain areas.

Lastly, funding remains a concern for many MFIs. Although large institutions like BRAC and FINCA have access to significant financial resources, smaller MFIs often need help to secure financing. In 2023, only **35%** of MFIs worldwide could meet their funding targets, which will likely remain the same in 2024.

#6. Future Outlook

Looking ahead, the future of microfinance appears promising. The market is projected to grow, particularly in regions with large unbanked populations. Microfinance Statistics suggest that by 2024, the global market could surpass **US$184 billion**, driven by increased demand for financial services in emerging economies. Digital transformation and social impact investing will likely remain critical trends shaping the industry’s evolution.

In conclusion, the microfinance sector is expanding, with new opportunities and challenges emerging as we move into 2024. The Microfinance Statistics for 2023 demonstrate the sector’s resilience and crucial role in promoting financial inclusion and economic development. As the industry grows, it will continue to provide essential support to millions of people worldwide, helping them build sustainable businesses and improve their livelihoods.

Conclusion

The microfinance sector stands at a crucial juncture, demonstrating remarkable resilience and growth while facing evolving challenges and opportunities. Microfinance Statistics showcases the industry’s expansion to a US$174 billion market in 2023, with projections reaching US$184 billion by 2024, underscoring its vital role in global financial inclusion.

As the sector evolves, integrating digital technologies, emphasizing sustainable practices, and focusing on social impact investing will likely shape its trajectory. The success of the financial system indicates the sector’s enduring relevance in promoting financial inclusion and economic development globally.