Introduction

Satellite Internet Statistics: In 2026, the satellite internet industry seems to be going through this kind of really transformative phase, mostly because low Earth orbit, or LEO, constellations are expanding so fast, plus there’s a growing need for broadband where the land lines and fiber are thin or just not there. On top of that, government budgets are being redirected toward digital inclusion programs, so the whole environment feels more pushy and accelerated.

At the same time, traditional geostationary satellite systems are getting supplemented, and sometimes outright replaced, by the newer style networks that come from providers like SpaceX Starlink and Eutelsat OneWeb. You can also see emerging entrants, such as Amazon Project Kuiper, showing up in the picture. The result is that satellite connectivity is slowly but surely becoming a key part of worldwide telecom infrastructure, not only for home internet but for aviation, maritime operations, business networks, defense communications, and even direct-to-device mobile connectivity.

This article explores key satellite internet statistics, highlighting major satellite categories and their current market positions within the global connectivity landscape.

Editor’s Pick

- The Ka-Band segment controls 31.25% of market revenue and is forecast to grow at an 18.22% CAGR.

- Two-way satellite internet services represent 51.05% of the market, which points to the shift toward interactive broadband connections.

- LEO satellite networks reached 42.10% market share in 2025.

- In 2026, Starlink ran 10,302 active satellites, keeping a constellation almost 16 times larger than OneWeb’s 654 satellites.

- Starlink’s long-term plan aims for 42,000 satellites.

- More than 41,000 satellites are planned across Starlink, Kuiper, Qianfan, Xingwang, and Amazon.

- Kuiper is aiming for download speeds of up to 400 Mbps.

- Starlink’s Direct-to-Device setup already works with 150,000+ daily users, and it pulled in 1.8 million.

- Then there’s AST SpaceMobile, supported by 50+ mobile operators that collectively cover close to 3 billion subscribers.

- SpaceX’s defence-related space agreements are estimated at around USD 10–12 billion, so that tells you satellite networks are playing a bigger and bigger part in national security.

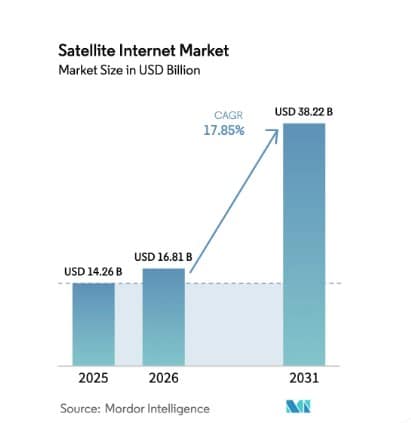

Satellite Internet Market Outlook

(Source: mordorintelligence.com)

- Looking at the satellite internet market in 2025, there’s this very noticeable move toward higher capacity systems, stronger enterprise uptake, and next-generation low Earth orbit (LEO) designs.

- In terms of frequency, Ka-Band came out as the biggest chunk, grabbing 31.25% of the total revenue, and it’s expected to keep the momentum going with an 18.22% CAGR through 2031.

- On the connectivity side, demand is clearly leaning into interactive services, and two-way satellite internet solutions were at 51.05% market share in 2025, with growth projected at 17.35% CAGR.

- Commercial demand stays the main money engine, since the commercial and enterprise segment makes up 53.60% of the market, while residential is set to grow the fastest as a user group at an 18.15% CAGR.

- Even the way satellites get deployed is evolving. LEO constellations took 42.10% of the market in 2025 and keep leading expansion with an 18.05% CAGR, which basically mirrors the rising investment in low-latency broadband services.

- By application, backhaul and rural cell-site connectivity represented 37.90% of the market, highlighting satellite internet’s role in bridging connectivity gaps. Meanwhile, mobility applications are expected to grow fastest at 18.52% CAGR.

- Regionally, North America held a dominant 34.20% market share, while Asia-Pacific is projected to be the fastest-growing region with an 18.50% CAGR through 2031.

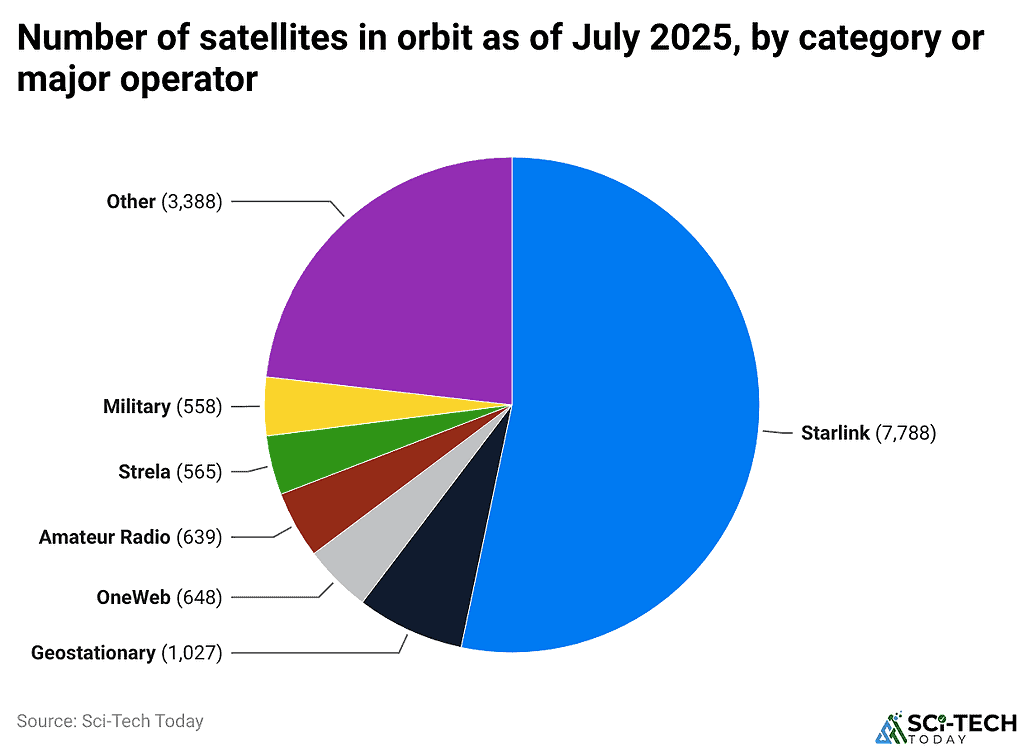

Active satellites By Category/Operator 2025

(Reference: statista.com)

- Data from 2025 did kind of show how fast the satellite internet sector has changed the whole space industry.

- The most noticeable number was Starlink’s 7,788 active satellites, which basically meant more than 50% of all active satellites orbiting Earth, as of July 2025.

- Starlink’s setup leans heavily on low Earth orbit (LEO) satellites, a way of doing it that aims for high-speed internet while keeping latency lower than older satellite approaches.

- For wider coverage, the company has described plans that are really not small, talking about a constellation of up to around 42,000 active satellites later on. In other words, it would enlarge its head start in that fast-moving, space-based communications space.

- OneWeb, Starlink’s closest LEO rival, had 648 satellites in operation as of July 2025.

- Even though it is way smaller, OneWeb built up some extra strength after its merger with Eutelsat in September 2023, making a combined organization that can work across both LEO and geostationary satellite markets, roughly speaking.

- On the money side, the picture is equally interesting. Eutelsat said it brought in €1.21 billion in revenue in fiscal year 2024, and it also expects the merged Eutelsat OneWeb operation to reach roughly €2 billion in annual revenue by 2027.

- Starlink’s big numbers are now sort of the yardstick, while Eutelsat OneWeb is trying to position itself as the most meaningful, serious challenger in the global satellite internet race that is still evolving, every quarter it seems.

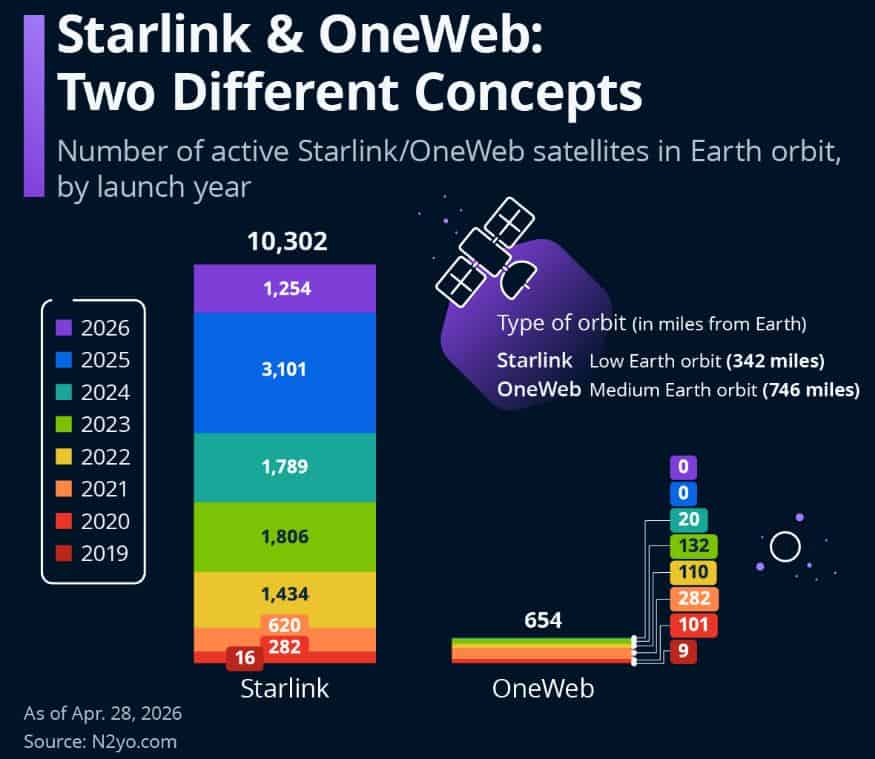

Starlink Vs. OneWeb – The Race To Space

(Source: statista.com)

- The global satellite internet market is mostly handled by two big low-Earth-orbit operators, but the scale difference between them is really noticeable.

- As of April 2026, Starlink had about 10,302 active satellites up and running, while OneWeb, it says it finished its constellation with 654 satellites total (648 in service, plus 6 used for testing).

- What stands out is the deployment tempo.

- From 2019 through 2026, the company behind Starlink basically kept stacking up, adding more than 10,000 satellites, like 3,101 satellites launched in 2025, and then another 1,254 added in early 2026.

- By contrast, OneWeb wrapped things up with just over 650 satellites, and their idea seems more like “ wider coverage per satellite ” rather than trying to win purely by sheer numbers.

- Starlink satellites fly at roughly 342 miles (550 km) above Earth, while OneWeb sits closer to about 746 miles (1,200 km).

- That lower altitude for Starlink generally helps with latency, so real-time internet works better for things such as video streaming, gaming, and business communications, at least that’s the expectation people talk about.

- When you look at the constellation size, Starlink’s fleet ends up nearly 16x bigger than OneWeb’s. That sheer scale can mean tighter global coverage and more room for network capacity.

- OneWeb, however, tends to make up for it with higher-altitude satellites, since each spacecraft can reach larger geographic regions, which then cuts down the total satellite count they need.

- New teams are showing up, including Amazon’s Project Kuiper, along with China’s Qianfan and Xingwang constellations, and they’re starting actual deployment work.

- So the next phase of the satellite broadband race looks like it will involve multiple major players, not only these two.

- Starlink seems to go all in on scale and capacity, with that huge constellation of more than 10,000 satellites.

- While OneWeb is more about efficiency, using a network of 654 satellites that operate at higher orbital altitudes. Either way, both approaches are clearly nudging how global satellite connectivity is going to look later.

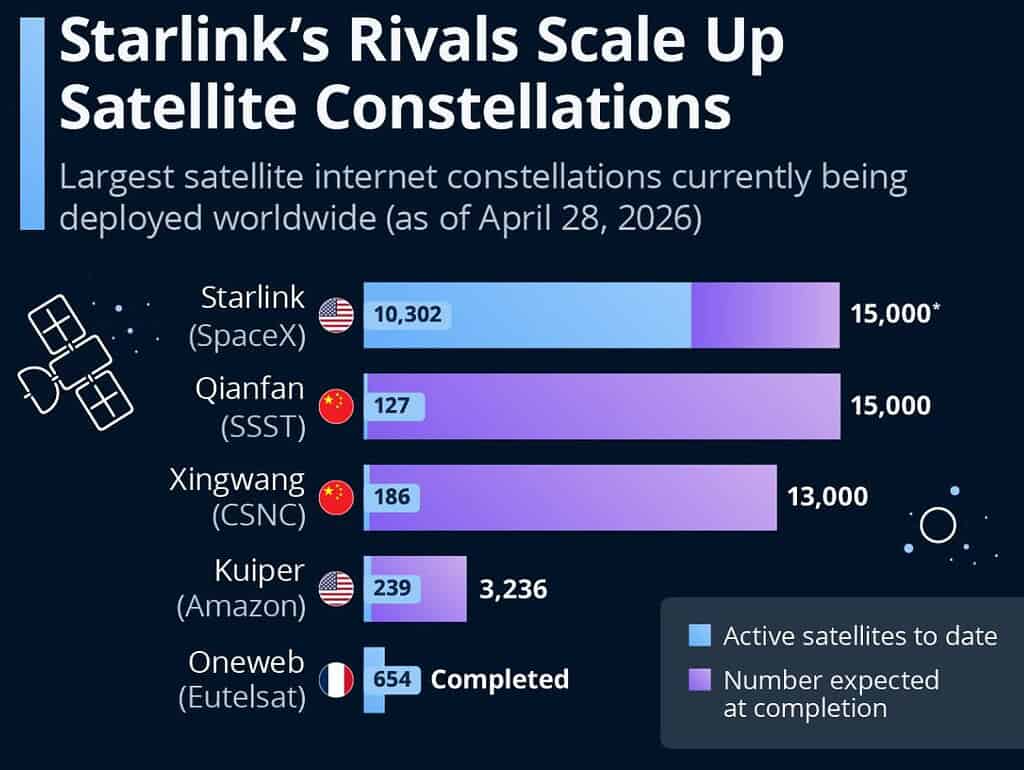

The Mega-Constellation Race – The Future Of Global Satellite Internet

(Source: statista.com)

- In 2026, the satellite internet space is turning into a big infrastructure race, where companies and governments deploy thousands of satellites to land broad coverage worldwide, or something close to that.

- The numbers indicate that Starlink SpaceX remains the clear frontrunner. It has 10,302 active satellites, which is about 85% of its initial Phase 1 target of 12,000 satellites.

- In relation to its eventual 42,000-satellite mega-constellation plan, that’s around 24.5%.

- China is coming up fast as the strongest challenger, though. Qianfan (SSST) has put 127 satellites into orbit aimed at a 15,000-satellite target.

- Xingwang (CSNC) has already launched 186 satellites, with plans for a 13,000-satellite constellation. Together, these two Chinese efforts could total 28,000 satellites, which is almost twice what Starlink is targeting right now.

- At the same time, Amazon’s Kuiper constellation has 239 active satellites. It is moving toward a planned fleet of 3,236 satellites, so it’s positioning itself as a serious long-term competitor in the broadband arena.

- Meanwhile, OneWeb (Eutelsat) feels different. Its constellation is basically already done with 654 satellites, making it the only major operator in this set that actually finished its first deployment step, not just started it.

- More than 41,000 satellites are planned across these five major constellations, highlighting the enormous investment being directed toward global satellite connectivity and the next generation of space-based internet services.

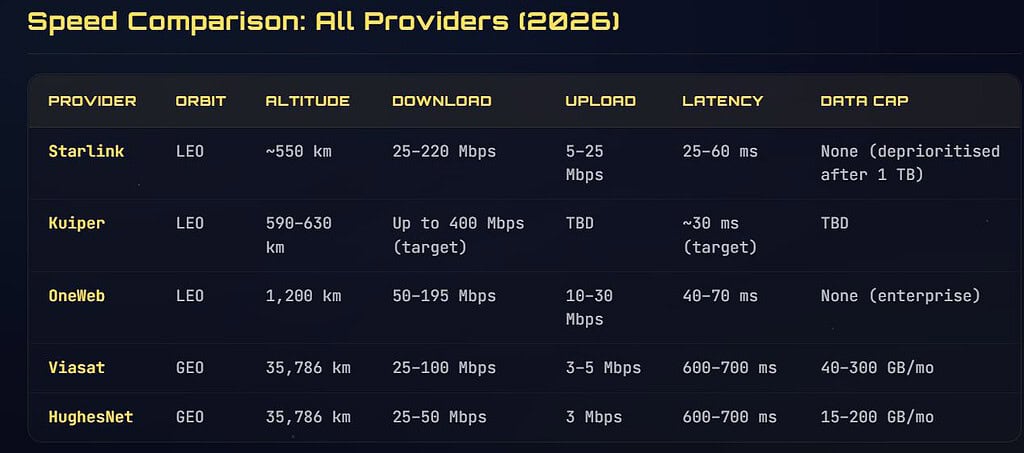

Satellite Internet Speed Battle 2026

(Source: orbitalradar.com)

- The 2026 satellite internet market kinda splits hard between newer Low Earth Orbit (LEO) setups and old-school Geostationary Earth Orbit (GEO) providers.

- Starlink is still leading the consumer side, with download speeds around 25–220 Mbps, upload speeds 5–25 Mbps, and latency somewhere between 25–60 milliseconds. That’s coming from an orbit of roughly 550 km.

- The offer is basically “unlimited” for most users, but it does deprioritize traffic after you hit about 1 TB of monthly data.

- Amazon LEO, while still in the process of rolling things out, is aiming for downloads up to 400 Mbps and latency closer to 30 ms. It runs at altitudes in the ballpark of 590–630 km, and it could end up as a fresh benchmark for satellite broadband.

- OneWeb, though, flies higher at about a 1,200 km orbit, and it tends to land at 50–195 Mbps download, with latency around 40–70 ms. Most of its focus is on enterprise and government users, and it doesn’t rely on the same kind of fixed data caps.

- Meanwhile, the GEO guys have a pretty obvious disadvantage, mainly because the round-trip timing is brutal.

- Viasat and HughesNet both operate at 35,786 km, and they deliver downloads in the 25 100 Mbps range for Viasat, while HughesNet sits around 25–50 Mbps.

- But latency stays high, about 600–700 milliseconds, so interactive or real-time uses feel less responsive. Data allowances vary by plan, typically from 15 GB up to 300 GB each month.

- Overall, the figures really suggest that LEO constellations are reshaping this whole satellite broadband space.

- The latency drops by something like 90–95% versus GEO systems, and speeds are getting competitive enough that providers like Starlink, Kuiper, and OneWeb are laying the groundwork for the next phase of worldwide internet connectivity.

Direct-To-Device (D2D) and Smartphone Integration

- Direct-to-Device (D2D) satellite connectivity has really shown up as one of the more transformative things in telecommunications during 2026.

- Instead of using the usual satellite setup, D2D technology lets normal smartphones grab cellular and internet access straight from satellites, without any specialized hardware, so kinda simpler than people expected, at least in practice.

- According to CNET, the early frontrunner right now is Starlink’s T-Satellite service. It was launched with 657 dedicated satellites, and it covers about 500,000 square miles of U.S. territory that was previously unserved.

- Within just six months after commercial operation, the service already supported connectivity for over 150,000 users every day.

- There was a lot of interest, like exceptionally strong demand, with nearly 1.8 million beta sign-ups logged before the official launch.

- T-Satellite costs only USD 10 per month, and compatibility already covers a large share of the roughly 350 million active smartphones in the United States.

- In terms of what it feels like, current performance is in the 2–4 Mbps range, while latency stays under 100 milliseconds, which works well for things like messaging, navigation, voice calls, and emergency communications, generally the stuff people care about first.

- But competition is not waiting around. AST SpaceMobile, supported by more than 50 mobile network operators that represent nearly 3 billion subscribers, rolled out BlueBird satellites 8–10 in June 2026.

- The company says it wants to deploy 45–60 satellites by the end of 2026, then push out to around 90 satellites worldwide eventually.

- On the financial side, AST reported more than USD 1 billion in contracted revenue commitments, plus roughly USD 3.2 billion in liquidity to keep the rollout moving.

- According to a CNBC report, another big thing kind of surfaced thanks to Amazon’s USD 11.57 billion purchase of Globalstar back in April 2026.

- Globalstar’s current network has 24 LEO satellites, and the way it plugs into iPhone satellite services pretty much gives Amazon fast access to an existing crowd of users plus spectrum assets that are, honestly, hard to replicate.

- Overall, the numbers suggest that D2D connectivity is drifting from a small, emergency-only kind of setup into something far more mainstream, like a regular communications platform.

- With hundreds of satellites already out there, millions of potential customers, and multi- billion-dollar commitments from Starlink, AST SpaceMobile, and Amazon, 2026 feels like the starting point of a fresh cycle where mobile coverage is coming more from space, rather than cell towers.

The Geopolitical Race and Defense Sector Adoption

- In 2026, you can see a clear shift in the space business. Satellite mega constellations are moving from commercial broadband networks toward strategic national security tools.

- The metrics really show how quickly governments are folding commercial space infrastructure into defense, intelligence, and related operations.

- The United States, in particular, has boosted military space capabilities through commercial partnerships.

- SpaceX’s Starshield unit operates under a USD 1.8 billion classified contract with the National Reconnaissance Office, the NRO.

- By mid-2026, at least 183 Starshield satellites were said to be in orbit at around 310 km altitude, supporting intelligence, surveillance, and reconnaissance missions, pretty much nonstop in practice.

- The U.S. Space Force has also gone ahead and kicked off the MILNET program, kinda like a planned constellation of about 480 military communication satellites, meant to deliver secure and self-reliant space-based links.

- At the same time, SpaceX sits on USD 5.9 billion in National Security Space Launch (NSSL) contracts running through 2032, plus there’s a reported USD 2 billion allocation that’s tied to missile-defense efforts.

- SpaceX’s defense-related portfolio that’s been publicly talked about is usually put in the USD 10–12 billion range.

- The Qianfan (Thousand Sails) constellation is aiming for roughly 10,000–15,000 satellites, while the Xingwang (GW) network is said to be headed toward 12,992 satellites.

- As of June 2026, Qianfan had already put around 200 satellites into orbit, including 54 satellites sent up across three different missions in April, May, and June 2026.

- Each launch went with 18 satellites per rocket, which kind of shows an aggressive cadence, not a slow and steady thing.

- China’s Xingwang constellation hit 162 satellites by May 2026, after starting from zero satellites in August 2024, and then reaching operational capability in just 22 months. It also ran its first maritime connectivity demonstration in January 2025, and that test was used to validate communications performance in the real world.

- All the above data points hint at an emerging geopolitical rivalry in low Earth orbit.

- The United States is leaning on commercial operators through defense agreements that add up to many billions, and China is pouring resources into constellations that exceed 10,000 satellites.

- As the pace of deployment keeps speeding up, these satellite networks are becoming strategic backbone infrastructure, the kind that supports communications, intelligence collection, and national security across the globe.

Conclusion

In 2026, the satellite internet industry is moving away from this niche connectivity thing and more toward a core part of worldwide telecommunications. A bunch of things are pushing it along, like fast rollouts of low Earth orbit constellations, more direct-to-device offerings, and the steady demand for broadband in areas that are still underserved. Starlink basically stays the biggest operator in terms of scale, but OneWeb, Amazon Kuiper, and a growing set of Chinese constellations are also making the space more competitive.

At the same time, satellite networks are not just a commercial play anymore; they’re turning into strategic tools for governments, defense agencies, and other critical communications setups. And since tens of thousands of additional satellites are expected to be launched in the next ten years, satellite internet looks set to shift how the world connects.

FAQ

Starlink currently operates about 10,302 active satellites in orbit.

LEO networks represent 42.10% of the global market.

Starlink provides roughly 25–220 Mbps download speeds, plus 25–60 ms latency.

D2D lets normal smartphones connect directly to satellites without special equipment or add-on hardware.

Over 41,000 satellites are projected across the world’s leading broadband constellation efforts.