Introduction

Know Your Customer Statistics: The financial industry operates on a critical balancing act. It is a balance of growth versus risk. On one side, there’s the push for fast, digital client acquisition. On the other, the non-negotiable legal duty to practice Know Your Customer (KYC).

These procedures, which involve verifying a client’s identity and assessing their risk profile, are the primary bulwark. They protect against money laundering, terrorism financing, and fraud. The data shows it’s a global financial, operational, and customer experience crisis. It costs billions of dollars. Additionally, millions of clients are lost.

So, we’ve consolidated the most recent and vital statistics to map the full lifecycle of KYC, from its cost burden and the penalties for failure to the power of the technology now being deployed to fix it. Let’s get started.

Editor’s Choice

- The annual operational cost for financial crime compliance, which includes intensive KYC procedures, collectively hits $61 billion across just the United States and Canada alone.

- A single financial firm’s average annual expenditure dedicated purely to AML and KYC operations sits at nearly $72.9 million

- The single most punitive regulatory action involved a $4.3 billion fine levied against a major digital asset platform for admitting significant failures in maintaining an effective AML program and implementing essential KYC

- North American regulators have dramatically intensified enforcement, accounting for an overwhelming 94% of the $4.6 billion in total global financial penalties issued in 2024.

- For corporate clients, the complex, manual process of a KYC review can cost between $1,500 and $3,000 for more than half (54%) of institutional banks, proving the cost inefficiency of traditional methods.

- The failure to deliver a seamless client experience is costly, as a high 70% of banks worldwide report actively losing potential clients due to slow or inefficient onboarding processes directly tied to KYC

- This operational lag results in an average client abandonment rate of approximately 10% during the initial application stage.

- The entire process of completing an initial KYC review for a new corporate entity takes an average of 95 days.

- Compliance efficiency remains low, with only about 33% of periodic, ongoing KYC reviews currently being fully automated.

- The global KYC software market is expected to reach approximately $5.89 billion by 2031, projecting a robust Compound Annual Growth Rate (CAGR) of 2%.

- Financial institutions are using AI and automation to target massive cost reductions of up to 50% across their entire KYC value chain.

- When fully automated solutions are deployed, the time required for new customer onboarding has been shown to decrease dramatically by as much as 87%.

- The adoption of advanced AI tools in KYC and AML operations has surged significantly, now utilized by over 82% of financial institutions globally.

The Cost of KYC Compliance

(Reference: coinlaw.io)

(Reference: coinlaw.io)

- The collective annual cost for financial crime compliance across just the United States and Canada has hit $61 billion.

- Looking across the pond, the cost burden is even higher, with the total annual compliance expenditure for firms operating in Europe, the Middle East, and Africa (EMEA) reaching approximately $85 billion.

- The average annual expenditure on combined AML and KYC operations for a single financial institution sits at nearly $72.9 million globally.

- For mid and large-sized institutions holding over $10 billion in assets, 82% report experiencing the highest cost escalations specifically for compliance technology, including advanced KYC software.

- Compliance teams often spend an estimated 40% to 60% of their total time managing regulatory data and fulfilling mundane manual tasks, severely limiting their capacity for high-value financial crime investigation.

- The cost of completing a KYC review for a single corporate client is substantial, costing between $1,500 and $3,000 for over half (54%) of all corporate and institutional banks.

| Statistic | Details on the Operational Drain |

| $61 Billion |

Annual financial crime compliance cost in the US & Canada. |

|

$85 Billion |

Annual financial crime compliance cost in EMEA. |

| $72.9 Million |

Average annual spend on AML/KYC per financial firm. |

|

54% of Banks |

Pay $1,500 to $3,000 per corporate KYC review. |

| 82% of Large Firms |

See the highest cost increases in KYC technology spending. |

The Financial Risk of KYC Non-Compliance

(Reference: trimplement.com)

(Reference: trimplement.com)

- In 2024, the total value of global financial penalties reached $4.6 billion, with fines being levied against institutions across all sectors, including traditional banks, digital asset platforms, and gaming operators.

- A stunning 94% of the $4.6 billion in global financial penalties imposed in 2024 originated from North American regulatory actions.

- The single largest fine in recent history was the $4.3 billion penalty paid by a major digital asset platform in 2023.

- A major UK bank was recently fined over £107 million by the Financial Conduct Authority (FCA) for “significant and prolonged weaknesses” in its KYC and Customer Due Diligence (CDD) controls.

- Enforcement actions specifically related to transaction monitoring breaches, which directly stem from poor customer understanding established during KYC onboarding, surged sharply, with penalties exceeding $3.3 billion globally in a recent period.

- In one recent year, penalties issued to banks globally saw an alarming increase of 522%, reaching $3.65 billion.

| Statistic | Details on Regulatory Penalties |

| $4.6 Billion | Total global financial penalties in 2024. |

| 94% of Fines | Attributed to North American regulatory actions in 2024. |

| $4.3 Billion | Largest single fine for KYC/AML failures against a digital asset firm. |

| 522% Increase | In penalties issued to banks globally in a recent year. |

| £107 Million | Fine imposed on a single UK bank for KYC/CDD weaknesses. |

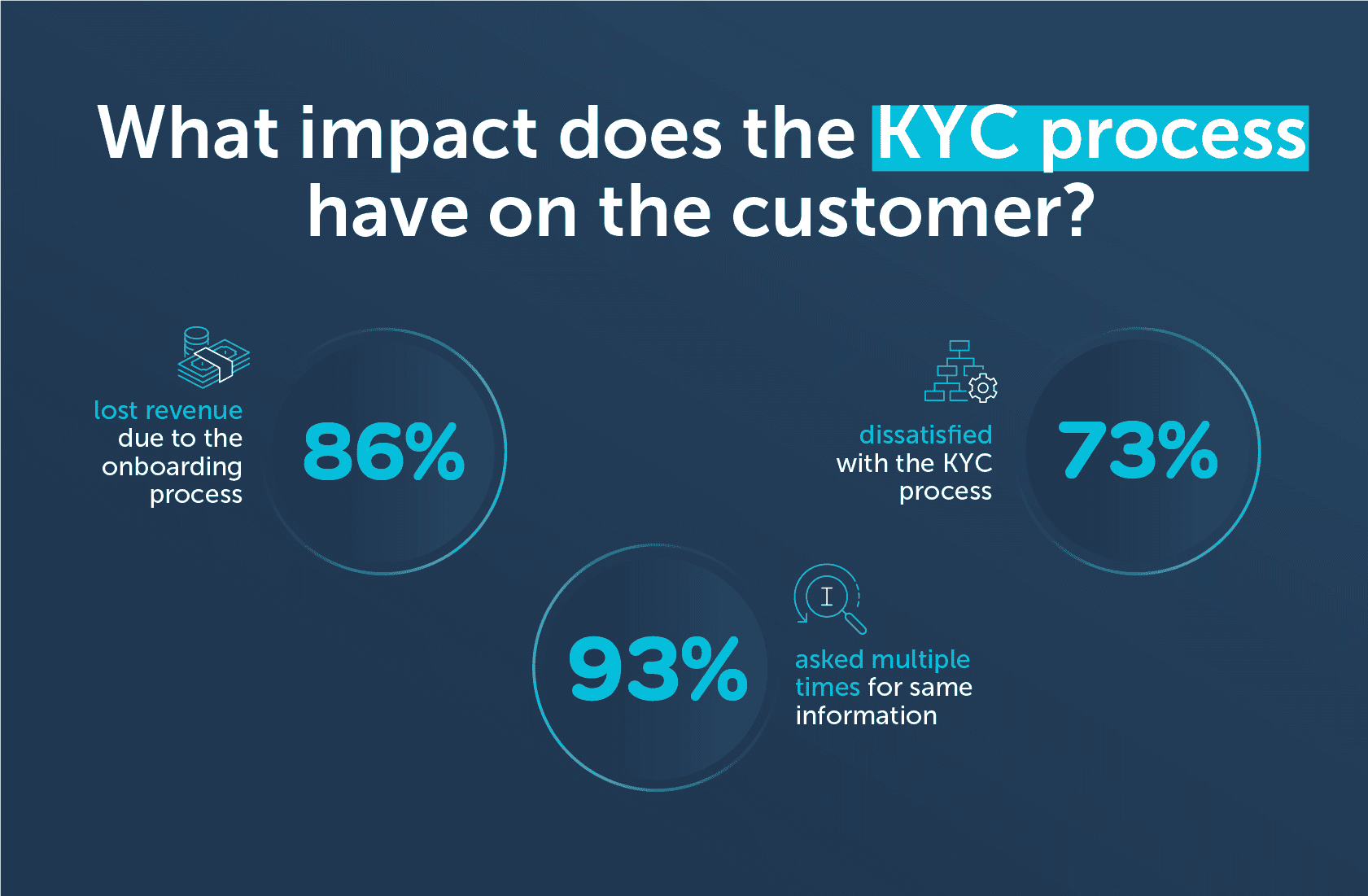

KYC and the Customer Journey

(Source: encompasscorporation.com)

(Source: encompasscorporation.com)

- A substantial 70% of banks worldwide report actively losing clients due to sluggish, inefficient onboarding processes.

- The average client abandonment rate during the application process is approximately 10%.

- The process for completing an initial KYC review for a new corporate client can take an average of 95 days, a period of over three months, up from an average of 84 days in the previous year

- For individuals, manual KYC processes relying on paperwork and slow identity checks can take over 18 minutes per customer.

- Globally, only an estimated 33% of periodic KYC reviews are fully automated, meaning the vast majority of ongoing client diligence still relies on labor-intensive, time-consuming manual efforts.

- 79% of banking executives point to manual KYC processes as the single biggest bottleneck that actively disrupts the customer experience and actively slows down core business operations.

| Statistic | Details on Customer Churn and Experience |

| 70% of Banks | Lose clients due to slow onboarding/KYC processes. |

| 10% | Average client abandonment rate during onboarding. |

| 95 Days | Average time to complete an institutional KYC review. |

| 18+ Minutes | Time required for a manual individual KYC check. |

| 33% | The low percentage of fully automated periodic KYC reviews. |

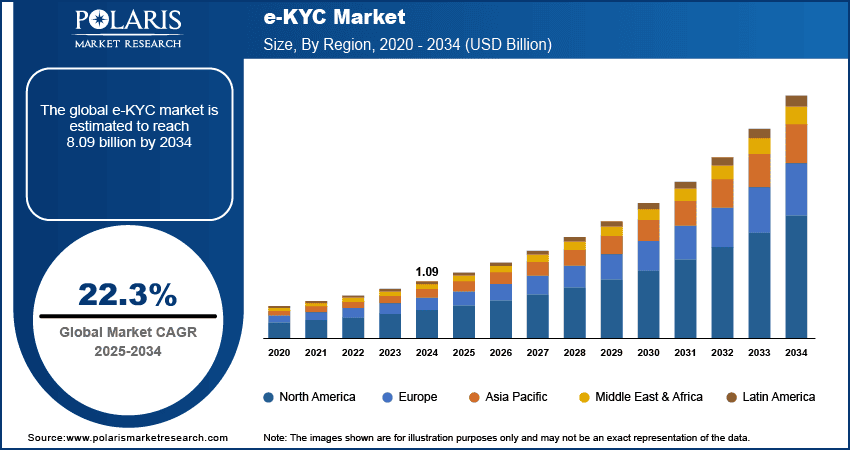

The Market Growth for KYC Technology

(Source: polarismarketresearch.com)

(Source: polarismarketresearch.com)

- The global KYC software market was valued at an estimated $2.35 billion in 2024 and is projected to skyrocket to approximately $5.89 billion by 2031.

- The broader Electronic-Know Your Customer (e-KYC) market is seeing even faster acceleration, with forecasts projecting a massive 22.3% CAGR between 2025 and 2034.

- The BFSI (Banking, Financial Services, and Insurance) sector remains the single largest end-user segment for KYC software, accounting for over 40% of the global market revenue.

- In terms of regional dominance, North America continues to hold the largest market share for e-KYC solutions, primarily due to the high volume of complex financial transactions and the high demand for advanced fraud detection capabilities.

- However, Asia Pacific (APAC) is projected to be the fastest-growing region due to rising regulatory awareness.

- Over 91% of financial institutions attribute high client abandonment rates not to the regulation itself, but to poor data management and fragmented, siloed workflows, indicating that technology integration and data orchestration, not just simple identity verification, are the core problem.

- A significant 38% of financial institutions have already planned or committed to implement AI-driven solutions to directly streamline compliance workflows, enhance data verification accuracy, and reduce the crippling delays associated with manual KYC processes.

| Statistic | Details on Technology Market Growth |

| $2.35 Billion | Estimated size of the KYC Software Market in 2024. |

| $5.89 Billion | Projected size of the market by 2031 (CAGR 14.2%). |

| 22.3% CAGR | The growth rate is projected for the e-KYC market (2025 to 2034). |

| 40% of Revenue | Share of the BFSI sector in the global KYC market. |

| 91% of Firms | Blame poor data management for high client abandonment. |

The Future of KYC and Automation

(Reference: complycube.com)

(Reference: complycube.com)

- Financial institutions like NeoBank, adopting AI technologies, are currently targeting cost reductions of up to 50% across their entire KYC value chain.

- KYC automation solutions have demonstrably reduced manual labor costs by up to 70% in various institutions.

- The time required for new customer onboarding has seen a radical transformation, with specific case studies showing a reduction in processing time by as much as 87%.

- AI-powered systems can generate a fully compliant, verified customer risk profile in less than 60 seconds, in stark contrast to the 18 minutes for a manual individual check or the 95 days for a corporate review.

- The use of advanced AI tools in AML and KYC operations has seen a massive surge, jumping from 42% of firms to over 82% in recent years, with Singaporean firms leading adoption at a high of 92%.

- One of the most immediate benefits of ML deployment is the reduction of false positives by up to 50%, allowing compliance analysts to focus only on genuine high-risk alerts.

| Statistic | Details on AI and Automation Impact |

| 50% Cost Reduction | Targeted by banks using AI in KYC processes. |

| 70% Reduction | Savings on manual labor costs via KYC automation. |

| 87% Reduction | Reduction in customer onboarding time with automation. |

| 82% of Firms | Current adoption rate of advanced AI tools in KYC and AML. |

| 60 Seconds | Time to create a fully verified, compliant risk profile with AI. |

Conclusion

Overall, the manual paper-driven KYC is rapidly drawing to a close, driven out by unsustainable costs and crushing regulatory penalties. These statistics make the case unavoidable: an annual $61 billion compliance burden and a 10% client abandonment rate are simply no longer financially viable metrics for any serious institution.

The change is underway. With the KYC software market growing at 14.2% and AI promising a 50% cut in operational costs, KYC is transforming. It evolves from a costly, static compliance checkpoint into a dynamic, “Perpetual KYC” system. This system leverages actual data and artificial intelligence to monitor risk 24/7.

This technology-first approach is the only way to manage multi-billion-dollar financial risk. Moreover, it does so without sacrificing the instant experience that modern clients demand. This data proves that for any institution wanting to grow and remain solvent, adopting these intelligent, automated measures is a necessity. It is the changing necessity of the decade. I hope you like this piece of work. If you have any questions, kindly let us know, and we will try to answer ASAP. Thanks for staying up till the end.