Introduction

Earth Observation Satellite Statistics: Earth Observation (EO) satellites have become one of the fastest-growing parts of the global space economy, and they deliver the kind of data that people rely on for climate monitoring, agriculture, defense intelligence, disaster response, infrastructure planning, and environmental sustainability.

This whole shift is kind of fueled by the mix of lower launch costs, smaller satellite tech, artificial intelligence, and cloud-based geospatial analytics, so deployment of EO satellite constellations is happening more quickly across the planet. By 2026, governments and commercial operators are putting significant money into high-resolution imaging, synthetic aperture radar (SAR), and hyperspectral systems, mostly because demand for real-time Earth intelligence keeps rising. Because of that, Earth observation satellites are moving away from just image-capturing platforms and toward AI-powered decision support systems that serve both public agencies and private organizations.

This article will show the recent Earth observation satellite statistics and their market performance.

Editor’s Choice

- The global Earth Observation (EO) satellite market is projected to grow from USD 4.3 billion in 2025 to USD 8.3 billion by 2035, so it is about double in overall value.

- A fairly steady 7.0% CAGR through 2035 suggests more and more reliance on satellite- driven geospatial intelligence, not just occasional use.

- North America leads with 46.9% of global EO revenue, and that’s roughly USD 2.0 billion in 2025.

- Satellite-based EO systems hold 67.8% market share, so space assets remain the backbone for Earth monitoring in practice.

- Low Earth Orbit satellites take 78.2% of the market, making LEO the most chosen orbit for high-frequency imaging sessions.

- Optical imaging stays on top with 51.7% market share, remaining the industry’s main observation technology, for now.

- EO satellite launches are expected to rise from 22 spacecraft in 2015 to 349 by 2029, almost a 16-fold increase, which is pretty big.

- The industry is expected to deploy 1,158 new EO satellites between 2026 and 2029, highlighting an unprecedented expansion cycle.

- Current EO systems generate approximately 50 terabytes of data daily, while the Sentinel fleet alone produces 20,000+ GB every day.

- Government and defense agencies account for 48% of global EO spending, making national security one of the industry’s largest growth drivers.

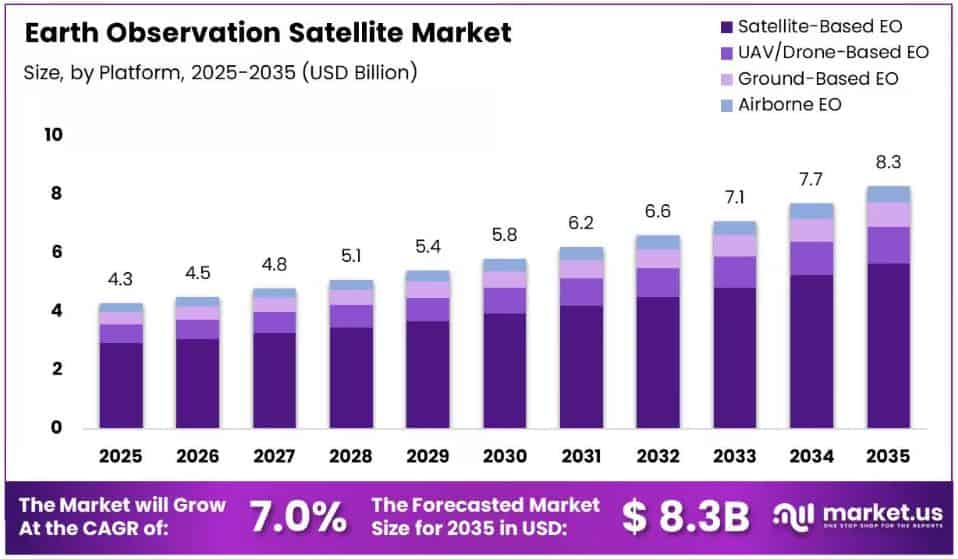

Earth Observation Satellite Market

(Source: market.us)

- The Earth Observation (EO) satellite sector seems to be sliding into a steady, kind of sustainable expansion phase.

- Overall, the global market was put at USD 4.3 billion in 2025, and it is expected to climb to roughly USD 8.3 billion by 2035, showing a healthy 7.0% compound annual growth rate (CAGR) through the 2026–2035 forecast window.

- On the regional side, North America is still the undisputed market leader, without much debate. In 2025, it brought in 46.9% of total global revenue, which is around USD 2.0 billion.

- The kind of lead comes from the strong footprint of government space programs, commercial satellite operators, and an overall mature Earth observation infrastructure in the area.

- When you look at platform segmentation, Satellite-Based Earth Observation systems held 67.8% of the global market share in 2025, and that suggests space-based monitoring remains the primary way to gather large-scale environmental and geospatial data.

- This position also points to a bigger dependence on satellite networks for near-real-time viewing and analytics, not just occasional imagery.

- Low Earth Orbit (LEO) satellites made up 78.2% of the market in 2025, so they’re the dominant orbital choice. Their capability to provide higher resolution imagery and more frequent revisit intervals has nudged LEO into the preferred place for current Earth observation missions.

- Optical Imaging kinda stayed the biggest slice, sitting at 51.7% of the total market share in 2025.

- Optical sensors, basically, keep acting as the backbone for Earth observation work, giving detailed visuals for environmental analysis and also monitoring use cases.

- On the applications side, Environmental Monitoring showed up as the leading use case, taking 21.5% of the market share in 2025. That outcome mirrors a growing appetite for satellite-based tracking of climate behaviors, ecosystems, natural resources, and those ongoing shifts across the environment.

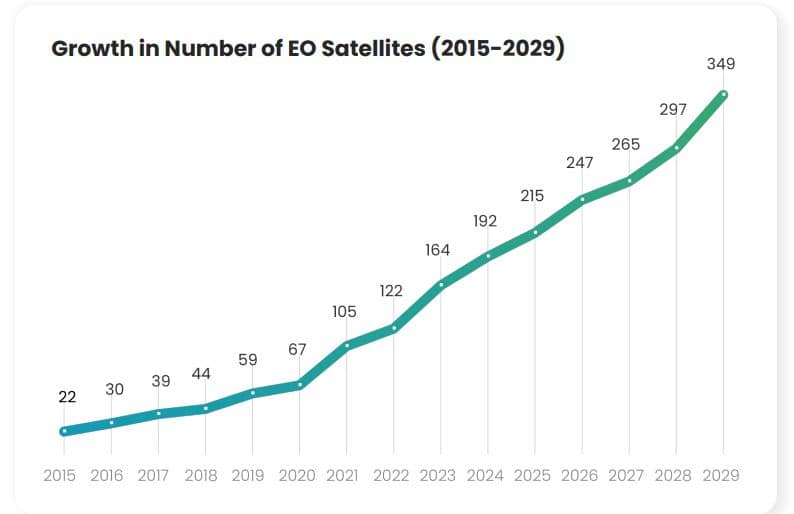

Rapid Expansion Of Earth Observation Satellites And Data-Driven Growth

(Source: Copernicus.eu)

- The Earth Observation (EO) satellite industry is currently in one of the strongest expansion cycles across the space sector.

- The data points to a very noticeable jump in deployment speed, moving from only 22 EO satellites launched in 2015 to 215 launched in 2025.

- Growth is also accelerating through 2026, with an estimated 247 launches. Looking ahead, projections suggest 265 satellites in 2027, 297 in 2028, and 349 by 2029.

- In relative terms, it is almost a 16-fold jump versus 2015, which underscores how fast the demand is scaling for satellite-enabled Earth monitoring capability.

- Over the next four years (2026–2029), around 1,158 Earth Observation satellites are expected to be launched worldwide. This big rollout wave indicates how governments and commercial operators are putting a lot of money into space-based imaging, surveillance, and analytics infrastructure, all together.

- The data suggests that 44 countries have plans to launch Earth Observation constellations over the next four years, kind of reflecting this growing strategic importance of EO capabilities across both developed and emerging space nations.

- At the same time, 72 companies either operate or plan to develop EO constellations, which also points to how much bigger the private-sector involvement is getting in that market.

- Today’s EO systems, including Sentinel, Landsat, and PlanetScope, together generate an estimated 50 terabytes of data every day. That massive data flow is quietly, but definitely, transforming industries from agriculture to environmental monitoring, and even disaster management and urban planning, too.

- In general, you can see it in more satellite deployments, more international participation, more commercial momentum, and a kind of unprecedented jump in daily geospatial data generation.

Edge Computing and Onboard AI Processing

- One of the bigger challenges the Earth observation industry faces in 2026 is no longer collecting data; it is transmitting it.

- Modern satellites generate information at very high rates, while communication links struggle to match that pace.

- The European Copernicus programme says the Sentinel satellite fleet alone produces more than 20,000 gigabytes of new Earth observation data every day, which is putting real strain on ground stations and downlink capacity.

- As imaging systems move toward better spatial, spectral, and temporal resolution, the production of data is growing far faster than transmission bandwidth can handle.

- Rather than sending whole datasets back to Earth, satellites are increasingly processing information right where it happens, in orbit.

- Research suggests that contemporary onboard computing platforms can handle dozens, even hundreds, of AI models at the same time.

- Some edge computing setups can run more than 100 AI algorithms in real time, so satellites can spot the meaningful events first and throw away the lower-value readings before transmission.

- Technical checks point out that merging AI-driven filtering, region-of-interest extraction, and smart, compressed representations can cut the usable downlink demand by a factor of ten, or even more.

- Put simply, missions that used to require tens of terabytes of raw imagery each day can now transmit smaller gigabyte-scale intelligence outputs instead. That means less pressure on bandwidth and usually faster response, less waiting in the loop.

- For instance, ESA’s OPS-SAT mission reported onboard deep-learning systems reaching better than 95% classification accuracy while also autonomously detecting anomalies in space.

- Further experiments indicate that AI inference can run with something like millisecond-to-second latency on radiation-hardened hardware, which supports near-real-time decisions during a single imaging pass, not hours later or whenever the downlink finishes.

- Earth observation operators are moving more and more toward “analytics-as-a-service” models, which means they deliver actionable intelligence rather than raw imagery, as you would have a decade ago.

- AI-powered satellites can help prioritize wildfire alerts, maritime anomalies, crop stress indicators, infrastructure changes, and environmental monitoring products, ensuring that only the most critical information reaches users first, or at least sooner than everything else.

- With satellites generating 20,000+ GB of data daily, supporting 100+ onboard AI algorithms, achieving 95%+ anomaly detection accuracy, and reducing transmission volumes by 10× or more, edge AI is rapidly becoming a foundational technology for next-generation Earth observation systems.

- As satellite constellations continue to expand, intelligent in-orbit processing is evolving from an innovation into a necessity for managing the growing flood of space-based data.

Dual-Use Technology – Defense and Commercial Synergies

- The Earth observation (EO) industry is undergoing a major transformation, driven by growing defense and intelligence demand, and honestly, it shows.

- Today, government and defense organizations account for approximately 48% of global Earth observation spending, making public-sector agencies one of the most important customers for commercial satellite operators. This shift highlights how national security budgets are increasingly supporting the growth of private satellite constellations and geospatial intelligence services.

- A key driver behind this trend seems to be the swift take-up of commercial Synthetic Aperture Radar (SAR) imagery.

- Instead of relying on traditional optical satellites, SAR systems can capture scene details through clouds, smoke, and even darkness, so it ends up being quite useful for intelligence, surveillance, reconnaissance, border monitoring, maritime awareness, and disaster response.

- Industry studies tend to point toward defense and intelligence agencies as the biggest and earliest people buying into commercial SAR services, which then keeps pressure on demand for high-resolution radar imagery for a long time.

- Official NRO documentation says that in 2022, the U.S. National Reconnaissance Office (NRO) announced what it called its largest-ever commercial imagery acquisition push via the Electro-Optical Commercial Layer (EOCL) program.

- Under that framework, contracts worth billions of dollars were awarded over the next decade to major providers like BlackSky, Maxar, and Planet.

- The setup includes a five-year base period, plus extension options that may run through 2032, so commercial operators get longer-term revenue sightlines and the kind of investment confidence that helps them plan.

- Further, NRO documentation states that EOCL enables imagery distribution to hundreds of thousands of users across defense, intelligence, and civilian agencies.

- At the same time, commercial operators are also treating these agreements as leverage to fund next-generation satellite fleets, advanced analytics platforms, and higher-revisit imaging constellations.

- Planet, for example, offers access to an archive that contains more than 2,000 images for every point on Earth’s landmass since 2009.

- Honestly, this kind of large-scale data is getting more and more important for both defense operations and commercial uses, too.

- At the same time, the broader market outlook seems to be keeping pace. Industry forecasts suggest the commercial Earth observation sector could grow from around USD 7 billion in the mid 2020s to over USD 15 billion by the early 2030s.

- The above figures revealthat 48% of EO spending is tied to government customers, multi-billion-dollar contracts that run through 2032.

- A market expected to go beyond USD 15 billion and then, basically double, defense demand is no longer just “helping” the Earth observation industry. It’s starting to act as one of its main growth engines.

Conclusion

Earth Observation satellites kind of became must-have infrastructure for environmental monitoring, climate research, defense intelligence, agriculture, disaster response, and commercial analytics, and yes, it’s not just a small thing anymore. The sector is seeing steady growth, mostly because more satellites are being deployed, government spending is going up, and people want real-time geospatial intelligence more than ever.

Also, fast improvements in artificial intelligence and edge computing are basically turning satellites from simple data gatherers into smarter decision-support platforms, where information is processed directly in orbit instead of only on the ground. At the same time, defense agencies are pushing market expansion faster, through long-term commercial imagery contracts and geospatial intelligence programs.

So as launch activity keeps climbing, data generation keeps rising, and AI adoption accelerates, Earth Observation satellites are expected to take an even bigger part in shaping global decision-making.

FAQ

The worldwide EO satellite market is estimated to be around USD 4.3 billion in 2025.

Roughly 1,158 EO satellites are forecast to launch globally from 2026 to 2029.

Low Earth Orbit, known as LEO, leads the market with 78.2% share.

Current EO systems together produce about 50 terabytes of data each day.

Government and defense organizations represent approximately 48% of global EO spending.