Introduction

Commercial Space Industry Statistics: In 2026, the commercial space industry is in this new phase that feels like it’s expanding really fast, like, moving away from a mostly government-run thing and into a worldwide marketplace powered by private capital. You can see it in satellite services, reusable launch vehicles, space-based communications, Earth observation, and this newer lunar commerce that’s starting to matter more and more.

Overall, it’s now one of the quickest growing high-tech sectors, and that’s not just vibes—declining launch costs, higher rates of satellite deployment, and the ongoing appetite for broadband connectivity across the world are all pushing it forward. Firms like SpaceX, Blue Origin, Rocket Lab, Planet Labs, plus a bunch of international startups, are changing the underlying numbers for space exploration. And because governments are partnering more and more with private operators, commercial space work is starting to sit at the center of global telecoms, defense, navigation, climate monitoring, and even the early stages of off-world infrastructure plans.

Editorial Select

- NASA now routes 73.5% of its budget through almost 5,000 commercial partners, which is basically speeding up the privatized space development.

- SpaceX’s Human Landing System contract rose to about USD 4.04 billion, with a maximum ceiling around USD 4.47 billion.

- The industry expanded from USD 371 billion in 2020 to USD 630 billion in 2025, driven by satellite broadband networks, commercial launches, and post-pandemic recovery.

- Growth is expected to continue, reaching USD 670 billion in 2026 as operational Starship flights begin and USD 740 billion by 2028 with the deployment of the Kuiper constellation.

- By late 2025, NASA had already paid USD 2.67 billion, or 66% of the HLS contract’s overall value.

- Blue Origin’s lunar lander effort is mixing USD 3.4 billion in NASA support with USD 3.4 billion from private investment, making it a USD 6.8+ billion package.

- In FY2023 alone, NASA’s top 20 contractors collected USD 14.78 billion in awards just by themselves.

- Worldwide commercial space activity reached a record 329 orbital launch attempts in 2025.

- U.S. companies wrapped up 206 commercial launches in 2025, which is the top annual total ever recorded.

- SpaceX kind of did 165 Falcon missions in 2025, which ended up being more than half of all worldwide orbital launches.

- On the market side, the global launch services segment was around USD 14–18 billion, and it’s been climbing roughly 15–19% CAGR.

- Starlink then crossed the 10,000 active satellites line, and it also expanded to something like 10.3 million subscribers spanning 164 countries.

- In 2025, Starlink’s revenue was USD 11.39 billion, and in 2026, projections are getting close to USD 20 billion.

- The global space economy hit USD 626 billion in 2025, and it’s projected to go beyond USD 1 trillion by 2040.

Space Industry Market Size

| Year | Market Size | Milestone |

| 2020 | $371B | Pre-Starlink scaling |

| 2022 | $424B | Post-COVID recovery |

| 2024 | $508B | Constellation deployments accelerate |

| 2025 | $630B | Current baseline |

| 2026 | $670B (est.) | Starship operational flights begin |

| 2028 | $740B (proj.) | Kuiper constellation online |

| 2030 | $950B (proj.) | Commercial space stations operational |

| 2035 | $1.8T (proj.) | Lunar economy emerging |

(Source: spacenexus.us)

- The growth trajectory of the global space industry from 2020 to 2035, highlighting key market milestones and future projections.

- The industry expanded from USD 371 billion in 2020 to USD 630 billion in 2025, driven by satellite broadband networks, commercial launches, and post-pandemic recovery.

- Growth is expected to continue, reaching USD 670 billion in 2026 as operational Starship flights begin and USD 740 billion by 2028 with the deployment of the Kuiper constellation.

- By 2030, the market could approach USD 950 billion, supported by commercial space stations. Looking further ahead, the sector is projected to reach USD 1.8 trillion by 2035.

- NASA’s lunar strategy in 2026 is getting more and more shaped by commercial partnerships, not so much by government-owned systems.

- With a USD 24.44 billion FY2026 budget in place, the agency now routes roughly 73.5% of what it spends each year through agreements and contracts with something like nearly 5,000 businesses, universities, and nonprofit organizations.

- A big piece of that shift is the Human Landing System, or HLS program. Back in 2021, SpaceX landed an initial USD 2.89 billion deal for a lunar lander, then later that agreement grew by USD 1.15 billion, so the overall figure sits around USD 4.04 billion, with a ceiling near USD 4.47 billion.

- By the end of late 2025, NASA had already paid out USD 2.67 billion, which is 66% of the total contract, and this happened after 49 program milestones were completed.

- The competitive angle also got wider. Blue Origin won a separate HLS contract worth USD 3.4 billion in 2023 and then added another USD 3.4 billion in private support, so together that becomes well over USD 6.8 billion in combined investment.

- The Commercial Lunar Payload Services (CLPS) program keeps showing NASA’s fixed- price style. At first, it was capped at around USD 2.6 billion, but that ceiling got pushed up to about USD 4.2 billion by 2026.

- By late 2025, NASA had already handed out roughly USD 1.5 billion across 12 lunar missions, and you can see investment nearing USD 2.6 billion, which feels pretty concrete.

- Looking ahead, NASA’s CLPS Phase 2 roadmap, in the next ten years, is aiming at 77 lunar lander missions with an estimated budget of around USD 6 billion.

- The whole idea is to bring the typical mission spend down from about USD 129 million to closer to USD 91 million per mission. That shift, from one price point to another, is the point, really.

- Estimates for the global space economy put the sector at USD 626 billion in 2025, and then forecasts go beyond USD 1 trillion by 2040. NASA’s commercial lunar efforts are being treated more and more like baseline infrastructure for all that later expansion.

- The agency leadership also claims that loosening traditional contractor reliance could trim costs by roughly USD 1.4 billion each year, not just once.

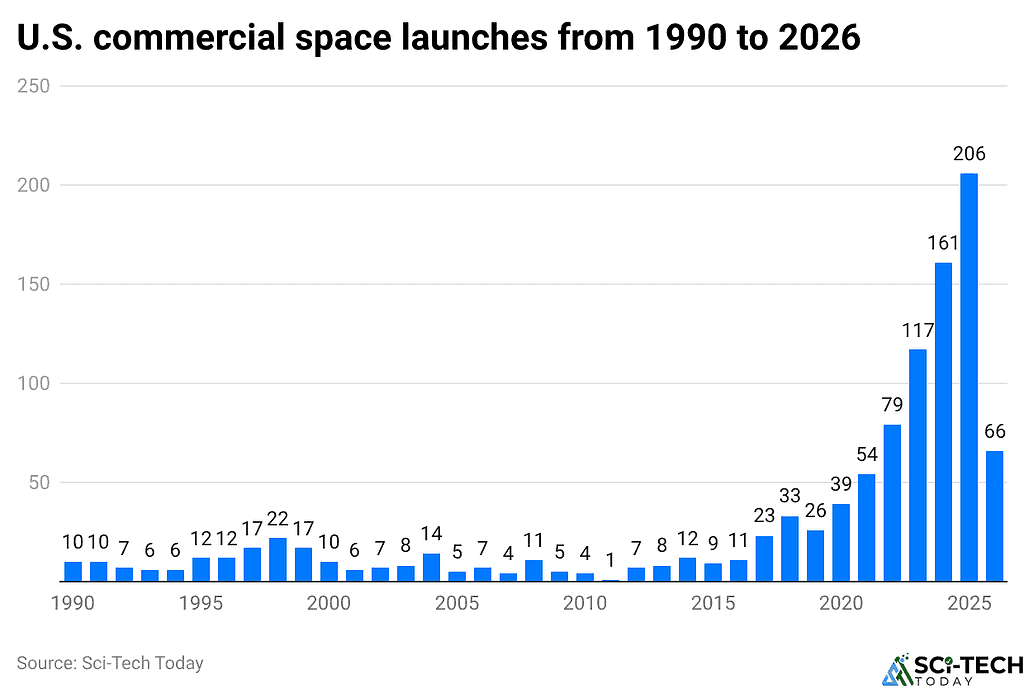

U.S Launch Boom – Commercial Spaceflight Reaches New Heights

(Reference: statista.com)

- The U.S. commercial space industry keeps moving forward at a pretty remarkable pace.

- In 2025, American companies did 206 commercial rocket launches, which is the highest annual total this century, and it really shows how fast private-sector space activity is growing.

- That same momentum is still going into 2026, with 66 commercial launches already finished by April 27, just like that. The numbers basically underline how much the market has changed in the last decade.

- Cheaper launch pricing and tougher rivalry have helped produce a noticeable rise in how often launches happen, so commercial spaceflight went from something small and specific to a real industrial marketplace.

- Firms like SpaceX, Blue Origin, and Rocket Lab have been important players, and they’ve helped the United States keep its position as the worldwide frontrunner in commercial launch activity.

Commercial Space Industry Launch Services

- The global launch services market hit about USD 14–USD 18 billion in 2025–2026, and it’s expanding at roughly a 15–19% CAGR, which makes it the quickest-growing big segment by percentage.

- During 2025, more than 329 orbital launch tries were logged worldwide, setting a new record.

- The United States accounted for most of that, by a wide margin.

- SpaceX specifically ran 165 Falcon 9/Heavy missions in 2025, which is over half of the global orbital launches by count, and it also lines up with about 65% of the mass delivered into orbit.

- In May 2026, SpaceX’s Starship reached a big milestone and managed its first fully commercial orbital payload delivery, not a test-by-default, deploying a 22-tonne Intelsat geostationary satellite.

- Both the Super Heavy booster and the Starship upper stage pulled off landing successfully, too. That outcome basically, officially moved Starship out of a development program and into a revenue-making commercial platform.

- Rocket Lab, the world’s second most prolific commercial launch provider, kind of set a company record in 2025 with 21 Electron launches, plus 100% mission success, and they said full-year revenue came in at USD 602 million, which is 38% growth year over year. They also noted a record backlog of USD 1.85 billion.

- Along the way, the firm landed a USD 816 million prime contract from the Space Development Agency to make 18 defense satellites, which sort of shows it is now a credible national security prime, not just a subcontractor or something.

- Meanwhile, Blue Origin’s New Glenn got to its third launch in April 2026, but then in May 2026, it had a static-fire explosion, which damaged the LC-36 launch pad, so now the plan is to get it back in flight before year-end.

Government Space Budgets By Country

(Source: orbitalradar.com)

- The commercial space world is getting more centered, more piled up among just a few global powers, and the United States still holds a big and almost commanding position, with USD 19.7 billion in the commercial space market.

- China is right on its heels at about USD 19.9 billion, showing how competition is sharpening between the world’s two biggest space economies, like, in a real way.

- After those two, the market kind of falls off a cliff in scale, not slowly. Japan is in third place at USD 4.9 billion, then France comes in at USD 4.5 billion, and Russia is at USD 3.4 billion.

- In Europe, Germany brings USD 2.7 billion, while Italy adds USD 2.3 billion. That sort of reinforces the idea that Europe is a major actor, but also a bit fragmented.

- Also, emerging markets are not waiting around. India’s commercial space sector sits at USD 1.9 billion, putting it among the top space economies, and it seems to mirror the way its launch ability is increasing, plus the private sector is getting more involved.

- The United Kingdom contributes USD 1.5 billion, and then South Korea at USD 0.7 billion, with Canada close behind at USD 0.6 billion; they pretty much round out the leading group.

- Taken together, these numbers show a highly concentrated industry, where the United States and China cover most of the commercial space activity.

- At the same time, places like India, South Korea, and Canada are steadily enlarging their role, suggesting the next decade may produce a wider and more competitive global space marketplace.

The LEO Gold Rush Megaconstellations and Broadband Dominance

- Low Earth Orbit (LEO) satellite systems are turning into the fastest-growing part of the commercial space industry.

- The worldwide LEO broadband market was valued somewhere between USD 8.4 billion and USD 9.8 billion in 2025, and it’s forecast to climb to about USD 47.2–USD 55.4 billion by That translates to a strong 18–20% compound annual growth rate (CAGR), which is not small at all.

- At the center of this transformation is SpaceX Starlink, which in March 2026 passed the mark of 10,000 active satellites, and by June 2026, it had grown to 10,397 operational satellites out of 10,413 in orbit.

- Throughout that stretch, the system kept an operational reliability rate that stayed over 99.9%, more or less. Today, Starlink basically makes up around 75% of all active, maneuverable satellites in Earth orbit.

- The deployment level is honestly not really comparable. Since SpaceX launched its first 60 satellites back in 2019, it has now put 11,901 satellites into orbit, with over 10,300 still operational.

- The user side has moved too; subscriber counts reached about 10.3 million users spread across 164 countries by Q1 2026, which is up from 4.4 million subscribers just a year earlier.

- Money-wise, Starlink brought in USD 11.39 billion in connectivity revenue in 2025, representing 61% of SpaceX’s overall revenue.

- Looking ahead, analysts are projecting USD 20 billion in revenue and USD 14 billion in EBITDA for 2026.

- On the production side, manufacturing capacity has scaled past 4,000 satellites per year, which is the highest rate ever achieved for a single spacecraft product line, at least in this context.

- Competition is starting to appear, but it still feels really behind. Amazon Leo, which used to be called Project Kuiper, had roughly 200 operational satellites in 2026, while Starlink is sitting at 10,000+.

- Amazon also committed more than USD 10 billion for the rollout and finished an USD 11.6 billion acquisition of Globalstar.

- Meanwhile, Eutelsat OneWeb runs a completed constellation of about 648 satellites, focused on connectivity services for enterprise and government customers.

- The above figures point to a pretty obvious direction: LEO mega-constellations are shifting from experimental space efforts into a multi-billion-dollar telecommunications backbone, and in practice, this creates one of the largest commercial openings in the entire global space economy.

Commercial Space Titans

- The commercial space industry is getting increasingly dominated by just a handful of companies, as they’re basically deciding the rules for valuation, revenue production, and overall operational scale. In 2026, SpaceX shows up as the sector’s defining company.

- IPO raised USD 75 billion at USD 135 per share, which put the company’s valuation around USD 1.8 trillion. Within 24 hours of trading, the stock slipped up to USD 160.95, and its market capitalization pushed past USD 2 trillion.

- Before the IPO, filings estimated annual revenue at more than USD 15 billion, while management pointed to an addressable market of nearly USD 28.5 trillion.

- Rocket Lab company pulled in USD 602 million in FY2025 revenue, that’s 38% year over-year growth, not small at all. Space Systems accounted for 67% of total revenue, while launch services made up the remaining 33%.

- On the execution side, Rocket Lab completed 21 Electron missions in 2025 with a 100% mission success rate, and that really reinforces its edge in small satellite launches.

- Iridium is still, arguably, one of the more financially steady operators in the whole area. The satellite communications company produced USD 831 million in FY2024 revenue, backed by its worldwide network supporting IoT, machine-to-machine communications, and satellite voice services.

- Then, in Earth observation, Planet Labs delivered record results with USD 73.4 million in Q1 FY2026 revenue, a 20% annual increase.

- The imaging network continues to watch the entire Earth’s landmass daily. Meanwhile, BlackSky generated approximately USD 102 million in FY2024 revenue, while Spire Global expanded its presence across weather intelligence and maritime analytics markets.

- Together, these figures highlight an industry transitioning from experimental growth to large-scale commercial maturity, with trillion-dollar valuations, billion-dollar revenues, and increasingly diversified business models driving the next phase of the global space economy.

- Sources: SpaceX IPO Filings (2026), Rocket Lab FY2025 Results, Iridium FY2024 Annual Report, Planet Labs Q1 FY2026 Earnings Report, BlackSky FY2024 Financial Results, Spire Global Corporate Reports.

Conclusion

The commercial space industry has kind of turned into one of the world’s most fast-moving technology areas, pushed by record launch activity, more and more satellite networks, government and private cooperation that keeps growing, plus the pretty steep decline in how much it costs to reach space in the first place.

Firms like SpaceX, Blue Origin, Rocket Lab, Planet Labs, and Iridium are basically reworking the economics of space using scalable business models, and some revenue streams that are getting much more varied over time. The big, almost explosive, pace of LEO broadband constellations, the new wave of lunar commercialization plans, and the rise of reusable rockets all point to a shift away from mostly exploration-only missions and toward something closer to sustainable commercial infrastructure.

And as the global space economy moves toward that trillion-dollar milestone, commercial operators are becoming the main drivers of new ideas and longer-term growth, in a way that’s hard to ignore.

FAQ

The global space economy sits at about USD 626 billion.

American companies carried out a record 206 commercial launches.

Starlink has more than 10,000 active satellites in orbit.

It should reach roughly USD 47–55 billion by 2034.

SpaceX is in the lead, with 165 launches in 2025, and that’s over half of the global orbital missions.