Introduction

Programmatic Advertising Statistics: Programmatic advertising has basically turned into the main way people buy and sell digital ads in 2026, and it lets marketers automate media buys with AI, machine learning, and real-time bidding (RTB). But as third-party cookies fade away and privacy rules get tighter, advertisers are pushing more money into first-party data, contextual placement, retail media, and AI-driven optimization. Lots of global brands are now shifting most of their digital ad budgets into automated channels, since programmatic platforms can deliver sharper audience reach, better campaign efficiency, and a more trackable return on investment.

These figures show how fast the Programmatic advertising market is growing, where investments are going, the persistent fraud issues, how quickly AI is being adopted, plus what the outlook looks like through 2026.

Editor’s Choice

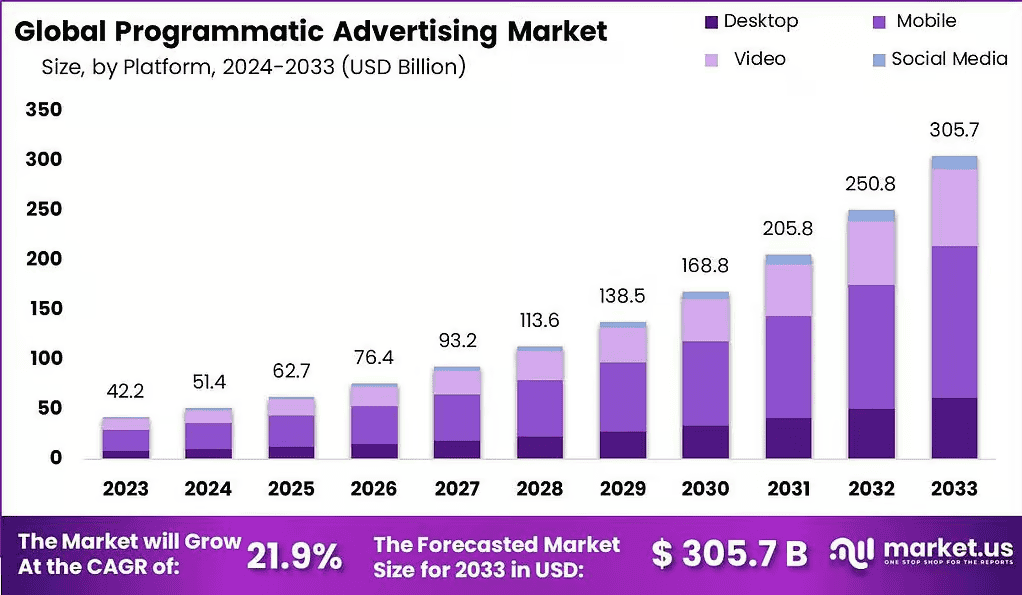

- Programmatic advertising is moving forward really fast, with the global market forecasted to jump from USD 42.2 billion (2023) to USD 305.7 billion by 2033 at a 21.9% CAGR, which suggests long-term momentum will continue.

- Global programmatic ad spending is expected to hit USD 821 billion in 2026, which is basically another sign that automation is the dominant engine inside digital advertising.

- North America leads with 41% of global programmatic spending (USD 337 billion), and 92% of display ads are being bought programmatically, so it kind of sets the benchmark for everyone else.

- Mobile still acts like the core of programmatic advertising, taking 50% of total ad budgets, meaning phones remain the main device for getting audience attention.

- Display advertising continues to dominate at USD 298 billion (36.3%), while Retail Media is the quickest grower, rising 34.1% year over year.

- Connected TV (CTV) is reshaping premium advertising, reaching USD 36 billion in spend, with 28% annual growth, and around 71% of CTV ads traded programmatically.

- Ad fraud is draining almost USD 71 billion each year; roughly 8.7% of global programmatic spending slips away.

- CTV ends up taking the bigger hit; it shows a 12.4% fraud rate, while Private Marketplaces tamp it down to 1.2%.

- 71% of the world’s top 200 advertisers are moving to clean room technologies.

Programmatic Advertising Market Size

(Source: market.us)

- The programmatic advertising market is moving into a phase of quick growth, pushed by automation and data-led media buying.

- Like, Market.us says the global programmatic advertising market was worth around USD 42.2 billion in 2023 and should climb up to USD 305.7 billion by 2033, with a 21.9% CAGR.

- In 2023, the real-time bidding segment had about 45%, so it became the leading method for transactions.

- At the same time, mobile platforms hold a 50% share, basically confirming that smartphones are still the main route for programmatic campaigns.

- For ad formats, display advertising takes the lead with 40% market share, which shows it keeps staying important for digital media strategies.

- Over 60% of all digital ad spend is now handled through programmatic platforms, so adoption is spreading across many industries.

- Also, industry estimates suggest that global programmatic advertising budgets will rise by more than USD 300 billion across the next four years, reflecting a lot of trust in automated ad tech.

- Around 50% of programmatic ad budgets go to mobile, and mobile programmatic ad spending has already passed USD 32.1 billion.

- Looking ahead, forecasts add that the whole industry could reach USD 62.7 billion by 2025, which further reinforces the move toward AI-driven, automated advertising ecosystems.

Regional Programmatic Ad Spending Highlights Strong Global Growth

(Source: digitalapplied.com)

- Programmatic advertising still kind of dominates the digital advertising space, and global spend is on track to hit USD 821 billion in 2026, which is about a 9.0% year-over-year lift.

- North America keeps being the biggest regional market, bringing in USD 337 billion, or roughly 41% of overall programmatic spending, and in fact, 92% of display advertising there is bought programmatically, which is honestly pretty standout.

- Asia-Pacific (APAC) lands next with USD 263 billion, 32% of global spend, and it also shows a solid 11.6% annual growth rate, while 88% of display advertising gets traded through programmatic channels.

- The regional numbers suggest that programmatic advertising has effectively become the normal way of buying digital media almost everywhere.

- Europe contributes USD 172 billion, holding 21% of the global share, and 89% of display advertising is delivered programmatically.

- Meanwhile, Latin America is smaller at USD 31 billion (3.8%), but it still manages a robust 13.1% year-over-year growth.

- The Middle East & Africa comes in at USD 18 billion (2.2%), yet it leads the regions with the fastest growth rate of 15.4%, and even if total spend is lower, 76% of display advertising in the Middle East & Africa is already programmatic, so adoption is moving pretty quickly.

- The above numbers mean mature markets keep pulling in the most dollars, but the emerging regions are expanding faster, so programmatic advertising is turning into a real global growth engine.

Programmatic Ad Spending By Channel

(Source: digitalapplied.com)

- Programmatic advertising keeps moving ahead across basically every big digital channel, but the growth now seems even more gathered into high-engagement formats like retail media, Connected TV (CTV), and digital video.

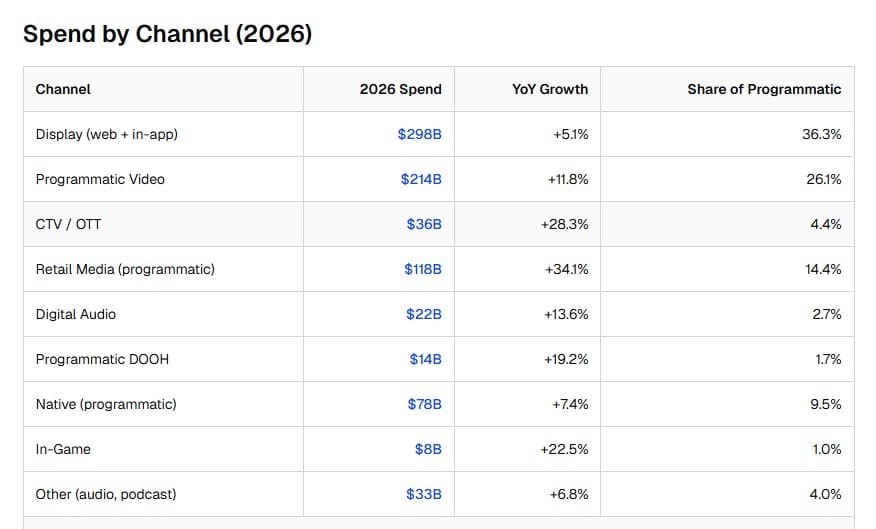

- In 2026, Display advertising is still the biggest programmatic lane, with USD 298 billion in spending, so 36.3% of all programmatic investment, even if the year-over-year movement is comparatively small at 5.1%.

- Programmatic Video is next at USD 214 billion, which comes to 26.1% of total spend, and it’s also rising faster by 11.8%, suggesting that video keeps pulling in the bigger ad budgets as consumer watching patterns shift.

- The sharpest momentum is kind of moving toward commerce-powered ecosystems and streaming platforms.

- Retail Media programmatic spending reaches USD 118 billion in 2026, delivers the strongest growth rate of 34.1%, and grabs 14.4% of total programmatic advertising, so it sits among the fastest-expanding pockets.

- CTV/OTT advertising lands at USD 36 billion, grows an impressive 28.3% year over year, and accounts for 4.4% of overall programmatic spending, which fits the idea that people are shifting audiences toward streaming services.

- In-Game advertising hits USD 8 billion after 22.5% growth, while Programmatic Digital Out-of-Home (DOOH) comes in at USD 14 billion, with a 19.2% increase, pointing to rising confidence from advertisers in immersive experiences and digital-first settings.

- More mature channels keep delivering pretty steady expansion, at least that’s what the numbers seem to say.

- Native advertising is sitting at USD 78 billion, which is 9.5% of programmatic spend, and it’s moving up at 7.4% each year.

- Meanwhile, Digital Audio grows 13.6% to reach USD 22 billion, so it accounts for 2.7% of all spending.

- Then the other programmatic stuff, like podcasts and extra audio inventory, adds up to USD 33 billion. That’s 4.0% of worldwide spending, with 6.8% growth.

- So, even if display still counts as the biggest bucket, the next wave of programmatic investment is getting pulled more by video, retail media, streaming television, gaming, and omnichannel digital experiences.

Connected TV Programmatic Advertising

(Source: digitalapplied.com)

- Connected TV, or CTV, is becoming the fastest-growing piece of programmatic advertising, and it really points to how quickly audiences are moving into streaming.

- In 2026, global programmatic CTV spend is expected to hit USD 36 billion, which is basically a solid 28% jump year-over-year.

- Programmatic transactions now make up 71% of all CTV advertising spend, so it’s pretty clear that automated media buying has turned into the main method for streaming television.

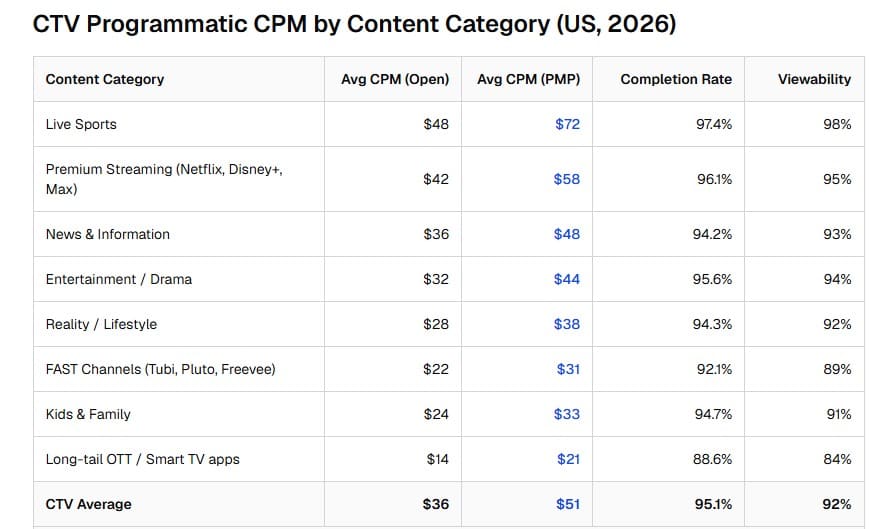

- Live Sports is still the top in ad value, showing an average CPM of USD 48 in open auctions, and USD 72 when it’s private marketplaces (PMPs). At the same time, it manages a 97.4% completion rate, plus 98% viewability.

- Premium streaming services, like Netflix, Disney+, and Max, tend to post USD 42 CPMs in open auctions and USD 58 CPMs in PMPs. They also bring 96.1% completion rates and 95% viewability, which is not a small detail.

- Across the broader market, the typical CTV CPM lands around USD 36 for Open and USD 51 for PMP, backed by a 95.1% video completion rate along with 92% viewability, which all suggests stronger viewer engagement.

- FAST channels average USD 22 CPMs in open buys, USD 31 in PMPs, and they still reach 92.1% completion with 89% viewability.

- Meanwhile, Long-tail OTT platforms sit lower at USD 14 open CPMs, USD 21 PMP CPMs, with an 88.6% completion rate and 84% viewability.

- The above figures imply advertisers are more and more ready to fund premium CTV spaces since they deliver both high engagement and campaign metrics that are actually measurable.

Programmatic Ad Fraud and Brand Safety

- Fraud risks now vary quite sharply across inventory types. Connected TV (CTV) has sort of emerged as the most vulnerable programmatic channel, showing an adjusted fraud rate around 12.4%, while the fraud schemes aimed at CTV rose by 140% year over year.

- According to Pixalate CTV Fraud Reports (2026), by comparison, Private Marketplaces (PMPs) still look like one of the safer buying environments, with fraud rates down to about 1.2% across premium publisher inventory. That big difference makes it pretty clear that inventory quality is becoming as important as audience targeting when someone is managing advertising budgets.

- These numbers also suggest advertisers need to judge campaign success beyond the usual stuff, like clicks and conversions.

- More money going into premium inventory, plus better fraud detection, continuous behavioral monitoring, and lead verification, is starting to feel not just helpful but essential for protecting media efficiency.

- AI-driven fraud keeps evolving, lowering exposure to higher-risk inventory, while pushing spending toward trusted supply routes, which offers a more durable plan for both performance improvement and budget safeguarding.

Performance Impact and Recovery

- The move into a privacy-first, signal-degraded world created real measurable performance problems, especially for performance marketers, yet the market sort of bounced back over time with investments in first-party data and solutions made for privacy-focused measurement.

- At first, brand campaigns showed a 6–9% drop in measured efficiency after cookie deprecation, but then came back hard, and by Q4 2025, they were usually within 2–4% of pre-cookie results.

- Direct-response efforts were hit more, with efficiency dipping 12–18% at the height of disruption, then they improved again, getting to roughly 4–7% of older performance as teams rolled out authenticated identifiers and clean room technologies.

- Even if a 47% match rate gives a workable base for privacy-first targeting, it still comes in pretty lower than the 68% match rate people got used to back in the peak third-party cookie era.

- Frequency management also kind of shows the real value of authenticated data, because you get 71% accuracy on authenticated inventory, versus only 38% accuracy on cookieless inventory. Still, that’s not the same as the 92% accuracy that was achieved during the cookie era.

- On top of that, privacy-safe measurement keeps rolling forward, with 71% of the world’s top 200 advertisers running at least one clean-room integration.

- 44% have already gone further, with three or more clean-room environments in place.

- The above numbers suggest the whole industry has moved away from leaning on third-party cookies and toward building more resilient, privacy-first advertising approaches. These are centered on trusted first-party data and those secure collaboration platforms, which now feel like the norm.

Conclusion

Programmatic advertising is kinda the backbone of the global digital ads ecosystem, pulled along by AI, automation, and also privacy-first tools. As spend goes past USD 821 billion in 2026, more advertisers are kinda leaning into first-party data, retail media, Connected TV, and contextual targeting, so campaigns run better, and audiences stay more engaged. Meanwhile, fraud losses keep climbing, and privacy rules are getting stricter, so the way media is purchased is changing too, which makes premium inventory and advanced verification tools feel like “must-have” investments.

Still, with steady market growth, fast AI adoption, and continuous innovation, programmatic advertising remains one of the most influential and pretty resilient parts of global digital marketing.

FAQ

Programmatic advertising is the automated buying and selling of digital ads using AI, machine learning, and real-time bidding.

Global programmatic advertising spending is forecasted to hit around USD 821 billion in 2026.

Retail Media is growing the quickest, with an increase of 34.1% year over year in 2026.

It’s estimated that advanced ad fraud wastes close to USD 71 billion, about 8.7% of overall global programmatic ad spending.

First-party data helps with better targeting precision, supports privacy compliance, and keeps campaign performance stable as third-party cookies fade away.